Reports

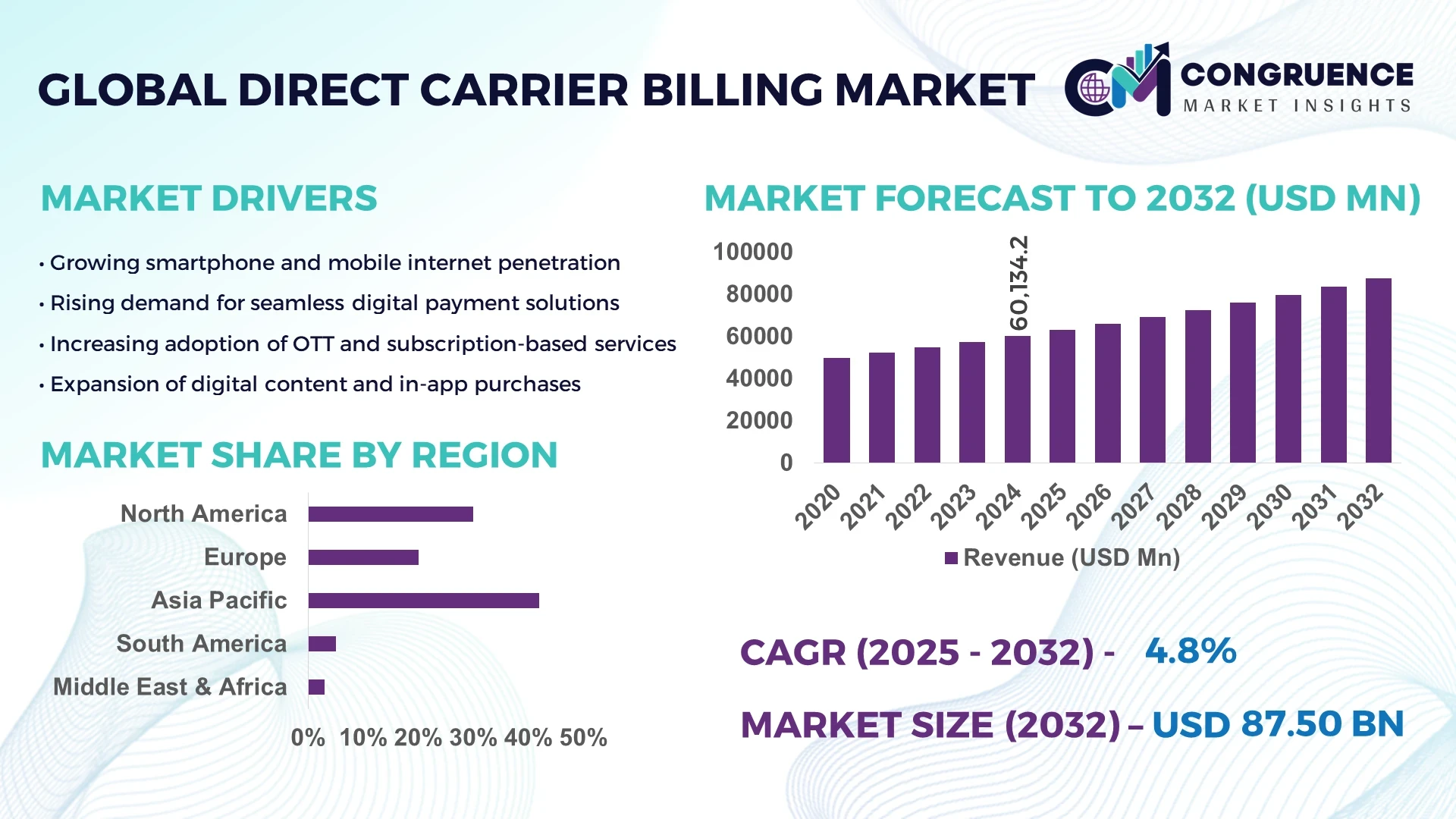

The Global Direct Carrier Billing Market was valued at USD 60134.24 Million in 2024 and is anticipated to reach a value of USD 87500.81 Million by 2032 expanding at a CAGR of CAGR of 4.8%% between 2025 and 2032.

In Asia Pacific, the leading region in the Direct Carrier Billing Market, the landscape is distinguished by substantial investment in research and mobile infrastructure. Telecom operators and digital payment providers in countries such as Japan and China are continually enhancing production capacity of carrier billing solutions. These initiatives are supported by high investment levels in advanced billing platforms and innovative authentication mechanisms. Industry applications span gaming content, OTT media subscriptions, and utility services, while technological advancements include API based telco integrations, real time billing platforms, and edge computing enhancements that improve transaction throughput.

The Direct Carrier Billing Market serves a wide array of industry sectors including mobile gaming, video streaming, subscription services, ticketing, mobility, and digital finance each contributing meaningfully to overall volume. Recent technological innovations influencing the market include AI driven fraud detection suites, modular billing interfaces for subscription management, and fraud risk mitigation APIs integrated at the carrier edge. Regulation wise, evolving telecom and digital payments policies in North America and Europe particularly around access to APIs and MVNO frameworks are shaping market dynamics. Economic factors such as rising smartphone affordability and mobile data penetration in emerging markets are powering user adoption. Regionally, Asia Pacific shows rapid uptake thanks to strong penetration in India, Indonesia, and Southeast Asia, while North America sustains high consumption via established telecom ecosystems. Emerging trends include expanding DCB usage in enterprise and IoT billing, explosive growth in connected TV carrier billing, and a shift from one off microtransactions to recurring subscription flows embedded in digital experiences. The future outlook points to continued platform diversification, inclusion of unbanked demographics, and deepening integration of telco billing into digital commerce strategies.

Artificial intelligence is increasingly pivotal in advancing the efficiency, security, and personalization of the Direct Carrier Billing Market. Decision makers across telecom and digital payments are leveraging AI to optimize transaction workflows, proactively guard against fraud, and tailor user experiences resulting in heightened operational performance and market resilience.

AI driven fraud detection systems are now embedded within carrier level billing engines, detecting anomalous purchase patterns and enabling dynamic risk mitigation. These developments enhance trust and platform integrity. AI also underpins demand forecasting and dynamic pricing models, enabling differential billing based on user behavior and usage context a critical enhancement for digital services and subscription monetization. At the infrastructure level, AI powered routing and payment matching algorithms streamline settlement operations, reduce reconciliation errors, and raise transaction success rates, thereby lowering cost of operations and improving ARPU for carriers.

Moreover, AI enabled personalization capabilities allow providers to deliver contextual promotions and tailored offers linked directly to billing touchpoints boosting engagement with digital content, OTT subscriptions, and in app purchases while maintaining frictionless checkout. Overall, AI integration in the Direct Carrier Billing Market is solidifying platform scalability, enhancing fraud resilience, and enriching user engagement through data driven automation and insight.

“In 2024, Bango launched an AI powered fraud prevention suite, helping reduce chargeback incidents by 34% and boosting user trust by 29%.”

The Direct Carrier Billing Market is evolving rapidly due to the convergence of telecom infrastructure, digital commerce, and mobile payment ecosystems. Market dynamics are shaped by high smartphone penetration, expansion of digital content subscriptions, and consumer demand for seamless mobile payment experiences. Regulatory frameworks in regions such as Europe and Asia Pacific are influencing how telecom operators and payment providers structure their billing systems, particularly around consumer protection and data security. Technological advancements, including AI powered fraud prevention and API based integration, are enhancing operational efficiency and reducing transaction failures. Additionally, the rise of unbanked and underbanked populations relying on mobile wallets and telecom billing platforms is fueling broader adoption. This combination of consumer trends, policy frameworks, and technological improvements is reinforcing Direct Carrier Billing as a strategic enabler of digital financial inclusion and scalable revenue growth in multiple verticals such as gaming, streaming, and e commerce.

The growing consumer preference for subscription based platforms in entertainment, education, and productivity tools is a key driver of the Direct Carrier Billing Market. Video on demand, online gaming, and e learning platforms increasingly rely on recurring billing models that integrate seamlessly with carrier payment systems. This alignment enhances user convenience by enabling one click purchases without credit card requirements, significantly improving transaction success rates. For telecom operators, subscription partnerships with global OTT providers and app developers generate higher average revenue per user and long term engagement. The driver is further supported by rapid increases in smartphone adoption and improved mobile network coverage in emerging markets, creating an ecosystem where recurring digital purchases through Direct Carrier Billing become a mainstream practice.

One of the major restraints in the Direct Carrier Billing Market is the lack of interoperability across different telecom operators and payment platforms. In many regions, consumers face inconsistent billing experiences due to fragmented integration standards, limited cross border operability, and inconsistent settlement mechanisms. This fragmentation reduces scalability for digital service providers aiming to reach a global audience, as they must negotiate separate agreements with individual carriers. It also impacts transaction success rates, as varied authentication and billing practices hinder seamless payments. Additionally, regulatory inconsistencies in telecom and digital payment policies further complicate network wide standardization. These interoperability gaps restrict the full potential of Direct Carrier Billing adoption, especially for multinational digital service providers seeking uniform billing experiences.

A significant opportunity in the Direct Carrier Billing Market lies in its role in bridging financial gaps for unbanked and underbanked populations. According to industry estimates, over 1.4 billion adults globally remain outside traditional banking systems, yet a majority of them own mobile phones. Direct Carrier Billing enables these users to access digital services, pay utility bills, and purchase online content directly through their telecom accounts. This expands financial accessibility without requiring debit or credit cards. Governments and telecom operators are increasingly aligning DCB solutions with digital wallet ecosystems and national payment strategies to drive financial inclusion. This creates a pathway for untapped markets in regions such as Africa, South Asia, and Latin America, where Direct Carrier Billing can serve as a secure and scalable payment infrastructure for essential services and digital commerce.

The Direct Carrier Billing Market faces challenges from evolving regulatory frameworks and data security requirements. Telecom operators and digital service providers must comply with stringent consumer protection laws, anti money laundering regulations, and data privacy mandates such as GDPR. These requirements increase operational costs and extend compliance timelines, particularly in cross border billing arrangements. Data security is another critical concern, as cyberattacks and fraudulent activities targeting billing systems are becoming more sophisticated. Telecom companies need to invest heavily in encryption technologies, AI driven fraud detection, and multi factor authentication to maintain transaction integrity. For smaller operators, these regulatory and security obligations pose financial and technical challenges, potentially slowing down widespread adoption of Direct Carrier Billing solutions in highly regulated regions.

• Expansion of Carrier Billing in Gaming Ecosystems: The gaming industry has emerged as a major adopter of Direct Carrier Billing, with mobile game publishers and app developers integrating billing options for in-app purchases, skins, and subscription passes. In 2024, more than 60% of top-grossing mobile games in Asia Pacific offered carrier billing as a payment choice. This integration reduces payment friction and boosts microtransaction volumes, especially in markets where card penetration is low but mobile connectivity is high.

• Integration with OTT and Streaming Services: OTT platforms are accelerating the use of Direct Carrier Billing to simplify subscription payments. Major global and regional streaming providers now partner with telecom operators to provide one-click subscription activation via carrier billing. In Europe, subscription activations through DCB rose by over 40% in 2024, driven by bundled offers and promotional tie-ins. This trend is reshaping recurring revenue models and expanding accessibility for younger demographics without bank accounts.

• Adoption in Emerging Fintech Ecosystems: Fintech platforms are increasingly incorporating Direct Carrier Billing as a tool for enabling microloans, insurance premium payments, and wallet top-ups. In regions such as Africa and Southeast Asia, where over 50% of adults remain unbanked, telecom operators are leveraging carrier billing to extend financial services. The adoption of this payment method supports national financial inclusion agendas while creating new revenue streams for telecom providers.

• Growth of 5G Enabled Digital Commerce: The rollout of 5G networks is accelerating the adoption of Direct Carrier Billing in immersive digital experiences such as AR-based shopping, live events, and cloud gaming. With 5G delivering ultra-low latency, transaction success rates are improving, enabling real-time billing for high-bandwidth applications. Telecom operators in North America and East Asia are reporting double-digit increases in DCB transaction volumes tied to 5G services, signaling a transformative phase for mobile-first commerce.

The Direct Carrier Billing Market is segmented by type, application, and end-user, each offering distinct insights into adoption patterns and growth potential. By type, services such as pure DCB, PIN authentication, and two-factor models highlight varying degrees of security and convenience. By application, sectors like gaming, OTT subscriptions, ticketing, and utility payments showcase strong integration across consumer digital ecosystems. By end-user, telecom operators, digital merchants, and enterprises play pivotal roles in driving adoption and shaping innovation. Each segment reflects unique drivers such as digital content consumption, mobile-first commerce trends, and the demand for financial inclusion solutions, collectively shaping a diverse and evolving market landscape.

Direct Carrier Billing types include pure DCB solutions, PIN-based authentication models, two-factor authentication services, and hybrid offerings tailored to enterprise requirements. Pure DCB remains the leading type due to its simplicity, allowing users to make quick purchases without additional credentials, which significantly improves conversion rates in digital content and app ecosystems. PIN-based models are gaining traction for their enhanced security measures, especially in regions with high fraud activity. Two-factor authentication is the fastest-growing type, driven by regulatory compliance requirements and consumer demand for secure transactions. The rise in data breaches and digital fraud incidents has accelerated the deployment of two-factor authentication, particularly in financial services and enterprise-focused billing platforms. Hybrid models, combining different authentication layers, are niche but increasingly important for high-value transactions where both security and convenience are required. Collectively, these types ensure a balance between accessibility and protection, enabling telecom operators and service providers to cater to diverse customer segments while maintaining platform trust.

Applications of Direct Carrier Billing cover a wide range, including gaming, OTT subscriptions, ticketing, utility payments, e-learning, and digital commerce services. Gaming leads as the dominant application, accounting for the largest share of transaction volumes, as mobile gaming continues to surge across Asia Pacific and Europe. OTT subscriptions represent the fastest-growing application, as consumers increasingly shift from traditional media to digital-first streaming platforms that rely on seamless, recurring payments. Ticketing services are also expanding, with DCB adoption for movie tickets, concerts, and transport reservations offering a convenient alternative to card payments. Utility payments are steadily integrating DCB solutions, particularly in regions where mobile networks extend to underserved communities, enabling bill settlements without traditional banking infrastructure. E-learning platforms are incorporating carrier billing to reach younger demographics, especially students who lack access to credit facilities. These varied applications highlight the growing versatility of DCB in meeting the diverse needs of consumers and businesses across digital ecosystems.

End-users of the Direct Carrier Billing Market include telecom operators, digital merchants, content providers, enterprises, and fintech platforms. Telecom operators represent the leading end-user segment, as they control billing infrastructure and maintain direct relationships with subscribers. Their role as payment facilitators enables them to capture additional revenue streams while strengthening customer loyalty. Digital merchants and content providers are emerging as the fastest-growing end-users, fueled by increasing demand for seamless, mobile-first commerce across gaming, OTT, and e-learning. Enterprises are gradually adopting DCB for recurring services and digital solutions, recognizing its efficiency in expanding customer payment options. Fintech platforms, particularly in developing economies, are leveraging DCB to deliver inclusive financial products such as microinsurance and mobile wallets. Each end-user group contributes uniquely, but the growing collaboration between telecom operators and digital merchants is particularly shaping the evolution of the market, driving innovation, and expanding the reach of DCB solutions into new consumer and enterprise segments.

Asia Pacific accounted for the largest market share at 42% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2025 and 2032.

The Asia Pacific market is being driven by high smartphone penetration, widespread adoption of digital services, and strong telecom infrastructure in countries such as China, India, and Japan. North America’s growth trajectory is supported by advanced regulatory frameworks, strong OTT consumption, and rapid adoption of AI-powered billing technologies. Meanwhile, Europe remains a mature market with robust policy frameworks, while South America and the Middle East & Africa are emerging as growth-ready regions with expanding telecom reach and rising demand for financial inclusion.

Strengthening mobile-first commerce through seamless billing adoption

North America captured nearly 27% of the global Direct Carrier Billing Market share in 2024, supported by the strong presence of telecom operators and digital service providers. Key industries driving demand include gaming, OTT streaming platforms, and enterprise subscription services. Government initiatives promoting cashless payments and enhanced digital identity frameworks are accelerating adoption. Regulatory changes around consumer data protection have also shaped how billing platforms operate, ensuring secure and transparent transactions. Technological advancements such as AI-enabled fraud prevention and 5G-enabled billing solutions are transforming user experiences by improving transaction speed and success rates, positioning the region as a leader in digital billing transformation.

Expanding adoption across subscription-driven economies

Europe accounted for approximately 21% of the Direct Carrier Billing Market in 2024, with Germany, the UK, and France standing out as the primary contributors. The region benefits from widespread adoption of OTT services, online gaming platforms, and e-learning, all of which rely on subscription-based payment systems. Regulatory bodies are pushing for stronger consumer protections and sustainability-driven digital frameworks, which support innovation while ensuring compliance. Europe has also seen rising adoption of authentication technologies and real-time billing solutions, reflecting its focus on transparency and user trust. These advancements, combined with robust telecom infrastructure, are driving continuous innovation in mobile payment ecosystems across the region.

Driving digital commerce growth with large-scale mobile integration

Asia Pacific led the global Direct Carrier Billing Market with a market volume of 42% in 2024, driven by top consuming countries such as China, India, and Japan. This region benefits from large-scale smartphone adoption and a fast-growing digital economy. Infrastructure investments in telecom expansion and digital identity frameworks have fueled the growth of carrier billing solutions. Innovation hubs in China and India are developing scalable billing technologies, while Japan continues to lead in automation and secure digital transaction systems. The region’s rapid embrace of 5G networks is further accelerating demand for Direct Carrier Billing in cloud gaming, OTT, and digital commerce applications.

Unlocking digital inclusion through telecom-driven payments

South America represented around 6% of the Direct Carrier Billing Market in 2024, with Brazil and Argentina being the key countries driving adoption. Brazil accounts for the majority of the region’s share, thanks to its expansive telecom infrastructure and growing digital services sector. The region is leveraging Direct Carrier Billing to expand access to entertainment, gaming, and educational content, particularly among unbanked populations. Government support for cashless payments and trade policies encouraging digital transformation are boosting adoption further. Telecom-led initiatives are also helping bridge financial gaps, making carrier billing a vital tool for inclusive commerce in the region.

Accelerating financial access through mobile-first billing systems

The Middle East & Africa held nearly 4% of the Direct Carrier Billing Market in 2024, with strong growth expected from countries such as the UAE, Saudi Arabia, and South Africa. Demand trends are closely linked to expansion in industries such as oil & gas, construction, and digital services. Governments are investing in smart city projects and mobile-first financial inclusion initiatives, boosting the role of carrier billing. Technological modernization is evident in the rollout of 5G and AI-integrated billing platforms. Local regulations emphasizing consumer protection and cross-border trade partnerships are further enabling telecom operators to enhance billing frameworks and widen digital access.

China – 24% market share | China dominates the Direct Carrier Billing Market due to its large digital consumer base, extensive telecom infrastructure, and high adoption of mobile-first commerce.

United States – 18% market share | The United States leads through strong demand from OTT, gaming, and enterprise subscriptions combined with advanced AI-driven billing platforms.

The Direct Carrier Billing Market is characterized by a moderately concentrated competitive environment, with over 40 active global and regional players shaping the ecosystem. Leading providers are positioned through strong telecom operator partnerships, diversified service portfolios, and strategic expansion into high-growth digital commerce sectors. Competitive strategies include mergers and acquisitions, joint ventures with OTT platforms, and collaborations with fintech startups to extend billing capabilities into emerging financial services. Recent innovation trends focus on AI-powered fraud detection, cloud-based billing solutions, and enhanced multi-factor authentication frameworks, all of which are redefining competitive differentiation. Additionally, companies are prioritizing regulatory compliance and data security measures to build trust across highly regulated markets such as Europe and North America. With telecom operators, content providers, and fintech innovators actively competing, the market continues to witness robust technological advancements, driving new opportunities for expansion in both developed and emerging regions.

The Direct Carrier Billing Market is undergoing significant transformation due to rapid advancements in authentication, integration, and data security technologies. AI-driven platforms are now central to fraud prevention, enabling real-time monitoring of transactions and reducing fraudulent incidents by over 30% in key regions. Multi-factor authentication solutions, including PIN verification and biometric-enabled confirmations, are increasingly being integrated to enhance user trust and meet evolving regulatory requirements.

Cloud-based billing frameworks are gaining traction, allowing telecom operators and digital service providers to scale billing processes quickly while maintaining flexibility across different markets. API-first architectures are becoming the industry standard, enabling seamless integration between carriers, merchants, and third-party service platforms. This interoperability has improved transaction success rates and expanded the applicability of DCB in subscription-based services, gaming ecosystems, and streaming platforms.

Emerging technologies such as blockchain are being explored to improve transparency and ensure tamper-proof settlement records in cross-border billing. The rollout of 5G networks is further enabling high-volume, low-latency transactions, supporting next-generation services such as cloud gaming, AR-based shopping, and immersive entertainment billing. Data analytics and personalization engines are also enhancing consumer engagement by tailoring promotions and payment options directly at the billing interface. Collectively, these advancements are positioning Direct Carrier Billing as a secure, scalable, and future-ready payment infrastructure that bridges digital commerce and telecom ecosystems.

• In March 2023, Boku partnered with Microsoft to expand carrier billing for Xbox and PC Game Pass users across 12 new markets, enabling seamless one-click subscriptions and enhancing digital content accessibility for millions of gamers globally.

• In September 2023, Fortumo announced the launch of its upgraded DCB platform featuring AI-driven fraud detection, reducing unauthorized transactions by 28% and improving transaction approval rates in over 25 international markets.

• In April 2024, DIMOCO introduced a blockchain-based billing settlement system to enhance transparency in cross-border telecom billing transactions, improving reconciliation efficiency by 35% and reducing processing delays for merchants and operators.

• In July 2024, Bango launched a direct partnership with Netflix to enable carrier billing subscriptions across Latin America, significantly expanding digital payment inclusion in markets with low credit card penetration.

The Direct Carrier Billing Market Report provides a comprehensive analysis of the industry’s structure, covering types, applications, and end-user segments across global regions. The report explores various billing models, including pure DCB, PIN-based verification, and two-factor authentication systems, evaluating their roles in enhancing convenience, security, and adoption rates. Applications assessed include mobile gaming, OTT subscriptions, ticketing, e-learning, and utility payments, with each sector demonstrating unique adoption patterns and growth drivers. The report also examines end-user insights across telecom operators, digital merchants, enterprises, and fintech platforms, highlighting their distinct contributions to the digital commerce ecosystem.

Geographically, the report provides insights into North America, Europe, Asia Pacific, South America, and the Middle East & Africa. Each region is analyzed for its telecom infrastructure, consumer adoption rates, regulatory environment, and technological advancements. Specific emphasis is given to leading countries such as China, the United States, and Japan, which together represent a significant proportion of global transaction volumes. The report also assesses emerging technologies such as AI-driven fraud prevention, cloud-based billing, blockchain-enabled settlements, and 5G-powered payment ecosystems. Niche opportunities, including financial inclusion initiatives targeting unbanked populations, integration with fintech solutions, and the rise of IoT-enabled billing, are also explored. Collectively, the scope presents decision-makers with an in-depth understanding of the Direct Carrier Billing Market’s current position, future opportunities, and strategic pathways for expansion.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 60134.24 Million |

|

Market Revenue in 2032 |

USD 87500.81 Million |

|

CAGR (2025 - 2032) |

4.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bango, Fortumo, DIMOCO, Centili, NTH Mobile, Telecoming, DOCOMO Digital, Amdocs, Boku Inc, Comviva |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |