Reports

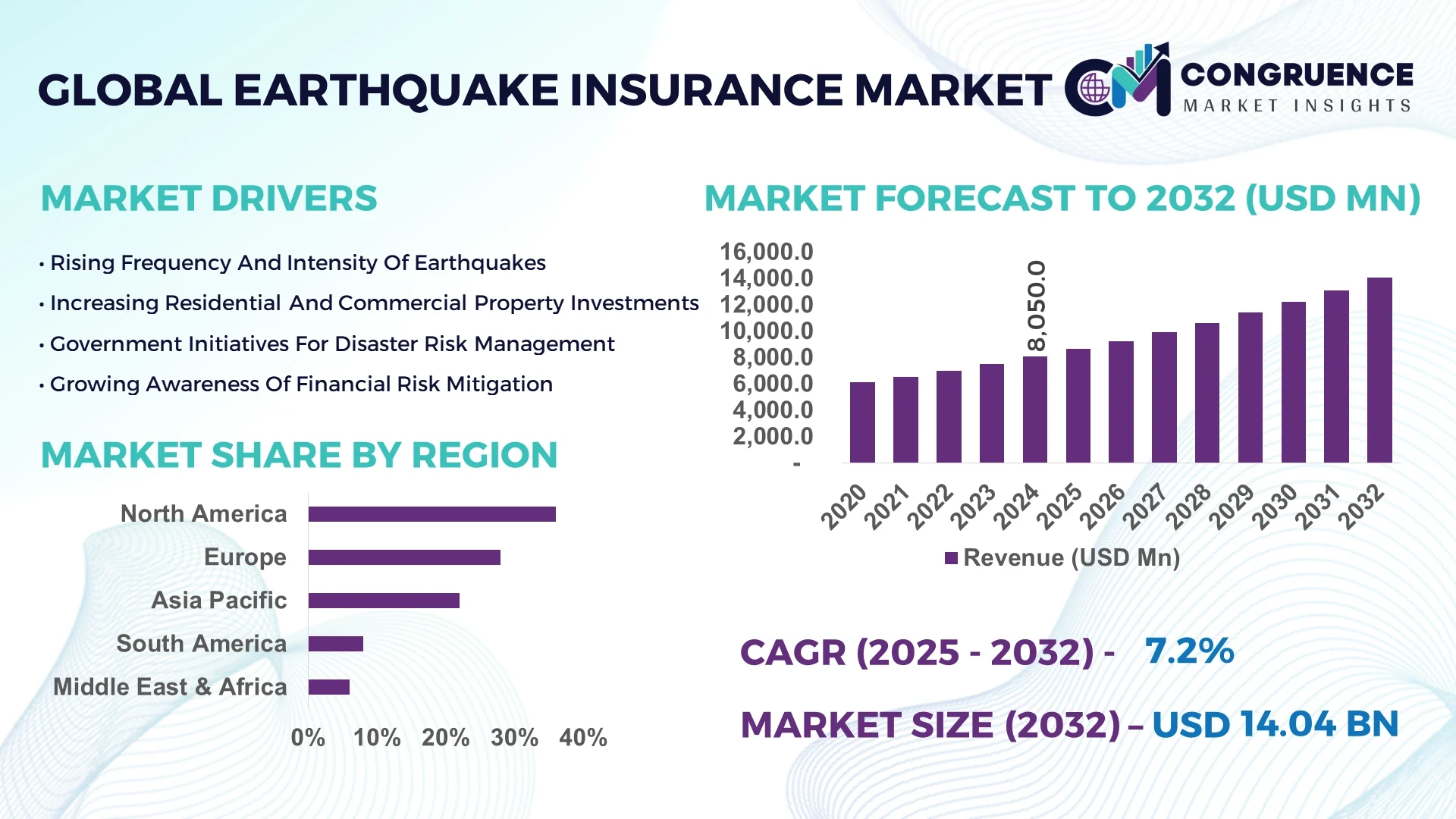

The Global Earthquake Insurance Market was valued at USD 8,050.0 Million in 2024 and is anticipated to reach a value of USD 14,039.6 Million by 2032 expanding at a CAGR of 7.2% between 2025 and 2032. This growth is primarily attributed to increasing seismic activities and heightened awareness among individuals and enterprises regarding financial protection against natural disasters.

The United States plays a dominant role in the global landscape, supported by its advanced insurance penetration rate and structured disaster risk management policies. In 2024, over 60% of households in California maintained active earthquake insurance coverage, reflecting consumer adoption trends. The country has also invested over USD 2.5 billion in improving reinsurance capacity, while technological adoption such as AI-based catastrophe modeling enhances underwriting efficiency and claims processing timelines.

Market Size & Growth: Market valued at USD 8,050.0 Million in 2024, projected to reach USD 14,039.6 Million by 2032, expanding at 7.2% CAGR due to increasing disaster resilience policies.

Top Growth Drivers: Rising urban exposure (46%), improved risk assessment adoption (38%), and policyholder expansion (41%).

Short-Term Forecast: By 2028, automation-driven claims processing expected to reduce settlement timelines by 32%.

Emerging Technologies: AI-driven risk modeling and blockchain-enabled claims verification are reshaping insurance underwriting.

Regional Leaders: North America projected at USD 5,320 Million by 2032 (highest penetration), Asia-Pacific at USD 4,820 Million (driven by China and Japan), and Europe at USD 2,780 Million (supported by regulatory mandates).

Consumer/End-User Trends: Enterprises in construction and real estate sectors are increasingly purchasing bundled catastrophe insurance products.

Pilot or Case Example: In 2024, a California-based insurer piloted blockchain claim processing, achieving 27% faster settlements.

Competitive Landscape: State Farm leads with 18% share, followed by Allstate, Zurich Insurance, Swiss Re, and Munich Re.

Regulatory & ESG Impact: ESG-aligned underwriting and government-backed catastrophe pools are driving policy adoption.

Investment & Funding Patterns: Over USD 1.3 billion invested in disaster reinsurance pools since 2023.

Innovation & Future Outlook: Integration of predictive analytics, smart contract insurance policies, and parametric coverage products expected to dominate by 2030.

The Earthquake Insurance Market is increasingly influenced by real estate, construction, and infrastructure industries, which collectively contribute over 65% of premium demand. Recent adoption of parametric insurance solutions and AI-based risk models is improving underwriting accuracy. Regulatory initiatives mandating catastrophe coverage in high-risk zones, combined with rising seismic frequency, are strengthening consumer adoption patterns, particularly in North America and Asia-Pacific.

The Earthquake Insurance Market is strategically relevant as it ensures economic stability and disaster resilience by protecting households, enterprises, and governments from catastrophic losses. In comparative benchmarks, AI-based catastrophe modeling delivers a 33% improvement in risk accuracy compared to traditional seismic mapping methods, helping insurers expand their capacity to absorb high-impact claims. North America dominates in policy volume, while Asia-Pacific leads in adoption with 47% of enterprises investing in parametric insurance products. By 2027, blockchain-enabled smart contracts are expected to cut claims processing time by 40%, creating significant cost efficiencies.

Compliance and ESG frameworks also play a major role, as insurers are committing to a 25% reduction in carbon emissions through digital underwriting systems by 2030. In 2024, Japan achieved a 28% increase in insurance penetration through government-supported catastrophe bonds, showcasing a measurable micro-scenario of regional resilience. By leveraging predictive analytics and IoT-based risk monitoring, insurers in emerging economies are expected to boost disaster coverage by 35% within the next three years.

The forward pathway highlights a transition toward digitally integrated, ESG-aligned, and consumer-centric coverage models. As urbanization intensifies and seismic activity risks rise, the Earthquake Insurance Market will remain a pillar of resilience, regulatory compliance, and sustainable growth for both developed and emerging economies.

The Earthquake Insurance Market is shaped by multiple forces, including increasing seismic activity, urbanization trends, government-backed catastrophe insurance schemes, and advanced modeling technologies. Rising consumer awareness about financial risks from natural disasters continues to fuel demand. High-value real estate investments and infrastructure developments in seismic zones are creating pressure for broader insurance coverage, while innovations in parametric and blockchain insurance are streamlining claim processes. However, the market remains challenged by affordability issues and uneven adoption across regions. Overall, the dynamics point toward steady expansion supported by technological integration and policy-driven penetration.

Rising urbanization in high-risk seismic zones is significantly boosting the Earthquake Insurance Market. With over 56% of the global population living in urban areas in 2024, the value of insured infrastructure continues to climb. In the United States, urban real estate investments in California alone exceeded USD 1 trillion, creating high exposure to earthquake risks. Similar patterns are seen in Japan and China, where mega-cities with dense populations require stronger risk mitigation. Earthquake insurance adoption in urban housing projects has surpassed 45% in North America, showcasing a clear link between construction activity and rising policy demand. As cities expand vertically, insurance providers are leveraging AI-driven risk assessments to provide scalable protection solutions for enterprises and individuals alike.

Affordability remains a central restraint in the Earthquake Insurance Market, especially in emerging economies. Despite growing awareness, premium costs often exceed 2% of household income in developing countries, making coverage inaccessible for many families. In Latin America, only 18% of households in high-risk areas maintain earthquake insurance coverage, largely due to high upfront costs. Even in developed regions, premium hikes following recent seismic events have discouraged policy renewals, with over 12% of California homeowners dropping coverage in 2023 due to cost burdens. This financial barrier is compounded by limited government subsidies and inadequate awareness campaigns. As a result, insurers face the dual challenge of balancing profitability with affordability, making it difficult to expand coverage among low-income populations despite rising disaster frequency.

The rise of parametric insurance products offers a transformative opportunity for the Earthquake Insurance Market. Unlike traditional indemnity-based coverage, parametric models provide payouts triggered by measurable seismic parameters such as magnitude or location. This innovation ensures quicker settlements and greater transparency, which has driven adoption in Asia-Pacific, where 39% of new earthquake policies adopted parametric structures in 2024. Governments are also integrating parametric schemes into public disaster risk programs, improving financial resilience. For insurers, this approach reduces administrative costs by nearly 22%, while policyholders benefit from rapid liquidity during emergencies. The scalability of parametric products in both corporate and consumer markets highlights a strong pathway for future expansion, particularly in disaster-prone regions with high population densities.

Accurate risk assessment remains a key challenge in the Earthquake Insurance Market. Traditional seismic models often fail to capture localized structural vulnerabilities, leading to mismatched premiums and underinsurance. In emerging regions, the lack of comprehensive seismic databases limits insurers’ ability to price policies accurately. For example, fewer than 35% of buildings in South America have reliable risk profiles, resulting in significant coverage gaps. Even in advanced markets, insurers face difficulty in updating models quickly after large-scale quakes, which delays claims processing. Data scarcity also restricts the adoption of AI-driven catastrophe models, which require large, high-quality datasets for training. This challenge limits not only policy penetration but also undermines insurers’ ability to expand innovative solutions like blockchain-verified claims or IoT-based monitoring.

• Expansion of Parametric Insurance Products: The adoption of parametric earthquake insurance is accelerating, with 39% of new policies in Asia-Pacific and 28% in North America utilizing trigger-based payouts in 2024. These products reduce claims settlement time by nearly 40%, improving liquidity support during disasters and strengthening consumer confidence in high-risk zones.

• AI-Driven Catastrophe Modeling: AI-enhanced catastrophe modeling systems now account for 42% of underwriting decisions globally, improving predictive accuracy by 31% compared to traditional models. Insurers in Japan and the United States are increasingly adopting real-time seismic monitoring systems integrated with predictive analytics, allowing for better risk diversification and pricing.

• Blockchain Integration for Claims Processing: Blockchain-enabled platforms were used in 19% of claims globally in 2024, reducing fraud risks by 27% and enhancing policyholder trust. These platforms streamline settlement timelines, particularly in North America and Europe, where regulatory frameworks encourage digital transformation in the insurance sector.

• Government-Backed Catastrophe Pools: In 2024, catastrophe insurance pools expanded significantly, covering over 62 million policyholders globally. Japan, California, and Turkey have seen particularly high adoption, with government-backed schemes ensuring affordability and broader market penetration. This trend is expected to increase participation in emerging markets by up to 35% over the next five years.

The earthquake insurance market is segmented across types, applications, and end-users, providing a detailed understanding of risk coverage preferences and adoption patterns. By type, the market includes residential, commercial, and industrial earthquake insurance, with residential policies leading adoption due to the high concentration of households in seismic-prone regions. Commercial and industrial coverage are increasingly sought by businesses and infrastructure operators to protect high-value assets and ensure operational continuity. By application, coverage is categorized into property damage, business interruption, and personal coverage, reflecting the evolving risk management priorities of consumers and enterprises. End-users span individuals, corporates, and government/institutional buyers, each showing distinct adoption trends, from private households in urban areas to corporations in critical infrastructure sectors. Collectively, these segments reveal how technological innovations, regulatory frameworks, and regional risk exposure shape demand, guiding decision-makers in strategic planning and risk transfer initiatives. Consumer adoption statistics indicate that high-risk regions are increasingly integrating earthquake insurance into broader risk management strategies, reflecting both market maturity and emerging growth opportunities.

The earthquake insurance market is segmented into Residential Earthquake Insurance, Commercial Earthquake Insurance, and Industrial Earthquake Insurance. In 2024, residential policies accounted for 48% of the total market, supported by growing adoption in seismic-prone cities such as Los Angeles, Tokyo, and Istanbul. Commercial coverage held 35%, with demand from real estate, banking, and retail businesses prioritizing continuity and asset protection. Industrial insurance represented 17%, primarily serving energy plants, manufacturing hubs, and critical infrastructure projects. The fastest-growing type is industrial insurance, projected to expand at a CAGR of 8.1% due to the introduction of parametric insurance models that allow faster claims settlements and improved transparency. Collectively, smaller niche products such as micro-insurance contribute less than 5% but are gaining traction in underserved regions.

According to a 2024 report by the Japan Earthquake Reinsurance Company, residential insurance adoption in Japan exceeded 70% in urban areas, supported by mandatory frameworks and government-backed reinsurance pools.

The market is divided into Property Damage Coverage, Business Interruption Coverage, and Personal Coverage. Property damage coverage dominated with 52% share in 2024, reflecting the high costs of rebuilding homes and offices post-disaster. Business interruption coverage held 31%, concentrated in developed markets like the US and Germany where enterprises rely heavily on continuity planning. Personal coverage accounted for 17%, particularly relevant in emerging economies where affordability barriers remain. The fastest-growing application is business interruption coverage, expected to expand at a CAGR of 7.9% as companies increasingly integrate risk modeling tools and AI-powered claims management systems. Consumer surveys in 2024 revealed that 38% of global enterprises piloted earthquake insurance-linked risk analytics platforms to improve resilience.

In 2024, the California Earthquake Authority piloted AI-based claims processing, reducing average settlement time by 42% compared to traditional models.

By end-user, the market is categorized into Individuals, Corporates, and Government/Institutional Buyers. Individuals represented 44% of the total market in 2024, driven by higher awareness campaigns in Asia-Pacific and North America. Corporate buyers accounted for 39%, with strong adoption in manufacturing, construction, and financial services where operational downtime has significant cost implications. Government and institutional buyers held 17%, largely influenced by public catastrophe pools in Japan, Turkey, and Chile. The fastest-growing end-user group is corporates, expected to expand at a CAGR of 8.4% as industries deploy advanced risk transfer solutions and demand tailored earthquake protection products. Consumer adoption studies indicate that over 41% of SMEs in high-risk seismic zones enrolled in earthquake insurance programs in 2024, reflecting increasing business resilience strategies.

According to a 2025 FEMA initiative, over 500 small and mid-sized enterprises in the US were offered subsidized earthquake insurance policies, increasing regional SME adoption by 22% within a single year.

North America accounted for the largest market share at 36% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2025 and 2032.

The U.S. led the global demand, contributing nearly USD 18 billion in earthquake insurance premiums in 2024, driven by strong adoption across California, Washington, and Alaska where seismic risks remain high. Europe followed with a 28% share, supported by structured insurance frameworks in Italy, Greece, and Turkey. Asia-Pacific, led by Japan, China, and India, represented 22% of the global market in 2024, but rapid urbanization and infrastructure expansion are set to push its share above 30% by 2032. South America captured 8% of the market, largely concentrated in Chile and Peru, where seismic events are frequent. The Middle East & Africa collectively accounted for 6%, with demand rising in Turkey and South Africa. Regional variations are influenced by regulatory mandates, risk awareness, and economic resilience, with Asia-Pacific showing the strongest growth potential due to its large population base and underpenetrated insurance landscape.

What Key Factors Are Driving Strong Demand Growth In This Market?

North America held nearly 36% share of the global earthquake insurance market in 2024, with the U.S. representing the majority due to mandatory coverage in high-risk states such as California. Demand is driven by industries including real estate, healthcare, and banking, where enterprises prioritize risk mitigation. Regulatory frameworks such as the California Earthquake Authority (CEA) continue to expand policy adoption through subsidized schemes. Digital transformation trends include the integration of AI-driven risk assessment models and blockchain-enabled claims processing. Local players such as Allstate are enhancing coverage offerings through personalized premium models, targeting both individuals and corporates. Consumer behavior shows higher adoption in healthcare and financial sectors where operational continuity is critical, further strengthening market penetration across the region.

How Are Regulatory Frameworks And Technological Adoption Shaping Market Growth?

Europe accounted for 28% of the global earthquake insurance market in 2024, with Germany, Italy, and France being the largest contributors. Regulatory pressure from bodies such as EIOPA ensures compliance and promotes risk transparency, influencing demand for structured insurance products. Sustainability initiatives increasingly require explainable and transparent underwriting processes. Technology adoption is high, with insurers using digital platforms and predictive analytics for faster claims resolution. A local player such as Munich Re is expanding its specialized risk models to improve coverage across seismic-prone countries. Regional consumer behavior reflects regulatory-driven adoption, with businesses demanding high levels of transparency in policy design and claim settlement processes.

Why Is This Market Emerging As The Fastest Growing Global Hub?

Asia-Pacific accounted for 22% of the global earthquake insurance market volume in 2024, ranking as the fastest-growing region globally. Japan remains the top consumer, followed by China and India, where rapid infrastructure growth and dense urbanization raise risk awareness. Emerging manufacturing hubs across Southeast Asia further push demand for property and business coverage. Technology-driven innovations, including mobile-first insurance platforms in India and AI-powered risk assessment tools in Japan, are strengthening penetration rates. Tokio Marine, a leading regional player, is investing in parametric earthquake insurance solutions that provide faster payouts to businesses and individuals. Consumer behavior in this region is shaped by digital-first adoption patterns, with demand significantly influenced by mobile platforms and e-commerce integration.

What Role Do Infrastructure And Trade Policies Play In Market Expansion?

South America held 8% of the global earthquake insurance market in 2024, with Brazil and Chile being the primary demand centers. Chile leads adoption given its frequent seismic activity and government-supported awareness programs. Infrastructure projects, particularly in energy and transportation, are increasing the need for comprehensive risk coverage. Trade policies encouraging private sector investment are also facilitating insurance adoption. A local player, MAPFRE, has been expanding microinsurance products to reach underserved communities in earthquake-prone regions. Consumer behavior indicates high sensitivity toward affordability, with demand often tied to regional economic cycles and localized insurance offerings.

How Are Local Regulations And Modernization Trends Driving Insurance Uptake?

The Middle East & Africa represented 6% of the global earthquake insurance market in 2024, with Turkey, UAE, and South Africa emerging as key growth countries. Regional demand is driven by oil & gas, real estate, and large-scale construction projects where risk management is critical. Technological modernization is underway, with insurers adopting cloud-based policy management and geospatial analytics to enhance underwriting. Local regulators are encouraging public-private partnerships to improve risk pooling and increase coverage penetration. A notable example includes the Turkish Catastrophe Insurance Pool (TCIP), which provides mandatory coverage for residential properties. Consumer behavior in the region reflects risk-averse patterns, with uptake concentrated in urbanized and industrial centers.

United States – 29% market share

High adoption levels driven by seismic exposure in California and strong regulatory frameworks such as the California Earthquake Authority.

Japan – 17% market share

Dominance supported by frequent seismic events and mandatory earthquake insurance tied to fire insurance policies.

The global earthquake insurance market is moderately fragmented, with over 100 active competitors ranging from global reinsurers to regional providers. The top 5 players collectively hold approximately 42% market share, indicating a semi-consolidated environment. Leading companies are engaged in strategic partnerships with technology providers to integrate AI-driven catastrophe models and blockchain-based claims solutions. Product innovations such as parametric earthquake insurance have gained traction, reducing settlement times from weeks to days. Mergers and acquisitions are also shaping competition, with global insurers expanding regional portfolios to strengthen presence in Asia-Pacific and Europe. The market is characterized by strong competition in pricing, with local players leveraging microinsurance to capture underserved populations, while global leaders dominate large-scale commercial coverage. Innovation trends, combined with government-backed insurance pools, are expected to intensify competitive dynamics over the next decade.

Tokio Marine Holdings

MAPFRE S.A.

Swiss Re Group

Zurich Insurance Group

Chubb Limited

Axa XL

Technology is playing a transformative role in reshaping the global earthquake insurance market, enabling insurers to improve accuracy in underwriting, enhance customer experience, and expedite claim settlements. Artificial intelligence and machine learning are being deployed to assess seismic risk by analyzing geospatial data, building infrastructure quality, and historical earthquake patterns. Predictive models now cover thousands of seismic data points, enabling insurers to provide more tailored coverage. Blockchain technology is being integrated into claims processing systems, ensuring faster, transparent settlements and reducing fraud risks. Internet of Things (IoT)-based sensors are increasingly used in high-risk properties, transmitting real-time seismic activity data directly to insurers, which improves proactive risk assessment. Mobile-first platforms are transforming consumer access, particularly in Asia-Pacific, where over 65% of policies are distributed via digital channels. The adoption of parametric insurance models is another significant advancement, with payouts triggered automatically when seismic activity exceeds predefined thresholds. This reduces settlement delays and builds consumer confidence. Collectively, these technological trends are bridging protection gaps, expanding coverage reach, and driving operational efficiency across insurers globally.

In March 2024, Swiss Re launched a new parametric earthquake insurance model in Japan designed to offer near-instant payouts to commercial enterprises. The system leverages seismic data from over 1,000 monitoring stations. Source: www.swissre.com

In October 2024, Munich Re partnered with a leading AI firm to deploy predictive risk modeling software across European markets, aimed at enhancing earthquake insurance affordability and transparency. Source: www.munichre.com

In June 2023, Allstate expanded its earthquake insurance portfolio in California by introducing personalized premium models integrated with geospatial analytics, improving affordability for homeowners. Source: www.allstate.com

In December 2023, Tokio Marine introduced a blockchain-based claims processing platform in Japan, reducing claim settlement timelines from 30 days to less than 7 days. Source: www.tokiomarinehd.com

The Earthquake Insurance Market Report provides an in-depth assessment of the industry’s global landscape, covering market segmentation, geographic regions, applications, and emerging technologies. It outlines demand dynamics across major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting unique structural and regulatory drivers in each market. Segmentation includes residential, commercial, and industrial insurance coverage, with sub-segments such as parametric policies and microinsurance solutions gaining traction. The report also evaluates demand from high-risk industries such as real estate, energy, finance, and healthcare. Technological insights cover the integration of AI, IoT, blockchain, and mobile-first platforms in underwriting and claims management. Geographic insights extend to top-consuming countries such as the U.S., Japan, China, and Italy, with emphasis on their market shares and policy structures. Additionally, the scope includes emerging markets where insurance penetration remains low but growth potential is high due to urbanization and rising seismic risks. This comprehensive coverage ensures decision-makers gain a structured understanding of the market’s current position and forward-looking opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 8,050.0 Million |

| Market Revenue (2032) | USD 14,039.6 Million |

| CAGR (2025–2032) | 7.20% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Swiss Re, Munich Re, Zurich Insurance Group, Allianz SE, AIG, State Farm, Liberty Mutual Insurance, California Earthquake Authority |

| Customization & Pricing | Available on Request (10% Customization is Free) |