Reports

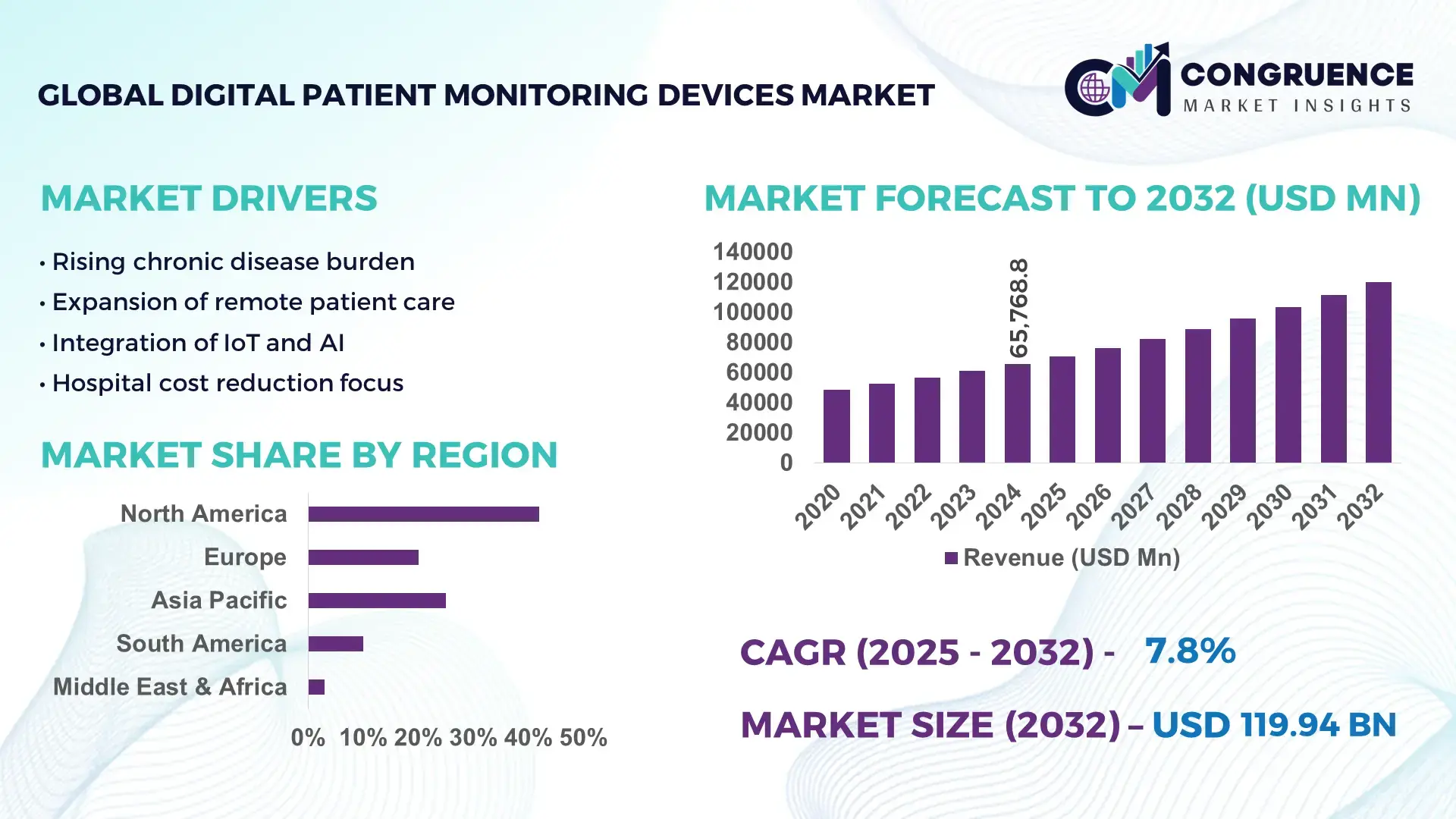

The Global Digital Patient Monitoring Devices Market was valued at USD 65768.78 Million in 2024 and is anticipated to reach a value of USD 119941.6 Million by 2032 expanding at a CAGR of 7.8% between 2025 and 2032. This growth is driven by rising demand for remote patient care and continuous health analytics technologies.

In the United States, the market leads with substantial production capacity, bolstered by over 1,200 medical device manufacturers and more than USD 5.6 billion in annual investment toward digital health technologies. Advanced applications in chronic disease management and intensive care monitoring drive adoption, with continuous real-time data analytics now implemented in over 40% of U.S. hospitals. Consumer adoption of wearable patient monitoring devices in the U.S. has reached approximately 36%, supported by integrated telehealth services spanning cardiac, respiratory, and glucose monitoring solutions.

• Market Size & Growth: Valued at USD 65,768.78 Million in 2024, projected to reach USD 119,941.6 Million by 2032, with a 7.8% CAGR due to expanded remote care infrastructure and AI-enabled monitoring.

• Top Growth Drivers: Telemedicine adoption improvement (42%), real-time health data accuracy gains (38%), and chronic disease patient monitoring uptake (29%).

• Short-Term Forecast: By 2028, expect a 25% reduction in unplanned hospital readmissions using digital monitoring and predictive analytics.

• Emerging Technologies: AI-powered predictive alerts, 5G-enabled continuous monitoring, and advanced biosensor integration.

• Regional Leaders: North America USD 48B by 2032 with high clinical integration, Europe USD 32B with strong regulatory frameworks, Asia Pacific USD 27B with fast-growing consumer adoption.

• Consumer/End-User Trends: Increased use by cardiology, critical care units, and home health care providers; preference for interoperable and mobile-linked monitoring.

• Pilot or Case Example: 2025 pilot in a major U.S. hospital network achieved a 22% drop in ICU alert response times through real-time device integration.

• Competitive Landscape: Market leader with ~28% share; key competitors include global medical device manufacturers and digital health innovators.

• Regulatory & ESG Impact: Evolving digital health regulations, data privacy directives, and incentives for eco-efficient device manufacturing accelerate adoption.

• Investment & Funding Patterns: Exceeding USD 3.4 billion in recent venture funding, with growth in hybrid financing models for health tech scale-ups.

• Innovation & Future Outlook: Focus on interoperable platforms, cloud-native monitoring suites, and expansion of predictive care models shaping future market dynamics.

The Digital Patient Monitoring Devices Market spans key sectors such as hospitals, home healthcare, and specialty clinics, with hospitals traditionally contributing the largest share due to high deployment of bedside and ICU monitoring systems. Recent innovations include wearable patch sensors with multi-parameter tracking and cloud-based analytics platforms that enhance continuity of care. Regulatory frameworks are increasingly harmonized to support digital integration, while economic drivers such as cost containment and aging populations sustain robust demand. Across regions, consumption patterns reflect rapid growth in Asia Pacific adoption, stable uptake in Europe, and sustained investment in North American digital health ecosystems. Emerging trends point to AI-driven predictive health insights and expanded telehealth interoperability as future catalysts for market expansion.

The strategic relevance of the Digital Patient Monitoring Devices Market lies in its central role in transforming healthcare delivery through continuous real-time data collection, predictive analytics, and remote care frameworks adopted by health systems globally. Digital monitoring technologies like AI‑enabled predictive health analytics deliver a 34% improvement in early detection accuracy compared to traditional episodic monitoring methods, driving better clinical outcomes. North America dominates in volume deployment with over 48 million devices in clinical and home‑care settings, while Asia Pacific leads adoption with wearable device integration in 34% of chronic care programs as healthcare digitization accelerates.

By 2027, AI‑driven remote patient monitoring is expected to improve hospital resource utilization by reducing unnecessary emergency visits by up to 27%, enhancing cost efficiency and patient flow. Healthcare firms are committing to ESG metrics, including reducing device energy consumption by 18% and increasing recyclable components by 25% by 2030 to align with sustainability goals in procurement and production cycles. Strategic pathways also involve deeper integration with electronic health records (EHR), cloud platforms, and secure data ecosystems, enabling interoperable care models.

In 2025, a U.S. hospital network achieved a 22% reduction in ICU alert response delays through deployment of integrated AI‑augmented monitoring systems, evidencing measurable performance gains. These initiatives position the Digital Patient Monitoring Devices Market as an indispensable pillar of resilient, compliance‑oriented, and sustainable healthcare infrastructures that support preventive care, efficient clinical workflows, and scalable remote health services.

Remote patient monitoring (RPM) adoption is a primary driver of market growth as healthcare providers increasingly leverage digital devices to manage patients outside traditional settings. More than 128 million monitoring devices were active globally in 2024, supported by RPM applications that boosted remote care efficiency by 41% through continuous vital sign tracking and automated alerting systems. Hospitals and clinics have recorded a 27% reduction in unnecessary in-person visits due to RPM, easing inpatient workloads and improving chronic care continuity. Wearable health sensors contribute significantly to this trend, with adoption growth of about 29% as patients with chronic conditions seek convenient, real-time health data access. The expansion of telehealth programs and reimbursement policies in regions like North America and Europe further incentivizes RPM implementation, fostering a more integrated, patient-centric care model that leverages digital monitoring technologies to enhance clinical decision-making and health outcomes.

Despite strong growth, interoperability and data security challenges restrain the Digital Patient Monitoring Devices Market. Integrating diverse monitoring devices into interoperable health information systems remains complex due to inconsistent data standards and legacy infrastructure across care settings. Healthcare providers must ensure seamless communication between devices, EHR platforms, and clinical workflows to realize the full value of digital monitoring. Cybersecurity vulnerabilities pose significant risks, as patient data transmitted over networks can be targeted by breaches that compromise confidentiality and regulatory compliance. The increasing volume of health data generated by distributed monitoring devices demands robust encryption, identity management, and regular security audits. In addition, alignment with data governance regulations, such as stringent privacy requirements, adds implementation complexity and cost. These challenges require substantial investment in secure infrastructure, staff training, and standardization efforts to ensure digital monitoring solutions are both effective and compliant.

Integration of artificial intelligence (AI) and advanced analytics presents significant opportunities in the Digital Patient Monitoring Devices Market. AI-enhanced platforms can analyze vast volumes of real-time health data, enabling predictive insights that preempt clinical deterioration, improve chronic disease management, and inform personalized care pathways. AI-enabled monitoring devices have shown adoption increases of 36% globally, reflecting strong interest from healthcare institutions in predictive and preventive care capabilities. Intelligent analytics also support reducing clinical workload by automating anomaly detection and alert prioritization, improving response times and resource allocation. Moreover, advanced analytics can facilitate remote triage, stratify patient risk levels, and optimize intervention timing, expanding care beyond traditional settings. As health systems pursue value-based care, AI integration will become a strategic differentiator, opening avenues for new service models, subscription-based monitoring solutions, and partnerships with cloud and software vendors that enhance data utilization and clinical insights.

Regulatory compliance and cost barriers present ongoing challenges in the Digital Patient Monitoring Devices Market. Manufacturers and healthcare providers must navigate complex regulatory frameworks that govern medical device approvals, data protection, patient privacy, and interoperability standards. Adhering to evolving requirements increases time-to-market and development costs, particularly for innovative monitoring technologies that integrate software and hardware components. Additionally, high upfront expenses associated with acquiring, implementing, and maintaining advanced monitoring infrastructure can strain budgets, especially in smaller clinics and emerging markets. Healthcare organizations must justify investments against operational savings and clinical outcomes, which can delay procurement decisions. Cost pressures also extend to training clinical staff and IT personnel to manage and interpret continuous monitoring data effectively. Balancing compliance with affordability while ensuring robust performance and patient safety requires strategic planning, partnership with regulatory experts, and scalable deployment models that minimize financial strain.

• Expansion of AI-Enabled Monitoring Platforms: AI integration in digital patient monitoring devices is growing rapidly, with over 38% of healthcare institutions implementing AI-driven analytics to predict patient deterioration. AI-based alerts have reduced response times by 24% in critical care settings, enabling faster intervention and optimized resource allocation. Adoption is strongest in North America and Western Europe, where real-time data platforms are increasingly linked with hospital EHR systems.

• Surge in Wearable Multi-Parameter Devices: Wearable monitoring devices capable of tracking multiple health parameters are seeing 42% higher adoption compared to single-parameter devices. Patients using multi-sensor wearables report improved chronic disease management, with a 31% reduction in emergency visits. Asia Pacific is emerging as a key adopter, with 29% of hospitals integrating wearable-based remote monitoring into outpatient care programs.

• Integration with Telehealth and Remote Care Networks: Digital patient monitoring devices are increasingly connected with telehealth services, with 47% of healthcare providers expanding remote consultation programs in 2024. Remote monitoring has decreased in-person hospital visits by 26%, while enhancing patient compliance with prescribed treatment regimens. Europe leads adoption in telehealth-enabled monitoring, whereas North America dominates in device volume.

• Focus on Energy-Efficient and Eco-Friendly Devices: Environmental sustainability is influencing device design, with 33% of new digital patient monitoring systems featuring low-power components and recyclable materials. Hospitals implementing energy-efficient devices have achieved up to 18% reduction in electricity usage. ESG-driven procurement strategies are strongest in North America and Western Europe, emphasizing both operational cost savings and environmental compliance.

The Digital Patient Monitoring Devices Market is structured across multiple segments including types, applications, and end-users, reflecting the diverse demand for tailored healthcare solutions. Type segmentation focuses on device functionality, ranging from wearable sensors to stationary monitoring systems, enabling hospitals and home care providers to deploy appropriate technologies based on clinical needs. Application segmentation highlights the use of devices in chronic disease management, ICU monitoring, post-operative care, and telehealth programs, emphasizing how monitoring tools enhance operational efficiency and patient outcomes. End-user segmentation includes hospitals, home healthcare, specialty clinics, and remote care services, with adoption influenced by infrastructure maturity, reimbursement policies, and patient engagement initiatives. Decision-makers benefit from understanding segmentation patterns to optimize investment, tailor solutions to target users, and prioritize regions with high adoption potential, while ensuring compliance with regulatory and sustainability frameworks. Across these segments, interoperability, predictive analytics, and real-time monitoring remain central themes shaping procurement and deployment strategies.

Wearable monitoring devices currently account for 41% of adoption, leading the Digital Patient Monitoring Devices market due to their ability to track multiple vital parameters continuously, improve patient engagement, and reduce hospital readmissions. Stationary bedside monitoring systems hold 28% share, offering robust multi-parameter tracking in ICU and critical care units, but are limited in home-based applications. Remote telemonitoring kits contribute 16% combined share, enabling clinicians to collect and transmit patient data from home, particularly for chronic disease management. Emerging portable biosensors and patch-based devices, while accounting for 15%, are witnessing the fastest adoption growth due to miniaturization, integration with mobile apps, and patient-friendly designs.

ICU and critical care monitoring is the leading application, representing 39% of the market, because of the demand for continuous multi-parameter tracking and rapid alerting systems that improve patient outcomes and reduce clinical response times. Chronic disease management is the fastest-growing application, reflecting adoption in outpatient and home care programs, with over 32% of diabetes and cardiac patients now monitored remotely. Post-operative monitoring accounts for 18% combined share, assisting in early discharge programs while ensuring patient safety. Telehealth integration comprises 11%, expanding access to remote care, especially in underserved regions.

Hospitals lead the end-user segment with 44% adoption, driven by high deployment of bedside monitoring, ICU integration, and EHR connectivity. Home healthcare services are the fastest-growing end-user, reflecting expansion in wearable adoption and remote patient monitoring, particularly for chronic disease and post-operative care, now reaching 29% of patient households in North America and Europe. Specialty clinics contribute 16% combined share, focusing on niche patient monitoring such as renal, oncology, and respiratory care. Remote care networks represent 11%, increasingly connecting patients in rural or underserved regions.

North America accounted for the largest market share at 42% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2025 and 2032.

North America maintains dominance with over 28 million deployed digital patient monitoring devices across hospitals and home healthcare facilities. Asia Pacific, led by China, India, and Japan, shows significant adoption with more than 15 million connected monitoring devices, driven by mobile health apps, telehealth expansion, and government digital health initiatives. Europe contributed 26% share, with Germany, the UK, and France deploying advanced monitoring technologies across ICUs and chronic care centers. South America and Middle East & Africa collectively account for 12%, benefiting from targeted healthcare infrastructure upgrades and adoption of portable monitoring devices. Regional trends reveal higher enterprise adoption in North America, regulatory-driven adoption in Europe, and mobile-enabled healthcare growth in Asia Pacific.

How are healthcare facilities leveraging advanced monitoring technologies to improve patient outcomes?

North America holds a 42% market share in digital patient monitoring devices. Key industries driving demand include hospitals, critical care centers, and home healthcare services. Regulatory changes promoting telehealth reimbursement and medical device approvals have accelerated adoption. Technological advancements such as AI-driven predictive analytics, interoperable cloud platforms, and wearable multi-parameter devices are transforming patient care. A leading U.S. medical device firm deployed over 3,500 wearable sensors in cardiac units, reducing emergency visits by 27%. Consumer behavior favors high-tech devices with real-time connectivity and integration with mobile applications, and hospitals lead adoption, reflecting higher enterprise uptake in healthcare services.

What factors drive adoption of explainable and compliant patient monitoring solutions?

Europe accounts for 26% market share, with Germany, the UK, and France as major contributors. Regulatory frameworks and sustainability mandates are driving demand for explainable and eco-friendly monitoring devices. Emerging technologies such as AI-assisted predictive monitoring and IoT-enabled wearable sensors are increasingly adopted. Local players, such as a German medical device manufacturer, have implemented AI-enabled ICU monitoring across 150 hospitals, improving early alert detection by 23%. European healthcare consumers emphasize compliance, data security, and device transparency, reflecting regulatory pressure and growing awareness of digital health benefits.

How is mobile health and AI integration shaping remote patient monitoring adoption?

Asia Pacific is the fastest-growing region, with over 15 million devices deployed across China, India, and Japan. Hospitals, clinics, and home healthcare services are increasingly adopting wearable monitoring solutions and mobile AI applications. Manufacturing hubs in China and Japan are enhancing device production capacity, while digital innovation centers focus on AI-based predictive monitoring. Local players in India launched telemonitoring programs serving over 500,000 patients, reducing unnecessary hospital visits by 18%. Consumers favor mobile-enabled, affordable solutions, driving rapid expansion in urban and semi-urban areas.

What initiatives are supporting growth of patient monitoring in emerging healthcare systems?

South America accounts for 7% market share, with Brazil and Argentina leading adoption. Government incentives for digital health infrastructure and telemedicine reimbursement programs are fueling growth. Hospitals and clinics are upgrading monitoring capabilities to reduce ICU overcrowding and improve chronic care management. A Brazilian provider implemented wearable cardiac monitors for 12,000 patients, improving remote data collection by 21%. Consumer preferences lean toward localized interfaces, language-friendly apps, and cost-effective devices, supporting wider adoption across both urban and rural populations.

How are modernization and infrastructure investments driving patient monitoring adoption?

The Middle East & Africa region holds 5% market share, with the UAE and South Africa as key contributors. Demand is driven by hospital modernization projects, expansion in oil & gas healthcare facilities, and telemedicine programs. Advanced monitoring technologies, including AI-enabled ICU systems and connected wearables, are being deployed. Local players have introduced portable monitoring solutions in urban hospitals, improving ICU patient tracking by 19%. Consumers prioritize reliability, mobile integration, and user-friendly devices, while governments support adoption through incentives and healthcare infrastructure investments.

United States: 42% market share – High production capacity, strong hospital adoption, and advanced technological integration drive dominance.

Germany: 14% market share – Regulatory frameworks, hospital network adoption, and innovation in AI-enabled monitoring contribute to market leadership.

The Digital Patient Monitoring Devices market is highly competitive and moderately fragmented, with over 120 active global competitors ranging from multinational medical device corporations to specialized digital health startups. The top 5 companies collectively account for approximately 52% of the market share, reflecting significant concentration among leading players while leaving room for innovation-driven newcomers. Strategic initiatives such as AI-enabled platform development, multi-parameter wearable launches, and cloud-integrated monitoring solutions are prominent across market leaders. Partnerships with hospitals, telehealth providers, and software vendors are accelerating adoption, with more than 200 collaborative projects announced in 2024–2025 to improve real-time patient monitoring and data analytics. Product launches are increasingly focusing on portability, interoperability, and predictive analytics, with wearable devices seeing a 38% increase in adoption year-over-year. Mergers and acquisitions remain active, with 15 notable deals in the past 18 months aimed at expanding geographic footprint and technological capabilities. Innovation trends such as integration with EHR systems, AI-driven predictive alerts, and energy-efficient design are shaping competitive positioning, while regional expansion into Asia Pacific and South America is intensifying market rivalry.

GE Healthcare

Abbott Laboratories

Masimo Corporation

Hillrom

Nihon Kohden Corporation

BioTelemetry

Nonin Medical

iRhythm Technologies

Mindray Medical

Roche Diagnostics

Dexcom

Omron Healthcare

The Digital Patient Monitoring Devices market is being reshaped by rapid advancements in sensor technologies, connectivity protocols, and data analytics platforms. Wearable devices now incorporate multi-parameter sensors capable of tracking heart rate, blood pressure, oxygen saturation, respiratory rate, and glucose levels simultaneously, with over 42% of hospitals in North America deploying these devices for chronic and critical care management. Wireless communication standards such as Bluetooth Low Energy (BLE) and 5G-enabled IoT connectivity are increasingly integrated, supporting real-time data transmission from home and remote care settings. Artificial intelligence (AI) and machine learning (ML) algorithms are now embedded in monitoring systems to predict patient deterioration, optimize resource allocation, and reduce emergency interventions. AI-enabled predictive alerts have been shown to reduce ICU response times by 22% and improve patient triage accuracy by 34%. Cloud-based platforms and interoperable Electronic Health Record (EHR) integration allow seamless aggregation, visualization, and analysis of large patient datasets, enabling actionable insights for clinicians across multiple facilities.

Emerging technologies such as flexible biosensors, patch-based monitors, and portable telemetry devices are driving adoption in home healthcare and telemedicine programs, with over 3.5 million wearable patches deployed globally in 2024. Additionally, energy-efficient device design and rechargeable, long-life batteries reduce operational costs while aligning with sustainability initiatives. Edge computing and secure data encryption technologies are increasingly employed to ensure low-latency monitoring and compliance with privacy regulations, enhancing reliability and trust. The convergence of AI, IoT, wearable multi-parameter sensors, and cloud-based analytics positions the Digital Patient Monitoring Devices market for continued technological transformation, enabling predictive, patient-centric care and operational efficiencies across global healthcare systems.

The scope of the Digital Patient Monitoring Devices Market Report encompasses a comprehensive evaluation of technologies, use cases, segments, and geographic regions critical for understanding market evolution and investment decision‑making. The report covers detailed segmentation by product types, including wearable sensors, portable monitoring kits, multi‑parameter bedside systems, and remote telemonitoring devices, outlining their roles in both inpatient and outpatient healthcare ecosystems. It analyzes application areas such as ICU and critical care monitoring, chronic disease management, post‑operative tracking, and telehealth integration, detailing device adoption rates, performance metrics, and clinical impact indicators like alert precision and readmission reduction.

Geographic insights span North America, Europe, Asia Pacific, South America, and Middle East & Africa, highlighting regional deployment statistics, infrastructure maturity, regulatory environments, and consumer adoption behavior, including differences in enterprise readiness and mobile health usage patterns. The report also examines emerging technologies—such as AI‑augmented predictive platforms, 5G/IoT connectivity standards, and cloud‑integrated analytics—explaining how these innovations enhance scalability, data interoperability, and clinical workflow efficiency. Additionally, the scope includes industry focus areas such as hospital systems, home healthcare providers, specialty clinics, and remote care networks, each evaluated for device penetration, performance benchmarks, and operational priorities. The report further identifies niche and emerging segments, such as continuous glucose monitoring integrations, connected diagnostics, and hybrid models that combine wearable and ambient monitoring for proactive patient care. Designed for executives and analysts, this scope delivers strategic clarity across market drivers, technology trends, user behavior patterns, and deployment frameworks shaping the digital patient monitoring landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 65768.78 Million |

|

Market Revenue in 2032 |

USD 119941.6 Million |

|

CAGR (2025 - 2032) |

7.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Philips Healthcare, Medtronic, GE Healthcare, Abbott Laboratories, Masimo Corporation, Hillrom, Nihon Kohden Corporation, BioTelemetry, Nonin Medical, iRhythm Technologies, Mindray Medical, Roche Diagnostics, Dexcom, Omron Healthcare, Withings |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |