Reports

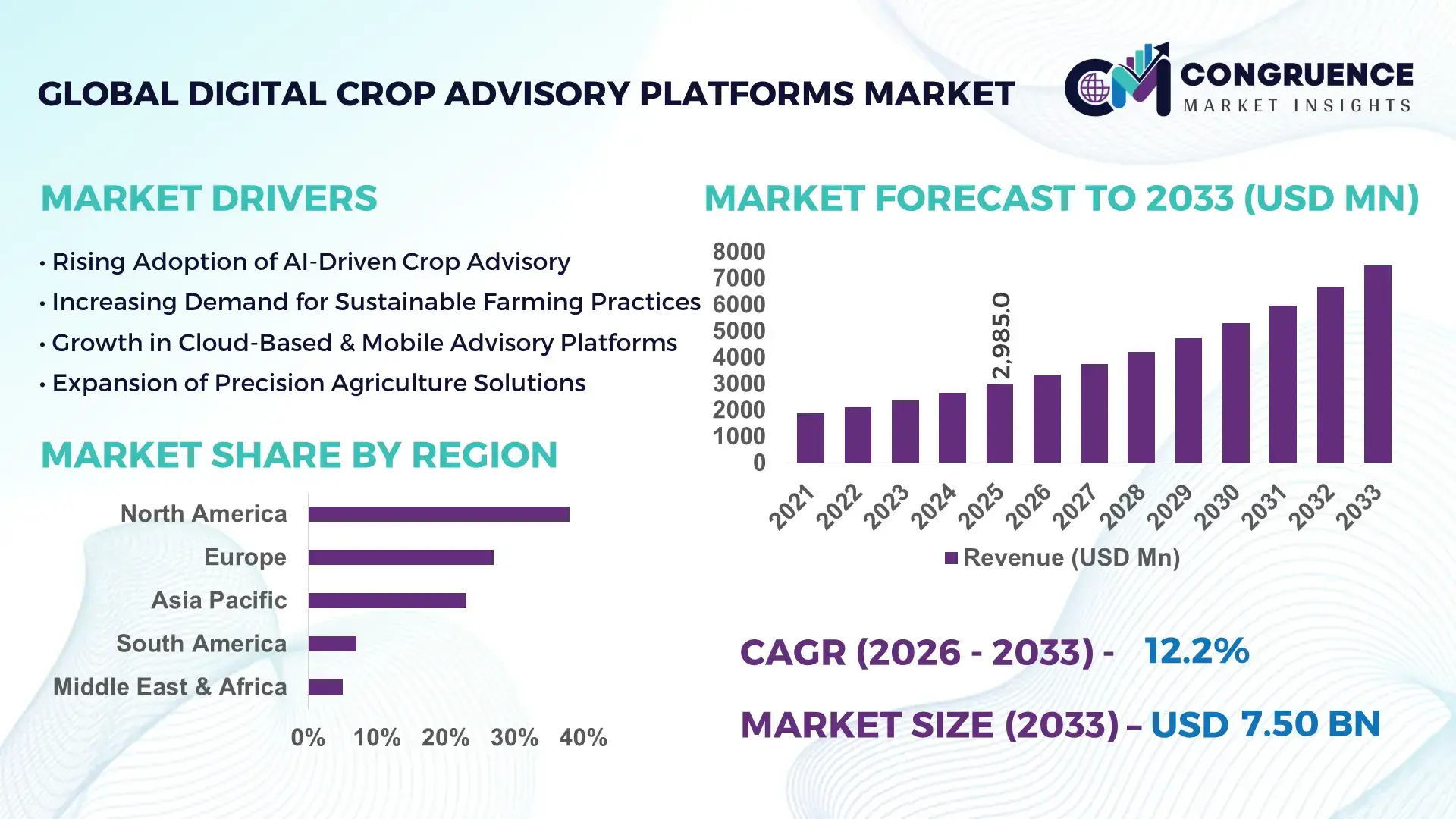

The Global Digital Crop Advisory Platforms Market was valued at USD 2,985.0 Million in 2025 and is anticipated to reach a value of USD 7,497.0 Million by 2033 expanding at a CAGR of 12.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by rapid digitization in agriculture, increasing integration of AI-based agronomy tools, and rising demand for data-backed yield optimization strategies.

The United States represents the most technologically advanced and investment-intensive country in the Digital Crop Advisory Platforms Market. Over 72% of large-scale farms in the U.S. utilize at least one form of digital farm management or advisory software, covering more than 110 million acres of cropland. Federal funding exceeding USD 1.5 billion under precision agriculture and climate-smart farming initiatives has accelerated digital advisory deployment. More than 65% of corn and soybean growers rely on satellite-driven crop monitoring platforms, while AI-enabled prescription mapping is used across approximately 40% of commercial row-crop acreage. Key applications include nutrient optimization, irrigation scheduling, pest forecasting, and carbon tracking. U.S.-based agritech startups secured over USD 900 million in venture investments in 2024 alone, supporting machine learning-based advisory engines and real-time field diagnostics integrated with IoT sensors.

Market Size & Growth: Valued at USD 2,985.0 Million in 2025, projected to reach USD 7,497.0 Million by 2033, expanding at 12.2% CAGR, driven by AI-powered farm analytics and climate-adaptive advisory systems.

Top Growth Drivers: Precision farming adoption exceeding 68%, yield improvement potential up to 25%, input cost reduction capability around 18%.

Short-Term Forecast: By 2028, AI-driven advisory platforms are expected to improve farm productivity KPIs by 20% and reduce fertilizer wastage by 15%.

Emerging Technologies: Integration of generative AI agronomy engines, satellite hyperspectral imaging, blockchain-enabled crop traceability systems.

Regional Leaders: North America projected above USD 2,900 Million by 2033 with 70% large-farm penetration; Asia-Pacific exceeding USD 2,200 Million with smallholder mobile adoption above 60%; Europe surpassing USD 1,800 Million driven by sustainability compliance digitization.

Consumer/End-User Trends: Commercial row-crop farms account for nearly 55% platform adoption, while specialty crop growers show 30% faster digital uptake.

Pilot or Case Example: In 2024, a Midwest U.S. pilot integrating AI nutrient modeling achieved 22% yield improvement and 17% nitrogen savings.

Competitive Landscape: Bayer Digital Farming holds approximately 18% share, followed by Corteva Agriscience, Trimble Agriculture, Syngenta Digital, and Climate LLC.

Regulatory & ESG Impact: Carbon farming programs target 30% emission intensity reduction by 2030, encouraging digital monitoring adoption.

Investment & Funding Patterns: Global agritech funding exceeded USD 2.4 Billion in 2024, with 35% directed toward AI-based advisory platforms.

Innovation & Future Outlook: Integration of real-time IoT soil sensors and AI weather modeling is shaping predictive advisory ecosystems for resilient agriculture.

Digital Crop Advisory Platforms Market serves row crops (55%), horticulture (25%), and specialty crops (20%), with AI-based nutrient optimization and pest forecasting being the fastest-adopted modules. Regulatory carbon accounting frameworks and climate-risk disclosures are accelerating enterprise adoption. Asia-Pacific smallholder digitization programs show 60% mobile advisory penetration. Increasing satellite resolution below 1 meter and drone-enabled analytics are strengthening predictive insights, positioning the sector for technology-led operational efficiency gains across global agricultural systems.

The Digital Crop Advisory Platforms Market holds strategic relevance as agriculture transitions from input-intensive to intelligence-driven production systems. AI-powered agronomy platforms deliver up to 25% yield improvement compared to conventional manual scouting methods, while predictive irrigation models reduce water usage by nearly 20% versus traditional scheduling standards. These measurable performance gains are reshaping farm-level decision frameworks and enterprise-level agri-investment strategies.

North America dominates in volume of digitally managed acreage exceeding 110 million acres, while Asia-Pacific leads in mobile advisory adoption with over 60% of digitally engaged smallholder users. By 2028, AI-enabled predictive crop stress modeling is expected to cut unplanned yield loss by 18%, significantly strengthening farm resilience. Firms are committing to ESG-linked metrics such as 30% reduction in fertilizer runoff intensity by 2030 through data-backed prescription mapping and nutrient optimization systems.

In 2024, a U.S.-based agribusiness deployment of satellite-linked advisory software achieved 21% improvement in water-use efficiency across 500,000 acres through AI irrigation modeling. Digital twin crop simulations are emerging as a next-generation benchmarking tool, offering 15% faster agronomic response compared to legacy advisory dashboards.

Looking ahead, the Digital Crop Advisory Platforms Market is positioned as a pillar of resilience, compliance alignment, and sustainable agricultural transformation, enabling climate-smart production, resource efficiency, and traceable value chains across global farming ecosystems.

The Digital Crop Advisory Platforms Market is evolving under the influence of digitization in agriculture, climate variability, and increasing regulatory compliance requirements. Over 65% of large-scale farms globally now deploy some form of digital farm management tool, indicating structural transformation in decision-making models. Advancements in remote sensing, satellite imaging with sub-meter resolution, and IoT-enabled soil diagnostics are enhancing advisory precision. Government-backed digital agriculture missions across Asia-Pacific and Europe are accelerating smallholder onboarding, while enterprise agribusinesses are integrating advisory dashboards with ERP and supply chain systems. Sustainability metrics, including carbon footprint monitoring and nitrogen efficiency tracking, are becoming embedded platform features. Additionally, mobile-based advisory applications are expanding rapidly, particularly in emerging economies where smartphone penetration in rural farming communities has surpassed 55%, reinforcing scalable, data-driven crop management practices.

Precision agriculture adoption is significantly driving the Digital Crop Advisory Platforms Market as farmers increasingly rely on data-backed decisions to optimize productivity. Approximately 68% of commercial farms in developed markets use GPS-guided machinery and satellite imaging tools integrated with advisory platforms. Variable rate technology (VRT) adoption has grown beyond 50% in large-scale grain farms, enabling site-specific nutrient and pesticide application. AI-driven crop stress detection systems can identify yield threats up to 10 days earlier than traditional scouting methods, reducing potential losses by 15–20%. Soil moisture sensor installations have increased by 30% annually in high-value crop segments, strengthening demand for integrated advisory analytics. As climate volatility intensifies, predictive modeling and real-time crop health alerts are becoming operational necessities, accelerating enterprise-wide subscription to digital advisory ecosystems.

Despite technological advancements, interoperability challenges remain a restraint for the Digital Crop Advisory Platforms Market. Nearly 40% of farms using digital tools report compatibility issues between machinery sensors, satellite feeds, and advisory dashboards. Fragmented data standards across equipment manufacturers create integration inefficiencies, leading to underutilization of advanced analytics modules. Additionally, rural broadband connectivity gaps affect approximately 25% of agricultural land in developing economies, limiting real-time data synchronization. High initial onboarding and customization costs for enterprise farms can extend deployment cycles by 6–12 months. Concerns regarding data ownership and cybersecurity risks are also rising, with 35% of surveyed agribusiness operators expressing hesitation in sharing field-level data across third-party cloud platforms. These structural barriers slow seamless platform scaling.

AI-based climate adaptation models offer significant growth opportunities within the Digital Crop Advisory Platforms Market. Extreme weather variability has increased crop yield volatility by nearly 20% over the past decade, intensifying demand for predictive forecasting tools. Machine learning models capable of processing 10+ years of weather and soil datasets can improve seasonal yield forecasting accuracy by 30%. Emerging carbon credit programs covering over 40 million hectares globally require precise digital measurement and reporting systems, opening new advisory revenue streams. Additionally, smartphone penetration among smallholder farmers in Asia and Africa has surpassed 60%, enabling scalable deployment of mobile-based advisory apps. Integration of drone analytics, which can reduce field inspection time by 70%, further enhances advisory service efficiency and monetization potential.

Increasing regulatory scrutiny on agricultural emissions and input usage presents operational challenges for the Digital Crop Advisory Platforms Market. Over 30 countries now mandate farm-level reporting of fertilizer and pesticide usage under environmental compliance frameworks. Platforms must incorporate carbon accounting, water usage metrics, and traceability dashboards aligned with global sustainability standards. Developing standardized carbon intensity measurement models across diverse cropping systems remains technically complex. Compliance verification processes can increase administrative workload by 15–20% for platform operators. Additionally, aligning advisory outputs with evolving ESG disclosure rules requires continuous software upgrades and integration of third-party validation tools. These compliance-driven requirements elevate R&D costs and extend product development cycles while increasing accountability pressures across agritech providers.

AI-Based Hyperlocal Weather Forecasting Adoption Surpasses 65% Among Commercial Farms: Advanced AI weather engines now process over 500,000 data points per farm annually, improving forecast accuracy by 28% compared to traditional meteorological advisories. Farms using hyperlocal prediction tools report 18% reduction in climate-related yield losses and 12% better irrigation planning efficiency.

Satellite Imagery Resolution Improving Below 1 Meter for Crop Diagnostics: High-resolution satellite imaging adoption has increased by 40% in the past three years, enabling early pest and nutrient deficiency detection with 20% faster response times. Over 75 million hectares globally are now monitored through remote sensing-integrated advisory dashboards.

Integration of Carbon Tracking Modules Across 45% of Enterprise Platforms: Sustainability-linked advisory features have expanded rapidly, with 45% of enterprise-grade platforms embedding carbon footprint measurement tools. Farms utilizing digital carbon monitoring systems report 22% improvement in nitrogen-use efficiency and 15% reduction in input over-application.

Mobile-First Advisory Applications Driving 60% Smallholder Engagement in Asia-Pacific: Mobile advisory app downloads in emerging markets have grown by 35% year-over-year. Push-notification-based agronomic alerts improve farmer response rates by 30%, while localized language support increases platform engagement duration by 25%, strengthening inclusive digital agriculture transformation.

The Digital Crop Advisory Platforms Market is segmented by type, application, and end-user, reflecting the expanding technological depth and diversified adoption patterns across global agriculture. By type, cloud-based advisory systems dominate deployments due to scalability and integration with IoT devices, while AI-driven predictive analytics modules are emerging rapidly as farms shift toward precision input optimization. On-premise systems remain relevant in regions with limited connectivity infrastructure.

By application, nutrient management and yield optimization represent the largest use cases, accounting for over 35% of total platform utilization, followed by irrigation scheduling and pest forecasting solutions. Carbon tracking and sustainability compliance modules are gaining traction as regulatory mandates expand across more than 30 countries.

From an end-user perspective, large commercial farms account for the majority of adoption, covering over 60% of digitally monitored acreage globally. However, smallholder farmer participation is rising steadily, supported by mobile-first advisory applications and public digital agriculture initiatives. Agribusiness corporations and cooperatives are also integrating advisory platforms into supply chain optimization frameworks, reinforcing enterprise-level deployment strategies.

The Digital Crop Advisory Platforms Market by type includes cloud-based platforms, on-premise solutions, AI-driven predictive analytics modules, and mobile-first advisory applications. Cloud-based platforms currently account for approximately 48% of total deployments due to their scalability, real-time data synchronization, and compatibility with satellite imaging and IoT sensors. In comparison, on-premise systems hold nearly 22%, primarily in regions where data sovereignty and connectivity constraints require localized infrastructure. AI-driven predictive analytics modules represent about 20% of installations but are expanding fastest, with an estimated CAGR of 15.8%, as farms increasingly demand machine learning-based yield forecasts and climate risk modeling. Mobile-first advisory applications contribute the remaining 10%, particularly in emerging economies where smartphone penetration in rural areas exceeds 60%.

The fastest growth is observed in AI-powered predictive platforms, driven by the ability to process multi-year agronomic datasets and deliver up to 30% higher forecast accuracy compared to rule-based advisory engines. These systems also reduce manual scouting time by nearly 40%, strengthening operational efficiency.

In 2024, the United States Department of Agriculture reported that over 55% of large-scale U.S. farms were using cloud-based farm management or advisory software integrated with precision agriculture tools, reinforcing the dominance of scalable digital platforms.

Application areas in the Digital Crop Advisory Platforms Market include nutrient management, irrigation scheduling, pest and disease forecasting, yield prediction, and carbon tracking & sustainability compliance. Nutrient management currently leads with nearly 35% share of total application usage, as precision fertilizer recommendations can reduce nitrogen over-application by up to 20%. Irrigation scheduling accounts for approximately 25%, supported by AI-based soil moisture monitoring systems that enhance water-use efficiency by 18%. Pest and disease forecasting contributes around 18%, while yield prediction tools account for 12%. Carbon tracking and compliance-focused modules represent the fastest-growing application, expanding at an estimated CAGR of 16.5%, driven by regulatory requirements in more than 30 countries mandating farm-level emission reporting. The remaining applications collectively account for about 10% of usage, including crop insurance analytics and supply chain traceability dashboards.

In 2025, over 40% of enterprise agribusinesses reported piloting AI-driven nutrient optimization modules across multi-state farming operations. Additionally, nearly 58% of digitally engaged farmers indicated higher trust in advisory platforms that integrate satellite imagery with soil analytics.

In 2024, the Food and Agriculture Organization highlighted the deployment of digital decision-support tools across more than 25 countries under climate-smart agriculture initiatives, supporting millions of farmers in nutrient and water optimization programs.

End-user segmentation in the Digital Crop Advisory Platforms Market includes large commercial farms, smallholder farmers, agribusiness corporations, cooperatives, and government-supported agricultural programs. Large commercial farms represent the leading segment with approximately 52% adoption share, supported by higher capital availability and integration of GPS-guided machinery across more than 70% of large-scale acreage in developed markets. Smallholder farmers account for about 28% of adoption, benefiting from mobile-based advisory apps and digital extension services. Agribusiness corporations and cooperatives contribute roughly 15%, leveraging advisory analytics for contract farming and supply chain optimization. Government and research institutions represent the remaining 5%, primarily for pilot and climate adaptation programs.

While large farms dominate current installations, smallholder adoption is growing fastest at an estimated CAGR of 17.2%, driven by smartphone penetration exceeding 60% in rural Asia-Pacific regions and subsidized digital agriculture initiatives. In 2025, nearly 38% of global agribusiness enterprises reported integrating digital crop advisory systems into enterprise resource planning platforms. Furthermore, 62% of younger farmers under age 40 show preference for mobile-based agronomic alerts compared to traditional advisory channels.

In 2024, the European Commission reported that digital advisory tools were integrated into national agricultural support programs across multiple EU member states, enabling thousands of farms to monitor nutrient usage and environmental compliance digitally.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.4% between 2026 and 2033.

North America’s leadership is supported by over 110 million acres under digital monitoring and more than 70% adoption of precision agriculture tools across large-scale farms. Europe holds approximately 27% share, driven by sustainability mandates covering over 40% of agricultural land under environmental compliance frameworks. Asia-Pacific represents nearly 23% of the global market, with more than 120 million smallholder farmers increasingly accessing mobile-based advisory applications. South America contributes around 7%, supported by large soybean and maize production clusters spanning over 80 million hectares. Middle East & Africa collectively account for 5%, with irrigation-focused advisory demand rising across water-stressed agricultural zones. Regional disparities are influenced by digital infrastructure maturity, farm size distribution, regulatory compliance intensity, and climate variability exposure.

North America holds approximately 38% share of the Digital Crop Advisory Platforms Market, supported by widespread digital infrastructure and enterprise-scale farm operations. The United States and Canada together manage over 150 million hectares of cultivated land, with more than 72% of large commercial farms deploying GPS-guided equipment integrated with advisory dashboards. Key demand originates from corn, soybean, and wheat production systems, where AI-driven nutrient optimization reduces fertilizer usage by up to 20%. Federal programs promoting climate-smart agriculture and conservation compliance impact over 60% of federally supported farmland. Technological advancements include hyperspectral satellite imaging below 1-meter resolution and IoT-enabled soil sensors with 95% real-time accuracy. Bayer Digital Farming and Climate LLC continue expanding AI prescription tools covering millions of acres. Regional consumer behavior indicates strong enterprise-led adoption, with over 65% of farm operators preferring subscription-based cloud platforms integrated with ERP and supply chain analytics systems.

Europe accounts for nearly 27% of the Digital Crop Advisory Platforms Market, driven by strong regulatory frameworks and environmental performance targets. Germany, France, and the United Kingdom collectively represent over 55% of the regional demand. More than 40% of EU agricultural land operates under compliance mechanisms linked to nutrient management and carbon reduction strategies. Digital advisory tools supporting nitrogen balance tracking have improved fertilizer efficiency by approximately 18% across monitored farms. Emerging technologies include AI-powered carbon accounting modules and blockchain-based traceability platforms integrated into farm advisory systems. Precision irrigation systems are installed across nearly 30% of high-value horticulture acreage. Yara International has expanded digital crop nutrition advisory services across multiple EU markets, enhancing farm-level decision precision. Regional behavior trends indicate regulatory-driven demand, with over 50% of European farmers prioritizing explainable AI outputs aligned with sustainability audits and reporting obligations.

Asia-Pacific holds about 23% share of the Digital Crop Advisory Platforms Market and ranks as the fastest-growing regional cluster. China, India, and Japan are the leading consuming countries, collectively representing over 65% of regional digital advisory users. The region supports more than 120 million smallholder farmers, with smartphone penetration in rural communities exceeding 60%. Government-backed digital agriculture missions in India alone target coverage of over 20 million farmers through AI-based advisory applications. Infrastructure modernization includes satellite-linked crop monitoring systems covering more than 50 million hectares in China. Innovation hubs across Bengaluru, Shenzhen, and Tokyo are advancing AI crop modeling and drone-enabled diagnostics that reduce field scouting time by 70%. Regional consumer behavior is highly mobile-centric, with more than 75% of advisory interactions occurring via app-based push notifications and localized language interfaces.

South America represents approximately 7% of the Digital Crop Advisory Platforms Market, primarily driven by Brazil and Argentina, which together cultivate over 90 million hectares of soybeans and maize. Brazil alone accounts for more than 60% of regional adoption, supported by large mechanized farm clusters. Digital irrigation and pest forecasting tools are increasingly deployed across export-oriented crop segments, where yield improvements of 15–20% significantly impact trade competitiveness. Infrastructure expansion in rural broadband has improved connectivity coverage to nearly 68% of productive farmland in Brazil. Government-supported digital innovation programs encourage precision farming integration for climate resilience. Local agritech firms are expanding satellite-based advisory coverage across soybean belts exceeding 35 million hectares. Regional consumer behavior reflects demand tied to commodity optimization and language-localized advisory tools tailored for Portuguese and Spanish-speaking producers.

Middle East & Africa account for roughly 5% of the Digital Crop Advisory Platforms Market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Agriculture in water-stressed regions is accelerating adoption of AI-based irrigation scheduling systems capable of reducing water consumption by 25%. Over 35% of commercial farms in the Gulf Cooperation Council countries deploy sensor-based irrigation monitoring solutions. Technological modernization efforts include greenhouse automation systems integrated with advisory dashboards covering more than 12,000 hectares in controlled-environment agriculture. South Africa leads Sub-Saharan adoption, supported by commercial grain and fruit export sectors. Government-backed food security initiatives aim to increase domestic crop productivity by 20% through digital agronomy programs. Consumer behavior trends show preference for water-efficiency analytics and climate-resilient crop planning tools aligned with desert and semi-arid farming conditions.

United States – 34% Market Share: Strong precision agriculture infrastructure covering over 110 million acres and high enterprise-level adoption of AI-based crop advisory systems.

China – 16% Market Share: Extensive smallholder digitization programs reaching over 50 million hectares and government-supported AI-driven smart agriculture deployment initiatives.

The Digital Crop Advisory Platforms Market is moderately fragmented, with more than 80 active global and regional technology providers competing across cloud-based agronomy software, AI analytics modules, and satellite-integrated advisory services. The top five companies collectively account for approximately 52% of the global market, indicating a semi-consolidated structure led by established agritech multinationals and precision agriculture specialists. Market leaders maintain competitive positioning through vertically integrated ecosystems that combine seed genetics data, satellite imaging, IoT sensors, and prescription-based agronomy engines.

Strategic initiatives in 2024–2025 have centered on AI model enhancement, geospatial analytics integration, and sustainability-linked advisory modules. Over 35% of major competitors expanded partnerships with satellite data providers to improve sub-meter crop health monitoring accuracy. More than 20 strategic collaborations were recorded between agritech firms and carbon credit verification platforms to embed carbon accounting dashboards directly into advisory systems. Product innovation remains a key differentiator, with nearly 40% of leading vendors launching upgraded AI-driven nutrient optimization engines capable of improving nitrogen-use efficiency by up to 22%.

Mergers and acquisitions activity remains selective but strategic, targeting drone analytics startups and soil data intelligence providers. Competitive intensity is further influenced by regional startups offering localized language advisory tools, particularly in Asia-Pacific and Latin America. Subscription-based SaaS models dominate pricing strategies, representing over 65% of deployment contracts among enterprise farms.

Syngenta Group

Yara International

BASF Digital Farming

Deere & Company

Farmers Edge

Granular Inc.

CropX Technologies

Ag Leader Technology

Topcon Agriculture

The Digital Crop Advisory Platforms Market is rapidly evolving through integration of artificial intelligence, remote sensing, IoT-enabled field diagnostics, and cloud-based analytics architectures. AI-driven predictive models now process over 10–15 years of historical weather and soil datasets, improving seasonal yield forecasting accuracy by approximately 30% compared to rule-based advisory systems. Hyperspectral satellite imaging with sub-meter resolution enables early pest detection up to 10 days earlier than manual scouting, reducing crop loss risk by nearly 18%.

IoT soil sensors capable of measuring moisture, pH, and nutrient variability in real time have achieved deployment densities of 1 sensor per 5–10 hectares in high-value crop systems. Integration with variable rate technology (VRT) allows fertilizer application precision within ±5% of optimal nutrient thresholds. Drone-based crop imaging adoption has increased by over 35% in commercial farms, reducing field inspection time by 60–70%.

Cloud-native SaaS architectures account for more than 65% of deployments, ensuring scalability across multi-location farm enterprises. Blockchain-enabled traceability modules are being embedded into advisory dashboards, covering over 40 million hectares globally for carbon tracking and supply chain transparency. Edge computing integration is emerging to reduce data latency by up to 25%, particularly in remote agricultural zones with limited connectivity. Collectively, these technologies are transforming advisory platforms from descriptive dashboards into predictive, prescriptive, and compliance-aligned digital ecosystems.

• In November 2025, CropX Technologies and Reinke Manufacturing announced an enhanced integration that brings CropX soil and agronomic data directly into Reinke’s ReinCloud® 3 platform, enabling farmers to access soil, weather, and agronomy insights in a unified interface for improved irrigation and crop management decisions. Source: www.cropx.com

• In March 2025, CropX Technologies launched the Strato 1 in-field weather station, providing real-time hyperlocal weather measurements feeding directly into CropX’s agronomy platform to strengthen on-farm decision support and improve operational planning. Source: www.cropx.com

• In December 2024, CropX announced a digital connection with CLAAS Farm Machinery that allows CLAAS machine data to flow into CropX’s precision agronomy platform, enabling combined data analytics for variable rate applications and improved farm optimization. Source: www.cropx.com

• In May 2025, Syngenta Group announced a strategic collaboration with Al Dahra to implement Cropwise® Operations digital farm management solutions across more than 220,000 acres, enabling centralized data monitoring, enhanced pest response, and improved water usage and irrigation efficiency. Source: www.syngenta.com

The Digital Crop Advisory Platforms Market Report provides comprehensive coverage across product types, applications, technologies, end-user categories, and geographic regions. The report evaluates cloud-based advisory systems, AI-driven predictive analytics engines, mobile-first agronomy applications, and on-premise farm management platforms. Application coverage includes nutrient optimization, irrigation scheduling, pest and disease forecasting, yield modeling, carbon accounting, and supply chain traceability.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, analyzing region-specific adoption patterns across more than 150 million digitally monitored hectares globally. End-user segmentation includes large commercial farms, smallholder farmers exceeding 120 million globally, agribusiness corporations, cooperatives, and government-backed digital agriculture initiatives.

The scope further assesses technology integration trends such as IoT sensor deployment densities, satellite resolution advancements below 1 meter, AI-based seasonal forecasting models improving prediction accuracy by up to 30%, and drone analytics reducing manual scouting time by nearly 70%. Regulatory and sustainability frameworks across over 30 countries are evaluated in relation to digital carbon tracking and nutrient compliance systems.

Additionally, the report reviews competitive positioning of over 80 active technology providers, subscription-based SaaS deployment models representing 65% of contracts, and strategic innovation initiatives shaping enterprise-level adoption. Emerging niche segments including regenerative agriculture analytics and climate risk modeling platforms are also examined, offering forward-looking insights for stakeholders seeking data-driven agricultural transformation strategies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,985.0 Million |

| Market Revenue (2033) | USD 7,497.0 Million |

| CAGR (2026–2033) | 12.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Bayer AG (Climate FieldView); Corteva Agriscience; Trimble Inc.; Syngenta Group; Yara International; BASF Digital Farming; Deere & Company; Farmers Edge; Granular Inc.; CropX Technologies; Ag Leader Technology; Topcon Agriculture |

| Customization & Pricing | Available on Request (10% Customization Free) |