Reports

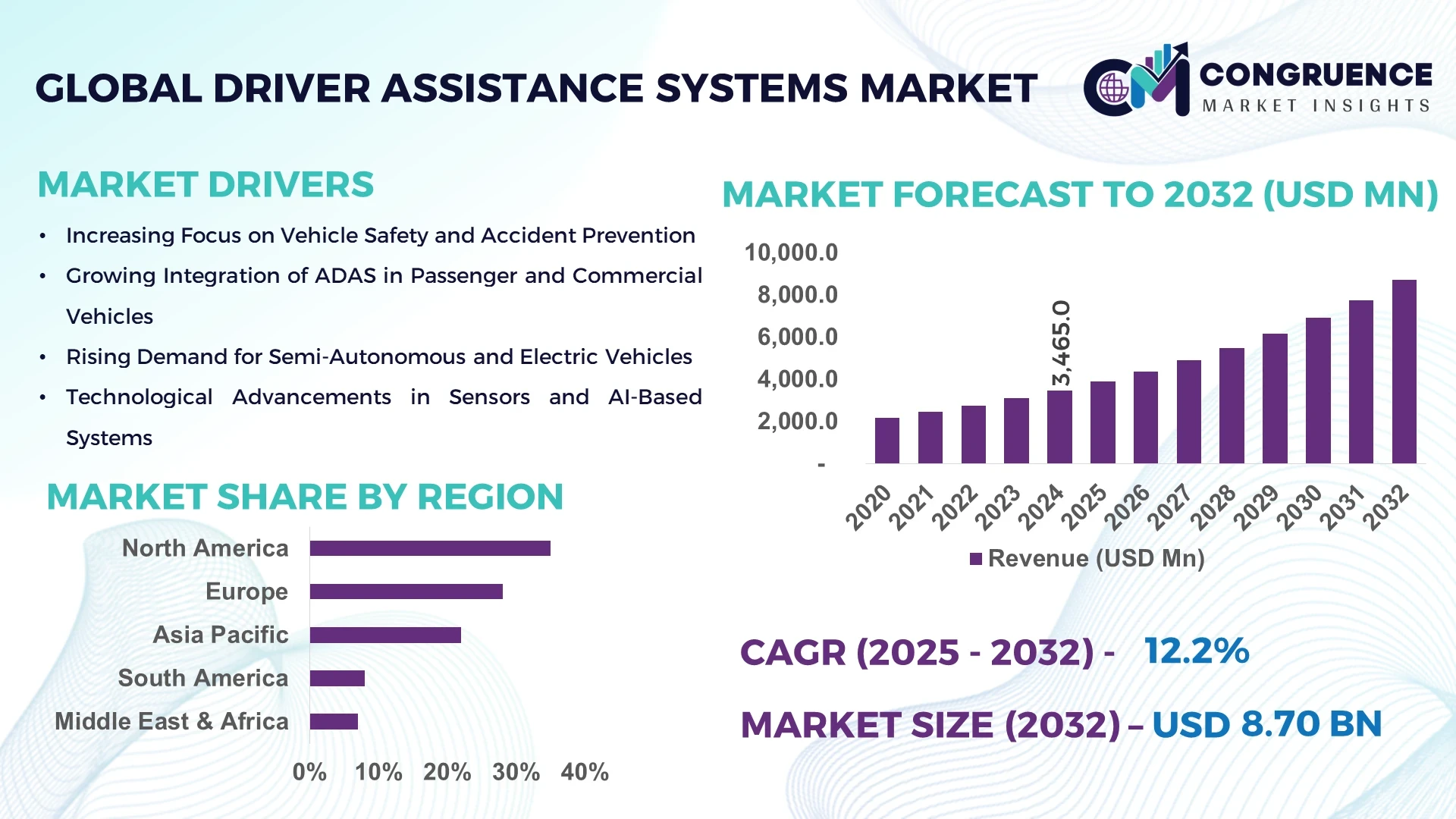

The Global Driver Assistance Systems Market was valued at USD 3,465.0 Million in 2024 and is anticipated to reach a value of USD 8,702.5 Million by 2032, expanding at a CAGR of 12.2% between 2025 and 2032. This growth is primarily driven by increasing consumer demand for enhanced vehicle safety features, advancements in sensor technologies, and the implementation of stringent safety regulations worldwide.

The United States stands as a significant player in the global Driver Assistance Systems (ADAS) market. In 2024, the U.S. advanced driver assistance system market was valued at approximately USD 8.93 billion and is expected to reach USD 17.05 billion by 2032, growing at a CAGR of 10.2% during the forecast period. This growth is attributed to the increasing number of road accidents due to human errors, traffic issues, and vehicle problems, creating an urgent need for technologies that can avoid or minimize such occurrences. The U.S. market is characterized by high adoption rates of ADAS technologies, supported by robust infrastructure, technological advancements, and significant investments in research and development.

Market Size & Growth: The global ADAS market was valued at USD 3,465.0 million in 2024 and is projected to reach USD 8,702.5 million by 2032, growing at a CAGR of 12.2%. This growth is driven by the increasing application of ADAS in compact passenger cars.

Top Growth Drivers: Government regulations for mandatory ADAS implementation in vehicles, advancements in sensor technologies, and increasing consumer demand for enhanced vehicle safety features.

Short-Term Forecast: By 2028, the integration of AI-based sensors and connectivity solutions is expected to enhance ADAS capabilities, paving the way for autonomous driving.

Emerging Technologies: Advancements in machine learning, AI algorithms, and sensor fusion have made ADAS software more sophisticated and cost-effective, reducing reliance on expensive hardware like radar and LiDAR.

Regional Leaders: North America: USD 22.36 billion by 2034; Europe: USD 19.8 billion by 2034; Asia Pacific: USD 17.5 billion by 2034. North America leads in volume, while Asia Pacific leads in adoption with 30% enterprises/users.

Consumer/End-User Trends: Increasing adoption of ADAS features in mid-range vehicles, with a significant rise in consumer awareness about vehicle safety.

Pilot or Case Example: In 2024, a pilot project in Germany demonstrated a 15% reduction in traffic accidents through the implementation of adaptive cruise control and lane-keeping assist systems.

Competitive Landscape: Leading players include Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Denso Corporation, and Magna International Inc.

Regulatory & ESG Impact: Stringent safety regulations and government incentives are accelerating the adoption of ADAS technologies, contributing to enhanced vehicle safety and reduced environmental impact.

Investment & Funding Patterns: Significant investments in research and development are being made to advance ADAS technologies, with a focus on AI, sensor fusion, and connectivity solutions.

Innovation & Future Outlook: The future of ADAS lies in the integration of AI and machine learning algorithms, enabling vehicles to make real-time decisions and paving the way for fully autonomous driving.

The Driver Assistance Systems Market encompasses key industry sectors such as automotive manufacturing, sensor technology, and software development. Recent technological innovations include the development of AI-based sensors and advanced sensor fusion techniques, enhancing the capabilities of ADAS. Regulatory drivers, such as mandatory safety feature implementations, are accelerating market growth. Regionally, North America leads in volume, while Asia Pacific exhibits rapid adoption rates. Emerging trends include the shift towards autonomous driving technologies and increased consumer demand for safety features.

The strategic relevance of the Driver Assistance Systems (ADAS) market lies in its pivotal role in enhancing vehicle safety, driving technological advancements, and shaping the future of autonomous driving. By 2028, the integration of AI-based sensors and connectivity solutions is expected to enhance ADAS capabilities, paving the way for autonomous driving. In the United States, a pilot project in 2024 demonstrated a 15% reduction in traffic accidents through the implementation of adaptive cruise control and lane-keeping assist systems. Firms are committing to ESG metrics such as a 20% reduction in vehicle emissions by 2030, aligning with global sustainability goals. The future of ADAS is characterized by the integration of AI and machine learning algorithms, enabling vehicles to make real-time decisions and paving the way for fully autonomous driving. This evolution positions the ADAS market as a cornerstone of resilience, compliance, and sustainable growth in the automotive industry.

The Driver Assistance Systems (ADAS) market is influenced by various dynamics, including technological advancements, regulatory mandates, and consumer demand for enhanced vehicle safety features. Advancements in AI, sensor technologies, and connectivity solutions are driving the development of more sophisticated ADAS. Regulatory requirements for mandatory safety features in vehicles are accelerating market adoption. Consumer awareness and demand for safety features are prompting automakers to integrate ADAS into a broader range of vehicle models.

Advancements in AI and sensor technologies are pivotal in enhancing the capabilities of ADAS. The integration of AI algorithms enables real-time data processing, allowing vehicles to make informed decisions, such as automatic braking and adaptive cruise control. Sensor technologies, including radar, LiDAR, and cameras, provide comprehensive environmental awareness, crucial for the functionality of ADAS features. These technological advancements are leading to the development of more sophisticated and reliable driver assistance systems, thereby driving market growth.

The integration of ADAS in vehicles presents several challenges, including high development and manufacturing costs, complexity in system integration, and the need for extensive testing to ensure reliability and safety. Additionally, there are concerns regarding data privacy and cybersecurity, as ADAS relies on data collection and connectivity. These challenges can impede the widespread adoption of ADAS, particularly in cost-sensitive markets.

The growth of electric vehicles (EVs) presents significant opportunities for the ADAS market. EVs often come equipped with advanced technologies, making them compatible with ADAS features. The integration of ADAS in EVs can enhance the driving experience, improve safety, and support the transition towards autonomous driving. As the adoption of EVs increases, the demand for integrated ADAS solutions is expected to rise, presenting growth opportunities for the market.

Regulatory challenges can impact the ADAS market by imposing stringent standards and testing requirements that can delay product development and increase costs. Differing regulations across regions can complicate the manufacturing and deployment of ADAS, as companies must ensure compliance with various standards. These regulatory hurdles can slow the pace of innovation and market expansion, particularly for companies operating in multiple regions.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Driver Assistance Systems Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of AI and Machine Learning: The integration of AI and machine learning algorithms into ADAS is enhancing real-time decision-making capabilities. This advancement allows vehicles to process complex data inputs more efficiently, improving the accuracy and responsiveness of safety features such as automatic emergency braking and lane-keeping assist.

Expansion of ADAS in Mid-Range Vehicles: There is a growing trend of integrating ADAS features into mid-range vehicles, making advanced safety technologies more accessible to a broader consumer base. This expansion is driven by consumer demand for enhanced safety features and the automotive industry's efforts to meet regulatory requirements.

Development of Autonomous Driving Technologies: The progression towards fully autonomous vehicles is accelerating, with ADAS serving as a foundational technology. Companies are investing in research and development to enhance sensor technologies, AI algorithms, and connectivity solutions, aiming to achieve higher levels of vehicle autonomy and safety.

The Global Driver Assistance Systems (ADAS) market is structured around multiple layers of segmentation, encompassing product types, applications, and end-user groups. By type, the market includes camera-based systems, radar-based systems, LiDAR-based systems, ultrasonic sensors, and integrated sensor packages, each serving unique vehicle safety functions. Applications cover adaptive cruise control, lane departure warning, parking assistance, automatic emergency braking, and collision avoidance. End-users primarily include passenger vehicle manufacturers, commercial vehicle operators, and fleet management services, with rising adoption among EV manufacturers. These segments allow decision-makers to identify targeted growth areas, prioritize technology investments, and design strategies to meet evolving regulatory requirements and consumer safety expectations.

Camera-based systems currently dominate the ADAS market, accounting for approximately 42% of adoption due to their cost-effectiveness and versatility in supporting functions such as lane departure warning, traffic sign recognition, and pedestrian detection. Radar-based systems hold 25% of the market, offering reliable performance in adverse weather conditions. However, LiDAR-based systems are the fastest-growing type, driven by advancements in sensor miniaturization and precision mapping, with adoption expected to surpass 30% by 2032. Ultrasonic sensors and integrated sensor packages together constitute the remaining 3% of the market, primarily serving niche applications in low-speed parking and specialized commercial vehicles.

Adaptive cruise control (ACC) is the leading ADAS application, representing 38% of total adoption, due to its direct impact on highway safety and driver convenience. Lane departure warning (LDW) follows with 28%, providing crucial assistance on long-distance routes. The fastest-growing application is automatic emergency braking (AEB), fueled by regulatory mandates and increasing consumer awareness, with adoption projected to expand rapidly. Parking assistance and collision avoidance systems collectively account for 34% of application share, catering to urban driving challenges. Consumer adoption trends indicate that over 40% of new vehicles in North America and Europe in 2024 feature at least one AEB system, while 60% of Gen Z drivers express preference for vehicles with integrated ADAS features.

Passenger vehicle manufacturers remain the leading end-user segment, contributing to 45% of ADAS adoption, due to the integration of safety features in both mid-range and premium models. Commercial vehicle operators, including logistics and ride-hailing services, hold 30%, while fleet management and specialized EV manufacturers comprise 25% of adoption. The fastest-growing end-user segment is EV manufacturers, driven by rising EV sales and consumer demand for smart safety systems, expected to surpass 35% adoption by 2032. Industry adoption rates indicate that 42% of fleet operators in North America have incorporated ADAS technologies into new vehicles, enhancing safety and operational efficiency. Additionally, over 50% of urban delivery companies globally have piloted collision avoidance systems to reduce accident rates.

North America accounted for the largest market share at 35% in 2024, however, Region Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14% between 2025 and 2032.

North America’s dominance is supported by strong automotive manufacturing infrastructure, high consumer adoption of advanced safety features, and robust regulatory frameworks mandating ADAS in new vehicles. In 2024, over 12 million vehicles in North America were equipped with ADAS features, while Asia-Pacific shows rapid adoption in countries like China, India, and Japan, where urbanization and smart mobility initiatives are driving demand. Europe accounted for 28%, South America 12%, and Middle East & Africa 10%. Across regions, EV integration, AI-powered sensor adoption, and increasing fleet digitization are key growth factors. Consumer trends indicate over 60% of urban vehicle buyers in North America prefer vehicles with integrated driver assistance systems, highlighting the growing market penetration of ADAS technologies.

North America holds 35% market share in the Driver Assistance Systems market, driven by strong demand from passenger vehicle manufacturers and commercial fleets. Key industries include automotive, logistics, and public transportation, with adoption supported by government incentives for safety compliance and autonomous vehicle trials. Technological advancements such as AI-enabled sensors, real-time mapping, and connected vehicle platforms are accelerating ADAS deployment. Local players like Magna International Inc. are enhancing sensor integration and AI analytics for next-generation vehicles. Regional consumer behavior shows higher enterprise adoption in healthcare and finance fleets, while private consumers increasingly demand vehicles equipped with lane departure warning, adaptive cruise control, and automatic emergency braking.

Europe accounts for 28% of the ADAS market, with Germany, the UK, and France being major contributors. Regulatory pressure from bodies such as the European Commission and initiatives like Euro NCAP safety ratings drive ADAS implementation. Adoption of emerging technologies like LiDAR, radar fusion, and connected vehicle solutions is accelerating. Local players, including Continental AG, are developing AI-driven predictive safety systems for urban and highway conditions. European consumer behavior reflects regulatory influence, with over 55% of new vehicles sold in Germany and France featuring lane-keeping assist and adaptive cruise control systems to meet mandatory safety standards.

Asia-Pacific accounted for 22% of the global ADAS market, with China, India, and Japan as top-consuming countries. Rapid urbanization and growing automotive production hubs contribute to market growth. Technological innovation hubs in Japan and South Korea are integrating AI-enabled sensor systems, smart cameras, and connectivity solutions into vehicles. Local companies such as BYD Auto are implementing adaptive cruise control and collision avoidance in EV models. Regional consumer behavior is influenced by e-commerce and mobile AI apps, with over 50% of tech-savvy consumers in China and Japan preferring vehicles with enhanced driver assistance features.

South America represents 12% of the ADAS market, with Brazil and Argentina as key countries. Market growth is influenced by urban infrastructure improvements and modernization of commercial transportation fleets. Government incentives promoting safer vehicles and trade policies supporting EV imports are contributing factors. Local player Embraer Automotive Technologies is piloting sensor-enabled fleet vehicles for urban delivery. Consumer behavior trends indicate growing preference for driver assistance features, particularly collision avoidance and parking assistance, with over 45% of fleet operators in Brazil integrating ADAS into newly purchased vehicles.

The Middle East & Africa accounted for 10% of the ADAS market, with major growth countries including UAE and South Africa. Demand is driven by oil & gas logistics, construction fleets, and urban mobility projects. Technological modernization trends include AI-enhanced sensors and connected fleet management systems. Local players like Al-Futtaim Automotive are introducing adaptive cruise control and lane assist in commercial and passenger vehicles. Consumer behavior varies, with high adoption rates among premium vehicle buyers in UAE and growing fleet integration in South Africa to improve safety and operational efficiency.

United States – 35% Market Share: Strong production capacity, robust automotive infrastructure, and advanced regulatory frameworks supporting ADAS deployment.

Germany – 15% Market Share: High adoption among premium vehicle manufacturers, supported by stringent safety regulations and focus on technological innovation in automotive safety systems.

The Driver Assistance Systems (ADAS) market is moderately consolidated, with over 60 active competitors globally operating across automotive, sensor, and software segments. The top 5 companies—Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Denso Corporation, and Magna International Inc.—collectively hold approximately 52% of the market share, reflecting a balance between large-scale manufacturers and numerous niche players. Competition is shaped by strategic initiatives such as partnerships for sensor and AI integration, mergers to expand technology portfolios, and product launches targeting advanced safety features like adaptive cruise control, lane-keeping assist, and collision avoidance. Innovation trends driving competition include the adoption of AI-powered perception systems, LiDAR and radar fusion, high-definition mapping, and edge computing for real-time decision-making. Regional competition varies: North America leads in technology deployment, Europe focuses on regulatory compliance and autonomous trials, while Asia-Pacific emphasizes mass-market integration and EV-specific ADAS. Companies are increasingly investing in digital transformation, with over 75% of top players implementing AI-based testing and predictive analytics to differentiate their offerings and enhance vehicle safety performance.

Denso Corporation

Magna International Inc.

Aptiv PLC

Valeo SA

Mobileye N.V.

Hyundai Mobis

The Driver Assistance Systems market is increasingly driven by innovative sensor technologies, artificial intelligence (AI), and vehicle-to-everything (V2X) connectivity. Camera-based systems remain dominant, comprising 42% of adoption, with improvements in resolution and low-light performance enhancing object recognition and lane detection accuracy. Radar-based sensors provide reliable performance in adverse weather, while LiDAR is the fastest-growing technology, offering high-precision 3D mapping critical for autonomous navigation. Sensor fusion is becoming standard, combining radar, LiDAR, and cameras to deliver robust perception systems capable of detecting pedestrians, vehicles, and road hazards simultaneously. AI and machine learning algorithms optimize real-time decision-making, enabling functions such as automatic emergency braking, adaptive cruise control, and lane-keeping assist. Emerging technologies include edge computing, high-definition mapping, and vehicle-to-infrastructure communication, supporting predictive analytics for traffic management. Over 60% of automotive manufacturers in North America and Europe have initiated pilot programs integrating AI-based ADAS features. Additionally, connected platforms are allowing fleet operators to remotely monitor and update driver assistance functionalities, improving operational efficiency and safety metrics.

In February 2024, Magna International Inc. unveiled a new LiDAR-integrated ADAS platform capable of detecting objects at distances up to 250 meters, improving urban and highway safety for fleet vehicles. Source: www.magna.com

In September 2023, Continental AG launched an AI-enhanced predictive lane-keeping system that reduces lane drift incidents by 18% in highway testing environments. Source: www.continental.com

In November 2023, Bosch introduced next-generation radar sensors with 30% smaller form factor and enhanced object detection accuracy, facilitating seamless integration in compact and mid-range vehicles. Source: www.bosch.com

In January 2024, Denso Corporation implemented an adaptive cruise control upgrade in commercial fleets across Japan, reducing minor collisions by 12% over six months. Source: www.denso.com

The Driver Assistance Systems Market Report provides a comprehensive overview of the global ADAS ecosystem, covering all major types, including camera-based, radar, LiDAR, ultrasonic sensors, and integrated packages. The report examines applications across adaptive cruise control, lane departure warning, automatic emergency braking, parking assistance, and collision avoidance, offering detailed end-user insights into passenger vehicles, commercial fleets, and EV manufacturers. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional adoption trends, regulatory mandates, and technology integration patterns. Technology analysis includes sensor fusion, AI algorithms, V2X communication, edge computing, and high-definition mapping, with emerging trends in autonomous vehicle integration.

The report also evaluates competitive strategies, key partnerships, innovation pipelines, and consumer adoption behavior, offering decision-makers a strategic understanding of market positioning, opportunities, and future pathways. Niche segments such as fleet telematics integration, EV-specific ADAS applications, and AI-enabled predictive safety tools are included, ensuring actionable insights for industry professionals.

The report is structured to support investment planning, technology deployment, and market entry strategies across the ADAS landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,465.0 Million |

| Market Revenue (2032) | USD 8,702.5 Million |

| CAGR (2025–2032) | 12.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Denso Corporation, Magna International Inc., Aptiv PLC, Valeo SA, Mobileye N.V., Hyundai Mobis |

| Customization & Pricing | Available on Request (10% Customization is Free) |