Reports

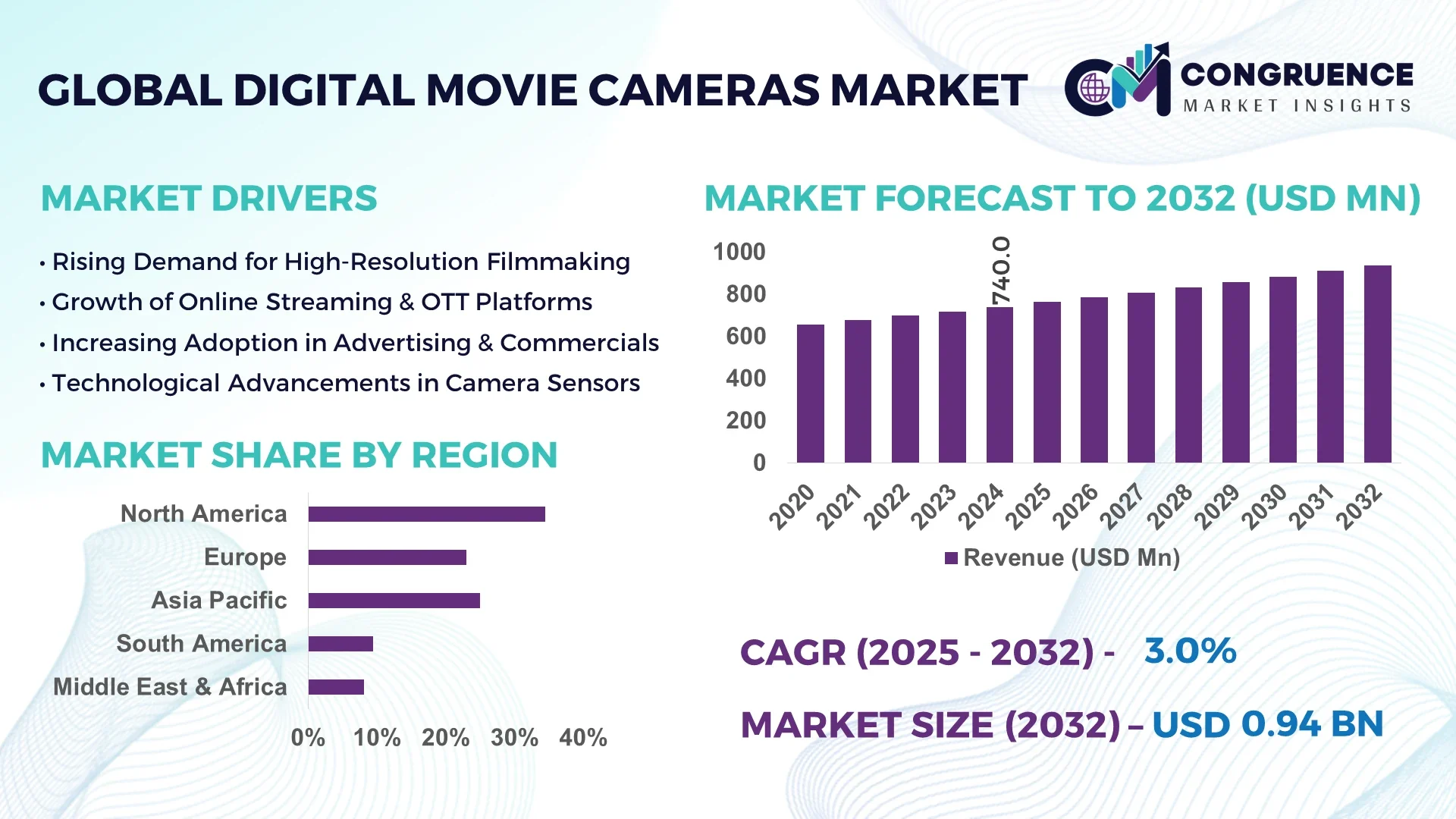

The Global Digital Movie Cameras Market was valued at USD 740.0 Million in 2024 and is anticipated to reach a value of USD 937.4 Million by 2032 expanding at a CAGR of 3.0% between 2025 and 2032.

In the United States, production facilities for cinema-grade digital movie cameras are equipped with state-of-the-art sensor fabrication lines and high-throughput assembly units, supported by over USD 500 million in annual R&D funding and consistent deployment in high‑budget film and broadcast projects across Hollywood studios and sports broadcasting networks, reflecting advanced technological readiness.

The Digital Movie Cameras Market spans professional film production, live broadcasting, independent media studios, and high‑end commercial imaging. Key sectors include feature film, television production, corporate video, and streaming content, with 4K resolution systems dominating device shipments. Recent innovations—such as integrated AI-based autofocus, onboard RAW encoding, and modular 8K-capable bodies—have reduced post-production workflows and enhanced field adaptability. Regulatory drivers include import tariff reductions for filmmaking gear in emerging economies and sustainability mandates for reducing electronic waste. Regional consumption patterns indicate strong demand across North America and Asia-Pacific, with rising content creation infrastructure and streaming platform penetration fueling equipment procurement. Future trends include edge-ML enabled camera modules, cloud-based camera control platforms, and increased adoption of mirrorless cinema systems among independent creators. Decision-makers are advised to prioritize partnerships with manufacturers offering value-added software and modular hardware upgrades to align with evolving production workflows.

Artificial intelligence is redefining the Digital Movie Cameras Market by elevating operational efficiency, reducing post-production workload, and enabling automated imaging workflows. AI-driven autofocus and subject tracking reduce manual setup and increase output speed, improving shooting accuracy by campaign-grade teams by over 30% in dynamic production environments. Enhanced scene recognition and auto-exposure algorithms allow cameras to adapt lighting and depth settings in real time, minimizing retakes and optimizing resource allocation. Embedded neural processing units (NPUs) now enable onboard noise reduction, HDR mapping, and tone curve adjustment in-camera, reducing the need for external image processing.

In live broadcasting and independent filmmaking, cameras utilizing in-camera AI metadata tagging streamline asset management by auto‑labeling takes based on detected scene elements—saving dozens of hours during content sorting. Start-up camera models with integrated computer-vision capabilities support automatic frame stabilization and match-frame color grading on the fly, reducing technician involvement. These AI-powered capabilities are reshaping deliveries to clients such as streamers and documentary filmmakers, enabling faster turnaround and lower crew needs. Hardware vendors in the Digital Movie Cameras Market are increasingly embedding machine learning inference chips, contributing to enhanced field performance, lower latency capture, and tighter integration with AI-based editing platforms. The adoption of AI across capture-to-edit pipelines is offering differentiators for camera brands and service providers alike.

“In July 2024, Blackmagic Design unveiled an internal AI engine in its latest cinema camera model, achieving 95% accuracy in autofocus tracking across handheld shot sets and reducing required manual adjustment time by 40%.”

The Digital Movie Cameras Market is shaped by rapid technological advancement, evolving content formats, and shifting consumer expectations. Resolution upgrades from 4K to 8K and beyond are driving capital equipment turnover within studios and broadcasters, while the rise of OTT and streaming platforms is intensifying demand for high frame rate and dynamic range capture. Independent content creators increasingly opt for mirrorless cinema cameras due to their portability and image quality, reshaping supply chains and sales channels. At the same time, manufacturers continuously integrate AI-based imaging and modular hardware customization to stay competitive. Global sports broadcasts, virtual production studios, and immersive media applications exert pressure on real-time processing capabilities. Geographic growth patterns show strong equipment uptake in North America and Europe, with emerging markets in Asia and Latin America rapidly scaling production budgets. The market dynamic reflects high differentiation among players based on software-hardware symbiosis, production efficiency, and ecosystem compatibility.

The Digital Movie Cameras Market is driven by the surging demand for cinematic quality in streaming, branded content, and live broadcast across platforms. Professional creators increasingly require 4K and higher resolution capture with high dynamic range, pushing studios and broadcasters to upgrade camera systems. Independent filmmakers and digital agencies also invest in modular camera bodies and interchangeable lens mounts to support varied production needs. The requirement for seamless remote production workflows and multi-camera real‑time control systems has further escalated adoption of cinema‑grade cameras. As global brands lean into immersive storytelling and live event coverage, demand for robust sensor performance, low‑light capabilities, and precision optics is heightening, shaping procurement decisions in this market.

Despite growing demand, the Digital Movie Cameras Market faces significant restraints due to the high capital costs of professional cinema cameras and rapid obsolescence. High-resolution sensor platforms and modular hardware upgrades mean new device models supplant prior lines regularly, often within 12‑18 months. This frequent turnover places strain on rental houses and production companies, which must budget for equipment refresh cycles. In addition, costs associated with proprietary lens ecosystems and accessory platforms limit flexibility. Smaller studios or independent creators may opt for lower‑cost alternatives or smartphone-based video tools. Maintenance expenses for high‑end systems, including image sensor calibration and firmware upgrades, add operational complexity, restraining uptake in cost‑sensitive segments.

The expanding creator economy and rise of streaming-first content models present an opportunity for the Digital Movie Cameras Market. Independent studios and digital-first platforms increasingly demand cinema-capable cameras for branded content, documentaries, and episodic series. Lower-cost mirror‑less cinema camera models enable production teams to achieve professional image quality with reduced crew size. Collaboration opportunities exist between camera manufacturers and software platforms to offer bundled AI‑powered editing workflows and cloud-based asset management. In sports, event, and corporate live content creation, remote-controlled cinema cameras and cloud-enabled capture systems are unlocking new use cases. Increased accessibility and flexible financing options are enabling smaller studios and creators to participate in professional-grade production, expanding total addressable demand.

A key challenge in the Digital Movie Cameras Market is the growing gap between advanced camera capabilities and available skilled operators. High‑end cinema cameras now incorporate complex features, such as embedded AI-NPU processing, dynamic range profiling, and frame-rate switching, requiring trained professionals for optimal use. Emerging regions and independent filmmakers may lack access to certified technicians, limiting full feature utilization. As camera firmware evolves rapidly, frequent retraining becomes necessary. Additionally, software updates and interoperability with editing platforms present integration challenges. This technical skills gap can slow deployment and deter adoption, particularly in decentralized production workflows.

Surge in Mirrorless Cinema Camera Adoption: Demand for mirrorless cinema cameras with interchangeable lens systems is rising sharply, with over 35% of new professional device shipments in 2024 attributed to 4K mirrorless models offering compact modular bodies and high frame rates enhancing on-location flexibility.

Onboard AI Metadata Tagging and Scene Recognition: More than ten camera models released in 2024 integrated AI-powered scene tagging that auto-labels shots based on detected elements—reducing editorial sorting time by up to 25% and improving post‑production workflow efficiency.

Transition to Modular 8K-Compatible Hardware Platforms: Several camera lines introduced in 2024 offer swappable sensor modules supporting 8K resolution upgrades, allowing studios to extend hardware lifecycles and support evolving production standards without purchasing entirely new bodies.

Rise in Cloud‑Based Camera Control Platforms: New firmware and hardware integrations launched in 2024 enable cloud-based remote camera management, allowing production teams to control multi‑camera rigs from distributed locations, increasing operational flexibility in live and virtual production environments.

The Digital Movie Cameras Market is segmented across three primary categories: type, application, and end-user. Each segment exhibits distinct consumption behaviors and growth trajectories based on technological integration, usage patterns, and evolving production demands. In the type segment, modular and handheld cameras show divergent adoption patterns based on budget and use-case requirements. Within applications, film and television production continue to dominate, while digital streaming and social content creation are expanding rapidly due to shifting content consumption. From an end-user perspective, professional studios remain dominant, but freelance creators and small production houses represent the fastest-expanding group, fueled by access to affordable, high-specification equipment. These segmentation insights reflect the increasing fragmentation and specialization of demand in global visual media ecosystems and are critical for stakeholders aligning product strategy and marketing outreach with evolving production trends.

In the Digital Movie Cameras Market, key product types include handheld digital cameras, shoulder-mount cameras, cinema-grade cameras, modular camera systems, and action/sports cameras. Among these, cinema-grade digital movie cameras are the leading category, widely adopted by professional studios and broadcasters due to their superior image quality, dynamic range, and compatibility with interchangeable lens systems. These cameras offer integrated professional codecs and color science engines suited for high-end productions.

Modular digital camera systems represent the fastest-growing segment. Their ability to support customizable configurations—including detachable sensors, processors, and storage units—caters to evolving technical needs across both film and digital media workflows. These systems also enable seamless integration with drones, robotic rigs, and virtual production platforms, enhancing versatility in dynamic environments.

Handheld and shoulder-mount cameras continue to serve documentary and on-the-go shooting needs, particularly for news, events, and small-scale productions. Action/sports digital cameras, though niche, contribute to immersive content generation in sports broadcasting and adventure filmmaking, often integrated with gyroscopic stabilization and waterproof features.

The Digital Movie Cameras Market serves multiple application areas, including feature film production, television and broadcasting, streaming content creation, documentary filmmaking, advertising and commercial shoots, and sports/event coverage. Feature film and television production form the core application segment, driven by sustained demand for high-resolution and high dynamic range recording required in cinematic storytelling and episodic content. These use-cases demand robust sensor technologies and deep post-production flexibility.

The fastest-growing application is streaming content creation, driven by the surge in OTT platforms and independent content studios. As digital-first media strategies expand, demand for professional-grade yet affordable digital cameras optimized for multi-camera and virtual production environments is accelerating. This segment is supported by cloud-based post-production ecosystems that pair well with AI-enhanced camera systems.

Documentary filmmaking and advertising agencies rely on lightweight, portable camera setups with advanced autofocus and real-time scene recognition. Sports and event coverage, while specialized, sees increasing investment in high-speed frame capture and integrated wireless controls for remote operation during live broadcasts and competitive events.

In terms of end-user segments, the Digital Movie Cameras Market caters to professional film studios, television networks, independent filmmakers, advertising agencies, corporate production teams, streaming content producers, and educational institutions. Professional film studios and broadcasters remain the largest end-users, investing in high-spec cameras to meet theatrical and large-scale distribution standards. These users require systems that support RAW formats, global shutter sensors, and high-capacity data storage to handle intensive production workflows.

The fastest-growing end-user segment is independent content creators and small production houses. Their growth is fueled by increased access to affordable, modular digital movie cameras with near-cinema capabilities. Paired with AI-driven editing tools and online monetization platforms, these users are increasingly producing competitive content with smaller teams and leaner budgets.

Corporate production teams and educational institutions also play key roles in shaping demand. Corporates are using digital movie cameras for internal branding, training, and live streaming, while universities and film schools integrate advanced camera systems into curricula to prepare students for evolving media careers.

North America accounted for the largest market share at 34.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

North America's dominance is driven by widespread adoption of digital cinematography in film studios and streaming platforms. In contrast, Asia-Pacific’s rapid growth is fueled by rising investments in entertainment infrastructure, expanding digital media consumption, and growing availability of cost-effective high-spec cameras. Both regions are influenced by technological innovation and evolving regulatory environments that support next-gen filming technologies and digital production workflows.

The North America Digital Movie Cameras Market captured a market share of 34.5% in 2024, with the U.S. being the largest contributor due to its dominance in global entertainment production. Demand is largely driven by film studios, OTT streaming platforms, advertising agencies, and sports broadcasting firms. Regulatory bodies have introduced digital infrastructure grants to support local film industries and promote innovation in production technologies. Advanced cinema-grade camera systems with AI-enhanced scene analysis, real-time rendering, and wireless connectivity are widely adopted across high-budget productions. Moreover, North American buyers are increasingly integrating digital movie cameras into virtual production studios equipped with LED volumes and XR environments.

The Europe Digital Movie Cameras Market held a market share of 27.1% in 2024, led by Germany, the UK, and France. These countries are investing heavily in digital transformation of media production, with national broadcasting agencies and independent studios demanding high-resolution and eco-efficient camera systems. Regulatory initiatives, such as the EU Green Deal, are also pushing manufacturers to produce energy-efficient and sustainable imaging systems. European buyers are early adopters of emerging technologies such as virtual cinematography, volumetric video capture, and AI-based content editing tools. These trends are reinforcing the region’s focus on sustainable yet cutting-edge media production.

The Asia-Pacific Digital Movie Cameras Market ranks highest in growth momentum, with countries like China, India, and Japan leading regional consumption. In 2024, this region represented 22.8% of global market volume, and demand is surging due to widespread expansion of local film studios and the explosive rise in regional OTT platforms. Advanced infrastructure in Japan and China supports high-capacity manufacturing of sensors and camera hardware, while India is emerging as a digital content powerhouse due to its expanding creator economy. Innovation hubs in South Korea and Singapore are also pushing the boundaries with AI-based production and virtual filming technologies.

The South America Digital Movie Cameras Market is experiencing steady growth, with Brazil and Argentina at the forefront. Brazil holds the largest share within the region due to its active telenovela and advertising industries. Market growth is further supported by regional tax incentives and cultural investment programs that subsidize audiovisual production. Infrastructure upgrades in urban centers and increased access to 4K and 8K content creation tools are encouraging small studios and content creators to adopt professional-grade digital movie cameras. The rise in independent cinema, combined with local government incentives, continues to elevate demand for mid-tier and modular camera systems.

The Middle East & Africa Digital Movie Cameras Market is seeing increasing demand from countries like UAE and South Africa, which are positioning themselves as regional filming hubs. Regional demand is bolstered by sectors such as tourism, oil and gas documentation, and government-funded promotional content. Dubai and Abu Dhabi have launched media free zones and provide funding incentives for digital content production. Technology modernization, especially in broadcasting and online streaming, is accelerating the adoption of digital movie cameras with AI-based capabilities, including automatic color grading and real-time metadata tagging. Trade agreements with global camera manufacturers have also enhanced access to high-end systems.

United States – 28.7% Market Share

Strong end-user demand from Hollywood studios and streaming platforms drives consistent investment in cutting-edge digital movie camera systems.

China – 18.3% Market Share

High production capacity and rapid growth in domestic film and OTT sectors fuel demand for advanced and affordable digital movie camera technologies.

The Digital Movie Cameras Market is characterized by a dynamic and competitive environment comprising over 35 active global manufacturers. The landscape features a mix of established camera brands and emerging innovators, each focusing on delivering high-resolution, modular, and AI-integrated filming equipment. Market leaders continue to secure their positions through aggressive product development, strategic partnerships with production houses, and frequent firmware upgrades to extend hardware lifespans.

In 2023–2024, competition intensified with new entrants offering compact digital cameras optimized for independent creators and online content producers. Companies are also investing in expanding their global distribution networks and entering untapped regional markets with mid-tier offerings. Recent trends include the integration of cloud-enabled workflows, real-time remote monitoring features, and machine learning algorithms that automate exposure, color grading, and facial recognition. Additionally, collaborations with software firms and virtual production platforms are influencing the innovation cycle, pushing competitors to continuously upgrade imaging sensors, frame rates, and low-light performance. Competitive success in this market increasingly depends on technological agility, user-centric design, and alignment with evolving production needs.

Canon Inc.

Sony Corporation

ARRI AG

Blackmagic Design Pty. Ltd.

RED Digital Cinema LLC

Panasonic Holdings Corporation

Nikon Corporation

Z CAM (Shenzhen ImagineVision Technology Limited)

AJA Video Systems

Kinefinity Inc.

Technological evolution is at the core of the Digital Movie Cameras Market, with manufacturers adopting innovations that redefine visual storytelling. Key trends shaping the market include full-frame sensors, high dynamic range (HDR) imaging, and real-time AI enhancements. Full-frame digital cameras now support up to 8K resolution with 16-bit RAW output, meeting the growing demand from cinema-grade productions. HDR capabilities continue to expand, enabling cameras to capture exceptional contrast ratios and rich color fidelity, even in challenging lighting conditions.

AI-powered features are being built directly into the cameras, facilitating autofocus tracking, scene-based exposure adjustments, and real-time metadata tagging. These features are vital in fast-paced production environments such as live sports and reality television. Furthermore, the market is witnessing the rise of modular camera systems, which allow filmmakers to customize setups with interchangeable lenses, recording modules, and viewfinders.

On the connectivity front, newer models now offer 5G and Wi-Fi 6 support, making live streaming and remote collaboration seamless. Onboard SSD storage, dual CFexpress slots, and cloud backup integration are also becoming standard in professional equipment. These technological advancements are pushing digital movie cameras to operate not only as imaging tools but also as intelligent systems embedded in broader digital production workflows.

• In April 2024, Blackmagic Design launched the URSA Cine 12K camera with a new full-frame sensor and open gate recording at 80 fps, targeting high-end cinema and virtual production environments.

• In January 2024, RED Digital Cinema unveiled its compact V-RAPTOR [X] 8K S35 camera, optimized for independent filmmakers and drone-based cinematography with support for real-time LUT application.

• In October 2023, Sony introduced its BURANO 8.6K cinema camera equipped with built-in image stabilization and dual base ISO technology, making it ideal for handheld and location-based shoots.

• In July 2023, Canon released the EOS C400, a full-frame digital cinema camera offering internal 6K RAW light recording and a new RF mount with electronic ND filter enhancements.

The Global Digital Movie Cameras Market Report offers a comprehensive analysis of the market landscape spanning product types, application domains, technologies, and regional insights. The scope covers both high-end professional-grade cinema cameras and compact digital cameras used in independent and online video production. It investigates modular systems, mirrorless designs, and full-frame sensor configurations, along with related technological ecosystems such as storage modules, wireless connectivity, and AI-based enhancements.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional performance, production hubs, and adoption trends. Application-focused analysis includes use in cinema production, live broadcasting, sports coverage, advertising, and online content creation. It also highlights niche and emerging segments such as virtual production studios, volumetric video capture, and cloud-native cinematography.

Additionally, the report explores industry shifts in user demand, regulatory standards, digital transformation initiatives, and the role of AI, 5G, and sustainability in camera manufacturing. The coverage is tailored to inform strategic decisions for equipment manufacturers, content producers, studios, and technology integrators seeking a clear understanding of where and how to compete in the evolving digital movie camera ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 740.0 Million |

| Market Revenue (2032) | USD 937.4 Million |

| CAGR (2025–2032) | 3.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Canon Inc., Sony Corporation, ARRI AG, Blackmagic Design Pty. Ltd., RED Digital Cinema LLC, Panasonic Holdings Corporation, Nikon Corporation, Z CAM (Shenzhen ImagineVision Technology Limited), AJA Video Systems, Kinefinity Inc. |

| Customization & Pricing | Available on Request (10 % Customization is Free) |