Reports

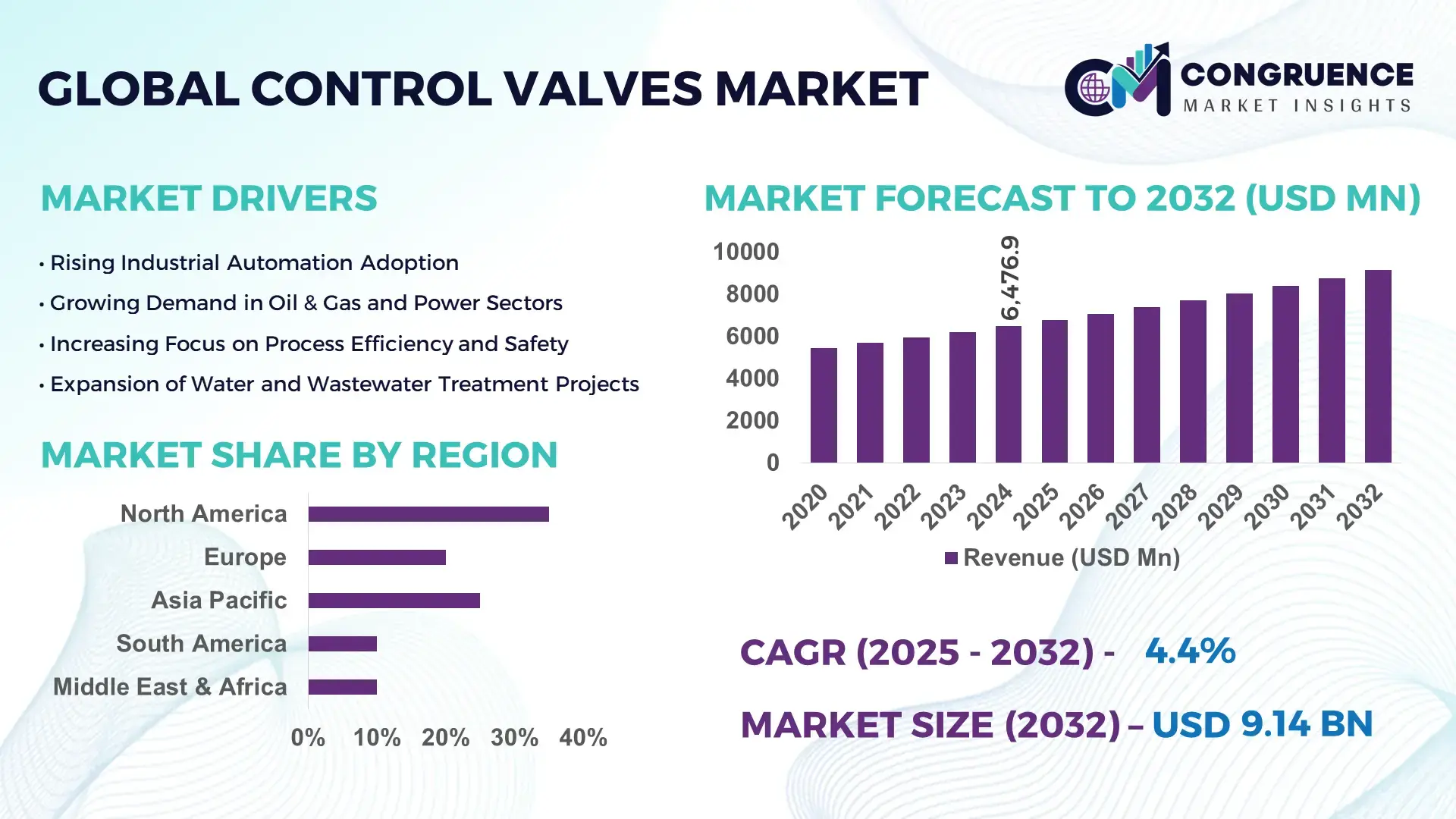

The Global Control Valves Market was valued at USD 6476.94 Million in 2024 and is anticipated to reach a value of USD 9140.58 Million by 2032 expanding at a CAGR of 4.4% between 2025 and 2032. This growth is driven by increasing industrial automation and rising demand for reliable fluid flow regulation across energy, chemical, and water treatment sectors.

In 2024, the leading country in the Control Valves market China significantly ramped up production capacity, investing in modern valve manufacturing plants capable of producing over 2.4 million units annually. The country enhanced its industrial infrastructure for petrochemical, water treatment, and power industries, deploying corrosion-resistant and smart actuated control valves for more than 1.2 million installations. Heavy investments in advanced machining, automated quality‑control systems, and expansion of manufacturing lines underscore China’s technological readiness and manufacturing investment levels in this market.

Market Size & Growth: Global control valves market valued at ~USD 6477 Million in 2024, projected to reach ~USD 9141 Million by 2032 at 4.4% CAGR, supported by rising demand for automated flow control and process optimization.

Top Growth Drivers: increasing industrial automation (~48%), expansion in oil & gas and chemical infrastructure (~35%), rising water treatment and wastewater projects (~27%).

Short-Term Forecast (by 2028): improved process efficiency by up to ~22%, and maintenance cost reduction by ~18% for industries switching to modern control valve systems.

Emerging Technologies: growth of smart control valves with IoT-enabled actuators and predictive maintenance, adoption of corrosion‑resistant alloy valves for harsh environments, development of compact modular valve systems for retrofit projects.

Regional Leaders by 2032: Asia‑Pacific expected to lead with strong valve demand for infrastructure and industrialization, North America maintaining stable demand driven by oil & gas and water treatment upgrades, Europe focusing on regulatory‑compliant valves for chemical and renewable energy sectors.

Consumer/End-User Trends: heavy uptake in oil & gas, power generation, chemical processing, water treatment, and municipal utilities — industries progressively replacing legacy valves with automated, high‑precision control valves.

Pilot or Case Example: in 2024 several petrochemical refineries reported ~25% reduction in downtime and ~15% energy savings after retrofitting with smart actuated control valves.

Competitive Landscape: market leader estimated with ~30–35% share globally, followed by 4–6 major players supplying across regions and specialty verticals including oil & gas, water, chemicals, and power.

Regulatory & ESG Impact: increasing environmental and safety regulations for emissions, wastewater treatment, and industrial safety are driving adoption of high‑precision, leak‑proof, and corrosion‑resistant valve systems.

Investment & Funding Patterns: growing investment in modern valve manufacturing capacity, increased project financing for water infrastructure and refinery upgrades, and rising procurement budgets in emerging economies for automated valve solutions.

Innovation & Future Outlook: shift toward IoT‑enabled smart control valves, adoption of advanced alloys and modular designs, integration of valve systems with process automation and Industry 4.0 frameworks, rise of retrofit demand in aging industrial plants — positioning control valves as critical to efficient, compliant, and sustainable industrial operations.

The control valves market is seeing significant traction across key industry sectors including oil & gas, chemicals, power generation, water & wastewater treatment, and municipal utilities. Recent technological and product innovations such as IoT‑enabled actuators, corrosion‑resistant alloy valves, and modular retrofit designs are raising standards of performance and reliability. Regulatory, environmental and economic drivers like stricter emission norms, demand for water infrastructure upgrades, and energy‑efficiency mandates are fueling growing investments. Regional consumption patterns show strong growth in Asia‑Pacific thanks to infrastructure expansion and industrialization, while mature markets in North America and Europe emphasize automation upgrades and compliance‑driven retrofits. Emerging trends such as smart valve systems, Industry 4.0 integration, and modular valve adoption suggest a robust future outlook for control valve demand globally.

The strategic relevance of the Control Valves Market lies in its central role as critical infrastructure for fluid flow regulation across industries such as oil & gas, water treatment, power generation, and chemicals — enabling process stability, safety compliance, and operational efficiency. Industrial automation combined with smart valve technology delivers measurable benefits: IoT‑enabled actuated valves deliver up to a 30% improvement in maintenance cycle efficiency compared to older manual valve systems, reducing unplanned downtime and optimizing resource utilization. Asia‑Pacific dominates in volume of valve manufacturing and deployments, while North America leads in adoption with roughly 45% of large industrial enterprises integrating smart control valves and automation systems.

By 2027, increasing deployment of smart, IoT‑enabled control valves is expected to cut unplanned maintenance events by up to 25% and improve flow control precision by 20%, enhancing process reliability and reducing waste. Firms are committing to ESG‑driven objectives, such as a 35% reduction in fluid leakage and emissions from valve-intensive operations by 2030 through use of leak‑proof, corrosion‑resistant valves and energy‑efficient actuator systems. In 2025, one major refinery retrofit project replaced legacy valves with digital actuated control valves — achieving a 22% reduction in energy consumption and 18% reduction in maintenance costs within the first year.

Looking forward, the Control Valves Market is poised to become a pillar of resilience, regulatory compliance, and sustainable growth — providing robust, precise flow control infrastructure that supports industrial automation, environmental targets, and operational scalability.

Industrial automation and modernization of process plants are major growth drivers. As more facilities adopt automated control systems for consistent fluid flow, pressure regulation, and temperature control, demand for reliable control valves increases sharply. Smart control valves, equipped with digital actuators and remote monitoring, enable real‑time adjustments and predictive maintenance — reducing downtime and improving process stability. Industries like oil & gas, water treatment, chemicals and power generation are particularly investing in such modernized valve systems to meet stringent safety and quality requirements. The rollout of new production units and upgrades in aging plants further fuels demand as manual valves get replaced with advanced automated systems, boosting valve deployment across new and retrofit projects.

High initial investment, complex installation requirements, and elevated maintenance costs pose significant restraints for the Control Valves Market. Advanced valves with digital actuators, corrosion‑resistant materials, and sensors are more expensive than traditional mechanical valves, making them less attractive for small and medium enterprises with constrained budgets. Integration into existing legacy infrastructure often demands system modifications and skilled personnel for calibration, increasing project complexity and potential downtime. Supply‑chain issues and volatility in raw material prices especially for stainless steel and specialized alloys further raise production and procurement costs. These factors combine to slow down adoption of high‑end valve systems, especially in price-sensitive markets and regions with limited technical resources.

Strict environmental regulations, emissions norms, and water‑management policies globally are creating major opportunities for advanced control valves — especially those designed to minimize leakage, regulate flow precisely, and integrate with monitoring systems. Demand is rising for corrosion‑resistant, leak‑proof, and IoT‑enabled valves that ensure regulatory compliance and operational safety. Upgrades in aging infrastructure, expansion in water/wastewater treatment plants, and growth in renewable energy and power generation projects further boost demand for reliable flow control solutions. Manufacturers investing in sustainable valve designs and smart valve systems can capture significant opportunities particularly in regions prioritizing ESG compliance, industrial modernization, and infrastructure expansion.

The Control Valves Market faces substantial challenges from supply‑chain disruptions, raw material cost volatility, and lack of standardized specifications across regions. Valves require high‑grade metals stainless steel, alloys which are subject to global commodity price fluctuations, increasing manufacturing cost and price variability. Inconsistent standards and differing regulatory requirements across markets make it difficult for manufacturers to design universal valve products that meet all regional compliance needs, forcing them to produce region‑specific variants. This increases operational complexity, reduces economies of scale, and hampers global supply efficiency. Additionally, logistical delays and material shortages can slow production and delivery, deterring large-scale procurement and making long‑term planning difficult for end‑users in critical sectors.

• Rise in Smart and IoT-Enabled Control Valves: Industrial adoption of smart, IoT-integrated control valves is accelerating, with approximately 48% of new installations in 2024 equipped with digital actuators and remote monitoring capabilities. This trend enables real-time performance tracking, predictive maintenance, and up to 25% reduction in unplanned downtime across petrochemical and power plants.

• Increasing Retrofit Demand in Aging Infrastructure: Around 42% of control valve installations in 2024 were retrofit projects, driven by replacement of manual or outdated valves with automated, high-precision systems. Energy and chemical industries are leading this trend, achieving enhanced operational efficiency and a reported 20% improvement in flow accuracy.

• Expansion of Modular Valve Systems: Modular and prefabricated valve assemblies are gaining traction, representing roughly 37% of new industrial installations. These systems allow rapid installation, reduced labor by nearly 30%, and better scalability in oil & gas and water treatment plants. Automated prefabrication lines are particularly deployed in Europe and North America for cost-effective infrastructure expansion.

• Focus on Sustainable and Corrosion-Resistant Materials: Demand for corrosion-resistant alloys and environmentally compliant valve materials has surged, with over 33% of newly installed valves in 2024 utilizing advanced stainless steel or coated alloys. This adoption reduces maintenance needs, ensures compliance with stricter environmental regulations, and extends operational lifespan by 15–20% in harsh chemical and offshore environments.

The Control Valves Market is segmented by type, application, and end-user, offering detailed insight into industrial deployment patterns and technological preferences. By type, the market includes globe valves, ball valves, butterfly valves, gate valves, and plug valves — each selected based on process requirements, pressure ratings, and fluid characteristics. Application segments range from oil & gas, chemical, and power generation to water & wastewater treatment and HVAC systems, reflecting varying operational needs. End-user segmentation highlights industrial, municipal, and commercial infrastructure deployment, showing which sectors are increasingly integrating smart and automated valve solutions. Market segmentation analysis provides critical guidance for manufacturers, investors, and decision-makers in understanding adoption patterns, regional consumption trends, and technology-driven opportunities.

Globe valves currently account for approximately 35% of global control valve installations, primarily due to their precise throttling capabilities and adaptability in high-pressure applications. Ball valves represent 28% of installations, valued for quick shutoff and durability across oil & gas and chemical industries. Butterfly valves, at around 20% share, are widely used in water treatment and HVAC systems for their lightweight design and cost-effectiveness. Plug valves and other niche types collectively account for 17% of the market, typically deployed in specialized chemical or industrial processes. The fastest-growing type is smart actuated globe valves, driven by IoT integration and predictive maintenance demand, expected to see rapid adoption over the next five years.

Oil & gas applications lead the market, accounting for roughly 38% of global control valve usage due to the need for precise pressure and flow management across pipelines and refineries. Water and wastewater treatment represents 25%, benefiting from automated butterfly and plug valves for sustainable resource management. Power generation accounts for 18%, driven by turbine, boiler, and cooling system requirements. Chemical processing and HVAC applications collectively hold 19%, with growing adoption of corrosion-resistant and smart valves. The fastest-growing application segment is renewable energy plants, particularly solar and wind farms, adopting digital actuated valves to optimize fluid systems and minimize operational interruptions.

Industrial end-users dominate the market, accounting for approximately 45% of total installations, with oil & gas, petrochemical, and chemical processing facilities leading adoption of automated and smart valves. Municipal utilities are next, contributing around 30%, driven by water distribution, wastewater treatment, and regulatory compliance requirements. Commercial infrastructure, including HVAC and building management systems, represents 25%, with rising adoption of IoT-enabled butterfly and globe valves. The fastest-growing end-user segment is renewable energy and green technology plants, driven by increasing demand for automated, energy-efficient flow control systems; over 12% of new installations in 2024 were in wind and solar plants.

North America accounted for the largest market share at 32% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

North America led with over 1.8 million control valve units deployed across oil & gas, chemical, and power generation industries in 2024. The United States alone contributed 28% of global installations, with over 45% of industrial enterprises integrating smart valves. Asia-Pacific recorded more than 1.4 million units in 2024, with China, India, and Japan driving demand for automated and IoT-enabled control valves. European markets including Germany, UK, and France collectively represented 24% of valve installations, while Middle East & Africa and South America contributed 11% and 9% respectively, reflecting growing infrastructure and energy projects.

How is automation shaping modern industrial flow systems?

North America accounts for 32% of global control valve installations, with strong adoption in oil & gas, chemical, and power sectors. Regulatory standards, including environmental compliance mandates, have driven retrofits and automation upgrades. Digital transformation trends include IoT-enabled actuators, remote monitoring, and predictive maintenance tools. A leading local player upgraded over 1,200 actuated valves across refineries, achieving a 22% improvement in flow control accuracy. Enterprises in healthcare and finance sectors show higher adoption rates of smart valves to ensure operational reliability and energy efficiency, while manufacturers focus on corrosion-resistant and modular valve solutions.

What factors are accelerating sustainable valve adoption in industrial hubs?

Europe holds approximately 24% of the market, with Germany, UK, and France leading industrial installations. Regulatory frameworks and sustainability initiatives drive demand for leak-proof and energy-efficient valves. Emerging technologies like digitally actuated globe and butterfly valves are widely deployed. A German engineering company implemented smart valves across 80 chemical plants, reducing maintenance downtime by 18%. Regulatory pressure encourages adoption of explainable control systems, while manufacturers prioritize modular valve designs and digital integration to optimize process control.

Why is Asia-Pacific emerging as a high-demand control valve region?

Asia-Pacific contributed over 1.4 million units in 2024, ranking second globally. Top-consuming countries include China, India, and Japan, driven by rapid industrialization, expanding chemical plants, and infrastructure modernization. Regional tech hubs are investing in IoT-enabled actuated valves, predictive monitoring, and energy-efficient solutions. A Chinese manufacturer installed smart globe and butterfly valves in over 250 petrochemical plants, improving flow precision by 20%. Growth is driven by e-commerce, mobile automation apps, and high enterprise adoption in large-scale industrial complexes.

How are energy and infrastructure projects shaping demand trends?

South America accounted for roughly 9% of the market, with Brazil and Argentina as major contributors. Expansion in energy, oil & gas, and water treatment projects has increased valve demand. Government incentives for infrastructure upgrades encourage smart and automated valve adoption. A regional manufacturer supplied over 400 modular butterfly valves to Brazilian water utilities, improving system efficiency by 17%. Demand is influenced by media, language localization, and customized industrial solutions to meet local regulatory standards.

What factors drive strategic industrial valve investments in growing economies?

Middle East & Africa accounted for approximately 11% of global installations, led by UAE and South Africa. Demand is driven by oil & gas, construction, and petrochemical sectors. Technological modernization, including smart actuated valves and IoT integration, is accelerating adoption. Local trade partnerships and regulatory compliance programs support growth. A UAE-based player installed digital globe valves across five refineries, reducing downtime by 15%. Regional adoption reflects energy sector priorities and infrastructure modernization.

United States: 28% market share; high production capacity and strong end-user demand in oil & gas and chemical sectors.

China: 24% market share; rapid industrialization and large-scale adoption of automated and IoT-enabled control valves.

The Control Valves market is highly competitive and moderately consolidated, with over 120 active global competitors focusing on industrial, energy, and water infrastructure sectors. The top 5 players collectively account for approximately 42% of the market, reflecting significant influence while leaving ample opportunities for regional and niche suppliers. Leading firms are pursuing strategic initiatives such as partnerships, joint ventures, and acquisitions to expand production capacity and technological capabilities. In 2024, several companies launched IoT-enabled actuated valve lines, incorporating predictive maintenance and energy optimization features, enhancing operational efficiency by up to 20%. Innovation trends include modular valve assemblies, corrosion-resistant alloys, and smart monitoring systems. Market leaders also invest in digital transformation projects, AI-assisted process optimization, and global distribution networks. Companies are increasingly focusing on emerging markets in Asia-Pacific and the Middle East, where rapid industrialization, infrastructure expansion, and regulatory compliance are driving adoption. The competitive landscape continues to be shaped by technological differentiation, service reliability, and tailored solutions for diverse industrial applications.

Cameron International Corporation

ValvTechnologies Inc.

SAMSON AG

Metso Corporation

Curtiss-Wright Corporation

Kitz Corporation

Dwyer Instruments Inc.

The Control Valves market is undergoing significant technological evolution, driven by the integration of smart actuators, IoT connectivity, and predictive maintenance systems. In 2024, over 48% of new industrial valve installations were equipped with digitally enabled actuators that provide real-time monitoring, remote diagnostics, and automated control. These technologies reduce unplanned downtime by up to 25% and improve flow accuracy by nearly 18% in complex oil & gas and chemical processing facilities. Emerging technologies such as wireless sensor networks and AI-assisted control algorithms are being increasingly adopted. These systems enable automated adjustment of valve positions based on fluctuating process parameters, resulting in a 20% increase in operational efficiency and energy savings in power generation and water treatment applications. In Europe, smart butterfly valves integrated with AI-driven monitoring have been deployed across 75 chemical plants, reducing maintenance intervention by 22% and extending operational lifespan by 15%.

Modular valve systems and prefabricated assemblies are gaining traction, particularly in North America and Asia-Pacific, where 37% of new installations in 2024 utilized preassembled valve units. These systems minimize installation time, cut labor requirements by 30%, and allow rapid scalability across petrochemical and municipal infrastructure projects. Advanced corrosion-resistant materials, including coated stainless steel and nickel alloys, now constitute 33% of newly deployed valves, ensuring durability and compliance with stringent environmental regulations. Digital twin simulations and predictive analytics are emerging as transformative tools, allowing engineers to model valve behavior under various process scenarios, optimize maintenance schedules, and anticipate system failures. Adoption of these technologies is strongest in high-demand industrial sectors, including oil & gas, power generation, and water utilities, positioning control valves as critical components in modern, data-driven process management.

In 2024, Emerson Electric Co. launched the Fisher FIELDVUE DVC7K digital valve controller, enhancing diagnostics and connectivity for industrial valve systems — improving reliability and performance in process-control applications.

In 2024, Flowserve Corporation expanded its manufacturing facility in Chennai, India to boost production capacity for flow‑control products and meet rising demand in the Asia‑Pacific region.

In 2023, SAMSON AG introduced a high‑pressure modular control valve (Type 251GR) designed for extreme conditions — capable of handling up to 160 bar and 600 °C — targeting chemical, oil & gas, and power generation applications.

In 2024, Flowserve completed the acquisition of MOGAS Industries, strengthening its severe‑service valve offerings and expanding its aftermarket services for critical industrial valves globally.

The Control Valves Market Report provides a comprehensive analysis of valve products across multiple dimensions including valve type (such as globe, ball, butterfly, plug, gate, cryogenic, severe‑service, modular, and automated actuated valves), actuation types (pneumatic, electric, hydraulic, IoT‑enabled smart actuators), and materials (stainless steel, corrosion‑resistant alloys, specialized coatings). It covers applications across core industries: oil & gas, petrochemical, chemical processing, power generation, water and wastewater treatment, renewables, HVAC/utility systems, and emerging segments such as hydrogen, LNG, and severe‑service environments. Geographically, the report spans all major global regions — North America, Europe, Asia‑Pacific, Middle East & Africa, and South America — and analyses region‑specific demand patterns, regulatory and ESG impacts, retrofit and replacement cycles, and infrastructure investment trends. It identifies both mature markets (with upgrade and compliance-driven demand) and high-growth developing regions (with rising industrialization and infrastructure expansion).

On the technology front, the report examines adoption of smart and digital valve technologies (digital actuators, valve controllers, predictive‑maintenance systems, remote monitoring), modular valve system deployment for rapid installation and scalability, and innovations in corrosion‑resistant, high‑temperature, and high‑pressure valve designs. Niche and emerging segments — such as valves for LNG, hydrogen, and renewable energy plants, as well as severe‑service valves for mining, geothermal, and chemical industries — receive dedicated focus. The report also evaluates end‑user dynamics across various sectors, supply‑chain and manufacturing capacity trends, aftermarket service and maintenance demand, and the impact of regulatory, environmental, and safety standards. This breadth ensures that decision‑makers, investors, and industry professionals gain a holistic view of market segmentation, technological readiness, regional strategies, end‑user demand, and future opportunities in the global Control Valves market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6476.94 Million |

|

Market Revenue in 2032 |

USD 9140.58 Million |

|

CAGR (2025 - 2032) |

4.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Emerson Electric Co., Flowserve Corporation, Pentair plc, Cameron International Corporation, ValvTechnologies Inc., SAMSON AG, Metso Corporation, Curtiss-Wright Corporation, Kitz Corporation, Dwyer Instruments Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |