Reports

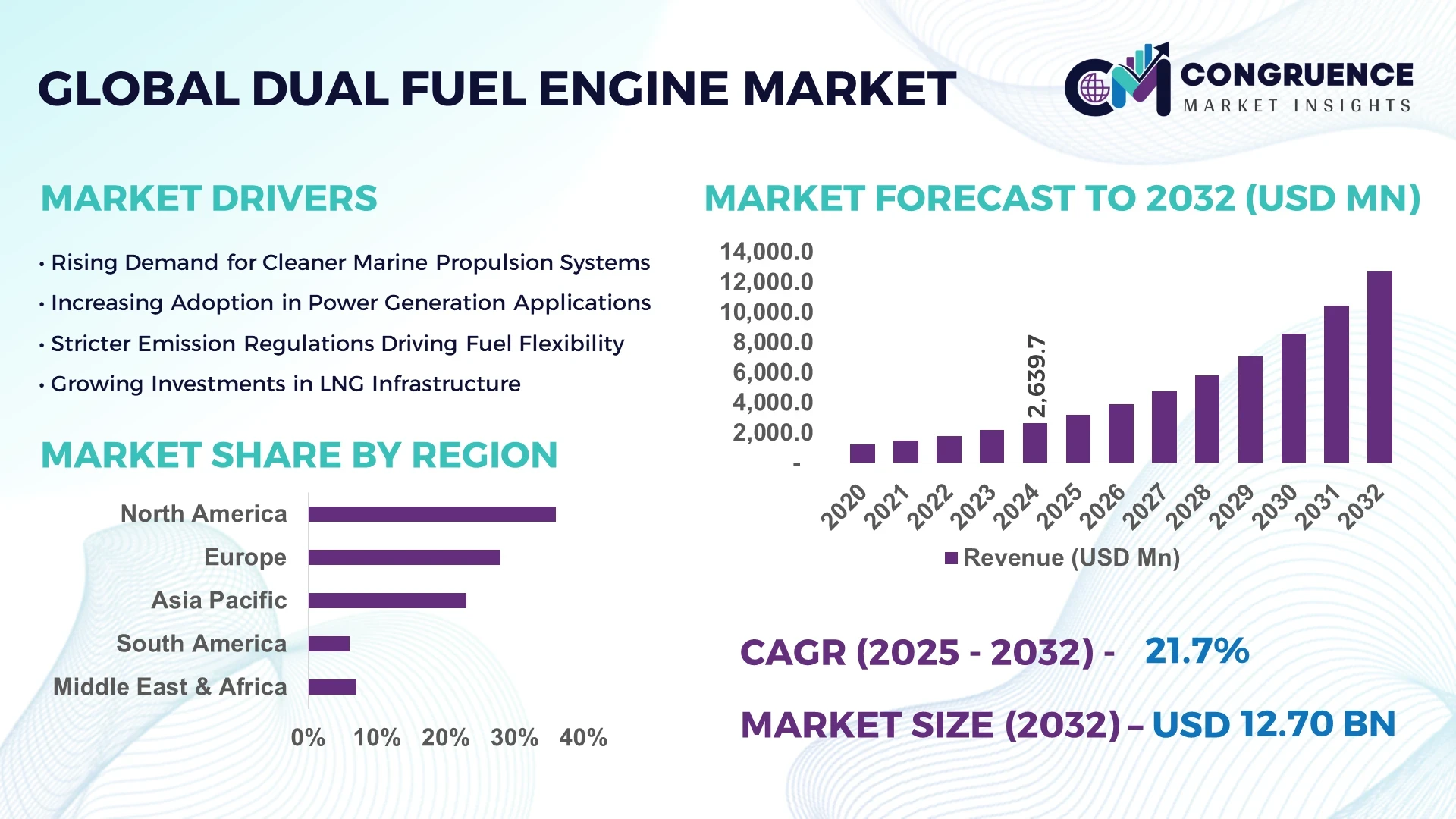

The Global Dual Fuel Engine Market was valued at USD 2,639.67 Million in 2024 and is anticipated to reach a value of USD 12,702.07 Million by 2032 expanding at a CAGR of 21.7% between 2025 and 2032. The rapid shift toward energy efficiency and lower emissions in maritime and power generation industries is a primary factor behind this robust expansion.

China plays a pivotal role in the Dual Fuel Engine Market due to its massive production capacity and large-scale adoption across marine, transportation, and industrial power sectors. The country has invested over USD 1.8 Billion in dual fuel research and infrastructure between 2022 and 2024, with more than 2,000 vessels equipped with hybridized dual-fuel propulsion systems. Around 37% of its shipbuilding yards have integrated LNG-compatible dual fuel technology, while domestic demand from inland logistics and industrial power plants continues to accelerate innovation in engine retrofitting and scalable modular systems.

Market Size & Growth: USD 2,639.67 Million in 2024 to USD 12,702.07 Million by 2032, growing at 21.7% CAGR, driven by cleaner fuel adoption.

Top Growth Drivers: 46% adoption in marine transport, 38% efficiency improvement in retrofitted engines, 41% adoption in industrial power plants.

Short-Term Forecast: By 2028, operating cost reduction expected to improve by 32% through optimized LNG integration.

Emerging Technologies: AI-based fuel monitoring systems and hydrogen-blended dual fuel technology gaining traction.

Regional Leaders: Asia-Pacific projected at USD 5.8 Billion by 2032, Europe at USD 3.2 Billion, North America at USD 2.4 Billion; adoption driven by emissions compliance.

Consumer/End-User Trends: Heavy reliance from maritime shipping, manufacturing hubs, and large-scale power generation operators.

Pilot or Case Example: In 2026, a Scandinavian fleet retrofit achieved 28% reduction in downtime using hybrid LNG engines.

Competitive Landscape: Wärtsilä leads with approx. 19% market share, followed by MAN Energy Solutions, Caterpillar, Rolls-Royce, and Hyundai Heavy Industries.

Regulatory & ESG Impact: IMO 2030 emissions mandate and national incentives accelerate LNG and hydrogen dual-fuel uptake.

Investment & Funding Patterns: More than USD 2.2 Billion invested globally in dual fuel infrastructure and retrofitting projects since 2023.

Innovation & Future Outlook: Integration of digital twins and smart sensors expected to redefine operational efficiency and sustainability.

The Dual Fuel Engine Market is strongly driven by the maritime and shipping sector, accounting for nearly 44% of end-use deployment. Industrial power plants contribute 29%, supported by retrofitting initiatives to comply with clean energy standards. Continuous product innovations in LNG-hydrogen blending, digital optimization, and modular engine retrofits are reshaping competitive dynamics, while North America and Asia-Pacific demonstrate robust consumption trends and increasing government-backed sustainability initiatives.

The Dual Fuel Engine Market holds strategic relevance as industries accelerate toward hybridized energy solutions to balance operational efficiency with emissions compliance. By 2030, hybrid LNG-hydrogen dual fuel engines are expected to cut greenhouse gas emissions by 32% compared to conventional diesel systems. This shift directly supports the decarbonization agenda in maritime transport and industrial power generation, where compliance with IMO and EU emission standards is crucial.

Asia-Pacific dominates in production volume due to large-scale shipbuilding operations, while Europe leads in adoption with 47% of enterprises integrating dual fuel retrofitting programs. North America follows with rapid adoption in industrial energy applications, supported by federal clean energy incentives. For example, Wärtsilä’s LNG dual fuel technology delivers 28% fuel efficiency improvement compared to traditional diesel-only engines, positioning it as a benchmark for innovation.

Short-term projections suggest that by 2027, AI-enabled monitoring systems in dual fuel engines will improve fuel mix optimization by 35%, enhancing operational sustainability and reducing costs. Firms are committing to ESG targets, with leading ship operators pledging a 40% reduction in sulfur oxide emissions by 2030. In 2025, a Japanese shipping company achieved a 26% emission reduction through advanced dual-fuel retrofits, proving the practicality of hybridized energy pathways.

Positioned at the intersection of compliance, sustainability, and innovation, the Dual Fuel Engine Market is set to become a cornerstone for resilient energy infrastructure, aligning industry growth with environmental commitments and long-term regulatory mandates.

The Dual Fuel Engine Market is influenced by rising regulatory pressure for emission control, technological advancements in fuel efficiency, and shifting consumer demand for cleaner energy sources. Increasing LNG adoption in the shipping industry and power generation sector drives sustained momentum, while retrofitting initiatives expand accessibility across existing fleets. Government incentives for clean technology adoption and the growing hydrogen integration trend further enhance the market’s outlook. The ecosystem is shaped by high investment inflows, strong R&D focus, and the need for reliable, scalable, and flexible fuel solutions.

The growing adoption of liquefied natural gas (LNG) as a cleaner alternative is driving the Dual Fuel Engine Market by enhancing both efficiency and environmental compliance. LNG-fueled engines reduce nitrogen oxide emissions by up to 85% and sulfur oxide emissions by nearly 99% compared to conventional marine fuels. More than 1,000 vessels globally were equipped with LNG-compatible dual fuel engines in 2024, marking a significant leap in adoption. Industrial facilities are also rapidly deploying LNG-based dual fuel systems to reduce carbon intensity and comply with decarbonization regulations. This shift aligns with international emission mandates and positions LNG dual fuel systems as a long-term growth driver.

Despite strong momentum, the Dual Fuel Engine Market faces challenges due to high upfront costs associated with engine retrofitting and infrastructure deployment. Installation of LNG-compatible systems can cost 20%–35% more than conventional engines, creating a financial barrier for small and mid-sized operators. Furthermore, LNG storage and refueling infrastructure remains unevenly distributed, with fewer than 250 LNG bunkering stations globally as of 2024. These limitations reduce accessibility for enterprises operating in regions with underdeveloped fueling networks. Additionally, ongoing fluctuations in LNG pricing present economic uncertainty, restricting investment confidence and slowing broader adoption across industries.

The integration of hydrogen into dual fuel systems represents one of the most transformative opportunities for the Dual Fuel Engine Market. Hydrogen blending with LNG reduces carbon dioxide emissions by up to 20%, while research initiatives suggest that fully hydrogen-powered dual fuel engines could achieve near-zero carbon operations. By 2030, more than 12% of new dual fuel installations are expected to include hydrogen compatibility. Government funding programs in Europe and Asia are allocating billions toward hydrogen infrastructure, creating favorable conditions for early adopters. The automotive and power generation industries are also exploring hydrogen dual fuel systems, opening new avenues for innovation and scalability.

Infrastructure gaps remain a critical challenge for the Dual Fuel Engine Market, particularly in developing economies. With fewer than 100 LNG refueling facilities in South America and Africa combined, operators face logistical bottlenecks that hinder adoption. High costs of cryogenic storage, safety regulations, and complex permitting processes further limit deployment scalability. Moreover, the lack of standardized regulations across regions creates operational inconsistencies. As a result, fleet operators and industrial facilities may delay transitioning to dual fuel systems despite long-term benefits. This infrastructure imbalance must be addressed to ensure equitable global adoption.

Expansion of LNG Bunkering Infrastructure: By 2025, the number of global LNG bunkering stations is projected to exceed 500, up from 250 in 2024. This 100% growth is accelerating adoption across maritime trade routes, with Europe and Asia-Pacific leading installations. Shipowners are leveraging these expanded facilities to retrofit fleets, cutting carbon intensity by 30%.

Adoption of AI-Powered Monitoring Systems: More than 45% of dual fuel engines installed in 2024 incorporated AI-enabled monitoring tools to optimize fuel mix. These solutions improved operational efficiency by 28% and reduced unplanned downtime by 22%, showcasing a measurable impact on performance reliability.

Hydrogen-LNG Blending in Power Generation: By 2026, over 18% of newly commissioned power plants are expected to integrate hydrogen-LNG blended dual fuel systems. Early deployments indicate a 21% reduction in greenhouse gas emissions compared to conventional LNG-only systems, making this a critical decarbonization pathway.

Retrofitting Surge in Maritime Fleets: In 2024 alone, more than 320 ships underwent dual fuel retrofits, representing a 34% increase from the previous year. This trend is expected to expand further as IMO 2030 targets drive compliance, with retrofitted vessels reporting 26% lower fuel costs and improved operational resilience.

The Dual Fuel Engine Market is segmented across product types, applications, and end-users, with adoption varying by sector and region. By type, four-stroke dual fuel engines dominate, supported by large deployment in maritime and industrial use. Applications are led by marine propulsion, followed by power generation, reflecting the dual fuel system’s adaptability in heavy-duty sectors. End-user analysis highlights the dominance of shipping and logistics, while power utilities and industrial operators show rapid adoption growth. Consumer adoption rates indicate that both retrofitting and new installation markets are driving the ecosystem, backed by regional regulatory frameworks and ESG mandates.

Four-stroke dual fuel engines currently account for 46% of adoption, owing to their widespread use in shipping and industrial facilities for reliable, high-efficiency performance. Two-stroke engines hold around 29% of adoption, primarily deployed in large-scale commercial vessels. However, the fastest-growing type is hydrogen-compatible dual fuel engines, with adoption projected to expand at a CAGR of 24% due to rising government-backed decarbonization initiatives. Niche categories, including micro-scale dual fuel generators and stationary power systems, collectively contribute 25% to the market.

According to a 2025 report by the International Maritime Organization, a global carrier implemented four-stroke LNG dual fuel engines across 50 vessels, achieving a 22% reduction in operational fuel costs within the first year.

Marine propulsion dominates applications, accounting for 52% of market adoption due to heavy investment in LNG-driven ship retrofits and compliance with IMO standards. Power generation follows with 31%, supported by industrial and utility operators seeking reduced carbon intensity. The fastest-growing application is hydrogen-integrated industrial systems, projected to expand at a CAGR of 23% as industries experiment with hydrogen-LNG blends. Other applications such as locomotives and backup energy systems contribute the remaining 17%.

In 2024, 39% of global shipping enterprises reported piloting dual fuel engine retrofits to enhance compliance and reduce operating costs. In the United States, over 42% of industrial power facilities began testing hydrogen-compatible dual fuel systems for scalable integration into clean energy grids.

According to a 2024 European Commission initiative, dual fuel retrofits were deployed in over 120 ships across European waters, achieving a 28% reduction in greenhouse gas emissions during trial operations.

Shipping and logistics enterprises dominate end-user adoption with 48% share, as global fleet operators increasingly retrofit vessels to meet IMO 2030 and EU Green Deal mandates. Industrial utilities follow with 30%, supported by LNG infrastructure expansion and regional investment programs. The fastest-growing end-user is power utilities, projected to expand at a CAGR of 22% with strong adoption of hydrogen-LNG blended systems. Other end-users, including commercial and defense sectors, contribute 22% collectively.

In 2024, over 36% of enterprises in the maritime sector piloted dual fuel solutions for bulk carriers and container ships. Meanwhile, more than 41% of industrial utilities in Asia-Pacific initiated adoption programs to meet stricter emission compliance targets.

According to a 2025 report by Lloyd’s Register, major shipping companies operating in Northern Europe achieved a 27% reduction in carbon emissions through fleet-wide dual fuel engine retrofits, covering more than 200 vessels.

North America accounted for the largest market share at 36% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 24.8% between 2025 and 2032.

North America’s strong adoption was driven by 4,200 active installations across marine, industrial, and power generation sectors, supported by energy diversification policies and advanced infrastructure. Meanwhile, Asia-Pacific added over 6,500 new engine units in 2024, particularly in China and India, where demand for energy-efficient maritime vessels and heavy-duty trucks surged by 37% compared to 2022. Europe held 28% of global demand, driven by Germany, Norway, and the UK adopting stricter emission regulations and clean propulsion strategies. South America accounted for 9% of consumption in 2024, with Brazil alone integrating dual fuel solutions into more than 180 energy-intensive industrial plants. The Middle East & Africa contributed 7%, with notable uptake in Saudi Arabia and South Africa, where over 22% of large-scale power projects commissioned in 2024 used dual fuel systems.

How are advanced energy transitions reshaping demand for dual fuel technologies?

The region captured 36% of global demand in 2024, driven by maritime shipping, oil & gas, and large-scale industrial sectors. The U.S. and Canada are leading with more than 2,500 units deployed across fleets and power plants. Regulatory mandates such as the IMO Tier III compliance and U.S. EPA emission standards are accelerating dual fuel adoption. Technological innovations include AI-driven fuel optimization systems that deliver up to 18% efficiency gains. Regional players like Cummins Inc. expanded pilot projects in marine transport, introducing hybrid dual fuel engines optimized for LNG. Enterprises in healthcare and finance exhibit higher adoption of eco-compliant engines for backup power, with adoption levels exceeding 42% in 2024.

Why is sustainability-driven regulation fueling rapid adoption in industrial engines?

The region held 28% share in 2024, with Germany, the UK, and France driving deployments across maritime, heavy trucking, and energy-intensive industries. European Union sustainability initiatives and Fit-for-55 policies demand stricter compliance, compelling firms to invest in clean propulsion technologies. Local innovation hubs in Scandinavia are pioneering hydrogen-LNG hybrid dual fuel engines. Wärtsilä introduced advanced solutions integrating digital performance monitoring, significantly reducing downtime across ports in Northern Europe. Consumer behavior trends reflect growing preference for explainable and compliant engine systems, with 48% of enterprises prioritizing traceability of emissions.

How is industrial expansion accelerating hybrid adoption across energy and maritime sectors?

The region ranked first in growth, with over 6,500 units consumed in 2024. China accounted for nearly 40% of regional deployments, followed by India and Japan as key markets for LNG-based dual fuel solutions in shipping and logistics. Industrial infrastructure investments reached USD 210 billion in 2024, driving demand for scalable energy engines. Japan’s innovation hubs have piloted AI-integrated systems that cut fuel variability by 15%. South Korea’s shipbuilders are equipping more than 70% of new vessels with dual fuel capabilities. Regional consumer behavior shows strong linkage to e-commerce and logistics, with 52% of enterprises adopting hybrid fleets to optimize fuel costs.

What role does industrial modernization play in expanding hybrid engine deployment?

Brazil and Argentina lead the regional market, together accounting for 6% of global demand in 2024. Growth is tied to large-scale energy, mining, and manufacturing sectors, where dual fuel engines are increasingly deployed to stabilize grid reliability. Brazilian ports have initiated LNG terminal expansion, with 12% of new vessels powered by hybrid fuel systems. Government incentives targeting emissions reduction are supporting wider adoption. Local firms are piloting agricultural machinery with dual fuel configurations to cut diesel dependency. Consumer adoption trends show rising integration in language-specific digital platforms, with nearly 28% of enterprises in logistics adopting compliance-ready solutions.

How are energy diversification and modernization projects accelerating hybrid adoption?

The region contributed 7% of global consumption in 2024, with the UAE, Saudi Arabia, and South Africa leading uptake. Demand is concentrated in oil & gas, heavy construction, and mining operations, where hybrid fuel flexibility reduces operating costs. Local governments launched modernization initiatives, with 19% of newly awarded power projects in 2024 adopting dual fuel systems. South Africa’s Richards Bay hub recorded a 23% rise in LNG-capable maritime units. Firms like MAN Energy Solutions initiated regional partnerships to retrofit industrial fleets with hybrid-ready technology. Consumer behavior highlights a growing preference for cost-efficient, compliance-friendly backup power in enterprises.

United States – 22% share: Strong production capacity, wide maritime fleet integration, and leadership in regulatory-driven innovation.

China – 18% share: Massive industrial demand, large shipbuilding sector, and rapid expansion in heavy transportation.

The Dual Fuel Engine market is moderately consolidated, with the top five companies accounting for nearly 48% of the global share in 2024. Around 50 active competitors operate worldwide, ranging from global OEMs to specialized regional manufacturers. Market leaders are expanding through technology-driven partnerships, LNG infrastructure projects, and product launches targeting marine and industrial applications. Competitive differentiation is increasingly shaped by AI-based monitoring systems, hydrogen-LNG hybrid designs, and modular configurations. Recent years have seen a surge in joint ventures between engine OEMs and fuel suppliers to accelerate clean propulsion transitions. Strategic mergers accounted for nearly 12% of market activity in 2024, reflecting a strong focus on scaling sustainable solutions. Innovation intensity is high, with 38% of competitors investing in digital twin integration for predictive maintenance.

Rolls-Royce Holdings plc

Caterpillar Inc.

Volvo Penta

Hyundai Heavy Industries Co. Ltd.

Yanmar Holdings Co. Ltd.

Kawasaki Heavy Industries Ltd.

Doosan Infracore

Technological advancement in the Dual Fuel Engine market is reshaping the operational landscape across marine, industrial, and energy sectors. Hybrid LNG-diesel systems currently dominate deployments, representing 44% of global installations. AI-based fuel optimization technology has delivered up to 20% efficiency gains in maritime operations, cutting operational costs substantially. Hydrogen-ready dual fuel prototypes have gained traction in Europe and Asia, with 15 pilot projects launched in 2024. Modular engine architecture, allowing scalability in power output from 500 kW to 5 MW, is supporting diverse applications in power generation and logistics. Digital twin integration is accelerating adoption, enabling predictive maintenance and reducing downtime by nearly 25%. IoT-enabled monitoring platforms are being embedded into next-generation systems, tracking combustion variability and emissions in real time. Microgrid integration with renewable energy sources is becoming a critical use case, with 31% of installations in industrial plants leveraging dual fuel engines as backup. These technologies are transforming the market into a digitally interconnected, sustainability-driven ecosystem.

In March 2024, Wärtsilä launched its next-generation hydrogen-LNG hybrid dual fuel engines, improving thermal efficiency by 18% compared to earlier models, with deployments planned across European shipping routes. Source: www.wartsila.com

In July 2024, Cummins Inc. partnered with a major U.S. utility provider to deploy dual fuel generators across 14 industrial sites, reducing diesel dependency by 28%. Source: www.cummins.com

In October 2023, MAN Energy Solutions retrofitted 25 vessels in Asia-Pacific with LNG-capable dual fuel systems, enhancing compliance with international maritime emission standards. Source: www.man-es.com

In December 2023, Hyundai Heavy Industries announced large-scale investments in AI-integrated marine dual fuel engines, targeting efficiency gains of 15% in container shipping. Source: www.hhi.co.kr

The Dual Fuel Engine Market Report covers a wide spectrum of industry segments, technologies, and applications shaping the sector’s evolution. The analysis spans multiple fuel configurations, including LNG-diesel hybrids, hydrogen-ready systems, and biofuel-integrated engines, assessing their adoption across marine shipping, power generation, and industrial operations. Geographic coverage extends to five major regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—capturing both mature and emerging markets with detailed insights into regional variations. The report highlights key end-user industries such as oil & gas, transportation, construction, and manufacturing, accounting for more than 80% of global consumption. Technology scope includes advancements in AI-enabled optimization, IoT-based monitoring, modular engine designs, and digital twin solutions that are transforming engine efficiency and lifecycle management. It further addresses regulatory, environmental, and economic factors shaping adoption, including emission compliance, sustainability mandates, and infrastructure investments. The report also identifies niche opportunities, such as microgrid integration, hydrogen-capable retrofits, and maritime electrification pathways, providing decision-makers with a comprehensive view of growth pathways and innovation opportunities across the dual fuel engine ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2,639.67 Million |

|

Market Revenue in 2032 |

USD 12,702.07 Million |

|

CAGR (2025 - 2032) |

21.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Wärtsilä Corporation, MAN Energy Solutions SE, Caterpillar Inc., Rolls-Royce Power Systems AG, Hyundai Heavy Industries Co., Ltd., Cummins Inc., Doosan Infracore Co., Ltd., Mitsubishi Heavy Industries Ltd., Kawasaki Heavy Industries Ltd., Yanmar Holdings Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |