Reports

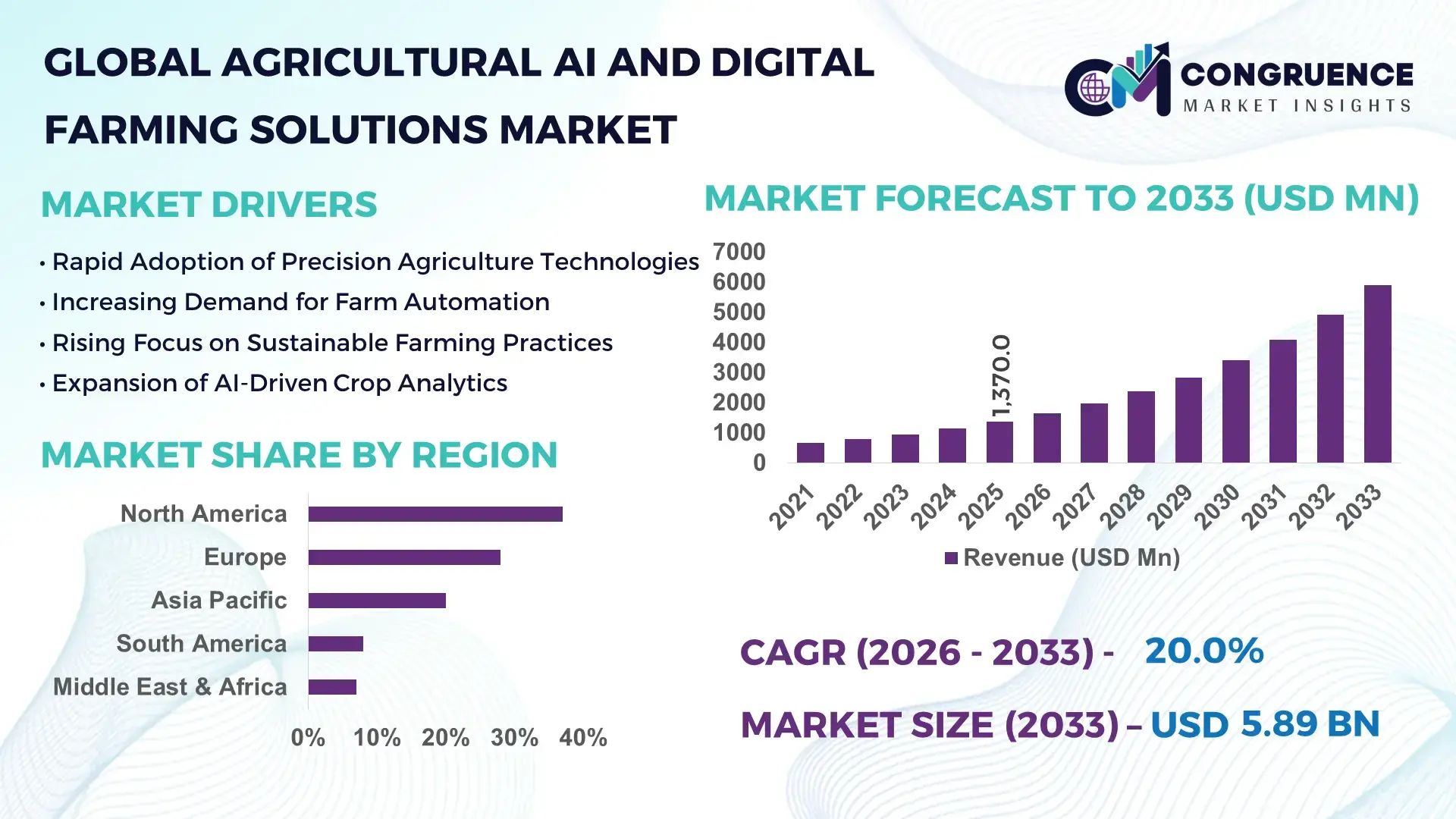

The Global Agricultural AI and Digital Farming Solutions Market was valued at USD 1,370.0 Million in 2025 and is anticipated to reach a value of USD 5,890.7 Million by 2033 expanding at a CAGR of 20% between 2026 and 2033, according to an analysis by Congruence Market Insights due to accelerated adoption of data‑driven farming practices and automation technologies. This growth is driven by rising demand for precision agriculture, labor optimization, and real‑time decision support tools across large commercial farms and agritech enterprises.

The United States leads the Agricultural AI and Digital Farming Solutions Market with extensive deployment of autonomous machinery, advanced sensor networks, and machine‑learning platforms across major crop belts. U.S. farms invested over USD 250 million in AI‑based crop monitoring systems in 2025, and adoption rates of digital farm management platforms exceed 60% among large enterprises. Production capacity for precision irrigation and yield‑optimization solutions is highest in the Midwest, with over 1,200 active installations of AI‑integrated hardware reported in 2025.

Market Size & Growth: Market valued at USD 1,370.0M in 2025, projected to USD 5,890.7M by 2033 at ~20% CAGR due to digital transformation in farming operations driving efficiency and predictive capabilities.

Top Growth Drivers: Precision agriculture adoption at 58%, cost savings via automation at 45%, data analytics utilization at 62%.

Short-Term Forecast: By 2028, digital solutions expected to improve crop yield predictability by up to 35% and reduce input costs by 28%.

Emerging Technologies: AI‑enabled drones for crop monitoring, edge computing for real‑time data processing, and machine vision for disease detection.

Regional Leaders: North America projected to reach USD 2,200M by 2033 with high mechanization; Europe at USD 1,850M with focus on sustainable farming; Asia Pacific at USD 1,560M with rapid digital adoption.

Consumer/End-User Trends: Large commercial farms leading adoption with integrated AI platforms; smallholders increasingly using mobile analytics tools.

Pilot or Case Example: In 2027, a Midwest farm cluster reported 32% reduction in fertilizer use through AI‑driven nutrient management pilots.

Competitive Landscape: Market leader commands ~28% share with key competitors including major global agritech and software firms.

Regulatory & ESG Impact: New agrotech standards and sustainability mandates are accelerating compliance‑oriented digital solutions.

Investment & Funding Patterns: Over USD 480M in venture funding into agri‑AI startups in recent cycles with growth in project financing for farm automation.

Innovation & Future Outlook: Integration of predictive analytics with autonomous machinery and expansion of 5G‑enabled field systems shaping next‑gen farming solutions.

Agricultural AI and Digital Farming Solutions span precision crop management, automated irrigation, livestock monitoring, and supply chain traceability systems. Recent innovations include real‑time soil health sensors and AI diagnostic tools improving decisions in crop rotation and pest control. Regulatory shifts favor low‑impact technologies, while economic drivers include rising labor costs and resource optimization imperatives, shaping regional uptake and future expansion.

The Agricultural AI and Digital Farming Solutions market is strategically relevant as farming enterprises seek measurable improvements in operational efficiency, sustainability performance, and resource utilization. Advanced AI platforms deliver up to 40% improvement in predictive accuracy compared to traditional statistical models, enabling precise irrigation scheduling, automated pest detection, and yield forecasting that directly improve profitability. While North America dominates in volume deployment of autonomous tractors and sensor networks, Europe leads in adoption with over 55% of agribusinesses integrating digital platforms. These regional variations reflect differing farm sizes, capital availability, and regulatory frameworks emphasizing environmental compliance and data interoperability.

Over the next 2–3 years, AI‑driven decision support systems are expected to cut water usage by 30% and fertilizer waste by 25% through optimized nutrient profiling and adaptive scheduling. Agricultural firms are committing to measurable ESG targets such as a 20% reduction in greenhouse gas intensity by 2028, leveraging digital tracking and analytics to monitor progress. In 2027, several large agritech integrators reported more than 35% improvement in harvesting efficiency using machine vision and robotics, underscoring the concrete performance gains realized through these innovations.

Strategically, market participants are focusing on building ecosystem partnerships, investing in scalable cloud platforms, and expanding modular AI toolkits that can adapt across diverse crop types and climates. The future pathway points toward convergence of AI with robotics, IoT, and edge computing, positioning the Agricultural AI and Digital Farming Solutions market as a pillar of resilience, compliance, and sustainable growth in global food systems.

The Agricultural AI and Digital Farming Solutions market dynamics are shaped by the shift from traditional farming to precision agriculture, increased demand for yield optimization, and the adoption of sensor‑based decision systems. Stakeholders are responding to labor constraints by implementing autonomous equipment and real-time analytics that reduce manual intervention. Regulatory mandates for environmental stewardship are also prompting investments in technologies that monitor soil health and reduce chemical inputs. Competitive pressures are driving suppliers to differentiate through feature‑rich software platforms that integrate machine learning, predictive models, and farm management systems, altering how agribusinesses plan, execute, and evaluate operations.

Demand for precision agriculture is driving market growth by enabling farmers to optimize inputs, increase output quality, and reduce waste. Precision agriculture technologies such as variable rate application systems and geospatial analytics use real‑time field data to fine-tune seeding, fertilization, and irrigation. Over 60% of large commercial farms have adopted geolocation services and AI‑powered monitors to manage variability within fields, leading to measurable increases in crop quality indices and reductions in water and chemical usage. These systems support risk mitigation by providing early warnings of pest outbreaks and nutrient deficiencies, empowering agronomists with actionable insights.

High implementation costs and infrastructure gaps restrain market growth as smaller farms face capital barriers to adopt sophisticated AI and digital solutions. Initial expenditures on sensors, connectivity infrastructure, and platform subscriptions can exceed operational budgets for mid‑sized farms, slowing uptake. Additionally, rural connectivity limitations in certain regions hinder real‑time data transmission and cloud-based analytics, restricting the practical utility of advanced tools. These financial and infrastructure constraints create adoption bottlenecks, particularly where traditional farming practices remain entrenched.

Integration of edge computing presents opportunities by enabling real‑time analytics directly in the field, reducing latency and dependency on centralized cloud systems. Edge devices process sensor data on-site, allowing instant decision support for irrigation control, pest detection, and machinery automation. Firms deploying edge-enabled AI platforms report improvements in response times of up to 50% for critical operational alerts. This technological shift opens markets in regions with limited connectivity and positions vendors to offer scalable, low-latency solutions tailored to diverse agricultural environments.

Technical skills gaps and data interoperability issues challenge market progress as farmers and agribusinesses struggle to manage complex systems and integrate heterogeneous data streams. Many digital farming platforms require specialized training to interpret analytics and adapt workflows, creating dependence on external consultants. Additionally, incompatible data formats between different vendors’ tools impede seamless integration, undermining comprehensive farm management views. These challenges slow deployment rates and can dilute the value proposition of sophisticated AI systems, particularly for users without IT support.

Expansion of Autonomous Crop Monitoring Technologies: Deployment of autonomous drones and ground rovers equipped with multi-spectral sensors has increased 48% year-over-year, enabling 24/7 field surveillance and early detection of crop stress across large acreage.

Growth in Mobile-First Farm Management Apps: Mobile apps tailored for small and medium farms have achieved 65% adoption in key regions, facilitating task planning, input tracking, and remote equipment status checks, boosting operational agility.

Adoption of AI-Based Predictive Analytics: Predictive models for pest and disease forecasting are now used by over 70% of commercial farms, delivering actionable risk alerts and supporting proactive field interventions.

Surge in Satellite-Enabled Soil & Weather Insights: Use of satellite imagery combined with AI to generate soil health and micro-weather forecasts has increased by 55%, underpinning more accurate irrigation scheduling and resource allocation.

The Agricultural AI and Digital Farming Solutions Market is segmented by type, application, and end-user, reflecting the diverse technological and operational needs of modern agriculture. By type, the market is dominated by autonomous machinery, precision sensors, and AI-powered analytics platforms, each contributing distinct functionality to crop monitoring, irrigation optimization, and yield forecasting. Application-wise, crop management systems, livestock monitoring solutions, and supply chain traceability tools represent the core functional segments. End-users range from large commercial farms and agribusinesses to smallholder and emerging-scale farms adopting mobile and cloud-based platforms. Integration of IoT devices, real-time monitoring systems, and AI-driven predictive models allows precision agriculture tools to deliver measurable efficiency improvements, reduce labor dependency, and enhance resource utilization across multiple farm types. Consumer adoption trends indicate that large-scale commercial farms implement multiple AI-enabled modules simultaneously, while smallholders focus on mobile-enabled solutions, creating a layered market structure.

Autonomous machinery currently leads the product type segment, accounting for approximately 38% of market adoption due to its role in enhancing efficiency, labor reduction, and consistent operation in field activities such as planting, harvesting, and monitoring. Precision sensors follow with a 30% adoption share, offering critical soil, moisture, and crop health data. AI-powered analytics platforms make up 20% of adoption, supporting decision-making and predictive modeling. Other niche types, including robotic irrigation systems and drone-based field assessment tools, contribute a combined 12% share, addressing specialized operational needs and experimental applications.

The fastest-growing type is AI-powered analytics platforms, driven by increasing demand for predictive insights, disease detection, and integrated farm management dashboards. Adoption is expanding rapidly across mid-sized and large commercial farms implementing cloud and edge-based solutions.

Crop management remains the leading application segment, accounting for 42% of total adoption. This is due to its critical role in yield optimization, resource allocation, and real-time crop health monitoring. Livestock monitoring systems follow with a 28% adoption share, providing critical data on animal health, feeding patterns, and productivity. Supply chain and traceability solutions account for 15%, ensuring efficient logistics, compliance, and food safety. Other applications, including soil analytics and irrigation optimization platforms, comprise the remaining 15% share.

The fastest-growing application is precision irrigation systems, driven by increasing water scarcity concerns, rising adoption of IoT-connected devices, and regulatory emphasis on sustainable water usage.

Consumer adoption statistics show that in 2025, over 60% of large commercial farms integrated crop management AI platforms, while smallholder adoption of mobile-enabled irrigation applications reached 48%.

Large commercial farms currently dominate the end-user segment with a 45% share, leveraging integrated AI and digital platforms to enhance operational efficiency and maximize output across multi-crop and multi-location operations. Small and mid-sized farms constitute 35%, adopting modular solutions for cost-effective, targeted improvements in irrigation, pest management, and crop rotation. Emerging farms and experimental agribusinesses make up the remaining 20%, often focusing on niche technologies such as drone monitoring, robotic weeding, and autonomous irrigation systems.

The fastest-growing end-user segment is mid-sized farms, fueled by improved accessibility of cloud-based analytics and affordable precision agriculture kits, enabling measurable efficiency gains and labor optimization.

Consumer adoption trends indicate that over 55% of mid-sized agribusinesses adopted AI-powered crop health monitoring systems in 2025, while 42% of smallholder farms integrated mobile-based irrigation tracking tools.

North America accounted for the largest market share at 37% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22% between 2026 and 2033.

North America maintained dominance due to its extensive deployment of AI-powered machinery and precision agriculture systems across over 250,000 commercial farms, with more than 60% of these farms implementing integrated digital platforms for crop management, irrigation optimization, and predictive analytics. Asia-Pacific is catching up with over 120,000 farms in China, India, and Japan adopting mobile-based AI solutions, while Europe follows with 30% regional adoption driven by sustainable farming policies and precision monitoring initiatives. South America and Middle East & Africa collectively account for 15% of the global market, showing steady adoption in large-scale agricultural export operations and desert agriculture projects.

North America accounts for approximately 37% of the global market share, driven by mechanized commercial farming and rapid adoption of AI-powered crop monitoring platforms. Key industries fueling demand include large-scale grain, corn, soybean, and horticulture production. Regulatory changes such as agricultural modernization grants and farm technology subsidies have encouraged investment in smart irrigation systems and predictive analytics. Technological advancements include deployment of autonomous tractors, IoT-enabled soil sensors, and drone-based crop surveillance. A notable example is John Deere, which has implemented AI-integrated machinery across Midwest farms, improving harvesting efficiency by over 30%. Enterprise adoption is highest in the U.S., with farms leveraging integrated systems to optimize resource allocation and monitor real-time crop health.

Europe holds roughly 28% of the market, with Germany, France, and the UK leading in precision agriculture adoption. Regulatory bodies and sustainability initiatives emphasize reduced chemical use, soil conservation, and digital reporting standards, driving the adoption of explainable AI and automated monitoring platforms. Emerging technologies include AI-powered pest detection, soil nutrient analysis systems, and predictive crop modeling. Local player AgriTech Europe has deployed autonomous drones across 500 hectares in Germany for real-time crop monitoring, improving input efficiency by 25%. European farms exhibit higher regulatory compliance adoption, focusing on explainable AI systems to meet environmental reporting standards.

Asia-Pacific accounts for approximately 20% of the global market volume, with China, India, and Japan being the top-consuming countries. The region’s infrastructure improvements and expanding mobile connectivity support high adoption of AI-powered irrigation, crop monitoring, and mobile farm management apps. Innovation hubs in China and Japan are integrating cloud-based predictive analytics with sensor-enabled farms. A leading local player, Xiaomi Smart Agriculture, has implemented AI-enabled irrigation and monitoring systems in over 10,000 hectares across eastern China, improving water usage efficiency by 28%. Consumer behavior trends indicate strong preference for mobile-based monitoring apps and e-commerce-enabled farm technology solutions.

South America holds approximately 8% of the market, with Brazil and Argentina as the key players. Large-scale commodity farming drives demand for AI-assisted monitoring of soy, corn, and coffee plantations. Infrastructure upgrades in irrigation and energy-efficient machinery support technology adoption. Government incentives such as agricultural modernization grants are increasing AI deployment for yield optimization and pest management. Local player AgroSmart has implemented cloud-based crop monitoring tools on 3,500 farms in Brazil, improving irrigation accuracy by 22%. Consumer adoption patterns indicate strong engagement with digital advisory tools for farm operations, particularly in regions producing export crops.

Middle East & Africa account for roughly 7% of the market, with UAE and South Africa leading adoption. Regional demand is driven by desert agriculture, irrigation optimization, and greenhouse crop production. Technological modernization includes AI-powered water management, drone-based crop monitoring, and IoT-enabled soil sensors. Trade partnerships and local regulations supporting sustainable farming are encouraging investment in smart agriculture systems. A regional example is Desert Farms in UAE implementing AI irrigation solutions across 1,200 hectares, reducing water consumption by 30%. Consumer behavior emphasizes technology adoption for resource optimization and climate-adaptive agriculture practices.

United States - 28% Market Share: High production capacity and widespread adoption of integrated AI platforms drive leadership.

China - 18% Market Share: Strong end-user demand supported by mobile-based AI applications and large-scale farm modernization.

The competitive environment in the Agricultural AI and Digital Farming Solutions Market is robust and increasingly dynamic, featuring a diverse mix of global technology providers, large agricultural OEMs, and specialized agritech innovators. As of 2025, there are over 80 active competitors worldwide, ranging from multifunctional platform providers to niche robotics and sensor developers. The nature of the market remains moderately fragmented, with the top five companies collectively holding approximately 42–47% of the total competitive footprint through widespread platform deployments and broad customer bases.

Leading players are actively pursuing strategic initiatives including cross‑industry partnerships, expanded product portfolios, and platform integrations to maintain competitive positioning. For example, major collaborations involve integrating satellite imagery, machine learning analytics, and autonomous machinery into unified farm management ecosystems, accelerating the pace of innovation. Over 15 significant partnerships and tech alliances were formed between 2023 and 2025, reflecting the intense focus on enhancing digital capabilities and field automation.

Innovation trends driving competition include modular AI analytics, edge computing for real‑time insights, and multimodal sensors that unify weather, soil, and crop data streams. Competitive strategies also emphasize expanding accessibility—smaller farms, cooperatives, and service providers are being targeted through tailored subscription models and developer ecosystems. Annual product launches and upgrades now number over 25 across major players, underscoring the pace of technological change in fields such as autonomous sprayers, predictive pest diagnostics, and integrated supply chain traceability. This competitive landscape demands continual adaptation and investment, making innovation leadership a key determinant of market share and long‑term viability.

Bayer Digital Farming

BASF Xarvio

AGCO Corporation

Topcon Positioning Systems

CNH Industrial

Climate Corporation

Taranis

DroneDeploy

Precision Planting

Yara International

Raven Industries

The Agricultural AI and Digital Farming Solutions Market is defined by a rich ecosystem of current and emerging technologies that are reshaping how farming operations are managed and optimized. AI‑powered analytics remains at the core, enabling real‑time interpretation of vast data sources including satellite imagery, IoT sensor outputs, and climatic patterns to support actionable insights on irrigation, nutrient applications, and pest management. Precision sensor networks deployed across fields now number in the tens of thousands, generating high‑frequency data that informs automated farm equipment and decision support systems.

Autonomous machinery and robotics have evolved from pilot stages into commercial deployments, with self‑navigating sprayers, planters, and crop monitors operating across large farm footprints, reducing dependency on manual labor and increasing consistency. These technologies incorporate machine vision, GPS‑aided navigation, and edge processing to adjust operations on the fly.

Cloud computing and edge AI are converging to improve responsiveness and scalability. Edge AI enables immediate processing of field data for real‑time adjustments, while cloud platforms aggregate historical and regional data to refine predictive models. Lightweight machine learning frameworks tailored for agricultural contexts are enabling localized insights even on modest hardware.

Advanced geospatial analytics—including near‑daily satellite data integrated into farm systems—provide macro and micro views of crop conditions, enabling early detection of stress and disease. Digital twins and simulation tools replicate field scenarios, allowing planners to test interventions virtually before applying them.

Mobile and multilingual advisory platforms are expanding reach into smallholder segments, adapting interfaces to regional languages and conditions to increase usability. Integrating multimodal data, these systems help farmers make science‑backed decisions on crop choice, irrigation scheduling, and risk mitigation. The synergy of these technologies is accelerating farm digitalization, enhancing productivity, sustainability, and resource efficiency across diverse agricultural contexts.

• In November 2025, Syngenta expanded its Cropwise digital platform into an open development ecosystem covering over 70 million hectares of farmland, enabling third‑party developers to build agronomic applications that enhance AI‑driven farm insights. Source: www.syngenta.com

• In September 2025, Syngenta unveiled a suite of AI‑driven agritech innovations focused on predictive crop disease modeling, satellite data analytics, and intelligent irrigation systems tailored for regional challenges, engaging more than 200 developers and engineers in collaborative sessions. Source: www.global‑agriculture.com

• In January 2026, SAP and Syngenta announced a multi‑year technology partnership to embed enterprise‑wide AI and cloud analytics into Syngenta’s operations, modernizing core agricultural processes and enhancing decision support across supply chains and grower services. Source: www.syngenta.com

• In March 2025, Syngenta and Planet Labs expanded their collaboration to deliver near‑daily high‑resolution satellite imagery at 3‑meter resolution to farmers worldwide, enhancing remote crop monitoring, stress detection, and field intelligence capabilities. Source: www.businesswire.com

The scope of the Agricultural AI and Digital Farming Solutions Market Report encompasses a broad and detailed examination of technologies, applications, regional dynamics, and competitive factors shaping the evolution of digital agriculture. It covers technology stacks from AI analytics platforms, autonomous robotics, and machine vision sensors to edge computing frameworks that enable real‑time data processing in the field. The report addresses application layers including precision crop management, automated irrigation, livestock monitoring, supply chain traceability, and multimodal advisory systems that serve both large commercial operations and smaller farming enterprises.

Geographically, the report analyses major regions such as North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing deployment volumes, adoption patterns, infrastructure readiness, and consumer behavior variations in each. It also segments the market by product type—including autonomous machinery, sensor networks, AI analytics engines, and mobile advisory suites—evaluating functional contributions and operational relevance.

The report integrates insights on end‑user categories, spanning large commercial farms, mid‑sized agricultural enterprises, and smallholder growers, highlighting differentiated technology usage patterns, adoption drivers, and support requirements. It identifies emerging niches such as generative AI advisory tools, satellite imagery analytics, and integrated decision support dashboards that blend climatic, soil, and crop health data. Strategic focus areas include innovation trends, ecosystem partnerships, and regulatory impacts that influence technology rollout, interoperability, and data governance practices. Tailored for decision‑makers, the report offers a clear roadmap of market breadth, technological evolution, and practical insights critical for long‑term strategic planning in the digital agriculture domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,370.0 Million |

| Market Revenue (2033) | USD 5,890.7 Million |

| CAGR (2026–2033) | 20% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | John Deere, Trimble Inc., AG Leader Technology, Bayer Digital Farming, BASF Xarvio, AGCO Corporation, Topcon Positioning Systems, CNH Industrial, Climate Corporation, Taranis, DroneDeploy, Precision Planting, Yara International, Raven Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |