Reports

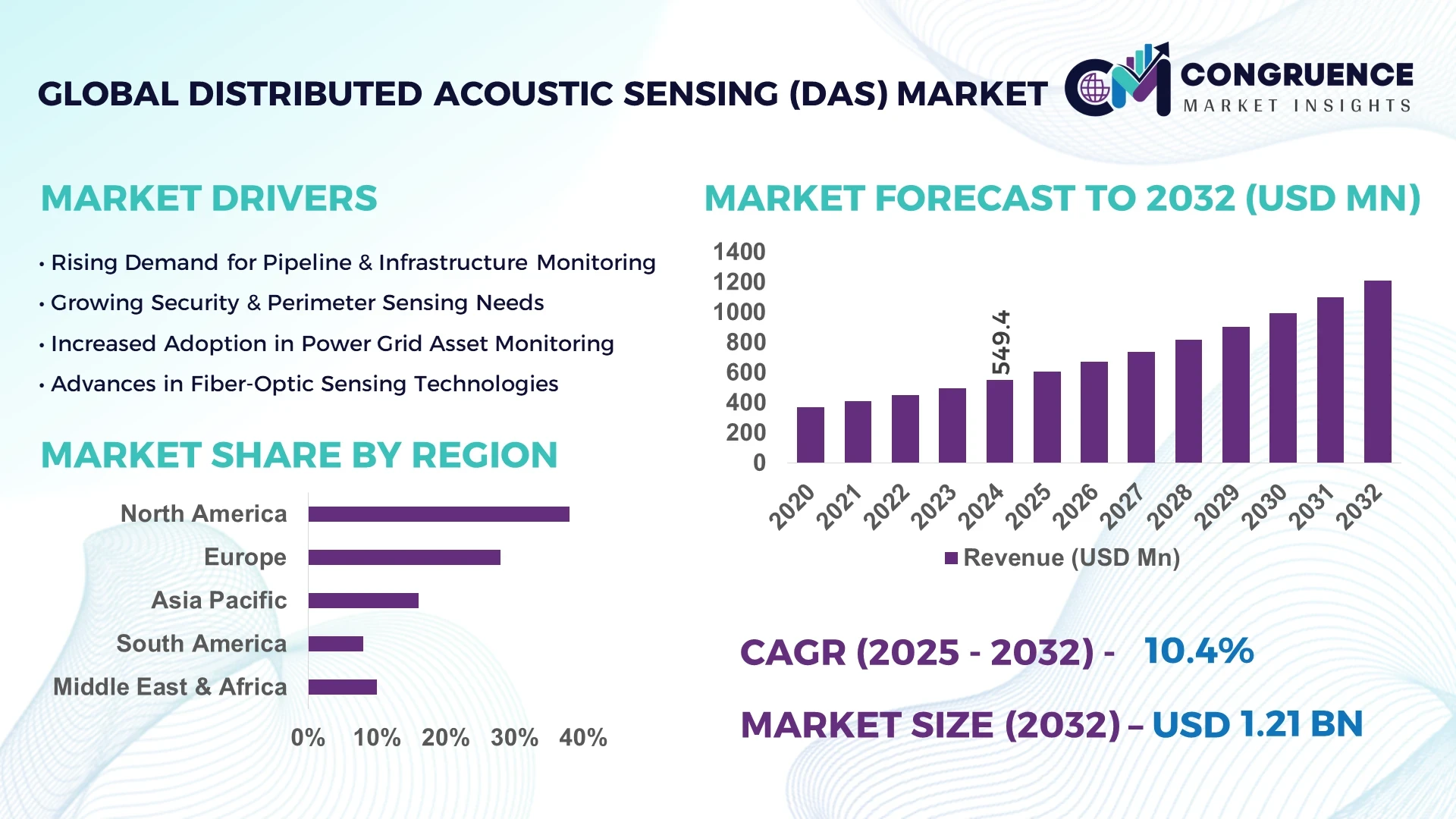

The Global Distributed Acoustic Sensing (DAS) Market was valued at USD 549.35 Million in 2024 and is anticipated to reach a value of USD 1,212.27 Million by 2032, expanding at a CAGR of 10.4% between 2025 and 2032.

Germany leads production capacity and technological advancement in the Distributed Acoustic Sensing (DAS) market, with leading firms investing heavily in fiber-optic sensing infrastructure. German manufacturers maintain substantial manufacturing capacity for DAS interrogator units and fiber-optic components, while government and private sector investments have boosted R&D in smart DAS monitoring solutions, particularly for infrastructure and environmental surveillance.

Key industry sectors include oil & gas, utilities, and security and surveillance. Oil & gas applications dominate demand, particularly in hydraulic fracturing diagnostics and pipeline integrity, while utilities are deploying DAS for grid-resilience monitoring and early fault detection. Recent innovations include silicon-photonic miniaturized interrogators achieving <1.2 m spatial resolution, hybrid fiber cables combining single-mode and multi-mode capabilities, and integrated analytics platforms offering real-time insight and cross-licensing between photonics and AI software providers. Regulatory mandates on pipeline safety, infrastructure surveillance, and environmental protection have accelerated DAS adoption. Regional consumption patterns show high uptake in North America and Europe, with emerging expansion in Asia Pacific. Environmental monitoring and smart-city applications using DAS for perimeter security, traffic flow analysis, and seismic detection are rapidly gaining prominence, shaping future growth trajectories in decision-making and operational optimization.

Artificial intelligence is revolutionizing the Distributed Acoustic Sensing (DAS) market by enhancing data interpretation, operational efficiency, and monitoring intelligence. AI-powered frameworks—particularly machine learning and deep learning—are increasingly embedded within DAS systems to automate the processing of massive acoustic data streams, reduce false positives, and deliver actionable alerts faster. Data-analytics services now outpace hardware sales, as operators engage AI-driven consulting for commissioning, daily monitoring of terabytes-per-kilometer data, and predictive maintenance cycle optimization.

Machine learning models embedded in DAS enable precise event classification, anomaly detection, and signal enhancement—delivering improved operational performance across pipelines, perimeters, and infrastructure networks. Edge analytics platforms now process data in real-time, preserving bandwidth and enabling rapid response. AI-augmented systems also facilitate fusion with IoT and smart-city networks, enabling DAS-based traffic monitoring, environmental surveillance, and smart-grid applications with minimal human supervision. As a result, operational workflows are streamlined, incident detection is more accurate and faster, and maintenance scheduling is optimized—boosting cost-effectiveness and strategic resource allocation for decision-makers in critical infrastructure sectors. The integration of AI is fundamentally transforming the Distributed Acoustic Sensing (DAS) market into a smarter, more responsive sensing ecosystem.

“The DAS-MAE self-supervised pre-training framework for distributed fiber-optic acoustic sensing achieved up to 64.5% relative improvement in few-shot classification and reduced recognition error to 5.0% with a 75.7% relative improvement over supervised training from scratch in external damage prevention.”

The Distributed Acoustic Sensing (DAS) market is experiencing robust transformation driven by advances in fiber-optic sensing technologies, expanding applications in critical infrastructure, and integration with AI-based analytics. Key trends include the miniaturization of interrogator units, improved spatial resolution below one meter, and expanded operational ranges exceeding 80 kilometers for continuous monitoring. Industries such as oil & gas, power utilities, defense, transportation, and environmental monitoring are increasingly adopting DAS for enhanced safety, operational efficiency, and predictive maintenance. Regulatory emphasis on asset integrity and environmental compliance continues to influence purchasing decisions. Furthermore, demand for high-speed data processing, combined with rising urban infrastructure investments, is reinforcing the market’s growth trajectory, creating a competitive environment where innovation and real-time analytics play pivotal roles in vendor differentiation.

The surge in large-scale infrastructure projects, including oil & gas pipelines, power transmission lines, and high-speed rail systems, has significantly increased the demand for Distributed Acoustic Sensing (DAS) solutions. DAS technology enables continuous, real-time monitoring across vast distances, allowing early detection of leaks, intrusions, or structural stress. In oil & gas, for example, fiber-optic DAS systems can detect third-party interference within seconds, reducing environmental damage and operational downtime. Transportation sectors are using DAS to monitor rail track integrity and detect train movements, improving safety and efficiency. With urban infrastructure expansion and heightened global security concerns, advanced DAS systems with improved sensitivity and lower maintenance requirements are becoming essential in asset management strategies worldwide.

Despite its advantages, the Distributed Acoustic Sensing (DAS) market faces deployment challenges due to the technical complexity of installation, calibration, and integration with existing infrastructure. High-performance DAS systems require specialized fiber installation or adaptation of existing optical cables, which can be costly and logistically demanding, particularly in remote or hostile environments. Furthermore, integrating DAS data streams with legacy SCADA systems or centralized monitoring platforms often necessitates additional software and hardware investments, as well as skilled personnel for configuration and maintenance. These technical and operational hurdles can delay project timelines, increase total cost of ownership, and discourage adoption in industries with limited technical expertise or budgetary constraints, especially in developing markets.

The emergence of smart city initiatives presents a significant opportunity for the Distributed Acoustic Sensing (DAS) market. DAS systems can be deployed along existing telecom fiber networks to provide real-time data on traffic flow, pedestrian movement, and environmental parameters such as seismic activity or noise pollution. Municipalities can leverage this data to optimize urban mobility, enhance public safety, and monitor environmental health without installing additional sensor hardware. In environmental monitoring, DAS is increasingly used for early earthquake detection, glacier movement tracking, and monitoring of wildlife activity in conservation areas. The ability to repurpose existing fiber infrastructure for multiple sensing applications not only reduces costs but also aligns with sustainable development goals, opening new growth avenues in urban planning and environmental research.

The high-volume data output from Distributed Acoustic Sensing (DAS) systems—often several terabytes per day—poses significant challenges in storage, transmission, and processing. Differentiating between genuine threat signals and environmental noise requires advanced algorithms, which can be computationally intensive and demand high-performance processing infrastructure. For large-scale deployments, particularly in national pipeline networks or cross-border infrastructure, managing this data while maintaining real-time alert capabilities can strain both technical resources and operational budgets. Additionally, the lack of standardized data formats and interoperability protocols complicates collaboration between different monitoring systems and agencies. Addressing these challenges will require industry-wide efforts in developing scalable analytics platforms, optimizing compression techniques, and establishing common operational standards for DAS networks.

• Integration of AI-Enhanced Event Classification Systems: AI-powered algorithms are increasingly embedded into Distributed Acoustic Sensing (DAS) solutions to improve event detection precision. Advanced models now achieve over 95% accuracy in differentiating between real threats, environmental noise, and operational vibrations. This has led to fewer false positives, faster incident verification, and improved asset protection. Industries such as oil & gas, rail transport, and border security are deploying AI-integrated DAS platforms to enhance operational safety while reducing the workload on monitoring teams.

• Expansion of Multi-Use Fiber Infrastructure for DAS Applications: Telecommunication operators are collaborating with DAS technology providers to utilize existing fiber-optic infrastructure for sensing purposes. This multi-use approach enables cities to track traffic conditions, monitor construction activities, and enhance security without installing new cables. Adoption is rising in smart city projects across Asia-Pacific and Europe, where combining telecom services with DAS monitoring is creating new operational and revenue models for infrastructure providers.

• Deployment of Ultra-Long-Range DAS Systems: Technological innovations have enabled DAS networks to operate over distances exceeding 100 kilometers while maintaining high spatial resolution. This capability reduces the number of interrogator units required for large-scale monitoring, making it cost-effective for pipeline operators, railway authorities, and border control agencies. These extended-range systems improve detection accuracy across wide geographic areas while lowering long-term operational costs.

• Rise in Modular and Prefabricated Construction: The move toward modular and prefabricated construction is influencing demand for DAS-enabled monitoring systems. Prefabricated infrastructure components can be embedded with fiber-optic sensing cables during production, ensuring faster installation and integrated safety monitoring. This approach is particularly prominent in North America and Europe, where time efficiency and stringent safety compliance drive adoption for transportation hubs, industrial facilities, and utility corridors.

The Distributed Acoustic Sensing (DAS) market is segmented into types, applications, and end-user categories, each with distinct operational priorities. By type, the market includes single-mode DAS, multimode DAS, hybrid fiber DAS, portable DAS units, and interrogator modules, offering varying levels of sensitivity, range, and deployment flexibility. Applications range from oil & gas monitoring, perimeter security, and transportation monitoring to utility infrastructure surveillance and environmental monitoring, with adoption influenced by safety, efficiency, and cost considerations. End-users encompass energy companies, defense and security agencies, transportation authorities, utilities, and research organizations. These segments reflect diverse integration requirements, driving innovation in fiber-optic sensing capabilities and system adaptability across industries.

Single-mode DAS leads the market due to its ability to deliver long-range, high-resolution monitoring essential for oil & gas pipelines and major infrastructure networks. This type is preferred where continuous surveillance across vast distances is critical. Multimode DAS, while more suited for shorter distances, offers superior sensitivity for industrial and security-focused applications in confined areas. The fastest-growing type is hybrid fiber DAS, which merges the benefits of single-mode range with multimode sensitivity, enabling flexible deployment in diverse environments. Portable DAS units cater to temporary or mobile monitoring needs, such as event security or emergency response. Interrogator modules, integral to system customization, are being adopted for research, defense projects, and upgrade-focused deployments, supporting specialized sensing requirements. Each type addresses specific industry needs, with innovation steadily enhancing performance and versatility.

Oil & gas monitoring remains the dominant application due to the industry’s reliance on DAS for early leak detection, third-party interference alerts, and operational safety. Long-distance pipeline operators particularly benefit from the technology’s ability to provide continuous coverage without deploying multiple sensors. Transportation monitoring is the fastest-growing application, driven by investment in high-speed rail networks and urban transit systems that use DAS for track fault detection, train localization, and trespass prevention. Perimeter security retains strong relevance in defense, energy, and data center facilities. Utility infrastructure monitoring is also expanding, with DAS integrated into power line and water pipeline systems for preventive maintenance. Environmental monitoring, while still emerging, is gaining traction for earthquake detection, glacier tracking, and wildlife observation, diversifying the technology’s scope.

Energy companies are the leading end-users, implementing DAS for comprehensive asset protection, including offshore platforms, onshore pipelines, and refineries. Their requirement for real-time, continuous monitoring aligns with DAS’s core strengths. Transportation authorities represent the fastest-growing end-user group, fueled by rail and metro expansions that demand high-precision safety monitoring and predictive maintenance. Defense and security agencies deploy DAS for perimeter intrusion detection, border surveillance, and critical facility protection. Utilities adopt DAS for grid stability monitoring, fault detection, and water distribution integrity. Research institutions also contribute to demand, particularly in seismic studies, environmental monitoring, and infrastructure resilience assessments, leveraging DAS’s data-rich capabilities for advanced analytics.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2025 and 2032.

The North American Distributed Acoustic Sensing (DAS) market benefits from extensive oil & gas infrastructure, advanced rail networks, and high defense and perimeter security spending. In contrast, Asia-Pacific is seeing accelerated adoption due to rapid infrastructure expansion, smart city projects, and large-scale investments in fiber-optic networks across China, India, and Japan. Europe maintains a strong presence, driven by environmental monitoring mandates and cross-border security initiatives. Meanwhile, emerging markets in South America and the Middle East & Africa are leveraging DAS for energy sector modernization, environmental safety, and strategic infrastructure protection, signaling significant potential for diversified growth globally.

Advanced Fiber-Optic Monitoring Driving Industrial Safety Solutions

Holding approximately 38% of the global volume in 2024, the region’s Distributed Acoustic Sensing (DAS) market is propelled by oil & gas, transportation, and defense applications. Government-backed infrastructure protection programs, particularly in pipeline safety and border monitoring, have boosted adoption. Regulatory frameworks, such as updated pipeline integrity management rules, are pushing operators toward real-time monitoring solutions. Technological advancements, including AI-enhanced event classification and ultra-long-range sensing systems, are streamlining operations and improving detection accuracy. The integration of DAS into smart grid and urban transit monitoring projects highlights the region’s commitment to digital transformation, ensuring consistent demand from both public and private sectors.

Energy Transition Initiatives Fueling Fiber-Optic Sensing Deployment

With a market share of around 28% in 2024, this region’s Distributed Acoustic Sensing (DAS) market is driven by Germany, the UK, and France, where energy transition policies and advanced industrial safety regulations dominate infrastructure investment priorities. The European Union’s sustainability initiatives, including stricter environmental monitoring requirements, have accelerated DAS deployment in renewable energy projects and cross-border transport corridors. Emerging technologies such as hybrid fiber sensing systems and AI-integrated analytics are being adopted to enhance efficiency in railway networks, offshore wind farms, and pipeline safety. Public-private partnerships are also expanding the role of DAS in environmental and urban security projects, strengthening its strategic market position.

Infrastructure Expansion and Smart Cities Powering Demand Growth

Ranked as the fastest-growing region, with substantial volume gains in 2024, the Distributed Acoustic Sensing (DAS) market in this area is led by China, India, and Japan. Massive infrastructure development projects, from high-speed rail expansion to cross-country oil & gas pipelines, are accelerating DAS adoption. China’s innovation hubs are producing advanced fiber-optic interrogators with improved resolution, while India’s telecom-driven fiber expansion is enabling cost-effective DAS deployments. Japan’s focus on seismic and tsunami monitoring through fiber sensing demonstrates the technology’s versatility. Rapid integration of DAS into smart city frameworks, urban traffic systems, and renewable energy monitoring platforms is further strengthening market growth potential.

Energy Sector Modernization Driving Fiber-Optic Monitoring Uptake

Brazil and Argentina anchor the region’s Distributed Acoustic Sensing (DAS) market, accounting for about 8% of global share in 2024. The modernization of oil & gas infrastructure, particularly offshore platforms and long-distance pipelines, is a key driver. Government incentives for energy efficiency and environmental monitoring are accelerating the adoption of DAS solutions. Brazil’s growing wind energy sector and Argentina’s expanding mining operations are deploying DAS for asset protection and operational safety. The technology’s ability to operate in challenging terrains is proving essential for infrastructure resilience, making it increasingly relevant in both industrial and environmental applications.

Oil & Gas Security and Infrastructure Surveillance Fueling Adoption

In 2024, this region accounts for around 10% of the global Distributed Acoustic Sensing (DAS) market, with strong demand from the UAE, Saudi Arabia, and South Africa. The dominance of the oil & gas sector continues to drive investments in long-distance fiber-optic monitoring systems for pipeline security. Mega infrastructure projects, including new rail networks and port expansions, are creating opportunities for DAS integration. Technological modernization, particularly the adoption of AI-driven analytics for real-time threat detection, is improving operational efficiency. Local regulations emphasizing energy infrastructure safety, combined with trade partnerships to import advanced sensing technologies, are enhancing adoption rates across key industries.

United States – 25% – Strong oil & gas infrastructure monitoring and high defense sector adoption of DAS for border and facility security.

China – 18% – Expansive fiber-optic network and rapid integration of DAS into smart city and large-scale infrastructure projects.

The Distributed Acoustic Sensing (DAS) market is characterized by a moderately consolidated competitive environment, with approximately 25–30 active global and regional players competing through technological innovation, strategic collaborations, and application-specific specialization. Leading companies differentiate themselves by integrating AI-powered analytics, enhancing signal processing accuracy, and expanding the sensing range of fiber-optic monitoring systems. Competitive positioning is increasingly shaped by industry-specific expertise, with some players focusing on oil & gas security and pipeline monitoring, while others target transportation, infrastructure safety, and environmental monitoring applications. Strategic initiatives such as partnerships between technology firms and telecom operators are enabling broader deployment across existing fiber networks. Product launches in 2023 and 2024 have introduced advanced DAS interrogators with improved sensitivity, multi-parameter sensing capabilities, and seamless integration into IoT and cloud-based platforms. Mergers and acquisitions are also influencing the landscape, with market leaders seeking to expand geographic reach and strengthen their presence in emerging regions. Innovation trends, particularly the convergence of DAS with distributed temperature sensing (DTS) and distributed strain sensing (DSS), are reshaping competitive dynamics and creating opportunities for market differentiation.

OptaSense Ltd.

Fotech Solutions Ltd.

Hifi Engineering Inc.

AP Sensing GmbH

Halliburton Company

Omnisens SA

Silixa Ltd.

Bandweaver Technologies Ltd.

Future Fibre Technologies Ltd.

Luna Innovations Incorporated

The Distributed Acoustic Sensing (DAS) market is evolving rapidly with the integration of advanced optical and digital technologies, enabling enhanced performance across industries such as oil & gas, transportation, security, and infrastructure monitoring. Modern DAS systems utilize coherent detection methods to transform standard single-mode optical fibers into continuous, real-time sensing arrays, covering distances of over 50 km with high spatial resolution. Recent innovations focus on AI-driven signal processing, which improves event classification accuracy by over 90% in certain industrial applications. Multi-parameter sensing capabilities, combining DAS with distributed temperature sensing (DTS) and distributed strain sensing (DSS), are expanding operational use cases, particularly in structural health monitoring and smart infrastructure. Miniaturized, portable DAS interrogators are gaining traction for temporary installations, such as event security and emergency monitoring. Cloud-based platforms now allow remote access to DAS data, enabling centralized control across multiple sites and integrating with predictive analytics for maintenance planning. Cybersecurity measures have also become critical, with encryption and secure data channels incorporated into modern DAS deployments. The emergence of low-power, high-sensitivity DAS modules is opening opportunities in renewable energy monitoring, environmental hazard detection, and seismic activity tracking, making the technology increasingly versatile for both high-volume industrial use and niche monitoring applications.

• In April 2024, Silixa launched its new Carina® Sensing System upgrade, delivering a 25% improvement in spatial resolution and extending the sensing range to 60 km, enabling enhanced performance for long-distance pipeline and perimeter monitoring applications.

• In February 2024, AP Sensing unveiled a hybrid DAS-DTS platform designed for integrated monitoring of temperature, strain, and acoustic data in a single unit, improving operational efficiency for energy and infrastructure operators.

• In October 2023, OptaSense introduced its next-generation fiber-optic intrusion detection software, featuring AI-based classification that reduced false alarms by 40% in field trials, significantly improving perimeter security monitoring.

• In May 2023, Halliburton expanded its fiber-optic sensing capabilities by introducing an advanced downhole DAS solution optimized for hydraulic fracturing operations, allowing operators to achieve higher accuracy in real-time fracture mapping.

The Distributed Acoustic Sensing (DAS) Market Report provides an in-depth assessment of the global industry landscape, encompassing technology developments, competitive dynamics, and application-specific demand drivers. The report covers all major market segments, including oil & gas pipeline monitoring, perimeter security, transportation infrastructure surveillance, and environmental hazard detection, with detailed insights into their respective adoption patterns and operational benefits. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing demand variations influenced by industrial activity, infrastructure development, and regulatory frameworks in each region.

From a technological perspective, the report evaluates coherent detection methods, hybrid sensing solutions (DAS-DTS-DSS), AI-powered analytics, portable and low-power DAS modules, and cloud-enabled monitoring platforms. The analysis also examines advancements in spatial resolution, sensing range, and cybersecurity for fiber-optic networks. Industry focus areas include energy sector monitoring, smart transportation systems, border and perimeter security, offshore infrastructure safety, and renewable energy applications such as wind farm and subsea cable monitoring.

The scope further includes emerging market opportunities, such as DAS integration with IoT networks for predictive maintenance and real-time data visualization, as well as niche applications in earthquake early-warning systems and mining operations. This comprehensive coverage ensures decision-makers have a clear understanding of the market’s technological breadth, geographic reach, and application diversity.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 549.35 Million |

|

Market Revenue in 2032 |

USD 1212.27 Million |

|

CAGR (2025 - 2032) |

10.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

OptaSense Ltd., Fotech Solutions Ltd., Hifi Engineering Inc., AP Sensing GmbH, Halliburton Company, Omnisens SA, Silixa Ltd., Bandweaver Technologies Ltd., Future Fibre Technologies Ltd., Luna Innovations Incorporated |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |