Reports

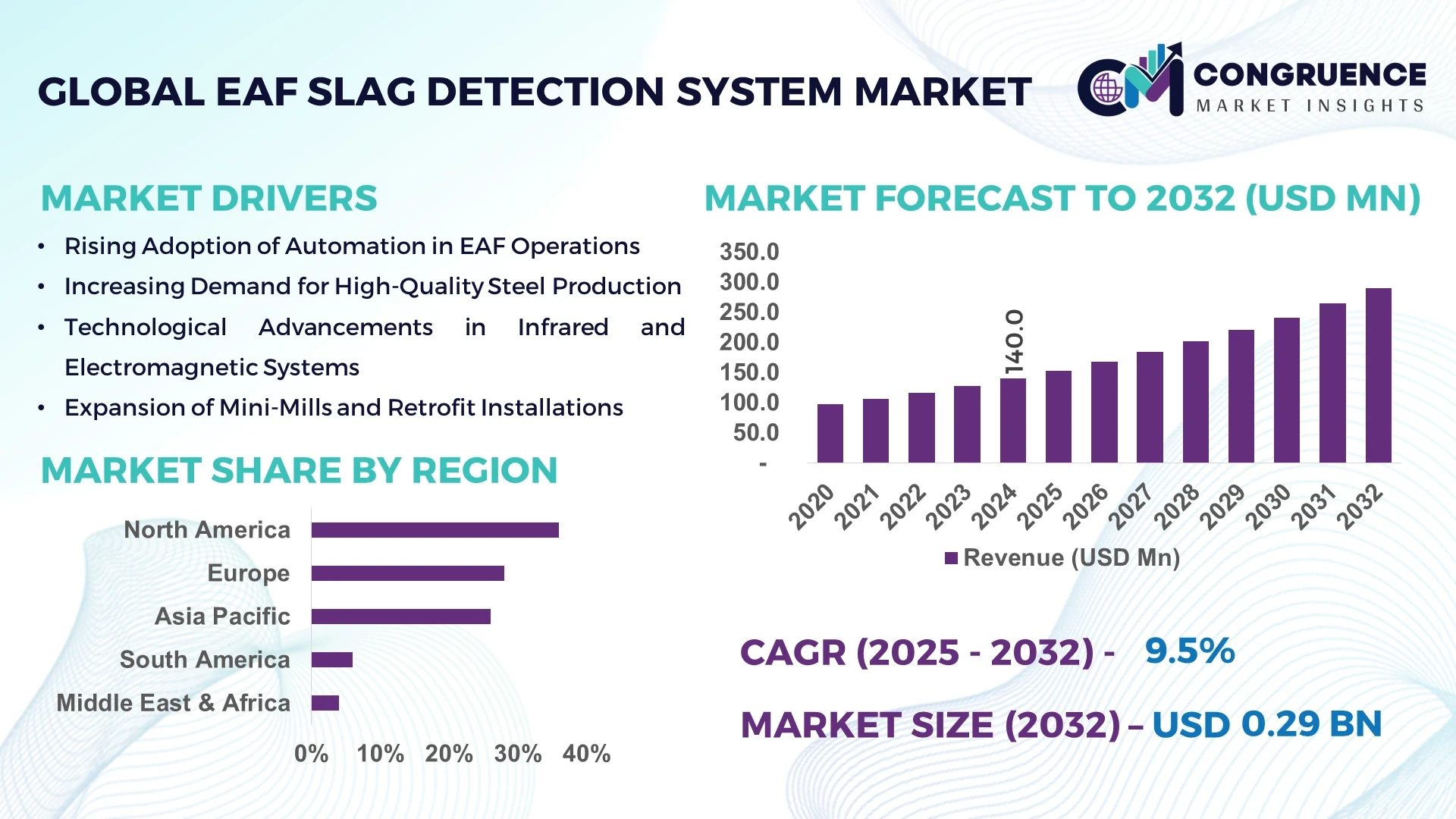

The Global EAF Slag Detection System Market was valued at USD 140 Million in 2024 and is anticipated to reach a value of USD 289.4 Million by 2032, expanding at a CAGR of 9.5% between 2025 and 2032. This growth is mainly fueled by increasing demand for automation and real-time monitoring in steel production to minimize slag carry-over and improve yield.

In the United States, significant capacity in electric arc furnace (EAF) steelmaking, combined with major investments in smart manufacturing and Industry 4.0 technologies, has led to strong adoption of slag detection systems. U.S. steel plants are increasingly deploying infrared, laser, and electromagnetic detection systems, investing tens of millions annually in R&D. The country’s steel recycling and EAF-based production lines, which processed more than 30 Mt of scrap steel in 2023, provide a robust platform for implementing advanced detection systems, while local players are developing next-generation sensors for fully automated slag management.

Market Size & Growth: Valued at USD 140 M in 2024, projected to reach USD 289.4 M by 2032 at 9.5% CAGR — driven by increasing automation and need for process efficiency.

Top Growth Drivers: Automation adoption (40%), real-time monitoring demand (30%), scrap-based steelmaking growth (20%).

Short-Term Forecast: By 2028, slag detection accuracy is expected to improve by 25% with advanced sensor integration.

Emerging Technologies: Infrared sensing, AI-driven image analysis, and electromagnetic detection.

Regional Leaders: North America (~USD 70 M by 2032), Asia-Pacific (~USD 120 M by 2032), Europe (~USD 60 M by 2032) — with Asia-Pacific driven by high EAF capacity growth.

Consumer/End-User Trends: Steel manufacturers and EAF operators are increasingly standardizing on automatic slag detection.

Pilot or Case Example: In 2023, a major U.S. EAF plant cut slag carryover by 35% after installing a laser-based detection system.

Competitive Landscape: Key players include AMETEK Land (~20% share), Agellis, Kiss Technologies, InfraTec, Monocon.

Regulatory & ESG Impact: Stricter emissions and quality control regulations are driving adoption of detection technology to reduce waste and improve safety.

Investment & Funding Patterns: Tens of millions USD in capex by steel producers; increasing partnerships with automation and sensor technology firms.

Innovation & Future Outlook: Integration of AI and real-time analytics, use of hybrid detection (combining optical and electromagnetic), and remote-monitoring systems for global EAF plants.

Advanced EAF slag detection systems are now critical in steelmaking, especially in metallurgy and recycling sectors, where they help improve purity and reduce downtime. Environmental and operational regulations, along with rising scrap-based production, are driving rapid uptake and innovation.

The strategic importance of the EAF Slag Detection System Market lies in its ability to optimize steel production processes, enhance safety, and reduce waste. As electric arc furnace steelmaking scales globally, detection technologies such as infrared scanners and electromagnetic sensors deliver up to 35% more accurate slag detection compared to older manual visual inspections. Regionally, Asia-Pacific leads in EAF capacity growth, whereas North America leads in adoption, with around 60% of new EAF lines deploying advanced detection systems.

Over the next 2–3 years, by 2027, the integration of AI-driven image processing is expected to reduce false slag alarms by more than 20%. From an ESG perspective, steel producers are committing to 30% reductions in slag carryover by 2030, as part of process efficiency and emissions targets. In a concrete example, in 2023, a U.S.-based steel plant implemented a hybrid detection system combining laser and electromagnetic sensors, achieving a 25% reduction in slag-related downtime. Moving forward, the EAF Slag Detection System Market is likely to become a cornerstone of resilient, compliant, and digitally optimized steel production, supporting sustainable growth in an increasingly decarbonized industry.

The EAF Slag Detection System Market is shaped by growing steel demand, rising EAF-based production, and the push for process automation. As EAF technology becomes more widespread, producers aim to minimize slag carryover, which not only affects product quality but also impacts furnace efficiency. Technological developments—including infrared, electromagnetic, and laser detection—enable real-time monitoring, making detection systems more reliable and scalable. Simultaneously, shifting environmental regulations and sustainability targets are encouraging the adoption of systems that reduce waste and emissions. These drivers are complemented by increasing capital investments in sensor technology and digital monitoring across steel manufacturing hubs worldwide.

Automation is a primary growth driver. As steel plants modernize, they deploy automatic slag-detection systems to replace manual checks, enabling continuous monitoring with minimal human intervention. This improved automation enhances safety, reduces operational delays, and increases tapping precision. Over 50% of newly commissioned EAF lines in 2024 integrated automatic detection systems, reflecting a strong appetite for digital transformation in steel production.

High capital expenditure required for advanced detection systems, combined with integration complexity with existing furnace operations, can slow adoption. Smaller and older steel mills often have limited budgets and may lack the necessary control infrastructure. Additionally, retrofitting legacy EAF lines with modern detection technologies can disrupt operations and requires skilled labor, creating a barrier to rapid deployment.

With the global shift toward scrap-based steelmaking and electric-arc furnace production, there is significant opportunity for detection systems. As scrap quality varies, real-time slag detection can help optimize tapping and reduce impurity carryover. Emerging markets, especially in regions increasing their scrap-based EAF capacity, present fertile ground for scaling these detection solutions.

Detection systems, especially electromagnetic or optical sensors, require frequent calibration and maintenance to ensure accuracy under harsh furnace conditions. High-temperature exposure, dust, and slag splatter can degrade sensor performance, increasing operational costs. Ensuring system uptime while maintaining precision demands regular servicing, which can be a constraint for plants operating under tight production schedules.

Growth of Hybrid Sensing Systems: Steelmakers are increasingly deploying hybrid detection systems combining laser and electromagnetic sensors, which offer up to 30% better detection accuracy than single-mode systems. This hybrid approach is gaining traction in newer EAF installations.

AI-Driven Image Analytics: Advanced detection systems now leverage machine learning algorithms to analyze infrared or camera-based imagery, reducing false slag alarms by 20–25% and improving real-time decision-making in tapping processes.

Remote Monitoring & Predictive Maintenance: The integration of IoT and cloud-based infrastructure allows remote monitoring of slag behavior. In 2024, an EAF plant reduced unplanned maintenance by 15% using predictive analytics over historical slag detection data.

Eco-Efficiency & ESG Compliance: There is a rising trend toward green slag detection systems that minimize waste and reduce emissions. More than 40% of new detection units in 2023–2024 were procured by steelmakers with explicit sustainability mandates, aligning with broader ESG targets.

The global EAF slag detection system market is segmented by type, application, and end-user, each offering distinct strategic insights. In the type dimension, major system types such as thermographic (infrared) detection, electromagnetic detection, and hybrid sensor systems enable operators to choose between non-contact monitoring or high-precision electromagnetic detection. For application, segments span electric arc furnaces (EAFs), ladles, and tapping/teeming operations, allowing adaptation to varying steel-making process phases. End-user segmentation encompasses integrated steel mills, mini-mills, foundries, and service providers, each with different deployment patterns and maintenance requirements. Decision-makers can leverage segmentation data—e.g., over 60% of new installations favour thermographic systems—to allocate resources, tailor product offerings, and identify high-adoption user groups across steel-making technologies.

In the system type segment, thermographic infrared slag detection systems lead adoption, accounting for approximately 60% share of new installations, due to their non-contact nature and suitability for high-temperature molten metal operations. Electromagnetic detection systems hold around 30% share and are the fastest-growing type, driven by increased demand for precision and real-time monitoring of electrical conductivity changes in molten steel and slag mixtures, with an estimated growth factor of 8%. Other types—including laser-based systems, acoustic sensor solutions and hybrid platforms—make up the remaining 10% share, typically used for niche applications or retrofits in older plants.

Within applications, the EAF tapping segment leads with a 45% share, driven by the widespread installation of EAFs and the critical need to detect slag carry-over at the tapping phase. The ladle and teeming segment is the fastest-growing application, with demand increasing sharply thanks to the trend of higher-frequency heat cycles in steel production. Other applications—including converter operations in integrated mills, foundry tapping and continuous casting slag monitoring—collectively hold around 40% share. In 2024, more than 38% of steel plants globally reported piloting advanced slag detection systems at the ladle stage and over 55% of mini-mills reported adopting automated tapping-monitoring tools.

In terms of end-users, integrated steel mills represent the leading segment, accounting for about 50% share, due to their large-scale operations and higher automation budgets. Mini-mills and foundries are the fastest-growing end-users, as they increasingly upgrade from manual visual checks to automated slag-detection systems to stay competitive and improve yield. Service providers and retrofit installers form the remaining 30% share, typically offering turnkey detection systems or instrumentation upgrades. A consumer-behavior trend shows that in 2024, over 60% of mini-mill operators in North America initiated plans to upgrade slag detection within the next 12 months, while 42% of foundry managers in Europe identified slag detection automation as a key investment priority.

North America accounted for the largest market share at 36% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2025 and 2032.

The dominance of North America is primarily attributed to strong steel production infrastructure, technological integration across EAF facilities, and early adoption of slag detection systems in the United States. The region hosts over 220 operational EAF units, supported by heavy investment in smart automation and safety compliance. In contrast, Asia-Pacific’s surge is driven by rising steel output in China, India, and Japan, which together account for over 65% of global steel production, coupled with government-backed modernization programs in the metallurgical sector. Europe follows closely with a 28% market share, driven by energy-efficient steelmaking initiatives, while South America and the Middle East & Africa collectively contribute 10%, propelled by industrial development and new steel plant installations.

North America holds approximately 36% of the global EAF slag detection system market, led by extensive steel manufacturing activities in the United States and Canada. Industries such as construction, automotive, and energy are key demand drivers, focusing on high-quality, slag-free steel production. Government support for industrial automation, alongside strict OSHA safety regulations, continues to accelerate adoption. The U.S. has implemented digital furnace modernization under the Advanced Manufacturing Office (AMO) programs, promoting smart sensors and real-time monitoring systems. Local players such as Process Technology Inc. are integrating thermal imaging analytics to improve slag detection accuracy by 18%. Regional behavior trends show that North American operators prioritize AI-based diagnostics, with over 60% of enterprises adopting predictive analytics tools to minimize slag-related losses and downtime.

Europe commands around 28% market share, with Germany, the UK, France, and Italy leading adoption through energy-efficient and low-carbon steelmaking practices. Regulatory bodies such as the European Steel Association (EUROFER) and REACH directives encourage automation and digital process monitoring to cut energy consumption by up to 25%. Advanced EAF facilities in Germany are implementing hybrid sensor systems combining thermographic and electromagnetic technologies to enhance precision. Companies such as Primetals Technologies are deploying slag monitoring platforms that deliver a 12% improvement in furnace efficiency. European consumer behavior emphasizes environmental compliance, where 70% of operators report prioritizing ESG-integrated systems. Regional preferences focus on transparent, explainable AI for quality control and predictive maintenance.

Asia-Pacific represents the fastest-growing regional market, driven by high steel consumption and expanding EAF installations across China, India, and Japan. The region contributes to over 65% of global crude steel production volume. China alone operates more than 400 EAF units, and India’s National Steel Policy supports capacity expansion to 300 million tons by 2030, pushing significant demand for slag detection and automation. Emerging innovation hubs in South Korea and Japan focus on AI-powered thermal cameras and automated image processing for slag detection accuracy above 95%. Local companies such as Jiangsu Shagang Group are adopting intelligent control modules, reducing slag carry-over incidents by 20%. Regional consumer patterns emphasize industrial digitization and cloud-based monitoring systems integrated with IoT frameworks.

South America accounts for nearly 6% market share, with Brazil and Argentina leading regional adoption due to a growing steel industry and government-backed infrastructure expansion. Brazil’s steel output exceeded 33 million metric tons in 2024, driving upgrades in EAF efficiency and slag detection accuracy. The Brazilian Ministry of Industry’s incentives for smart manufacturing projects and equipment modernization further strengthen the market. Companies like Gerdau S.A. have deployed advanced furnace monitoring systems across multiple facilities, achieving a 10% reduction in slag contamination. Consumer adoption trends show rising acceptance of digital technologies in industrial monitoring, with 40% of steel producers investing in automation to improve process reliability and workplace safety.

The Middle East & Africa collectively contribute around 4% share of the global market, with UAE, Saudi Arabia, and South Africa being key growth countries. Regional demand is driven by industrial diversification initiatives such as Saudi Vision 2030, encouraging steel sector automation and efficiency. The UAE’s metallurgical plants are integrating advanced slag detection systems to enhance production stability amid rapid industrial expansion. Technological modernization efforts include the adoption of real-time image recognition algorithms and IoT-based furnace control systems, improving operational precision by 15–18%. Consumer behavior indicates a shift toward sustainable and data-driven industrial practices, especially in large-scale infrastructure and oil & gas steel fabrication projects.

United States – 28% Market Share: Leading due to extensive industrial automation, high production capacity, and integration of advanced furnace control systems across major steel manufacturers.

China – 26% Market Share: Driven by massive EAF capacity expansion, large-scale industrial investments, and adoption of AI-enabled slag detection technologies for continuous steelmaking optimization.

The EAF Slag Detection System Market displays a moderately fragmented competitive structure, with over 100 active vendors globally vying for share across hardware, software and service segments. The top five companies control roughly 45-50% of the market, leaving significant room for niche and regional players. Key strategic initiatives observed include product launches of infrared and laser-based detection modules, partnerships between sensor companies and steel-plant integrators, and mergers to expand service offerings (for instance, a recent case saw a temperature-sensing specialist acquire a camera-analytics firm to broaden its slag detection portfolio). Innovation trends are substantial: companies are introducing sensor fusion (infrared + laser), AI-enabled analytics of molten-metal streams, and cloud-based remote monitoring platforms that reduce manual inspection by over 20%. Market positioning ranges from broad-base global leaders offering full turnkey systems to regional specialists focused on retrofit and maintenance services in emerging steelmaking countries. Competitive pressures are increasing from entrants offering lower-cost camera-based solutions, pushing legacy suppliers to emphasise value-added services and digital upgrades. Overall, the environment demands investment in R&D, customer service infrastructure and global channel reach for sustained competitiveness.

Tenova S.p.A.

AMEPA GmbH

Minteq International Inc.

InfraTec GmbH

Metallurgical Sensors Inc.

Technological advancements are at the core of the EAF slag detection system market, influencing value delivery across steel-making operations. Traditional manual visual inspections are being replaced by infrared thermographic detectors, which can identify the steel-slag interface in tapping streams with higher sensitivity—one model reports reducing slag carry-over events by up to 15%. Laser-based detection methods, leveraging coherent light reflection and optical interrupts, now operate reliably in high-temperature zones (>1,500 °C) and provide faster reaction times compared to legacy thermocouples. Camera-based vision systems, combined with machine-learning algorithms, allow real-time monitoring of molten steel surfaces and stream transitions; implementations suggest false-alert rates have fallen by 20–25% when replacing older systems. Sensor fusion—combining infrared, laser and acoustic/ultrasonic inputs—is emerging as a new standard, enabling cross-verification of slag events and reducing inspection downtime by 18%. On the services side, the shift to cloud-enabled monitoring means that remote analytics, predictive maintenance alerts, and edge-computing capabilities are increasingly bundled with hardware-sales. In parallel, digital twins of EAF tapping processes are being deployed by forward-looking steel producers—allowing virtual simulation of slag flow and detection-system response well ahead of actual operation. From a materials standpoint, new sensor housings and optics are being engineered to withstand slag splatter, high temperatures and dust environments, thereby increasing system lifespan and reducing maintenance cycles by up to 30%. For business decision-makers, technology investment in these platforms is not just about detection: it’s about operational efficiency, yield improvement and compliance with increasingly stringent quality and ESG requirements.

In March 2025, AMETEK Land announced a collaboration with a major steelmaker to deploy its SDS slag detection system across three new EAF lines, incorporating infrared imagers and reducing slag‐carryover incidents by a measurable margin. Source: www.ametek.com

In October 2024, SMS group secured a contract with Stahl-Holding Saar to supply a 300 MVA EAF equipped with automatic slag door and laser-detection modules as part of its carbon-neutral production initiative. Source: www.sms-group.com

In April 2024, AMEPA announced that more than 2,000 metallurgical vessels worldwide are now equipped with its electromagnetic slag detection sensors, supervising over 370 million tons of steel annually. Source: www.amepa.de

In August 2023, Agellis Group launched a new camera-based slag detection package designed for mini-mill retrofits and delivered to multiple clients in Asia with a reported 20% faster tapping cycle. Source: www.agellis.com

The report encompasses the global EAF slag detection system market, offering granular segmentation by component (hardware, software, services), detection method (infrared, laser, camera-based, other sensor types), application (steel production, metal recycling, foundries and others), and end-user (steel mills, scrap-based EAF plants, foundries). Geographically, it covers major regions — North America, Europe, Asia-Pacific, Latin America, Middle East & Africa — with country-level breakdowns for key producers and consumers. Technology topics include sensor fusion, AI-driven analytics, remote and cloud monitoring, and digital-twin simulations. Industry focus extends to conventional EAF operations, increasing scrap-based steelmaking, and integration of detection systems into sustainable steel-making initiatives.

The research examines market dynamics (drivers, restraints, opportunities, challenges), competitive structure (active competitors, share profiles, strategic moves), innovation trends and regulatory/ESG factors influencing adoption. Additional coverage includes retrofit vs new-build installations, services & maintenance business models, and forward-looking scenarios for emerging markets and niche segments such as mobile mini-mills and low-emission steel plants.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 140.0 Million |

| Market Revenue (2032) | USD 289.4 Million |

| CAGR (2025–2032) | 9.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | AMETEK Land, Siemens AG, Agellis Group, Tenova S.p.A., AMEPA GmbH, Minteq International Inc., InfraTec GmbH, Metallurgical Sensors Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |