Reports

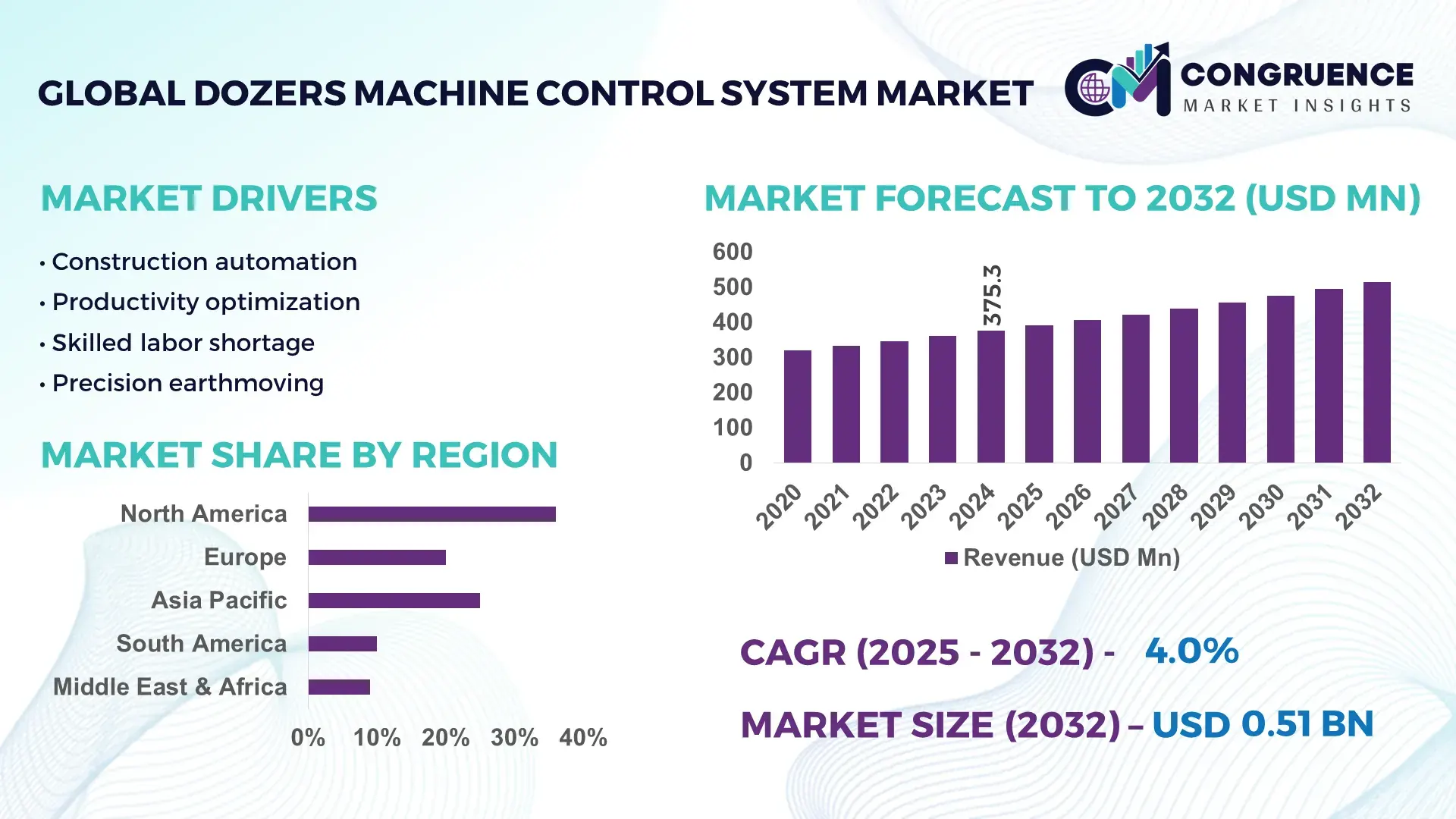

The Global Dozers Machine Control System Market was valued at USD 375.31 Million in 2024 and is anticipated to reach a value of USD 513.64 Million by 2032 expanding at a CAGR of 4% between 2025 and 2032. This growth is driven by increased infrastructure spending and rising automation adoption in earthmoving operations.

In the United States, the dozers machine control system market exhibits robust industrial activity, with over 60,000 units of machine control systems deployed across heavy construction, mining, and infrastructure projects by 2025. U.S. manufacturers have invested approximately USD 120 million in R&D for advanced GNSS and sensor fusion technologies, enhancing precision grading and fuel efficiency. Production capacity in key U.S. facilities exceeds 15,000 advanced control units annually, with strategic partnerships driving integration in large-scale highway, dam, and airport projects. Domestic demand reflects high adoption in commercial and government contracts, with over 75% of large contractors specifying automated control systems for new dozers operations.

• Market Size & Growth: 2024 market valued at USD 375.31M, projected at USD 513.64M by 2032, CAGR 4%, propelled by infrastructure digitalization and efficiency demands.

• Top Growth Drivers: Adoption of automated guidance (+28%), precision grading needs (+22%), and operational cost savings (+18%).

• Short-Term Forecast: By 2028, fleets with machine control systems to achieve up to 15% reduction in project cycle times.

• Emerging Technologies: Integration of AI-based terrain modeling, real-time sensor fusion, and 5G-enabled telematics.

• Regional Leaders: North America ~USD 185M by 2032 (advanced tech uptake), Europe ~USD 120M (infrastructure upgrades), Asia Pacific ~USD 150M (rapid construction expansion).

• Consumer/End-User Trends: Heavy civil contractors increasingly standardizing machine control systems for earthworks, quarrying, and site preparation.

• Pilot or Case Example: 2025 U.S. interstate upgrade pilot showed 12% fuel savings and 20% uptime gains using GNSS machine control.

• Competitive Landscape: Market leader ~32% share; key competitors include Trimble Inc., Topcon Positioning Systems, Leica Geosystems, and Hexagon AB.

• Regulatory & ESG Impact: Emission reduction standards and government incentives for precision construction technologies accelerating deployments.

• Investment & Funding Patterns: Recent investments exceeding USD 250M in automated construction tech start-ups and strategic alliances.

• Innovation & Future Outlook: Increasing integration with BIM workflows, autonomous dozer prototypes, and cloud-based analytics platforms shaping future market dynamics.

Dozers Machine Control System Market dynamics show sustained transformation with heavy civil engineering, mining, and infrastructure sectors driving differentiated adoption patterns. Key industry sectors such as road construction and large-scale earthmoving contribute significant deployment volumes, while mining operations prioritize durability and sensor precision. Technological innovations include real-time terrain feedback, automated blade control, and predictive maintenance algorithms that reduce downtime and enhance productivity. Regulatory frameworks emphasizing safety and emissions reductions further influence procurement policies, and regional consumption patterns highlight rapid uptake in APAC due to escalating construction activity. Future demand will be shaped by autonomous integration, scalable software platforms, and higher investment in digital machine fleets.

The Dozers Machine Control System Market is strategically relevant because it directly improves productivity, compliance, and capital efficiency in large-scale earthmoving, infrastructure, and mining operations where even marginal performance gains translate into significant cost and time savings. Advanced 3D GNSS-based machine control delivers about 25% higher grading accuracy compared to traditional 2D laser guidance standards, reducing rework, material wastage, and fuel consumption while improving project predictability for contractors and public agencies. Asia–Pacific dominates in volume due to its scale of infrastructure and mining activity, while Europe leads in adoption with approximately 62% of large contractors actively using machine control systems as part of digital construction programs.

By 2028, AI-driven terrain modeling and automated blade optimization are expected to improve site productivity by 15% and reduce idle time by 12% through real-time decision support and predictive adjustments. From a compliance and ESG perspective, firms are committing to carbon intensity improvements such as 10% reductions in fuel-related emissions by 2030 through optimized machine operation and reduced rework cycles. In 2025, Australia’s mining sector achieved a 14% reduction in earthmoving cycle times through the deployment of AI-assisted machine control and fleet analytics across open-pit operations.

Looking ahead, the Dozers Machine Control System Market is becoming a structural enabler of resilient project execution, regulatory alignment, and sustainable growth, supporting the transition toward data-driven, low-emission, and automation-ready construction and resource extraction ecosystems.

Large-scale infrastructure and mining investments are a primary driver of demand for Dozers Machine Control Systems because they involve high earthmoving volumes where precision and speed have direct financial impact. Highway, rail, airport, and renewable energy projects increasingly rely on automated grading to meet tight timelines and quality standards. For example, modern highway construction programs report up to 20% reductions in earthworks rehandling when automated control is applied. In mining, precise blade control reduces overcutting and undercutting, improving ore-to-waste ratios and reducing haulage volumes. Governments and private developers are also requiring digital reporting of as-built data, which machine control systems can automatically generate. This combination of scale, performance expectations, and data requirements is pushing contractors to standardize machine control across fleets, accelerating adoption in both developed and emerging economies.

The initial capital cost of Dozers Machine Control Systems, including hardware, software licenses, installation, and training, can be significant, particularly for small and mid-sized contractors. A full 3D machine control setup can add tens of thousands of dollars per machine, creating barriers for firms operating on thin margins or short-term contracts. In addition, system complexity and the need for skilled operators and technicians limit adoption in regions with low digital maturity. Downtime associated with calibration, software updates, and sensor maintenance can also discourage users who prioritize equipment availability over precision. Interoperability issues between different brands of machines, software platforms, and data formats further increase integration costs and operational friction, slowing broader market penetration despite the long-term efficiency benefits.

Automation and digital construction initiatives create substantial opportunities for the Dozers Machine Control System market by expanding its role from a productivity tool into a core digital infrastructure asset. Integration with Building Information Modeling, digital twins, and cloud-based project management systems allows machine control data to be used for real-time progress tracking, compliance verification, and predictive maintenance. Autonomous and semi-autonomous dozer projects further increase the value of machine control as a foundational technology layer. In regions with labor shortages, automated control reduces dependence on highly experienced operators, improving workforce flexibility. Public-sector smart infrastructure programs and private-sector sustainability targets also create demand for technologies that can document material usage, emissions, and performance outcomes, positioning machine control systems as both an operational and reporting solution.

As Dozers Machine Control Systems become increasingly connected, they generate large volumes of operational and geospatial data that must be securely stored, transmitted, and governed. Cybersecurity risks, including unauthorized access to machine control systems or project data, raise concerns for contractors and infrastructure owners. Regulatory fragmentation across regions regarding data ownership, privacy, and cross-border data transfer complicates deployment for multinational firms. Additionally, differing technical standards for positioning accuracy, safety certification, and digital construction compliance increase complexity for vendors and users alike. These challenges require ongoing investment in secure architectures, standardized interfaces, and regulatory alignment, increasing operational costs and slowing the pace of global harmonization and adoption.

• Rapid integration of AI-enabled blade automation improving grading precision by 25% and reducing rework by 18%

Construction and mining operators are increasingly deploying AI-assisted blade control and terrain-recognition software that automatically adjusts blade position in real time. Field data shows average grading accuracy improvements of 25% and a reduction in corrective passes by 18%, lowering fuel consumption by around 10%. More than 40% of new high-capacity dozers delivered in 2025 are now pre-configured for AI-assisted control, accelerating digital standardization across large fleets and long-duration infrastructure projects.

• Expansion of modular and prefabricated construction increasing demand for precision systems in 55% of new projects

The rise of modular and prefabricated construction is reshaping demand for Dozers Machine Control Systems as earthworks must meet tighter tolerances to fit pre-manufactured components. Around 55% of new projects using modular methods report measurable cost benefits, while site preparation times fall by about 20%. Europe and North America together account for over 60% of modular adoption, directly increasing demand for high-precision grading and digital layout capabilities.

• Fleet-wide digitalization driving 30% growth in connected machine control deployments and 15% uptime improvement

Contractors are scaling from single-machine deployments to fleet-level machine control integration, linking dozers with centralized cloud platforms. Approximately 30% more machines are now connected compared to three years ago, enabling predictive maintenance and remote diagnostics that improve equipment uptime by 15%. This shift supports better asset utilization, standardized workflows, and improved compliance reporting across multi-site operations.

• Sustainability and emissions optimization reducing fuel use by 12% and supporting 10% carbon intensity reduction targets

Machine control systems are increasingly used to optimize earthmoving paths and reduce unnecessary blade movements, cutting fuel consumption by an average of 12%. Large contractors are aligning these gains with corporate targets of 10% carbon intensity reductions by 2030, making digital control a core element of sustainability strategies and procurement decisions for infrastructure and mining projects.

The Dozers Machine Control System market is segmented by type, application, and end-user, each reflecting different operational needs, digital maturity levels, and investment priorities. By type, 2D, 3D GNSS-based, and semi-autonomous control systems serve varying accuracy and automation requirements, with higher-end systems increasingly favored for complex and large-scale projects. By application, infrastructure construction, mining, and commercial site development dominate usage, driven by earthwork volume, precision needs, and compliance obligations. End-user segmentation highlights large contractors and mining operators as primary adopters, while public infrastructure agencies and mid-sized construction firms represent important secondary segments. Adoption intensity correlates strongly with project scale, regulatory requirements, labor availability, and digital integration strategies. Together, these segmentation dimensions illustrate that the market is shifting from optional add-on technology toward a core operational platform embedded into modern earthmoving workflows.

2D machine control systems currently account for approximately 38% of installed systems, driven by their lower cost and suitability for simpler grading tasks such as bulk earthworks and agricultural land preparation. However, 3D GNSS-based machine control systems represent about 47% of adoption and are the leading segment due to their ability to deliver centimeter-level accuracy, support complex designs, and integrate with digital construction workflows. Semi-autonomous and fully automated control systems remain smaller but strategic, together representing roughly 15% of deployments, mainly in mining and large infrastructure projects.

3D GNSS-based systems are also the fastest-growing type, with adoption expanding at about 12% annually, supported by falling sensor costs, improved satellite coverage, and increasing digital tender requirements. The remaining systems, including laser-based and hybrid configurations, retain niche relevance for indoor, tunnel, and confined-space projects, contributing a combined share of around 15%.

Infrastructure construction is the leading application, accounting for roughly 44% of system usage, as highways, railways, airports, and flood control projects require high-volume, high-precision earthworks and standardized digital reporting. Mining follows with about 33% adoption, where machine control supports slope stability, ore boundary control, and waste reduction. Commercial and industrial site development represents the remaining 23%, driven by logistics parks, industrial estates, and large real estate projects.

Mining is the fastest-growing application with adoption rising at approximately 11% annually, supported by automation strategies, safety requirements, and the need to improve material selectivity and reduce haulage inefficiencies. Infrastructure growth remains stable but large-scale, while commercial construction benefits from faster project delivery and reduced labor dependence.

Large construction contractors are the dominant end-users, accounting for about 48% of deployments, as they manage multi-project portfolios where standardization and data integration deliver strong returns. Mining companies represent around 34% of users, driven by automation, safety, and productivity priorities. Public infrastructure agencies and smaller contractors together contribute the remaining 18%, typically adopting systems through mandated digital construction programs or subcontracting requirements.

Mining operators are the fastest-growing end-user group, with adoption increasing at approximately 10% annually, fueled by autonomous haulage integration, safety compliance, and cost control pressures. Large contractors continue to expand usage through fleet upgrades and digital transformation initiatives, while public agencies drive adoption indirectly through procurement standards.

North America accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5% between 2025 and 2032.

North America deployed over 18,000 units of Dozers Machine Control Systems in 2024, primarily across highway construction, mining, and energy projects. Europe followed with 26% share, with Germany and France leading adoption. Asia-Pacific recorded 30,500 units under operation, driven by rapid infrastructure and smart city initiatives in China, India, and Japan. South America accounted for 6% of the global installations, while Middle East & Africa represented 5%, largely concentrated in oil & gas and large-scale urban development projects. Across regions, digital integration of GNSS, sensor fusion, and AI-assisted control is standardizing precision grading, with over 62% of fleets globally now equipped with advanced machine control systems.

How are digital upgrades transforming precision earthmoving in North America?

North America holds 36% of the Dozers Machine Control System market, led by demand from infrastructure construction, mining, and energy sectors. Government incentives for sustainable construction practices and federal safety regulations encourage high adoption, with over 75% of large contractors using digital machine control. Technological trends include AI-assisted blade optimization, cloud-connected fleets, and GNSS-based 3D grading. Local player Trimble Inc. continues to expand its North American footprint by integrating cloud analytics and autonomous-ready systems into new dozer fleets. North American consumers prefer full-service, integrated solutions with predictive maintenance, reflecting high enterprise adoption rates in construction and resource extraction operations.

Why is regulatory compliance driving smart grading adoption in Europe?

Europe accounts for 26% of global Dozers Machine Control System deployments, with Germany, France, and the UK as the leading markets. Regulatory frameworks and sustainability mandates have accelerated the adoption of advanced control systems, with over 60% of public-sector projects specifying 3D GNSS or semi-autonomous solutions. Emerging technologies such as AI-assisted terrain analysis and laser-guided hybrid systems are gaining traction. Local player Topcon Positioning Systems has implemented connected machine fleets for major highway projects in Germany, reducing rework by 14%. European contractors prioritize explainable, certified systems to meet compliance, while commercial adoption is rising due to digital infrastructure initiatives and labor efficiency requirements.

How is infrastructure expansion fueling machine control demand in Asia-Pacific?

Asia-Pacific holds the largest volume of new installations, with China, India, and Japan leading consumption. The region accounts for roughly 30% of global Dozers Machine Control System deployment, driven by highways, metro networks, and industrial park construction. Rapid urbanization and large-scale mining operations are creating demand for automated grading and fleet integration. Technology hubs in Japan and China focus on AI-assisted blade control and cloud-based fleet management. Local player Komatsu has launched GNSS-equipped dozers with remote diagnostics, supporting over 12,000 units across industrial and infrastructure projects. Consumer behavior in Asia-Pacific shows high adoption for project efficiency, cost reduction, and integration with digital construction workflows.

What factors are shaping precision earthmoving adoption in South America?

South America represents 6% of the global Dozers Machine Control System market, with Brazil and Argentina leading demand. Key growth drivers include large infrastructure projects, mining, and energy sector expansions. Governments are offering incentives to modernize construction fleets, while trade partnerships facilitate access to GNSS-based control systems. Local companies have begun retrofitting dozers with digital guidance, improving grading accuracy by 10–12%. Regional consumer behavior emphasizes affordability and ruggedized solutions suitable for diverse terrain and climate conditions, with a rising preference for systems that support multi-machine integration and data reporting for compliance purposes.

How is modernization influencing construction and mining operations in Middle East & Africa?

Middle East & Africa accounts for 5% of Dozers Machine Control System installations, with the UAE, Saudi Arabia, and South Africa as major markets. Growth is driven by oil & gas infrastructure, urban development, and transport networks. Digital modernization trends include semi-autonomous dozers, AI-assisted grading, and cloud-connected fleet monitoring. Government regulations on safety and emissions encourage adoption of precision control systems. Local operators are piloting GNSS-equipped fleets to reduce material wastage and operational downtime by over 10%. Regional consumer behavior favors high-durability systems with remote diagnostics due to challenging environmental conditions and dispersed project sites.

United States: 36% market share – High production capacity and strong contractor adoption in large-scale infrastructure projects.

China: 28% market share – Rapid infrastructure expansion, industrial construction, and technological integration drive adoption of advanced machine control systems.

The Dozers Machine Control System market is moderately consolidated, with roughly 35–40 active global competitors. The top five companies collectively account for approximately 68% of total market deployments, reflecting strong dominance by leading technology providers while leaving space for specialized regional players and innovative start-ups. Key competitors are strategically investing in AI-assisted automation, cloud integration, and GNSS-based solutions to differentiate their offerings. Product launches and pilot programs continue to be a major competitive tool, with over 120 new system models or software upgrades introduced globally between 2023 and 2025. Partnerships and strategic alliances are also shaping market dynamics; more than 25 collaborations between construction OEMs and software providers were established in the past two years to accelerate autonomous and semi-autonomous dozer deployments. Innovation trends such as predictive maintenance, fleet telematics, and multi-machine coordination are increasing competitive pressure, particularly among North American and Asia-Pacific players. Regional market fragmentation exists in South America and Africa, where smaller local suppliers contribute approximately 15–20% of deployments, creating a dynamic competitive environment. The market landscape favors firms that combine technological leadership, service support, and digital ecosystem integration to secure long-term contracts with large infrastructure and mining operators.

Leica Geosystems

Hexagon AB

Caterpillar Inc.

Deere & Company

Kubota Corporation

Doosan Infracore

CNH Industrial

The Dozers Machine Control System market is increasingly driven by the integration of advanced technologies that enhance precision, efficiency, and operational safety. GNSS-based 3D machine control remains the core technology, deployed in approximately 47% of high-precision projects, offering centimeter-level grading accuracy across highways, mining, and large-scale civil construction. Semi-autonomous and fully autonomous control systems are expanding, with over 12,000 units globally equipped for AI-assisted terrain modeling and automated blade adjustment in 2025. These systems reduce rework by up to 18% and fuel consumption by 10%, while enabling operators to manage multiple machines from a central console.

Emerging technologies such as AI and machine learning are enhancing predictive maintenance and real-time decision-making, with fleets using connected sensors achieving a 15% improvement in uptime and a 12% reduction in operational errors. Inertial measurement units (IMUs) combined with GNSS sensors are improving stability and accuracy on uneven terrain, allowing dozers to operate efficiently on slopes exceeding 25 degrees. Cloud-based telematics platforms are enabling centralized data monitoring, performance analytics, and compliance reporting, with more than 65% of large contractors now using connected machine fleets.

LiDAR integration and 3D scanning are also gaining traction for automated site modeling, enabling earthwork planning with sub-5 cm tolerances. Additionally, collaborative software platforms are facilitating the seamless integration of machine control data with Building Information Modeling (BIM), allowing engineers and project managers to optimize earthworks scheduling and material allocation. The convergence of AI, cloud connectivity, and sensor fusion positions the Dozers Machine Control System market at the forefront of digital construction transformation, offering measurable operational benefits and long-term strategic value for large-scale projects.

• In March 2023, Komatsu unveiled its intelligent Machine Control 2.0 dozers — including the D39PXi‑24, D51PXi‑24 and D71PXi‑24 models — showcasing proactive dozing control that can improve productivity by up to 60% compared to conventional grading methods by using terrain data to plan blade passes automatically during operations. (komatsu.com)

• In October 2024, John Deere expanded its next‑generation SmartGrade technology across its 450, 550 and 650 P‑Tier small dozers, now compatible with both Topcon and Leica machine control solutions, enabling operators to achieve accurate grading with simplified setup and enhanced in‑cab troubleshooting via Wireless Data Transfer and Remote Display Access. (Groff Tractor & Equipment)

• In September 2024, Komatsu announced advancements in teleoperation technology for dozers and drills, introducing non‑line‑of‑sight teleoperation capabilities to improve remote control, productivity and worker safety in high‑risk environments, marking a significant step toward broader remote and autonomous operations. (komatsu.com)

• In November 2024, Hitachi Construction Machinery hosted the inaugural Hitachi Construction Machinery Challenge 2024, awarding Sodex Innovations, Teleo and Veristart Technologies for solutions poised to transform heavy machinery operations; these winners are set to participate at bauma 2025 to explore collaboration opportunities and further market innovation. (Hitachi Construction Machinery)

The scope of the Dozers Machine Control System Market Report encompasses a comprehensive analysis of technology implementations, operational applications, end‑user segments, and regional deployment patterns globally. This report evaluates machine control systems ranging from basic 2D guidance to advanced 3D GNSS‑based and semi‑autonomous control solutions, detailing how inertial sensors, cloud connectivity, and AI enhancements are reshaping machine accuracy and operator efficiency. It examines application environments such as infrastructure projects, mining operations, commercial and industrial site preparation, highlighting differential system requirements and performance outcomes across diverse earthwork tasks. The report segments the market by product types — including traditional guidance systems, integrated AI‑assisted control, and retrofit‑ready kits — and tracks how technological innovation influences adoption metrics such as installation units, precision levels, and machine uptime enhancements. Geographic analysis includes North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with granular insights into leading countries, regional consumer behavior, regulatory incentives, and digital transformation trends. Operational use cases, like integration with predictive maintenance and fleet telematics, are explored alongside key sector drivers including safety mandates, labor optimization, and environmental performance targets. Emerging and niche segments such as autonomous retrofit solutions, hybrid machine control architectures, and mixed‑fleet interoperability are also detailed to provide decision‑makers with a forward‑looking view of capabilities, deployment considerations, and strategic planning imperatives for capitalizing on evolving machine control ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 375.31 Million |

Market Revenue in 2032 | USD 513.64 Million |

CAGR (2025 - 2032) | 4% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Trimble Inc., Topcon Positioning Systems, Komatsu Ltd., Leica Geosystems, Hexagon AB, Caterpillar Inc., Deere & Company, Kubota Corporation, Doosan Infracore, CNH Industrial |

Customization & Pricing | Available on Request (10% Customization is Free) |