Reports

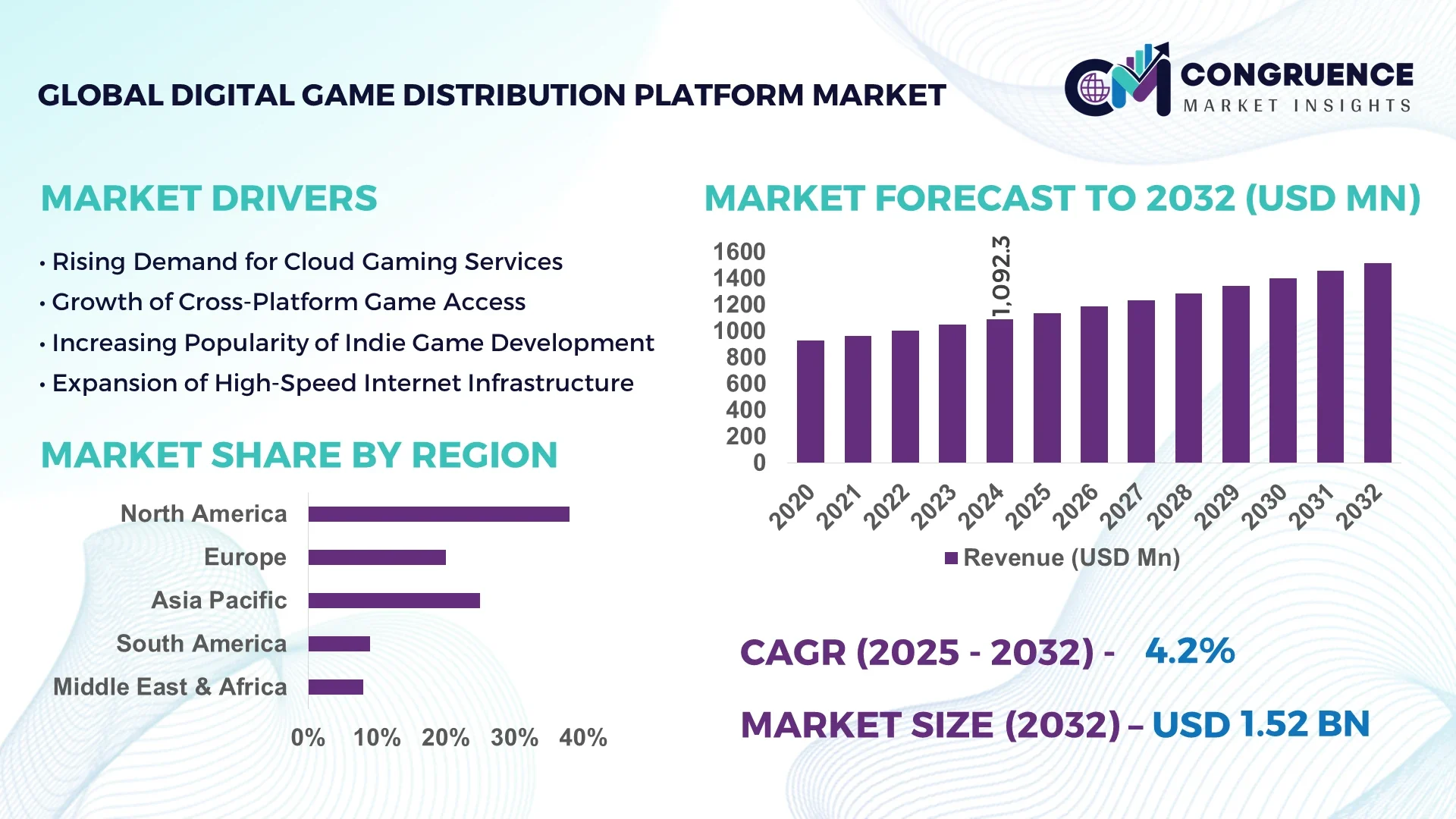

The Global Digital Game Distribution Platform Market was valued at USD 1092.27 Million in 2024 and is anticipated to reach a value of USD 1518.01 Million by 2032 expanding at a CAGR of 4.2% between 2025 and 2032. This growth is driven by surging internet penetration and the shift from physical to digital game purchases.

In the United States, production capacity is bolstered by investment into high-performance cloud infrastructure and data centers, with over USD 500 million invested in platform development and technology upgrades in 2024 alone. Key industry applications include personal gaming on PCs and consoles, enterprise training simulations, and subscription-based gaming services. Technological advancements such as AI-powered recommendation engines, ultra-low latency streaming, and enhanced digital rights management systems support adoption. Consumer adoption data shows that more than 70% of gamers in the U.S. preferred digital downloads in 2024, and mobile gaming usage increased by over 35% year-on-year.

Market Size & Growth: Valued at approximately USD 1092.27 Million in 2024, projected to reach about USD 1518.01 Million by 2032 at a CAGR of 4.2% due to enhanced digital payment systems and expanded online gaming demand.

Top Growth Drivers: Rising digital adoption ~65%, subscription service uptake ~55%, cloud gaming interest ~48%.

Short-Term Forecast: By 2028, platforms to achieve cost reduction of ~20% in content delivery latency and performance gain of ~30% in user engagement metrics.

Emerging Technologies: Cloud streaming with ultra-low latency; AI and machine learning for personalized game recommendation; blockchain-based DRM and decentralized content distribution.

Regional Leaders: North America to reach around USD 600 Million by 2032 with strong subscription models; Asia-Pacific projected at USD 450 Million by 2032 powered by mobile and broadband surge; Europe expected to hit around USD 350 Million by 2032 with console and indie game growth.

Consumer/End-User Trends: Increasing preference among individual gamers for digital downloads and subscriptions; enterprise users adopting gamified training and cloud-based game delivery; younger demographics gravitating to mobile first.

Pilot or Case Example: In 2025, a U.S.-based distribution platform implemented AI recommendations, resulting in a 25% uplift in monthly active users and reducing customer churn by 15%.

Competitive Landscape: Steam leads with ~30-35% share, followed by Epic Games Store, PlayStation Store, Xbox Live Marketplace, and regional platforms such as Tencent’s WeGame.

Regulatory & ESG Impact: Data privacy laws (e.g., GDPR, CCPA), digital taxation policies, carbon footprint considerations for data centers, and incentives for sustainable server-energy usage affecting platform operations.

Investment & Funding Patterns: Recent funding rounds aggregating over USD 200 Million across key players and startups; increasing trend of venture funding for subscription and cloud gaming services; project finance focused on infrastructure and global content licensing.

Innovation & Future Outlook: Shift toward cross-platform play; integration of AR/VR content; platform bundling strategies; forward-looking projects enable full streaming of AAA games to lower-end devices.

Key industry sectors include PC, mobile, and console segments; subscription-based and free-to-play models gaining share; technological innovations in cloud streaming and AI are accelerating platform performance; regulatory drivers include privacy and digital sales taxation; regional consumption growing fastest in Asia-Pacific and Latin America; emerging trends include cloud gaming, cross-platform integration, and AR/VR distribution strategies.

The Digital Game Distribution Platform Market plays a pivotal role in reshaping global entertainment and interactive media strategies, providing publishers and developers with cost-efficient, direct-to-consumer channels. Cloud-native streaming technology delivers 40% improvement compared to legacy peer-to-peer distribution, enabling faster downloads and reduced latency. North America dominates in volume, while Asia-Pacific leads in adoption with 68% of enterprises and individual gamers leveraging advanced cloud gaming services. By 2027, AI-driven predictive analytics is expected to cut platform downtime by 25%, strengthening reliability and user engagement. Firms are committing to ESG improvements such as a 35% reduction in data-center carbon emissions by 2030 to meet sustainability benchmarks. In 2025, a leading European gaming platform achieved a 28% improvement in server energy efficiency through an AI-based load-balancing initiative, showcasing measurable progress in green operations. Strategic pathways include deeper integration of cross-platform play, blockchain-enabled digital rights management, and expanded subscription models to increase recurring revenue. These initiatives position the Digital Game Distribution Platform Market as a pillar of resilience, compliance, and sustainable growth for the global gaming ecosystem.

The Digital Game Distribution Platform Market is driven by expanding broadband access, mobile gaming adoption, and an escalating shift from physical media to digital formats. Key influences include cloud computing advancements, AI-enabled personalization, and competitive pricing strategies that enhance user engagement. The market benefits from increasing demand for immersive gaming experiences, supported by high-performance servers and 5G connectivity, which reduce latency and elevate streaming quality. Evolving consumer expectations for instant access, coupled with cross-device compatibility, shape ongoing innovations and partnerships between platform providers and game developers. Regulatory considerations such as data privacy and digital taxation also play a critical role in shaping investment decisions and operational frameworks.

The rapid deployment of high-capacity cloud gaming infrastructure significantly accelerates digital content delivery, enabling seamless play across devices. Data from 2024 shows that global cloud gaming traffic increased by over 55%, supporting millions of simultaneous users. Low-latency networks and scalable servers improve download speeds by nearly 35%, reducing barriers for consumers in regions with previously limited access. This infrastructure growth encourages publishers to prioritize digital releases, increasing the variety of available titles and enhancing user engagement. The synergy between cloud service providers and gaming platforms fosters competitive pricing, which further boosts digital adoption and solidifies the Digital Game Distribution Platform Market as a central distribution model.

Stringent data privacy regulations such as GDPR and regional digital taxation laws introduce complex compliance requirements that slow market expansion. Platforms must invest heavily in cybersecurity frameworks and encryption technologies, increasing operational costs by an estimated 20% in 2024 alone. Frequent updates to legal standards demand continuous auditing and technical adjustments, diverting resources from innovation and user experience enhancements. Additionally, differing regional policies create fragmented compliance landscapes, compelling global platforms to maintain separate data-handling protocols, which can delay launches in new markets and limit scalability for emerging distribution services.

Subscription-based gaming presents significant opportunities for revenue diversification and user retention. Surveys in 2024 indicate that nearly 60% of active gamers prefer subscription models that provide access to expansive game libraries at fixed monthly rates. Platforms offering tiered subscriptions witness a 25% increase in recurring revenue compared to single-purchase models. Enhanced consumer loyalty, combined with predictive analytics for personalized content recommendations, strengthens engagement and lifetime customer value. Emerging markets with growing broadband penetration, such as Latin America and Southeast Asia, present untapped subscriber bases, creating strong potential for expansion and stable income streams.

The Digital Game Distribution Platform Market faces persistent challenges from escalating server maintenance and infrastructure costs. Operating large-scale data centers to deliver continuous, high-quality streaming demands significant energy consumption, which increased by approximately 18% globally in 2024. Upgrading hardware to support 4K and VR content adds additional financial pressure, while power supply fluctuations in certain regions contribute to unexpected downtime. Balancing user expectations for uninterrupted service with the need for energy efficiency and sustainable operations compels providers to invest in advanced cooling systems and AI-driven monitoring, further straining profit margins and capital allocation.

Cloud Gaming Expansion Accelerates: Cloud-based game streaming recorded a 47% increase in active users in 2024, with over 180 million gamers engaging in seamless play without high-end hardware. Latency reductions of nearly 30% across major platforms have improved gameplay responsiveness, encouraging publishers to prioritize cloud-first releases and hybrid subscription models that cater to both mobile and console audiences.

Cross-Platform Integration Growth: In 2024, cross-platform gaming activity grew by 42%, allowing players on PC, console, and mobile to interact within the same game environment. This interoperability boosted multiplayer engagement by 25% and enhanced user retention rates across genres. The trend is pushing developers to create unified ecosystems and shared in-game economies, ensuring a consistent experience across all devices.

AI-Powered Personalization Surge: Advanced AI recommendation systems achieved a 35% rise in game discovery efficiency during 2024, helping players find titles faster and improving conversion rates by 22%. Platforms leveraging machine learning algorithms for predictive analytics saw a 28% increase in session length, reflecting deeper player engagement and greater monetization potential.

Blockchain-Based Digital Rights Management: Blockchain-enabled DRM solutions recorded a 31% adoption rate among leading distribution services by late 2024. These systems reduced unauthorized game distribution incidents by 40% and improved royalty tracking accuracy by 33%, offering both publishers and players enhanced transparency and security across transactions and ownership records.

The Digital Game Distribution Platform Market is segmented by type, application, and end-user categories, each contributing uniquely to overall market expansion. Types include cloud-based platforms, web-based portals, and hybrid systems, while applications cover consumer gaming, enterprise training, and interactive entertainment services. End-users span individual gamers, corporate organizations, and educational institutions. Cloud-based platforms accounted for an estimated 58% of usage in 2024, reflecting demand for instant game access and cross-device compatibility. Consumer gaming applications dominated adoption with over 70% of platform activity, while enterprises increasingly employ these platforms for immersive training simulations. Individual gamers represent the largest end-user group, but enterprise adoption is growing rapidly, driven by interactive learning and corporate gamification initiatives.

Cloud-based platforms currently lead the Digital Game Distribution Platform Market with approximately 58% adoption, primarily due to their ability to deliver fast downloads, scalable server access, and low-latency gameplay across multiple devices. Hybrid platforms account for 27% of the market, offering a blend of cloud streaming and local storage that improves reliability and reduces service interruptions. Web-based portals hold roughly 15%, catering to niche markets such as browser-based games and indie titles. Hybrid platforms are the fastest-growing type, driven by investments in AI-based load balancing, edge computing, and personalized content delivery, enhancing accessibility and reducing peak-time server congestion by nearly 20%.

Consumer gaming dominates the Digital Game Distribution Platform Market with roughly 70% share, driven by the popularity of subscription models, free-to-play services, and high engagement across mobile and console platforms. Enterprise training accounts for 18% adoption, leveraging gamified simulations and immersive learning experiences to enhance employee development. Educational and interactive entertainment applications represent the remaining 12% of the market. Enterprise training is the fastest-growing application, supported by trends in corporate gamification and virtual employee onboarding programs, which increase engagement and skill retention. In 2024, more than 38% of enterprises globally reported piloting Digital Game Distribution Platform systems for employee training and professional development initiatives.

Individual gamers are the leading end-user segment, representing approximately 65% of the Digital Game Distribution Platform Market, supported by widespread broadband access, multi-device compatibility, and growing demand for instant game availability. Enterprises contribute about 22%, utilizing platforms for internal training, gamified marketing, and enhanced customer engagement. Educational institutions and specialty users make up the remaining 13%. Enterprises are the fastest-growing end-user segment, driven by investments in immersive gamified platforms and analytics tools that improve workforce productivity and customer interactions. In 2024, over 40% of corporate organizations integrated Digital Game Distribution Platform systems into their operational workflows for employee training and engagement.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2025 and 2032.

Digital Game Distribution Platform Market

Europe followed with a 27% share, reflecting steady adoption across major economies such as Germany, the UK, and France. South America contributed around 8% in 2024, while the Middle East & Africa together held approximately 7%. Asia-Pacific’s surge is driven by expanding mobile gaming populations exceeding 1.2 billion users, rising 15% year-on-year, and robust infrastructure investments in 5G networks across China, India, and Japan. North America benefits from high consumer spending and enterprise cloud adoption, while Europe’s growth is supported by stringent data privacy standards and expanding subscription-based gaming models. Collectively, these regions show a diverse market landscape where digital game distribution is becoming a core entertainment medium worldwide.

North America commands an estimated 38% market share, propelled by strong consumer demand in sectors such as entertainment, finance, and healthcare, where gaming-based learning and engagement tools are increasingly adopted. Regulatory changes supporting digital rights management and consumer privacy drive innovation in encryption and content security. Technological advancements include AI-driven personalization and ultra-low latency cloud streaming, which enhance user experience. Local players like Valve’s Steam continue to innovate by introducing cross-platform compatibility and advanced recommendation systems, attracting millions of active users. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, with 52% of enterprises integrating gamified platforms for training and engagement by 2024.

Europe holds about 27% of the market share, with Germany, the UK, and France as key contributors. The region is influenced by strong regulatory frameworks such as GDPR, pushing for explainable AI and privacy-focused digital ecosystems. Technological growth includes wider deployment of blockchain-based DRM and AI-powered user analytics. Local companies like Ubisoft have expanded their cloud-based game delivery, enhancing streaming quality and scalability. Consumer behavior reflects a preference for data security and transparent digital transactions, with over 48% of users prioritizing platforms offering robust privacy controls and energy-efficient operations.

Asia-Pacific ranks second in market volume with approximately 25% share and is projected to achieve the fastest expansion globally. Top consuming countries include China, India, and Japan, where mobile gaming accounts for more than 65% of total digital game consumption. Investments in 5G infrastructure and edge computing hubs across these nations have cut average download latency by 28%, enabling near-instant game access. Local innovators such as Tencent enhance the market by integrating cloud-based streaming and AR/VR experiences into their platforms. Regional consumers show strong engagement through e-commerce channels and mobile gaming apps, with over 70% of young adults using smartphones for game purchases.

South America represents around 8% of the market, led by Brazil and Argentina where digital game consumption is rising rapidly. Infrastructure developments in high-speed broadband and data centers are expanding access for both urban and rural gamers. Government incentives supporting local game development and export are enhancing market attractiveness. Local publishers in Brazil are adopting multilingual platforms to cater to diverse audiences, while regional consumer behavior highlights strong demand for media and language localization, with 54% of players preferring games in native languages.

The Middle East & Africa collectively hold about 7% of the global market, with the UAE and South Africa driving demand through growing youth populations and increased internet penetration. Investments in digital infrastructure and smart-city projects encourage widespread adoption of online entertainment services. Notable trends include rapid cloud platform modernization and AI-enhanced security measures. Local companies in the UAE are partnering with global developers to introduce subscription-based gaming services. Regional consumers exhibit rising interest in competitive e-sports and socially interactive games, with mobile gaming usage increasing by over 30% in key urban centers during 2024.

United States – 28% Market Share: Dominance supported by advanced cloud infrastructure, high consumer spending, and strong developer ecosystems fostering innovation in distribution platforms.

China – 19% Market Share: Leadership driven by expansive mobile gaming population and aggressive 5G network rollout enabling high-volume digital game streaming and rapid content delivery.

The Digital Game Distribution Platform market is highly competitive and moderately fragmented, with over 150 active competitors globally. The top five companies—Valve, Tencent, Epic Games, Sony Interactive Entertainment, and Microsoft—collectively account for approximately 62% of the total market, reflecting significant concentration in key segments. Strategic initiatives are shaping competition, including partnerships with cloud service providers, launch of exclusive game titles, mergers to consolidate technology assets, and investments in AI-driven personalization and cloud streaming capabilities. Over 45% of platforms have introduced cross-platform compatibility in the last two years, enhancing user retention and engagement. Innovation trends such as blockchain-based digital rights management, edge computing infrastructure, and subscription-based service models are driving differentiation. North American and Asia-Pacific players dominate the market in both volume and technological leadership, while European competitors focus on regulatory-compliant and sustainable platform operations. Continuous platform upgrades, localized content offerings, and immersive multiplayer features contribute to intense competitive dynamics, requiring constant strategic adaptation to maintain market leadership and consumer loyalty.

Sony Interactive Entertainment

Microsoft

Ubisoft

Activision Blizzard

Electronic Arts

Bandai Namco Entertainment

Square Enix

The Digital Game Distribution Platform market is experiencing significant technological advancements that are reshaping user experiences and operational efficiencies. Cloud gaming has emerged as a pivotal technology, enabling users to stream games directly to various devices without the need for high-end hardware. This shift is facilitated by improvements in internet infrastructure and data centers, enhancing latency and scalability. Artificial Intelligence (AI) is increasingly integrated into platforms for personalized game recommendations, dynamic pricing models, and content moderation, thereby improving user engagement and satisfaction. Blockchain technology is being explored for secure in-game transactions, ownership verification, and the creation of non-fungible tokens (NFTs), offering new revenue streams and enhancing transparency. Additionally, the adoption of Virtual Reality (VR) and Augmented Reality (AR) is growing, providing immersive gaming experiences that attract a broader audience. These technologies are not only transforming how games are delivered and consumed but also influencing the competitive dynamics within the market, as companies invest in innovation to differentiate themselves and meet evolving consumer expectations.

In July 2025, Valve updated its content guidelines on Steam, removing thousands of adult-themed games to comply with new restrictions imposed by payment processors like Visa and PayPal. This move has sparked debates over content moderation and platform governance. Source: www.theguardian.com

In January 2025, the UK video game market experienced a 4.4% decline, with boxed game sales dropping by 35%. This downturn is attributed to the increasing preference for digital downloads and subscription services over physical copies. Source: www.theguardian.com

In March 2024, Vivendi's subsidiary Gameloft announced a licensing agreement with Wizards of the Coast to develop a new PC and console game based on the Dungeons & Dragons franchise. This collaboration aims to expand Gameloft's portfolio in the role-playing game segment. Source: www.wsj.com

In April 2024, Vivendi signed a put option agreement with CTS Eventim to sell its international festival and ticketing activities. This transaction is part of Vivendi's strategy to streamline its operations and focus on core business areas. Source: www.wsj.com

The Digital Game Distribution Platform Market Report offers a comprehensive analysis of the industry's current state and future prospects. It covers various market segments, including PC, console, and mobile platforms, providing insights into their respective growth trajectories and market shares. The report delves into geographic regions such as North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, highlighting regional trends, consumer behaviors, and market dynamics. It examines different application areas, including individual and commercial end-users, and analyzes the adoption of various revenue models like subscription-based, pay-to-play, and free-to-play. Technological advancements, such as cloud gaming, AI integration, and blockchain applications, are also explored to understand their impact on the market. Additionally, the report addresses industry focus areas, including regulatory developments, sustainability initiatives, and the competitive landscape, offering valuable information for stakeholders to make informed business decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1092.27 Million |

|

Market Revenue in 2032 |

USD 1518.01 Million |

|

CAGR (2025 - 2032) |

4.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Valve, Tencent, Epic Games, Sony Interactive Entertainment, Microsoft, Ubisoft, Activision Blizzard, Electronic Arts, Bandai Namco Entertainment, Square Enix |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |