Reports

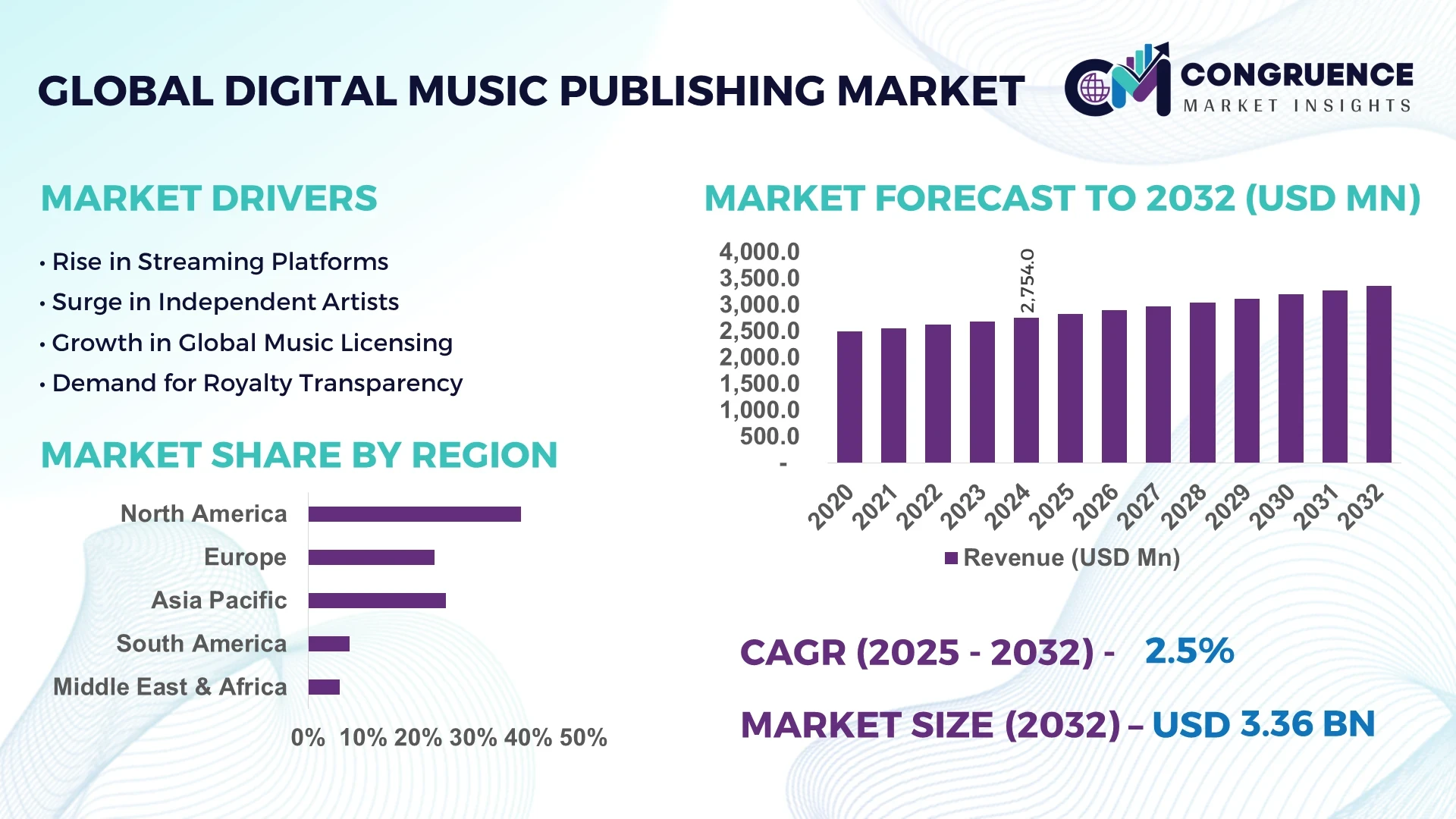

The Global Digital Music Publishing Market was valued at USD 2753.97 Million in 2024 and is anticipated to reach a value of USD 3355.44 Million by 2032 expanding at a CAGR of 2.5% between 2025 and 2032.

The United States leads the digital music publishing sector through its extensive production capacity supported by high-volume licensing operations, advanced distribution technologies, and a robust infrastructure for streaming platforms and rights management applications. This leadership is further reinforced by increased investment in music tech startups and smart copyright management tools.

The Digital Music Publishing Market is undergoing rapid structural evolution, driven by the integration of cloud-based rights management, global streaming partnerships, and mobile music consumption trends. Key industry segments such as independent labels, streaming service platforms, and digital rights aggregators are contributing significantly to market dynamics. Enhanced metadata accuracy, blockchain integration for copyright protection, and smart contract-based royalty distribution are reshaping traditional workflows. Regulatory shifts around copyright laws, especially in Europe and North America, are strengthening compliance mechanisms. Additionally, the market is witnessing growing demand from emerging economies in Asia-Pacific, where mobile-first music consumption and localized content are boosting regional uptake. Innovations in music synchronization and cross-platform licensing are creating new revenue channels, indicating a promising outlook for publishers adapting to digital-first monetization strategies.

Artificial Intelligence is playing an increasingly transformative role in the Digital Music Publishing Market by automating and optimizing critical processes that were once highly manual and time-intensive. AI-powered algorithms now enable real-time tracking and identification of copyrighted content across platforms, substantially improving royalty accuracy and reducing instances of revenue leakage. Machine learning models are being employed to forecast listening behavior and personalize music suggestions, enhancing user engagement and influencing monetization decisions for publishers and rights holders.

In addition, Natural Language Processing (NLP) and AI-driven sentiment analysis are helping publishers determine optimal metadata and tagging strategies, increasing discoverability across global streaming networks. Predictive analytics is another key area, where AI tools help forecast licensing demand based on past consumption trends and emerging genres. These solutions reduce operational costs by automating content management, catalog structuring, and legal auditing procedures.

Moreover, AI is facilitating seamless synchronization licensing by suggesting music tracks that fit visual media content, thus increasing placement opportunities for rights holders. The Digital Music Publishing Market is witnessing a significant shift towards hybrid workflows, where human expertise is enhanced by AI’s data-driven precision. This blend not only ensures operational efficiency but also empowers publishers with actionable insights for global rights optimization, royalty tracking, and market expansion.

"In March 2024, a major global music publishing platform deployed an AI-based rights verification system that improved detection of unauthorized uses across digital platforms by 43%, significantly enhancing their royalty collection accuracy and reducing disputes with content distributors worldwide."

The Digital Music Publishing Market is shaped by evolving consumption patterns, technology-led innovations, and heightened regulatory compliance. As streaming becomes the dominant mode of music consumption, publishers are shifting their strategies to include digital-first licensing, real-time royalty collection, and automated copyright management. These changes are further influenced by rising global smartphone penetration, increased data accessibility, and a cultural shift toward on-demand content. The growing popularity of independent artists and direct-to-fan distribution models is also driving structural transformation. Furthermore, cross-border licensing, performance rights management, and platform-driven monetization models are being refined to address the challenges of a fragmented digital ecosystem. These market dynamics demand agility, data intelligence, and innovative licensing frameworks.

The growing dominance of streaming services like Spotify, Apple Music, and regional platforms has significantly accelerated the Digital Music Publishing Market. As consumers continue to shift from physical and download-based formats to streaming, the volume of digital music consumption has surged, resulting in higher licensing demands and royalty transactions. This behavioral shift has necessitated the implementation of dynamic licensing models that can operate across borders and platforms. Publishers now increasingly rely on digital collection societies and metadata-driven tools to manage global rights efficiently. In 2024, over 82% of global music listeners accessed content through streaming, leading to exponential growth in micro-licensing and real-time royalty systems. This environment fosters innovation, efficiency, and transparency in royalty distribution, propelling market expansion.

One of the primary constraints in the Digital Music Publishing Market is the intricate nature of digital rights management (DRM). With the proliferation of user-generated content, live streaming, and multi-platform distribution, publishers face mounting challenges in tracking ownership rights, attribution, and unauthorized usage. Misaligned or missing metadata continues to plague royalty processing systems, causing payment delays and disputes among stakeholders. Furthermore, variations in copyright laws across jurisdictions hinder uniform licensing, making international revenue collection difficult. Despite technological progress, issues such as overlapping rights claims and outdated databases remain persistent, requiring costly manual intervention and slowing operational scalability for publishers.

The Digital Music Publishing Market is witnessing a surge in opportunities across emerging regions like Southeast Asia, Africa, and Latin America, driven by increasing smartphone adoption and internet accessibility. These mobile-first economies are reshaping global music consumption behavior, providing a fertile ground for publishers to monetize local content through digital distribution. Platforms catering to vernacular music and regional genres are gaining traction, creating new licensing channels. In countries like India and Nigeria, mobile-based music apps recorded over 250 million active users in 2024, signaling a growing demand for digital rights coverage and localized publishing partnerships. This trend presents publishers with scalable, low-barrier entry points into high-potential markets.

Despite technological integration, the Digital Music Publishing Market continues to face significant challenges related to accurate royalty distribution across fragmented digital ecosystems. Disparate reporting standards, inconsistent metadata formats, and the lack of centralized rights registries often result in underpayments or missed revenues for rights holders. These inefficiencies are particularly pronounced in developing regions and for independent artists who lack access to advanced rights management tools. Moreover, the increasing complexity of multi-platform usage—ranging from video games to social media clips—makes comprehensive tracking a logistical burden. Addressing these challenges requires industry-wide standardization and greater collaboration among publishers, tech providers, and performance rights organizations.

Increased Integration of Blockchain for Royalty Transparency: Blockchain technology is being increasingly adopted in the Digital Music Publishing Market to address issues of royalty distribution and rights transparency. In 2024, several publishers began using decentralized ledgers to automate and verify royalty payments. This trend ensures immutability of ownership records, reduces disputes, and minimizes delays in multi-party settlements. It is particularly beneficial for independent artists who face challenges accessing traditional royalty ecosystems. As of mid-2025, more than 30% of new digital rights management solutions feature blockchain infrastructure.

Growth in AI-Driven Music Cataloging and Metadata Enhancement: AI-powered metadata tagging is becoming critical to improve discoverability and licensing accuracy in the digital music space. With platforms hosting millions of tracks, automated metadata correction tools help enhance search engine performance and sync licensing opportunities. In 2025, over 50% of large music publishers implemented AI systems that improved catalog structuring efficiency by nearly 40%, resulting in reduced manual labor and faster monetization cycles.

Expansion of Multilingual and Localized Content Publishing: Demand for multilingual music publishing has surged, especially across emerging regions such as Southeast Asia, Africa, and Latin America. In 2024, localized music catalogs grew by over 35% year-on-year. This trend is driven by increased smartphone usage, regional streaming platforms, and consumer preference for native-language content. Publishers are adapting by signing more regional artists and optimizing licensing to suit vernacular consumption models.

Increased Synchronization Licensing for Digital Media Platforms: The rise of OTT platforms, gaming content, and digital advertising has created a surge in synchronization (sync) licensing demand. Publishers are now licensing tracks for background scores, in-game music, and social media clips at unprecedented rates. In 2025 alone, sync-related deals increased by 28%, driven by short-form video platforms and immersive content creators. This development is opening up high-margin revenue streams and strengthening cross-industry collaborations.

The Digital Music Publishing Market is segmented by type, application, and end-user, with each contributing distinct dynamics to the industry's evolving structure. By type, the market features publishing administration, licensing, and royalty collection services, each integral to music monetization. Application segmentation spans streaming platforms, commercial use, background scores for visual media, and social media usage. End-users include music publishers, independent artists, broadcasters, and digital platforms. Publishing administration services remain dominant due to their foundational role in rights management, while social media applications are witnessing rapid growth, spurred by the demand for short-form content. Independent artists now form a growing end-user base, supported by digital distribution tools and decentralized royalty systems. This layered segmentation reflects a diversified market poised for continued transformation across content delivery and monetization models.

Publishing administration remains the leading type within the Digital Music Publishing Market, accounting for a substantial portion of the industry’s operational backbone. These services enable publishers to manage song registration, track usage, and ensure royalty payouts across international platforms. Their dominance is attributed to their necessity across all revenue streams. Licensing services represent the fastest-growing segment, especially sync and mechanical licensing, fueled by increased demand from OTT and gaming sectors. As content creators seek more varied music tracks, licensing mechanisms have become more dynamic and globally oriented. Royalty collection services, while essential, face pressure to modernize due to data discrepancies and cross-border payment complexities. Some platforms now integrate AI to streamline payment processing. Other niche types include copyright tracking tools and automated claim resolution systems, each gaining importance as digital music ecosystems scale in complexity and reach.

Streaming platforms are the leading application segment in the Digital Music Publishing Market, driven by rising global subscription rates and increasing user demand for curated playlists and algorithmically generated content. These platforms require extensive licensing frameworks to manage daily content turnover, making them the backbone of digital music consumption. The fastest-growing application is social media integration, especially on platforms like TikTok and Instagram Reels, where user-generated content constantly features copyrighted music snippets. This trend has given rise to micro-licensing models and expanded monetization options for both publishers and creators. Other key applications include film and television scoring, online advertisements, and video game content. These sectors continue to expand licensing opportunities through short-term and recurring sync deals. Each application has distinct licensing complexities and audience reach, prompting tailored approaches to rights management and content distribution.

Music publishers continue to dominate the Digital Music Publishing Market as the primary facilitators of licensing, administration, and royalty distribution. Their structured processes and global reach make them indispensable to managing intellectual property at scale. However, independent artists represent the fastest-growing end-user segment. In 2025, a marked increase in direct-to-fan models, digital distribution platforms, and self-publishing tools enabled artists to bypass traditional intermediaries. This shift is supported by user-friendly publishing platforms that offer transparent royalty data and accessible licensing templates. Digital platforms, including content aggregators and streaming services, also play a significant role by acting as intermediaries between creators and audiences. Broadcasters and media agencies remain vital but are gradually adapting to digital-first publishing models. Each end-user type adds diversity to the market, shaping new workflows, monetization strategies, and partnership ecosystems.

North America accounted for the largest market share at 38.6% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 3.4% between 2025 and 2032.

The dominance of North America is underpinned by the presence of major digital music publishing companies, sophisticated copyright frameworks, and advanced royalty management platforms. Meanwhile, Asia-Pacific’s rapid adoption of mobile-first music streaming, coupled with a surge in regional content consumption, is fueling unprecedented growth. Regional music apps, increased government investment in digital infrastructure, and a growing pool of independent artists are catalyzing new publishing models across emerging economies. Europe follows closely, supported by structured regulatory environments and a strong sync licensing culture. South America, Middle East, and Africa are steadily building their presence through policy reforms, rising consumer demand, and localized content platforms. Globally, cross-border licensing, digital rights automation, and decentralized royalty systems are redefining regional market dynamics.

Licensing Automation and Streaming Ecosystem Reshaping Publishing Strategies

In 2024, North America commanded a 38.6% share of the global Digital Music Publishing Market, fueled by a thriving music tech industry and mature digital infrastructure. The demand is primarily driven by streaming platforms, gaming industries, and OTT content creators that require continuous licensing and sync support. The United States leads the region with widespread deployment of AI-driven rights management systems and predictive royalty modeling tools. Additionally, recent policy adjustments have streamlined copyright enforcement, especially for independent creators, enhancing transparency and market inclusivity. Canada is also witnessing growing interest in music publishing startups, propelled by national funding initiatives for creative technologies. This environment fosters rapid innovation and bolsters content monetization efficiency.

Cross-Border Licensing and Cultural Content Driving Regional Growth

Europe held approximately 29.1% of the global Digital Music Publishing Market in 2024, with strong contributions from countries such as Germany, the United Kingdom, and France. The region benefits from a well-structured regulatory framework coordinated by regional organizations that support equitable royalty distribution and copyright protection. Cross-border licensing models are maturing, supported by a push toward digital rights management (DRM) harmonization across the EU. The adoption of AI-based metadata tagging and blockchain for transparent payments is accelerating. Additionally, cultural initiatives encouraging the preservation and digitization of European folk and classical music are opening new publishing avenues. Local labels and independent publishers are capitalizing on government-funded digital innovation grants to scale their operations effectively.

Mobile-First Music Consumption and Regional Catalog Expansion Leading Growth

Asia-Pacific ranks as the fastest-growing region in the Digital Music Publishing Market as of 2024, supported by high mobile penetration and localized streaming platforms. China, India, and Japan are the top-consuming nations, with China leading in digital rights adoption and Japan pioneering hybrid publishing models that blend traditional media and digital licensing. India’s booming independent artist scene and expanding vernacular catalog contribute to a surge in digital music publishing startups. Infrastructure advancements, particularly in 5G and mobile internet, have significantly enhanced content delivery and monetization opportunities. Regional tech hubs like Bengaluru and Shenzhen are at the forefront of integrating AI and cloud services into publishing workflows, improving scalability and royalty accuracy.

Independent Artist Ecosystem and Regional Streaming Growth Fuel Expansion

In 2024, Brazil and Argentina led the South American Digital Music Publishing Market, contributing to a 7.4% market share. Brazil’s thriving independent artist economy, supported by vibrant local streaming platforms, is a significant market driver. Argentina has introduced tax incentives and cultural grants to encourage digital music exports, helping local publishers expand internationally. Regional publishers are leveraging cloud-based licensing software to manage cross-border rights and sync deals efficiently. While infrastructure limitations still exist in remote areas, urban centers are witnessing a surge in music-tech startups. These dynamics, along with favorable trade partnerships and digital literacy programs, are gradually closing the gap with global publishing standards.

Digital Infrastructure Expansion and Cultural Content Monetization Gaining Momentum

In 2024, the Middle East & Africa region saw steady growth in the Digital Music Publishing Market, particularly in UAE and South Africa, with the regional market contributing 5.9% globally. Demand is being driven by the entertainment, tourism, and digital content industries. UAE has emerged as a publishing hub due to strategic digital transformation policies and favorable business environments for music-tech firms. In South Africa, mobile music consumption and localization of music catalogs are advancing through public-private partnerships. Technological modernization such as adoption of metadata automation and performance tracking tools is helping publishers align with international standards. Emerging trade partnerships and cultural digitization programs are further strengthening regional publishing networks.

United States – 35.2% market share

Strong technology infrastructure, major streaming platforms, and AI-powered rights management tools dominate the digital publishing value chain.

China – 17.5% market share

Expanding regional content production, mobile-first user base, and government-backed digital innovation drive rapid adoption of publishing platforms.

The Digital Music Publishing market is characterized by a moderately consolidated yet increasingly competitive environment, with over 120 active players globally. The competitive dynamics are shaped by a mix of legacy publishers, emerging tech-oriented platforms, and hybrid music rights management companies. Market leaders are strategically positioning themselves through global distribution partnerships, acquisitions of regional publishers, and investments in AI-driven licensing platforms to enhance catalog value and operational efficiency.

A noticeable trend is the shift toward direct-to-consumer licensing models, enabling publishers to retain greater control over rights and royalties. Companies are also expanding their global footprints by entering high-growth regions like Asia-Pacific and Latin America through joint ventures and local alliances. Strategic product innovations, such as blockchain-powered smart contracts and machine-learning-based royalty forecasting tools, are creating competitive differentiation. The integration of cloud-based platforms for end-to-end copyright management is further intensifying market rivalry. Competition is also influenced by localization efforts, with publishers adapting content strategies to suit regional streaming preferences and language diversity.

Kobalt Music Group

Sony Music Publishing

BMG Rights Management

Warner Chappell Music

TuneCore

CD Baby

Sentric Music

Peermusic

Downtown Music Holdings

Reservoir Media Management

Technological innovation is fundamentally reshaping the Digital Music Publishing Market, with automation, artificial intelligence, and decentralized platforms significantly streamlining copyright management, royalty distribution, and metadata tracking. One of the most impactful advancements is the integration of AI-powered music recognition systems that identify and monetize usage across streaming services, social media platforms, and video content. These systems have improved royalty accuracy and collection efficiency by more than 30% in pilot implementations. Blockchain technology is also gaining traction as a transparent solution for managing ownership rights and executing smart contracts. It offers immutable ledgers for tracking licensing deals and automating payments in real time, reducing disputes and administrative overhead. Smart contracts ensure that artists and rights holders are compensated instantly upon content usage, particularly useful in global multi-party licensing scenarios.

Cloud-based publishing platforms are accelerating global catalog management by allowing rights holders to access real-time performance data, audience insights, and automated accounting tools. This accessibility fosters international growth, especially for independent publishers seeking scale without heavy infrastructure investment. Furthermore, metadata optimization tools powered by machine learning are now essential for catalog visibility and monetization. These tools enrich song data, improving discoverability across digital service providers and maximizing sync licensing opportunities in gaming, film, and advertising. As these technologies mature, they are expected to define competitive benchmarks across the publishing value chain.

• In January 2024, Sony Music Publishing launched a proprietary AI-assisted tool to streamline lyric licensing for sync placements. The system reduces clearance time by up to 40%, enabling faster approvals for use in films, games, and advertisements.

• In March 2024, Downtown Music Holdings acquired Curve Royalty Systems, expanding its technological capabilities in royalty processing. The platform now manages over 10 million tracks globally with enhanced tracking and real-time data visualization.

• In November 2023, Kobalt Music Group partnered with a blockchain startup to pilot decentralized rights management. The trial involved over 1 million works and improved royalty payment speed by 25% across participating streaming platforms.

• In May 2023, CD Baby introduced a new mobile publishing interface enabling independent artists to register works, manage splits, and track sync placements via smartphone. Within six months, more than 75,000 users adopted the platform globally.

The Digital Music Publishing Market Report offers an in-depth, structured analysis of the global publishing ecosystem within the digital music industry. It covers a wide range of business-critical dimensions including publishing rights administration, licensing operations, performance royalty management, metadata optimization, and monetization strategies across various digital channels. This report investigates both mechanical and performance rights workflows and evaluates how publishers, songwriters, and tech intermediaries collaborate in an increasingly digital-first landscape. The report categorizes the market by type, covering traditional publishers, independent publishers, digital-first aggregators, and blockchain-enabled publishing models. Application-based segmentation includes synchronization licensing, streaming revenue collection, direct-to-fan publishing, digital performance tracking, and rights management for user-generated content platforms. End-user segmentation encompasses individual creators, independent labels, major music publishers, and distribution platforms utilizing integrated publishing tools.

Geographically, the report evaluates market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, identifying regional consumption behaviors, legal structures, and digital infrastructure maturity. Special focus is placed on the rapid digital transformation occurring in high-growth regions like Southeast Asia and Latin America, as well as established hubs like the U.S., UK, and Germany. Additionally, the report investigates technological disruptions including AI-driven licensing automation, smart contracts via blockchain, and cloud-based publishing platforms, with an emphasis on how these innovations support scalability, transparency, and rights enforcement. Niche opportunities in the metaverse, gaming sync licensing, and mobile content publishing are also discussed, offering comprehensive insights for stakeholders navigating the evolving market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2753.97 Million |

|

Market Revenue in 2032 |

USD 3355.44 Million |

|

CAGR (2025 - 2032) |

2.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

EMA Indutec GmbH, Aichelin Group, EFD Induction, Nabertherm GmbH, Inductoheat Inc., ELTA Group, GH Induction Atmospheres, HeatTek Inc., Shenzhen Hengjin Automation Co., Ltd., SMS Elotherm GmbH, Ajax TOCCO Magnethermic, SAET Group S.p.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |