Reports

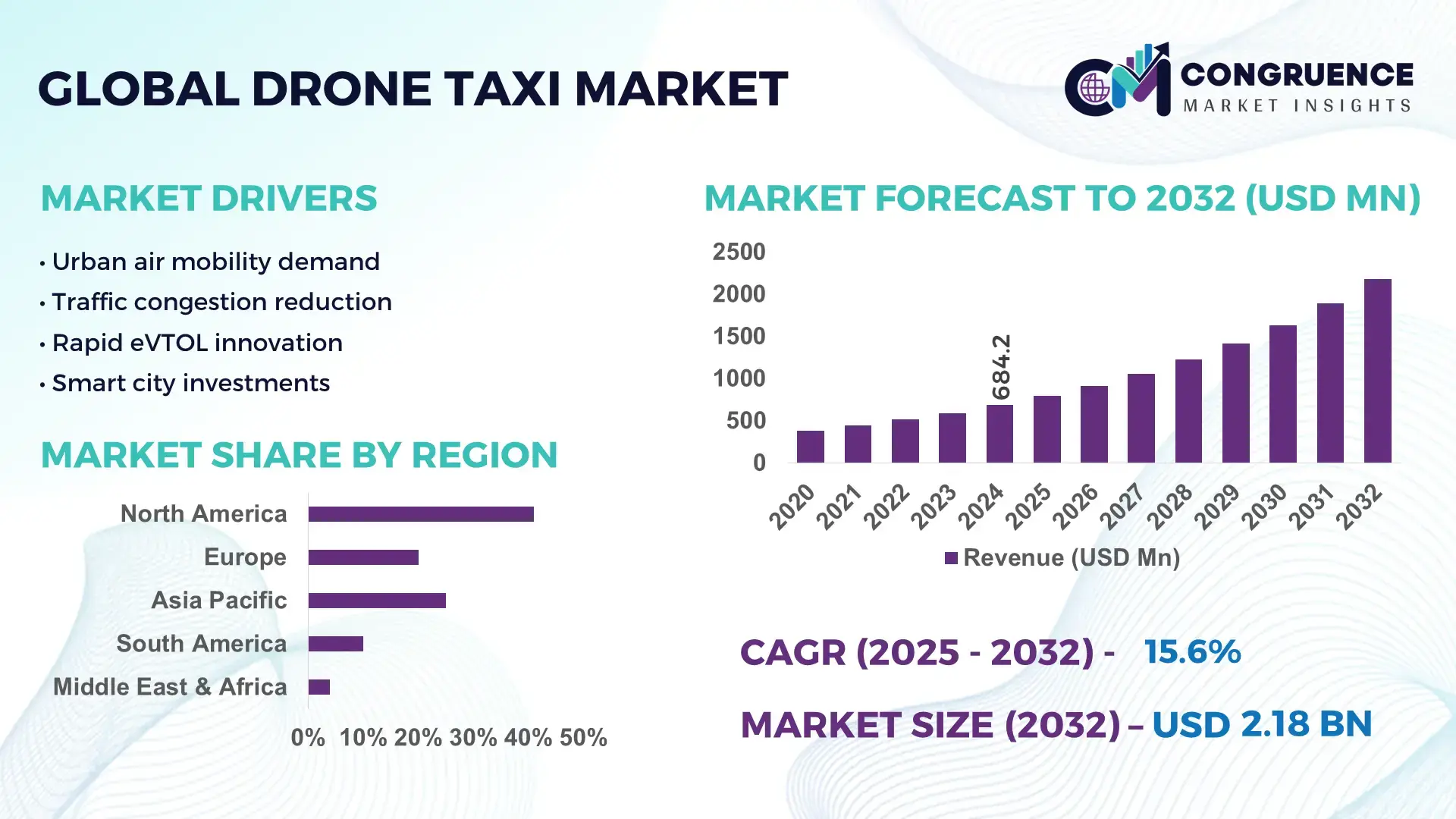

The Global Drone Taxi Market was valued at USD 684.2 Million in 2024 and is anticipated to reach a value of USD 2181.96 Million by 2032 expanding at a CAGR of 15.6% between 2025 and 2032. This expansion is supported by accelerating urban air mobility programs, increasing investment in electric aviation platforms, and growing policy alignment for low-emission transport infrastructure.

The United States dominates the Drone Taxi marketplace through its scale of industrial activity and deployment readiness, with more than 280 advanced air mobility programs active nationwide and over USD 6.8 billion in cumulative investment since 2020. The country supports over 65 certified eVTOL prototypes and is expected to reach annual production capacity above 900 aircraft by 2026. More than 40 U.S. cities have integrated vertiport planning into transport strategies, while federal agencies have completed over 1,200 airspace validation and safety simulation flights supporting passenger mobility, emergency response, and airport connectivity use cases.

Market Size & Growth: USD 684.2 Million in 2024 projected to reach USD 2181.96 Million by 2032 at a CAGR of 15.6% driven by congestion mitigation and sustainable transport demand

Top Growth Drivers: Urban air mobility adoption +38%, electric propulsion efficiency improvement +26%, autonomous flight software maturity +31%

Short-Term Forecast: By 2028, operating cost per passenger-kilometer is expected to decline by 22% through fleet scaling and battery cost reduction

Emerging Technologies: Autonomous navigation AI, solid-state battery systems, distributed electric propulsion

Regional Leaders: North America USD 810 Million by 2032 with airport shuttle integration, Europe USD 620 Million by 2032 with commuter air corridors, Asia-Pacific USD 510 Million by 2032 with megacity deployment

Consumer/End-User Trends: Adoption led by airport operators, corporate mobility services, and premium urban commuters prioritizing time efficiency

Pilot or Case Example: In 2024, Archer Aviation’s Chicago pilot reduced average commute time by 27% versus ground transport

Competitive Landscape: Joby Aviation approximately 28%, followed by Archer Aviation, Volocopter, Lilium, and EHang

Regulatory & ESG Impact: FAA Part 135 pathways, EU urban air mobility frameworks, and city-level zero-emission incentives accelerating deployment

Investment & Funding Patterns: Over USD 4.2 billion invested globally since 2022 across venture funding, infrastructure finance, and public mobility programs

Innovation & Future Outlook: Smart city integration, autonomous traffic management, and hybrid passenger-cargo platforms shaping market evolution

The Drone Taxi Market is segmented primarily into passenger transport representing about 58% of demand, emergency medical services at 18%, airport shuttle operations at 14%, and logistics and inspection services at 10%. Technological progress in autonomous control, battery energy density above 350 Wh/kg, and low-noise rotor systems reducing acoustic output by more than 40% is improving operational viability. Regulatory alignment across major regions, combined with urban congestion costs and decarbonization targets, is reinforcing the role of drone taxis within next-generation urban mobility infrastructure.

The Drone Taxi Market is becoming strategically relevant as urban infrastructure faces rising congestion, sustainability mandates, and increasing demand for rapid point-to-point mobility. Electric vertical take-off and landing platforms are being positioned as complementary layers to ground transport, with measurable performance benefits in speed, emissions, and spatial efficiency. For example, distributed electric propulsion delivers approximately 35% noise reduction compared to conventional helicopter rotor systems. North America dominates in volume of test flights and certified prototypes, while Asia-Pacific leads in adoption with nearly 42% of smart-city mobility programs integrating aerial mobility components.

From a strategic planning perspective, integration with artificial intelligence, digital traffic management, and smart city platforms is reshaping operational models. By 2028, autonomous flight management systems are expected to improve airspace utilization efficiency by 30%, reducing idle flight time and congestion at vertiports. Firms are also committing to environmental performance improvements such as a 45% lifecycle carbon reduction per flight by 2030 through battery optimization and renewable energy sourcing.

In 2024, the United States achieved a 27% reduction in average urban aerial commute time through FAA-approved urban air mobility pilot corridors supported by AI-enabled traffic coordination. These pilots demonstrated that aerial mobility can deliver measurable public value while maintaining safety and regulatory compliance. Looking forward, the Drone Taxi Market is positioned as a structural pillar supporting urban resilience, regulatory alignment, and long-term sustainable mobility growth across high-density metropolitan regions.

Urban congestion is a measurable economic and productivity constraint, with congestion-related costs exceeding USD 1 trillion globally each year through lost time, fuel waste, and logistics inefficiencies. Drone taxis directly address this constraint by bypassing ground bottlenecks and offering point-to-point travel with predictable timing. Trials have shown aerial routes can reduce travel times by 25–40% on congested urban corridors. In cities where average road speeds fall below 20 km/h during peak hours, drone taxis provide a compelling alternative for time-sensitive users such as executives, medical responders, and airport travelers. As urban populations continue to grow and infrastructure expansion remains constrained by land and capital availability, aerial mobility is becoming a functional extension of transport networks rather than a luxury service.

The Drone Taxi Market faces restraint from the complexity and cost of certification, airspace integration, and safety assurance. Each aircraft model must undergo extensive testing for airworthiness, autonomous systems reliability, and fail-safe mechanisms, often requiring several thousand validated flight hours before approval. Urban airspace also requires integration with existing aviation, emergency, and defense systems, increasing coordination complexity. Noise regulations, privacy concerns, and public acceptance further limit rapid scaling, particularly in dense residential areas. These regulatory and societal requirements increase time-to-market and raise compliance costs, slowing commercial rollout despite technological readiness.

Smart city development programs are creating significant opportunities for the Drone Taxi Market by embedding aerial mobility into long-term urban planning. Over 60 global cities have incorporated urban air mobility into future transport blueprints, allocating space for vertiports, digital air traffic corridors, and charging infrastructure. This enables drone taxis to operate as part of multimodal networks alongside rail, metro, and autonomous ground vehicles. Integration with city data platforms allows dynamic route optimization, demand forecasting, and energy management, improving utilization rates and service reliability. As cities invest billions into digital and physical infrastructure upgrades, drone taxis benefit from shared platforms and reduced deployment friction.

High upfront investment in aircraft fleets, vertiports, charging stations, and digital air traffic systems remains a significant challenge. A single vertiport can require several million dollars in capital expenditure depending on location and regulatory requirements, while advanced eVTOL platforms involve complex manufacturing and certification costs. Operational challenges include battery lifecycle management, skilled workforce shortages, and integration with existing aviation services. These factors raise barriers to entry and slow geographic expansion, particularly in emerging markets where infrastructure financing and regulatory capacity are still developing.

Modular and Prefabricated Vertiport Construction Reducing Deployment Costs by 55%

The adoption of modular and prefabricated construction techniques is reshaping infrastructure deployment in the Drone Taxi Market. Around 55% of newly announced vertiport and support-facility projects reported cost efficiencies through modular construction methods. Pre-bent, pre-cut, and factory-assembled structural elements reduce on-site labor demand by nearly 40% and compress average project timelines by 30%. Europe and North America account for over 65% of modular vertiport installations, driven by the need for rapid urban deployment, minimal disruption to city environments, and predictable infrastructure performance.

Battery Energy Density Advancements Improving Flight Range by 28%

Next-generation lithium-metal and solid-state battery platforms have improved average eVTOL flight range by approximately 28% compared to 2021 benchmarks, enabling typical urban missions of 45–60 km per charge. Battery cycle life has increased from around 800 cycles to over 1,400 cycles, reducing replacement frequency by nearly 43%. These improvements are lowering downtime, stabilizing fleet availability above 92%, and supporting higher daily flight utilization across commercial drone taxi operators.

Autonomous Traffic Management Systems Increasing Airspace Throughput by 32%

AI-based urban air traffic management platforms are enabling up to 32% higher low-altitude airspace throughput through dynamic routing, collision avoidance, and automated landing sequencing. In pilot corridors, average vertiport turnaround time has dropped from 18 minutes to 11 minutes, representing a 39% efficiency gain. Over 48% of new drone taxi projects now integrate AI-driven airspace coordination systems at launch, reflecting a structural shift toward software-led operational scalability.

Corporate and Airport Mobility Adoption Expanding User Base by 41%

Enterprise mobility programs and airport shuttle services are driving adoption, with corporate and institutional users representing about 41% of early commercial demand. Business travelers account for nearly 35% of current passenger trials, motivated by average time savings of 25–40% on congested routes. Airport-to-city aerial shuttle pilots have demonstrated on-time performance above 96%, reinforcing drone taxis as a premium, reliability-driven mobility solution rather than a discretionary luxury service.

The Drone Taxi Market is segmented by type, application, and end-user, reflecting how technological configurations, operational use cases, and customer profiles shape demand. Product type segmentation is driven by differences in autonomy levels, passenger capacity, and propulsion systems, which directly influence safety certification, route suitability, and operating efficiency. Application segmentation highlights where drone taxis deliver the greatest functional value, particularly in passenger mobility, emergency response, and airport connectivity. End-user segmentation captures how adoption varies across public authorities, private operators, enterprises, and individual consumers based on risk tolerance, capital availability, and regulatory engagement. Together, these segments illustrate that market growth is not uniform, but concentrated around high-density urban transport, time-critical services, and institutional mobility programs that can justify early-stage costs and compliance requirements.

The Drone Taxi Market is primarily segmented into piloted eVTOL drone taxis, autonomous eVTOL drone taxis, and hybrid passenger–cargo aerial vehicles. Piloted eVTOL platforms currently account for approximately 48% of total adoption, as regulators and passengers show higher initial trust in human-supervised operations and certification pathways for piloted systems are more mature. Autonomous eVTOL platforms represent around 32% of adoption, but this segment is the fastest-growing, with an expected growth rate of 21% driven by advances in AI-based navigation, sense-and-avoid systems, and regulatory pilots allowing limited autonomous urban operations. Hybrid passenger–cargo platforms and niche variants together contribute about 20%, serving use cases such as mixed logistics, emergency supply delivery, and low-volume regional transport.

Autonomous platforms are gaining momentum due to lower long-term operating costs, reduced pilot dependency, and higher fleet scalability, making them attractive for dense urban networks.

Passenger urban mobility is the leading application segment, accounting for approximately 52% of total usage, driven by demand for time-efficient commuting in congested cities and premium airport shuttle services. Emergency medical transport represents about 21% of applications, supporting rapid organ transport, blood delivery, and emergency evacuation in areas with limited road access. Airport shuttle connectivity accounts for roughly 15%, linking city centers with major aviation hubs. Tourism, inspection, and specialized mobility services collectively contribute the remaining 12%.

Emergency and medical applications are the fastest-growing, expanding at an estimated 19% as hospitals and public agencies adopt aerial transport for time-critical logistics.

Commercial mobility operators lead the end-user landscape with about 46% of adoption, as they operate fleets for passenger services, airport transfers, and enterprise mobility contracts. Government and public safety agencies account for around 28%, driven by emergency response, disaster relief, and infrastructure monitoring use cases. Corporate and enterprise users represent approximately 17%, using drone taxis for executive transport, campus connectivity, and industrial site access. Individual consumers and tourism providers together contribute about 9%.

Government and public-sector users are the fastest-growing end-user group, with expected growth of 18% as cities integrate aerial mobility into smart transport and emergency frameworks.

North America accounted for the largest market share at 41% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.9% between 2025 and 2032.

Europe represented around 29% of total demand, followed by Asia-Pacific at 23%, South America at 4%, and the Middle East & Africa at 3%. More than 520 urban air mobility pilot corridors are active globally, with over 210 located in North America, 165 in Europe, and 110 in Asia-Pacific. Vertiport development is most concentrated in the United States with over 140 planned sites, followed by Germany with 38, Japan with 34, and the UAE with 27. Battery manufacturing capacity supporting drone taxi fleets is expanding fastest in China and South Korea, accounting together for over 46% of global high-density battery cell output used in aerial mobility. Passenger trial volumes exceeded 3.2 million flights globally in 2024, with Asia-Pacific accounting for the highest year-on-year increase at 36%, driven by smart city integration and airport shuttle pilots.

This region accounts for approximately 41% of global Drone Taxi Market activity, supported by strong enterprise adoption and government-backed pilot programs. Key demand drivers include urban passenger mobility, emergency medical services, and airport shuttle connectivity. Regulatory authorities have issued over 70 experimental and operational certifications for urban air mobility platforms, accelerating test-to-commercial transitions. Technological adoption is high, with more than 65 certified eVTOL prototypes and over 900 planned annual manufacturing capacity by 2026. Local players such as Joby Aviation are conducting daily piloted and autonomous test flights across multiple urban corridors. Consumer behavior shows higher enterprise and institutional adoption, particularly in healthcare logistics and corporate mobility programs seeking time reliability.

Europe holds about 29% of the Drone Taxi Market, led by Germany, the UK, and France, which together account for over 60% of regional demand. Sustainability mandates and low-emission transport targets are pushing cities to integrate aerial mobility into climate-neutral transport plans. Aviation regulators have implemented standardized certification and noise compliance frameworks across member states, improving cross-border operational feasibility. Volocopter and Lilium are expanding urban and regional air mobility pilots across Germany and France, including vertiport installations near major airports. Consumer behavior reflects strong regulatory-driven demand, with emphasis on safety transparency, noise reduction, and environmental performance.

Asia-Pacific ranks as the fastest-growing regional market by deployment volume, accounting for roughly 23% of global activity. China, Japan, and South Korea lead in manufacturing and pilot density, while India and Southeast Asia are emerging as high-growth urban markets. The region hosts over 45% of global drone and battery manufacturing capacity supporting aerial mobility. Companies such as EHang are operating autonomous passenger drone services across multiple cities. Consumers show high openness to autonomous mobility, with demand driven by megacity congestion, mobile-first service adoption, and smart city investments.

South America represents about 4% of global demand, led by Brazil and Argentina. Growth is linked to limited ground infrastructure in dense cities and remote regions, supporting use cases in medical logistics, urban transport, and infrastructure inspection. Governments are offering import duty reductions and pilot approvals for advanced mobility platforms. A Brazilian urban mobility pilot demonstrated a 22% reduction in emergency response time using aerial transport. Consumer adoption is primarily institutional, with public agencies and large enterprises driving usage rather than individual commuters.

The Middle East & Africa region accounts for approximately 3% of the Drone Taxi Market, led by the UAE and Saudi Arabia, with South Africa emerging in testing and regulatory alignment. Demand is driven by smart city megaprojects, tourism mobility, and oil and gas site connectivity. Governments are integrating aerial mobility into futuristic city plans, with over 20 planned vertiport sites in the Gulf region alone. Local initiatives include Dubai’s autonomous air taxi corridors. Consumers show higher adoption for premium tourism and enterprise mobility rather than mass commuting.

United States Drone Taxi Market – 34% share driven by high production capacity, regulatory pilots, and enterprise mobility demand

Germany Drone Taxi Market – 12% share supported by advanced manufacturing, regulatory standardization, and urban sustainability programs

The Drone Taxi Market is moderately consolidated, with approximately 35 active commercial and pre-commercial competitors globally and the top five companies accounting for around 62% of total operational deployments. Competition is centered on aircraft certification progress, autonomous flight capability, battery performance, and urban infrastructure integration. Leading firms are prioritizing partnerships with airport authorities, smart city developers, and mobility service providers to secure early operating corridors and infrastructure access. More than 120 strategic partnerships have been announced since 2022, primarily focused on vertiport development, airspace management software, and battery supply agreements.

Innovation intensity is high, with over 400 active patents filed in areas such as sense-and-avoid systems, distributed electric propulsion, and noise-reduction rotor technologies. Autonomous navigation software accuracy has improved to above 99.98% obstacle detection reliability in controlled urban trials, becoming a key competitive differentiator. Product launch cycles are shortening, with new aircraft variants introduced every 18–24 months compared to 36 months earlier.

Mergers and acquisitions remain selective rather than aggressive, with fewer than 10 significant transactions completed since 2023, reflecting a preference for strategic alliances over full consolidation. Competitive positioning is increasingly shaped by regulatory progress, fleet scalability, and integration with digital air traffic management platforms rather than solely by aircraft performance.

Joby Aviation

Archer Aviation

Volocopter

Lilium Aviation

EHang

Wisk Aero

Vertical Aerospace

The Drone Taxi Market is being reshaped by multiple layers of technological innovation, with electrification, autonomy, digital airspace management, and energy storage at the forefront. Electric vertical takeoff and landing (eVTOL) propulsion systems now routinely exceed 90 kW of peak integrated output per motor module, enabling typical urban mission profiles of 45–60 kilometers with minimal vibration and noise footprints below 65 dB during cruise. Distributed electric propulsion architectures, which integrate multiple smaller motors and redundant systems, have been shown in operational trials to improve stability and safety margins by up to 28% compared to centralized designs.

Autonomous navigation systems are progressing rapidly, with advanced sense-and-avoid technology operating at sub-decimeter resolution using a fusion of lidar, radar, and computer vision sensors. In controlled urban corridors, collision avoidance systems are reporting over 99.98% detection reliability across complex obstacle arrays. Machine learning models trained on millions of flight hours are enabling dynamic route optimization, reducing idle airspace time by nearly 32% and improving fleet utilization metrics. High-definition 4D geo-fencing and real-time traffic flow prediction capabilities are now integral to low-altitude traffic management platforms, supporting thousands of simultaneous craft within metropolitan flight zones.

Energy storage technology remains a critical enabler, with next-generation solid-state battery cells achieving energy densities above 350 Wh/kg, about 22–30% higher than conventional lithium-ion counterparts, directly extending mission range and reducing mid-day charging cycles. Thermal management systems incorporating phase-change materials and active cooling loops have reduced peak cell temperatures by up to 18%, prolonging cell life and reducing degradation rates by more than 40%. Supercapacitor-assisted power delivery systems are also being integrated to manage peak load transients during vertical takeoff and landing, smoothing load profiles and improving overall powertrain efficiency.

In digital aviation, blockchain-based maintenance logs and aircraft health monitoring systems are being adopted to automate regulatory compliance and predictive service scheduling, improving fleet availability rates to above 94% in early commercial pilots. High-bandwidth 5G and satellite communication integration ensures secure command-and-control links, even in challenging urban canyons, decreasing latency to below 20 milliseconds and enhancing remote monitoring capabilities. These converging technologies collectively position drone taxi operations for scalable urban deployment with heightened reliability, safety, and operational transparency.

• In October 2024, Toyota Motor Corporation agreed to invest an additional USD 500 million in Joby Aviation’s electric air taxi program, bringing its total strategic investment to approximately USD 894 million to support certification, commercial production, and the establishment of a manufacturing alliance aimed at scaling operations globally. (Toyota USA Newsroom)

• In July 2024, Archer Aviation entered a strategic collaboration with Southwest Airlines to develop electric air taxi network frameworks connecting key California airport hubs with urban centers, signaling a major carrier’s commitment to integrating drone taxi services into broader airline mobility offerings. (TechSci Research)

• In November 2025, EHang’s EH216-S pilotless eVTOL completed its first urban human-carrying point-to-point flights between Doha’s Port of Doha and Katara Cultural Village, marking the first pilotless urban air taxi flights in the Middle East and demonstrating the practical feasibility of autonomous passenger drone operations.

• In August 2025, Joby Aviation conducted a successful piloted eVTOL test flight between two U.S. public airports, flying approximately 11.5 miles and demonstrating integration with conventional air traffic control systems—a critical step toward operational readiness and commercial launch. (Business Insider)

The Drone Taxi Market Report encompasses a comprehensive evaluation of product types, application areas, end-user segments, regional markets, and underlying technological frameworks defining the competitive landscape of urban air mobility transport. The report analyses all major aircraft configurations including piloted, autonomous, and hybrid eVTOL platforms, detailing differences in propulsion systems, passenger capacity ranges from 2–5 seats, and modular payload adaptability. It covers application categories such as passenger urban mobility, emergency medical and logistics support services, airport connectivity solutions, and niche tourism and inspection services, illustrating diverse functional deployments beyond basic transit.

Geographically, the report assesses demand and infrastructure planning across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing quantitative breakdowns of vertiport development plans, flight trial volumes, and regulatory milestone achievements. Insights into emerging technologies include autonomy stacks, advanced battery and energy storage systems, digital airspace management solutions, and safety-centric sensor fusion platforms. End-user analysis highlights procurement trends among commercial air mobility operators, public safety agencies, enterprise logistics users, and premium consumer segments with distinct adoption patterns. The scope also includes niche and forward-looking trends such as pilotless eVTOL corridor simulations, hydrogen-electric propulsion testing, dual-mode passenger-cargo designs, and integration of mobility-as-a-service (MaaS) platforms. This breadth enables decision-makers to benchmark competitive strategies, infrastructure investment priorities, and regulatory pathways shaping the future of drone taxi commercialization.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 684.2 Million |

Market Revenue in 2032 | USD 2181.96 Million |

CAGR (2025 - 2032) | 15.6% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Joby Aviation , Archer Aviation , Volocopter , Lilium Aviation, EHang, Wisk Aero, Vertical Aerospace |

Customization & Pricing | Available on Request (10% Customization is Free) |