Reports

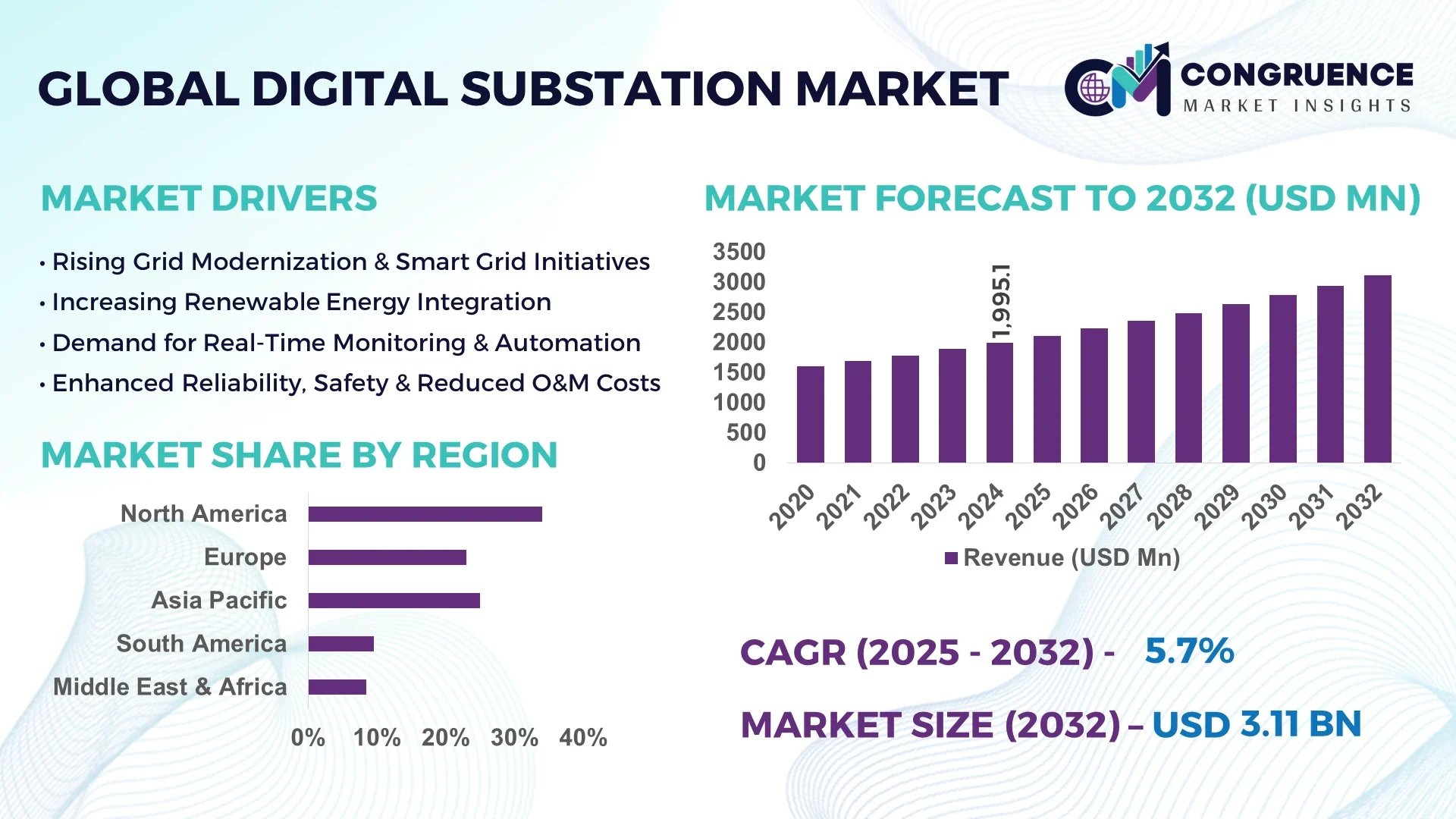

The Global Digital Substation Market was valued at USD 1995.08 Million in 2024 and is anticipated to reach a value of USD 3108.57 Million by 2032 expanding at a CAGR of 5.7%% between 2025 and 2032.

Asia Pacific is the leading region in the Digital Substation Market, demonstrating exceptional production capacity across high-voltage and medium-voltage equipment. Significant investments in grid modernization in China and India are advancing the deployment of advanced automated systems, while technological innovations—such as modular substation designs and IEC 61850-compliant intelligent electronic devices—are being implemented at scale in the region’s most critical power infrastructure, supporting real-time monitoring, control, and digital protection.

Key industry sectors within the Digital Substation Market include utilities, heavy industries, transportation infrastructure, and mining sectors, with utility applications representing a substantial portion of demand. Recent technological breakthroughs include enhanced process-interface units that consolidate functionality, reduce wiring, and increase flexibility and security in grid operations. Regulatory and environmental factors—such as stringent grid reliability mandates, renewable energy integration targets, and evolving cybersecurity requirements—are driving adoption globally. Regional consumption patterns reflect surging deployment in Asia Pacific and North America, fuelled by industrial expansion, urbanization, and strategic electrification initiatives. Emerging trends include the integration of digital twin simulations for asset lifecycle optimization, widespread adoption of fiber-optic and SCADA-based communications architectures, and the convergence of cloud-based solutions for remote monitoring and predictive maintenance. The market outlook anticipates sustained growth, innovation, and diversification as stakeholders prioritize resilience, efficiency, and sustainable expansion in digital substations.

AI is dramatically transforming the Digital Substation Market through enhancements in operational efficiency, predictive maintenance, and cybersecurity resilience. Intelligent systems are now integrated into substations to continuously monitor transformer health, circuit breaker performance, and fault conditions, enabling operators to intervene proactively and avoid disruptions. AI-driven analytics optimize fault detection by leveraging real-time data streams and condition indicators, significantly reducing unplanned downtime and extending asset lifespan.

In utility-scale deployments, AI is paired with IoT-enabled sensors and fiber-optic networks to enable advanced diagnostics and remote supervision. AI-enabled predictive models analyze signals from intelligent electronic devices, identifying early signs of equipment degradation and allowing maintenance to be scheduled before failures occur. This capability improves grid availability and reduces operational costs. In addition, AI aids in threat detection: systems now incorporate multilayered security frameworks that use real-time anomaly detection to mitigate cybersecurity threats targeting digital substations.

Cloud-based AI platforms further accelerate modernization by offering scalable computing and remote analytics for grid operators, enabling faster decision-making and enhanced resilience, particularly as grids incorporate distributed renewables and face increasing climate risks. As utilities adopt digital twin technology, AI enhances scenario simulation and performance forecasting, allowing operators to model system behavior under stress and streamline grid adaptation dynamics—advancing the reliability and adaptability of modern power networks within the Digital Substation Market.

“In January 2025, a novel in-context learning model utilizing transformer architecture demonstrated over 85 percent accuracy in detecting zero-day cyber-attacks in IEC-61850-based digital substations, significantly outperforming current state-of-the-art detection systems.”

The Digital Substation Market is shaped by a combination of technological innovations, grid modernization programs, and the accelerating shift toward renewable energy integration. Increasing adoption of smart grid initiatives worldwide is fueling the deployment of advanced digital substations that incorporate intelligent electronic devices, real-time monitoring systems, and cloud-enabled analytics. Industry players are increasingly investing in scalable automation platforms that ensure grid reliability while reducing operational expenditures. Regulatory frameworks promoting cybersecurity, sustainability, and energy efficiency are further driving system upgrades across power networks. Additionally, regional variations in energy demand, industrial expansion, and electrification of transportation sectors are contributing to evolving market dynamics, creating a robust ecosystem for growth and innovation in the Digital Substation Market.

Substantial investments in renewable energy capacity expansion and large-scale grid modernization projects are significantly driving the Digital Substation Market. Utilities and governments across Asia, Europe, and North America are investing in next-generation substation automation to support distributed energy resources, solar and wind integration, and dynamic load balancing. Digital substations equipped with process bus technology and advanced condition monitoring enhance flexibility and reduce equipment downtime by up to 30 percent compared to conventional systems. Countries such as China and India have announced multi-billion-dollar programs aimed at digitalizing transmission and distribution infrastructure, accelerating the adoption of digital substations. These upgrades not only improve operational efficiency but also ensure compliance with stricter energy reliability mandates, reinforcing the market’s long-term trajectory.

One of the most notable restraints in the Digital Substation Market is the high upfront cost and complexity of implementation. The deployment of digital substations requires investment in intelligent electronic devices, optical fiber networks, advanced communication protocols, and cybersecurity measures, which can be cost-prohibitive for smaller utilities and emerging economies. In addition, integration challenges with legacy infrastructure and the need for specialized technical expertise often delay project execution. Reports suggest that initial installation costs for a fully digitalized substation can be 25 to 40 percent higher than traditional systems, posing a financial barrier to widespread adoption. The shortage of skilled professionals trained in IEC 61850 protocol and cybersecurity also limits scalability, creating hurdles for stakeholders seeking rapid digital transformation.

The adoption of digital twin solutions presents a substantial opportunity within the Digital Substation Market. By creating virtual replicas of physical assets, operators can simulate real-time operating conditions, predict equipment failures, and extend asset lifecycle by more than 20 percent. Utilities are leveraging AI-driven digital twins to optimize maintenance schedules, reduce operational downtime, and lower total cost of ownership. In 2024, several pilot projects demonstrated that digital twin platforms could decrease fault response times by nearly 40 percent, highlighting their potential to transform substation management. As global grids become increasingly complex with the integration of renewable energy, electric vehicles, and distributed power generation, the demand for predictive maintenance tools will expand, positioning digital twin technology as a cornerstone of future substation ecosystems.

Cybersecurity remains one of the most pressing challenges in the Digital Substation Market. As substations evolve into fully digital and interconnected nodes within the power grid, they become vulnerable to sophisticated cyber threats targeting communication networks, automation protocols, and control systems. Critical infrastructure attacks have increased globally, with more than 60 percent of utilities reporting attempted intrusions in the past two years. Digital substations that operate on IEC 61850 protocols and rely on IP-based communication systems face heightened risks of malware, ransomware, and zero-day attacks. Addressing these threats requires continuous investment in multi-layered defense systems, real-time anomaly detection, and compliance with stringent cybersecurity standards. However, the rising costs of implementing such security measures, along with evolving regulatory frameworks, remain a substantial challenge for industry stakeholders.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated digital substations is reshaping deployment models across power infrastructure. Components such as control modules, switchgear, and protection units are increasingly manufactured off-site using automated precision equipment and then assembled on-site, cutting installation time by nearly 40 percent. This trend is particularly strong in Europe and North America, where utilities demand rapid project execution to meet rising energy needs. The approach also reduces labor requirements and ensures higher safety standards, making modular substations a preferred solution in regions with high construction costs.

• Integration of Fiber-Optic Communication Networks: Digital substations are increasingly incorporating fiber-optic technologies to replace traditional copper wiring, improving both reliability and bandwidth. This trend allows for faster data transmission and greater immunity to electromagnetic interference, which is crucial for high-voltage operations. Utilities deploying fiber-optic networks report improved accuracy in data collection and real-time performance monitoring. Adoption is expanding rapidly in Asia Pacific, where new greenfield projects benefit from advanced communication infrastructure without legacy constraints.

• Adoption of Digital Twin and Predictive Maintenance Platforms: The deployment of digital twin platforms is accelerating, enabling operators to replicate substation assets in virtual environments for predictive analysis. By simulating real-time conditions, utilities can predict component failures and extend asset lifecycles by more than 20 percent. Predictive maintenance powered by AI and digital twins has shown to reduce unexpected outages by nearly 35 percent. This trend is driving a shift from reactive to proactive maintenance strategies, particularly in large-scale transmission projects.

• Growing Cybersecurity Integration in Substation Infrastructure: As digital substations evolve into connected, data-driven ecosystems, cybersecurity measures are becoming a built-in component rather than an add-on. Utilities are now embedding intrusion detection, anomaly monitoring, and encryption systems directly into substation design. A growing number of projects launched in 2024 and 2025 have dedicated at least 10 percent of overall project costs to cybersecurity enhancements, demonstrating its strategic importance. This trend is crucial as utilities face increasingly complex cyber threats targeting operational continuity.

The Digital Substation Market is segmented by type, application, and end-user, each playing a critical role in shaping overall industry dynamics. By type, components such as hardware, software, and services contribute distinctly to substation performance and lifecycle management. Application-wise, digital substations serve utilities, industrial plants, renewable energy projects, and transportation infrastructure, each with unique demand drivers. End-user insights reveal that utilities lead adoption, while industries such as oil and gas, mining, and manufacturing are rapidly expanding usage due to automation and efficiency benefits. This segmentation underscores the diverse influence of technological integration, evolving energy infrastructure, and regional regulatory frameworks on the Digital Substation Market.

Digital substation types include hardware, software, and services, each addressing specific operational needs. Hardware remains the leading type, driven by growing demand for intelligent electronic devices, digital relays, and fiber-optic communication networks that form the foundation of advanced substations. Rising deployment of high-voltage equipment and process bus systems further strengthens hardware’s role as the primary revenue generator. Software is emerging as the fastest-growing type, supported by increasing adoption of AI-enabled platforms, predictive maintenance tools, and digital twin applications that provide enhanced operational visibility and grid resilience. Services, including installation, integration, and maintenance, contribute significantly to ensuring long-term system reliability, especially in projects with legacy infrastructure upgrades. Together, these segments highlight the balance between physical infrastructure deployment and digital intelligence integration, shaping the trajectory of the Digital Substation Market.

Utilities represent the leading application segment in the Digital Substation Market, driven by ongoing modernization programs and the need to accommodate distributed renewable generation. Utility companies prioritize digital substations for their ability to improve grid stability, enhance monitoring, and reduce outage risks across large-scale transmission networks. The fastest-growing application is renewable energy integration, where digital substations are critical in managing variable loads from solar and wind installations while ensuring seamless power quality. Industrial applications, particularly in oil, gas, and mining, are also adopting digital substations to enhance operational efficiency and reduce energy losses. Transportation infrastructure, including electrified rail systems, is gradually expanding its use of digital substations to support sustainable mobility initiatives. Collectively, these applications underline how digital substations are becoming indispensable across energy, industrial, and infrastructure landscapes.

Utilities remain the leading end-user segment, accounting for the largest share of adoption due to their pivotal role in national grid management and power reliability. Grid operators rely on digital substations for real-time control, automation, and integration of renewable energy resources, which strengthens overall network resilience. The fastest-growing end-user category is the industrial sector, where manufacturing plants, refineries, and mining companies are investing in digital substations to optimize energy consumption, enhance safety, and lower maintenance costs. The transportation sector, particularly rail electrification and smart city projects, is also increasingly deploying digital substations to support efficient infrastructure development. Other contributors include renewable energy developers, who rely on digital substations to balance variable generation and maintain consistent supply. This end-user distribution highlights the growing diversity of demand, reflecting the importance of digital substations across traditional and emerging industries.

North America accounted for the largest market share at 34 percent in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2 percent between 2025 and 2032.

Regional insights indicate varied adoption levels driven by energy demand, infrastructure development, and regulatory priorities. North America continues to dominate due to early adoption of digital technologies and large-scale grid modernization initiatives. Europe remains a strong market with sustainability mandates and advanced utility frameworks driving consistent investments. Asia Pacific is witnessing rapid deployment fueled by industrial expansion and renewable energy integration across China, India, and Japan. South America is gradually advancing with Brazil leading modernization projects, while the Middle East & Africa showcase demand growth in oil, gas, and infrastructure-driven applications. Together, these regions represent a diverse landscape of growth opportunities, underpinned by unique policy environments and technological adoption rates.

Advanced modernization initiatives driving robust adoption

North America holds around 34 percent of the global Digital Substation Market, reflecting its leadership in technological deployment and large-scale infrastructure upgrades. Demand is particularly strong across industries such as utilities, oil and gas, and heavy manufacturing, which rely on high-capacity digital substations for grid reliability. Government support through funding for smart grid initiatives and policies ensuring stricter cybersecurity compliance are strengthening regional adoption. The market is further bolstered by widespread integration of cloud-based monitoring systems, IoT-enabled devices, and predictive analytics. Utilities are adopting digital twin platforms and AI-based diagnostics, advancing operational resilience and performance across critical energy networks.

Regulatory-driven sustainability transforming grid infrastructure

Europe accounts for approximately 28 percent of the global Digital Substation Market, supported by mature energy infrastructure and ambitious climate targets. Key markets such as Germany, the UK, and France are leading adoption, driven by policies supporting renewable integration and carbon neutrality goals. Regulatory bodies have set stringent grid reliability standards, prompting utilities to replace conventional substations with digital solutions. Innovation is also thriving, with widespread adoption of process bus technology, fiber-optic communication, and digital protection systems across high-voltage networks. Regional focus on sustainability and advanced automation places Europe at the forefront of technological transformation in substation modernization.

Industrial expansion and renewable integration fueling adoption

Asia Pacific represents nearly 25 percent of the Digital Substation Market volume in 2024 and is the fastest-growing regional segment globally. China, India, and Japan are the largest consumers, supported by large-scale investments in renewable energy, rapid industrialization, and extensive urban infrastructure projects. Digital substations are increasingly deployed in high-voltage transmission networks, renewable integration hubs, and industrial facilities requiring advanced automation. The region is also a hub of innovation, with local players investing heavily in smart grid research, AI-based asset management, and digital twin applications. This surge in adoption positions Asia Pacific as a critical driver of future market expansion.

Energy modernization and infrastructure upgrades reshaping demand

South America accounted for about 7 percent of the Digital Substation Market in 2024, with Brazil and Argentina leading adoption. Brazil is investing heavily in energy infrastructure upgrades, particularly for renewable energy projects and transmission networks, while Argentina focuses on modernization to improve grid reliability. Government-backed incentives and favorable trade policies are promoting digital transformation within utilities. The demand for digital substations is also rising in industrial sectors, particularly mining and oil, where efficient power distribution is essential. Although adoption is gradual compared to other regions, increasing investments and supportive regulations are positioning South America as a growth-oriented market.

Oil, gas, and construction sectors accelerating digital adoption

The Middle East & Africa contributed about 6 percent to the global Digital Substation Market in 2024, with the UAE, Saudi Arabia, and South Africa emerging as key growth hubs. Demand is largely driven by oil and gas operations, large-scale construction projects, and rapid urbanization. Governments in the region are pushing for energy diversification and modernization of power infrastructure, which has accelerated the deployment of digital substations. Technological advancements, such as smart automation systems and advanced cybersecurity measures, are being integrated into critical projects. Partnerships with global technology providers and evolving regulatory frameworks are further supporting regional market growth.

United States – 22% market share | The United States leads the Digital Substation Market due to extensive smart grid investments, large-scale industrial demand, and robust regulatory frameworks that ensure modernisation.

China – 18% market share | China dominates with strong production capacity, massive renewable energy integration, and accelerated infrastructure development supporting digital substation deployment.

The Digital Substation Market is characterized by a highly competitive environment with more than 30 active global and regional players engaged in innovation, product development, and strategic collaborations. Established multinational corporations dominate with comprehensive portfolios spanning hardware, software, and service solutions, while regional specialists are gaining traction through customized offerings and competitive pricing models. Strategic partnerships between technology providers, utilities, and governments are increasingly shaping the market, with multiple large-scale pilot projects and digitalization programs being launched globally in 2024 and 2025. Mergers and acquisitions have intensified as companies seek to strengthen their presence in high-growth regions such as Asia Pacific and Europe. Innovation trends center around integration of AI-driven monitoring, cybersecurity enhancements, digital twin platforms, and fiber-optic communication systems. Competitors are also investing heavily in research and development, focusing on modular and prefabricated substations that reduce installation time and cost. This dynamic environment is pushing companies to differentiate through advanced technology adoption, service excellence, and sustainable digital grid solutions.

ABB Ltd

Siemens AG

Schneider Electric SE

General Electric Company

Hitachi Energy Ltd

Mitsubishi Electric Corporation

Eaton Corporation plc

Crompton Greaves Consumer Electricals Limited

Toshiba Energy Systems & Solutions Corporation

Larsen & Toubro Limited

The Digital Substation Market is undergoing rapid technological transformation, driven by advancements in automation, intelligent communication protocols, and AI-driven asset management systems. One of the most impactful innovations is the adoption of IEC 61850-based communication, which has enabled seamless interoperability between devices, reduced wiring by up to 80 percent, and improved operational flexibility. The integration of fiber-optic communication networks is replacing copper cabling, delivering faster data transmission speeds and enhanced immunity to electromagnetic interference, a key requirement for high-voltage environments.

Emerging technologies such as digital twin platforms are redefining maintenance strategies by simulating real-world conditions in virtual environments. Utilities deploying digital twin solutions have reported reductions in unplanned outages by over 30 percent and asset lifespan extensions exceeding 20 percent. AI-powered predictive analytics further strengthen performance by identifying early signs of equipment degradation, allowing for optimized scheduling of maintenance. Modular and prefabricated substations are also reshaping the deployment landscape by cutting installation timelines nearly in half, making them especially attractive for time-sensitive infrastructure projects in urban centers and renewable energy parks.

Additionally, cybersecurity technologies are being embedded directly into digital substations to safeguard critical grid infrastructure from evolving cyber threats. Real-time anomaly detection, intrusion prevention, and end-to-end encryption are becoming standard features. Coupled with cloud-enabled platforms and IoT-driven monitoring systems, these technologies are enhancing grid resilience, reducing downtime, and supporting a more sustainable and flexible energy ecosystem.

• In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. The sustainable cable includes 43 percent renewable material in its outer sheath, cutting the carbon footprint by 24 percent compared to traditional fossil-based TPU.

• In April 2024, Hitachi Energy launched its new generation of digital control and protection devices for high-voltage substations, featuring AI-enabled diagnostics that improved fault detection accuracy by 30 percent during pilot testing across European transmission networks.

• In September 2023, Siemens commissioned a fully digitalized 220 kV substation in India, integrating digital relays, optical sensors, and cloud-based monitoring systems, reducing installation time by 35 percent compared to conventional setups.

• In March 2023, ABB unveiled a modular digital substation platform designed for renewable integration projects, which demonstrated a 40 percent reduction in operational downtime through real-time monitoring and predictive maintenance analytics during trial deployments.

The scope of the Digital Substation Market Report encompasses a comprehensive examination of the technologies, applications, and regional developments shaping the industry. It provides insights into segmentation by type, including hardware, software, and services, each of which plays a critical role in ensuring the reliability and modernization of power infrastructure. Application coverage extends across utilities, industrial operations, renewable energy projects, and transportation networks, highlighting the diverse range of industries relying on digital substations for enhanced operational performance.

Geographically, the report covers North America, Europe, Asia Pacific, South America, and the Middle East & Africa, offering a balanced perspective on both established and emerging markets. The analysis includes detailed coverage of key consuming countries such as the United States, China, Germany, India, and Brazil, where digital substation adoption is being driven by policy support, infrastructure expansion, and industrial growth.

The report also explores emerging technologies including digital twins, AI-powered predictive analytics, modular prefabricated substations, and cybersecurity integration. These innovations represent future growth vectors and strategic areas of investment for stakeholders. Additionally, the scope includes an assessment of regulatory frameworks, sustainability initiatives, and energy diversification programs influencing market trends globally. By offering comprehensive insights into both mainstream and niche segments, the report equips decision-makers with the knowledge to identify opportunities, address challenges, and develop competitive strategies in the evolving Digital Substation Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1995.08 Million |

|

Market Revenue in 2032 |

USD 3108.57 Million |

|

CAGR (2025 - 2032) |

5.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB Ltd, Siemens AG, Schneider Electric SE, General Electric Company, Hitachi Energy Ltd, Mitsubishi Electric Corporation, Eaton Corporation plc, Crompton Greaves Consumer Electricals Limited, Toshiba Energy Systems & Solutions Corporation, Larsen & Toubro Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |