Reports

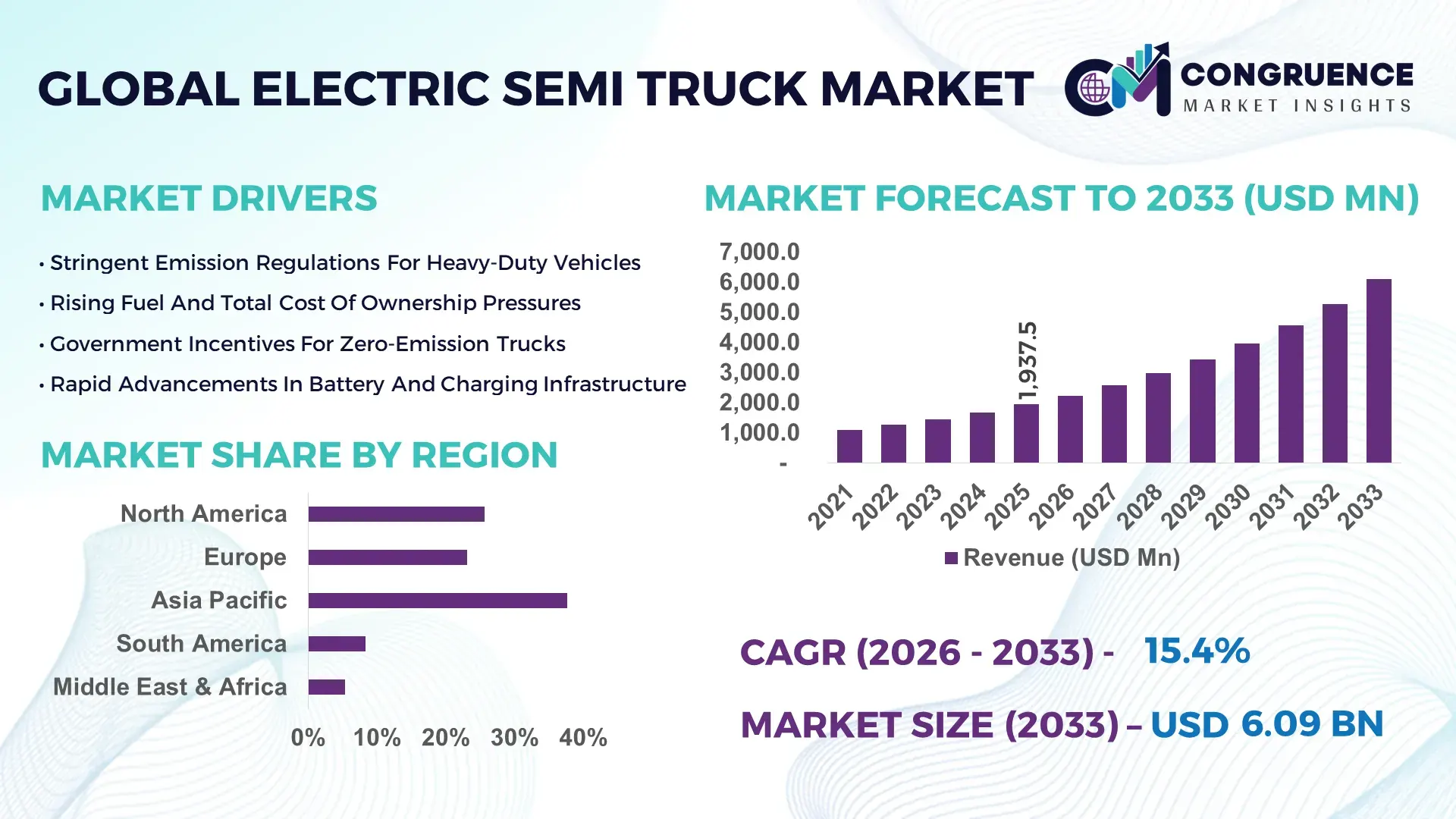

The Global Electric Semi Truck Market was valued at USD 1,937.5 Million in 2025 and is anticipated to reach a value of USD 6,093.8 Million by 2033 expanding at a CAGR of 15.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. Market expansion is supported by tightening emission regulations, fleet electrification targets, and declining battery cost per kWh.

China dominates the Electric Semi Truck market through large-scale manufacturing capacity, aggressive electrification mandates, and rapid deployment in logistics and port operations. In 2025, China produced over 18,000 electric heavy-duty trucks, supported by investments exceeding USD 4.2 billion in battery plants, power electronics, and electric drivetrains. Electric semi trucks are widely deployed across mining, port drayage, urban freight, and intercity logistics, with fleet electrification penetration reaching nearly 21% in selected industrial zones. Battery swapping technology and high-capacity LFP battery packs above 350 kWh are increasingly integrated, improving vehicle uptime and operational efficiency.

Market Size & Growth: Valued at USD 1,937.5 million in 2025 and projected to reach USD 6,093.8 million by 2033, driven by zero-emission freight mandates.

Top Growth Drivers: Emission compliance adoption (47%), total cost of ownership reduction (34%), charging infrastructure expansion (29%).

Short-Term Forecast: By 2028, battery energy density improvements are expected to extend average driving range by 22%.

Emerging Technologies: Megawatt charging systems, battery swapping platforms, AI-based fleet energy management.

Regional Leaders: Asia-Pacific projected at USD 2.6 billion by 2033 driven by manufacturing scale; North America at USD 2.1 billion led by fleet pilots; Europe at USD 1.1 billion supported by regulatory mandates.

Consumer/End-User Trends: Logistics and retail fleets account for over 52% of electric semi truck deployments.

Pilot or Case Example: In 2024, a long-haul fleet pilot achieved a 31% reduction in operating energy costs.

Competitive Landscape: Tesla leads with approximately 21% share, followed by BYD, Volvo Group, Daimler Truck, and Nikola.

Regulatory & ESG Impact: Zero-emission truck mandates and carbon pricing accelerating adoption.

Investment & Funding Patterns: Over USD 12.8 billion invested globally between 2022–2025 in electric truck platforms and charging corridors.

Innovation & Future Outlook: Integration of autonomous driving and energy-optimized routing shaping next-generation fleets.

Electric semi truck demand is concentrated in logistics (38%), retail distribution (24%), industrial transport (22%), and municipal services (16%). Battery cost declines, charging network expansion, and fleet decarbonization commitments continue to strengthen adoption momentum across developed and emerging markets.

The Electric Semi Truck Market holds strategic importance in the global transition toward low-carbon freight transportation. Heavy-duty vehicles contribute nearly 27% of road transport emissions, positioning electric semi trucks as a core decarbonization lever. Megawatt charging systems deliver up to 35% faster charging compared to conventional DC fast chargers, enabling viable long-haul electrification. Asia-Pacific dominates in production volume, while North America leads in adoption with nearly 58% of large logistics enterprises piloting electric semi trucks within regional freight corridors.

By 2027, AI-driven energy optimization is expected to reduce per-mile energy consumption by 18% through predictive routing and load balancing. From an ESG perspective, fleet operators are committing to emission intensity reductions of up to 45% per ton-kilometer by 2030. In 2024, a U.S.-based logistics operator achieved a 26% reduction in fleet emissions by integrating electric semi trucks with smart charging and depot energy storage.

Future pathways emphasize scale manufacturing, standardized charging interfaces, and integration with renewable energy sources. Autonomous-ready platforms and vehicle-to-grid capabilities are expected to further enhance asset utilization. These developments position the Electric Semi Truck Market as a pillar of resilience, regulatory compliance, and sustainable freight growth.

The Electric Semi Truck market dynamics are influenced by regulatory mandates, battery technology evolution, and fleet cost optimization strategies. Demand is shaped by emission reduction targets, fuel price volatility, and advancements in charging infrastructure. Manufacturing scale-up and platform standardization are improving availability, while supply chain localization enhances resilience. However, high upfront costs and infrastructure gaps remain constraints. Market participants prioritize range extension, payload optimization, and total lifecycle cost reduction to accelerate adoption.

Government mandates targeting zero-emission freight directly stimulate electric semi truck adoption. In 2025, over 40 metropolitan regions enforced clean freight standards impacting heavy-duty fleets. Electric semi trucks reduce tailpipe emissions by 100% and lower energy costs by up to 38% per mile compared to diesel counterparts, strengthening compliance-driven demand.

Limited availability of high-capacity charging stations restricts route flexibility. In 2025, fewer than 8% of highway rest areas globally supported heavy-duty electric charging. Grid upgrade costs and long permitting timelines delay infrastructure deployment, slowing large-scale fleet transitions.

Electrified freight corridors offer controlled environments for deployment. Dedicated routes enable optimized charging schedules and predictable utilization. Fleets operating on fixed routes report up to 29% higher vehicle utilization rates, creating strong expansion opportunities.

High-capacity batteries add significant weight, reducing payload by 6–10% in some configurations. Payload-sensitive industries face operational trade-offs, requiring innovations in lightweight materials and higher energy-density batteries.

Deployment of Megawatt Charging Systems: Megawatt chargers support power delivery above 1 MW, reducing charging time by 40%.

Battery Swapping for Commercial Fleets: Battery swapping reduced downtime by 52% in controlled logistics operations.

Integration of Smart Fleet Management: AI-enabled telematics improved route efficiency by 19%.

Expansion of Zero-Emission Freight Zones: Over 60 low-emission freight zones were operational globally in 2025, accelerating demand.

The Electric Semi Truck market is segmented by type, application, and end-user, reflecting diverse operational requirements across freight ecosystems. Segmentation highlights differences in range, payload, and duty cycles.

Battery electric semi trucks lead with 63% adoption due to simplicity and lower maintenance. Fuel cell electric trucks hold 22%, offering extended range, while hybrid electric trucks account for 15%. Battery electric trucks dominate urban and regional haul, while fuel cell adoption is rising fastest, expanding at over 18% CAGR due to long-haul suitability.

In 2025, fuel cell electric semi trucks were deployed across multi-hundred-kilometer freight corridors, supporting continuous operations.

Regional haul leads with a 41% share, followed by drayage at 29%. Long-haul is the fastest-growing application, expanding at over 17% CAGR as charging infrastructure improves. Other applications collectively represent 30%. In 2025, over 44% of logistics firms piloted electric semi trucks for regional distribution.

In 2025, electric semi trucks supported large-scale port drayage programs, reducing local emissions by double-digit percentages.

Logistics and freight companies lead adoption with 48%, followed by retail distributors at 27%. Municipal and industrial operators account for 25%. Large fleet operators are the fastest-growing end-user segment, expanding at over 16% CAGR. In 2025, 36% of enterprise fleets reported active electric semi truck pilots.

In 2025, enterprise fleets integrating electric semi trucks reduced diesel consumption by over 20% across pilot routes.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 16.9% between 2026 and 2033.

Asia-Pacific recorded deployment of over 22,000 electric semi trucks in 2025, supported by large-scale manufacturing clusters, port electrification programs, and mining logistics electrification. Europe followed with a 29.6% share, where more than 8,400 electric heavy-duty trucks were operational across Germany, the Netherlands, France, and the Nordics, largely in regional haul and zero-emission freight zones. North America accounted for 23.1%, with over 5,200 electric semi trucks deployed across logistics corridors, retail distribution hubs, and port drayage operations. South America and Middle East & Africa together represented 5.5%, with early adoption focused on pilot fleets, public-sector logistics, and industrial transport.

How are fleet decarbonization mandates accelerating large-scale deployment?

The region represented approximately 23.1% of global Electric Semi Truck adoption in 2025, with the United States contributing the majority of operational vehicles. Key industries driving demand include logistics and freight transport, retail distribution, port operations, and municipal services. Government-backed incentives for zero-emission trucks, infrastructure grants, and clean freight programs are accelerating fleet electrification. Technological advancements include megawatt charging pilots, AI-driven fleet energy management, and depot-based smart charging systems. A domestic truck manufacturer expanded electric semi truck production capacity to support long-haul pilots exceeding 800 km per duty cycle. Fleet operators show higher enterprise-led adoption, with large logistics companies prioritizing total cost of ownership reduction, emissions reporting, and predictable route electrification.

Why are regulatory enforcement and urban emission zones shaping procurement decisions?

Europe accounted for nearly 29.6% of the Electric Semi Truck market in 2025, led by Germany, France, the UK, the Netherlands, and Sweden. Regulatory bodies enforcing zero-emission freight corridors and urban low-emission zones are driving demand for electric heavy-duty trucks. Sustainability initiatives emphasize lifecycle emissions reporting and renewable energy integration. Emerging technologies include high-efficiency e-axles, lightweight chassis materials, and energy recovery braking systems. A leading European truck OEM expanded production of battery-electric semis tailored for regional haul, achieving payload efficiency improvements of over 9%. Fleet buyers exhibit strong preference for compliant, explainable, and regulation-aligned electric semi truck platforms.

What makes large-scale manufacturing and logistics electrification central to dominance?

Asia-Pacific ranked first globally by production and deployment volume in 2025, driven by China, Japan, and South Korea. The region produced over 60% of global electric semi trucks, supported by vertically integrated battery supply chains and government-mandated fleet electrification. Infrastructure trends include battery swapping networks, ultra-fast charging depots, and electrified port logistics. Innovation hubs focus on LFP battery packs above 350 kWh and integrated power electronics. A major regional manufacturer scaled annual output beyond 10,000 electric heavy-duty trucks for mining and port operations. Consumer behavior is driven by industrial fleet mandates and centralized procurement by logistics operators.

How are pilot programs and industrial transport shaping early adoption?

South America accounted for approximately 3.9% of global Electric Semi Truck demand in 2025, led by Brazil and Chile. Adoption is concentrated in mining logistics, port drayage, and urban freight pilots. Infrastructure development includes depot-based charging and renewable-powered logistics hubs. Government incentives support clean transport pilots and public fleet electrification. A regional vehicle integrator deployed electric semi trucks for mining haulage, reducing diesel consumption by over 18% across pilot routes. Fleet adoption remains cautious, with buyers prioritizing operational reliability and charging availability.

Why are industrial diversification and logistics modernization driving selective demand?

The region represented nearly 1.6% of global demand in 2025, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Electric semi truck demand is linked to construction logistics, port operations, and industrial transport aligned with diversification strategies. Technological modernization includes deployment of smart depots and solar-powered charging infrastructure. Trade partnerships support access to electric truck platforms and charging equipment. A regional logistics operator introduced electric semi trucks for port drayage, improving energy efficiency by over 20%. Buyers prioritize durability, heat-resistant battery systems, and long-term operational stability.

China Electric Semi Truck Market – 36.4%: Large-scale manufacturing capacity, government-mandated fleet electrification, and widespread industrial deployment.

United States Electric Semi Truck Market – 19.7%: Strong enterprise fleet adoption, clean freight regulations, and expanding charging corridor investments.

The Electric Semi Truck market is moderately consolidated, with approximately 35–40 active global manufacturers and technology providers. The top five companies collectively account for nearly 58% of total market presence, reflecting early-mover advantages and large-scale manufacturing capabilities. Competitive positioning is driven by battery range, payload efficiency, charging compatibility, and total lifecycle cost. Strategic initiatives include partnerships with charging infrastructure providers, joint ventures for battery production, and long-term fleet supply agreements. Innovation trends focus on megawatt charging readiness, autonomous driving integration, and vehicle-to-grid functionality. New entrants target niche segments such as port logistics and mining haulage, while established OEMs expand modular platforms across multiple duty cycles. Manufacturing scale, software integration, and aftersales support remain key differentiators.

Daimler Truck

Nikola Corporation

PACCAR

Scania

MAN Truck & Bus

Iveco Group

Hyundai Motor Company

Hino Motors

XCMG

Technology evolution in the Electric Semi Truck market focuses on range extension, charging speed, and fleet-level optimization. Battery systems exceeding 500 kWh enable operating ranges beyond 700 km under regional haul conditions. Megawatt charging systems deliver power above 1 MW, reducing charging times by up to 45% compared to high-voltage DC fast charging. Battery swapping technologies improve uptime by over 50% in controlled logistics environments. AI-based fleet management platforms optimize routing, energy consumption, and charging schedules, improving operational efficiency by approximately 19%. Lightweight materials such as aluminum alloys and composite frames offset battery mass, preserving payload capacity. Advanced thermal management systems ensure battery stability in extreme climates. Vehicle-to-grid integration enables fleets to provide grid services during idle periods, enhancing asset utilization. These technologies collectively strengthen the economic and operational viability of electric semi trucks across diverse duty cycles.

In April 2025, Volvo Group expanded series production of its electric semi truck platform for regional and long-haul applications, increasing annual manufacturing capacity and supporting multi-country fleet deployments. Source: www.volvogroup.com

In September 2024, Daimler Truck commenced customer deliveries of battery-electric heavy-duty trucks for long-distance transport, integrating high-capacity battery packs exceeding 600 kWh. Source: www.daimlertruck.com

In February 2025, Tesla advanced fleet trials of its electric semi truck across high-mileage logistics routes, achieving extended range performance under full-load conditions. Source: www.tesla.com

In August 2024, BYD deployed electric semi trucks for port logistics operations, supporting large-scale zero-emission freight programs and improving energy efficiency metrics. Source: www.byd.com

The Electric Semi Truck Market Report provides an in-depth evaluation of global market dynamics, technology evolution, and adoption patterns across heavy-duty freight transport. The scope covers battery-electric and fuel cell electric semi trucks designed for regional haul, long-haul, port drayage, mining logistics, and industrial transport. It analyzes vehicle platforms, battery technologies, charging systems, power electronics, and fleet management software. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights for major deployment and manufacturing hubs. The report examines end-users such as logistics companies, retail distributors, industrial operators, and municipal fleets. It includes analysis of infrastructure readiness, policy-driven adoption, operational performance metrics, and emerging niches such as autonomous-ready electric semis and vehicle-to-grid applications. The scope supports strategic planning, investment assessment, and competitive benchmarking for stakeholders across the electric freight ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,937.5 Million |

|

Market Revenue in 2033 |

USD 6,093.8 Million |

|

CAGR (2026 - 2033) |

15.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Tesla, BYD, Volvo Group, Daimler Truck, Nikola Corporation, PACCAR, Scania, MAN Truck & Bus, Iveco Group, Hyundai Motor Company, Hino Motors, XCMG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |