Reports

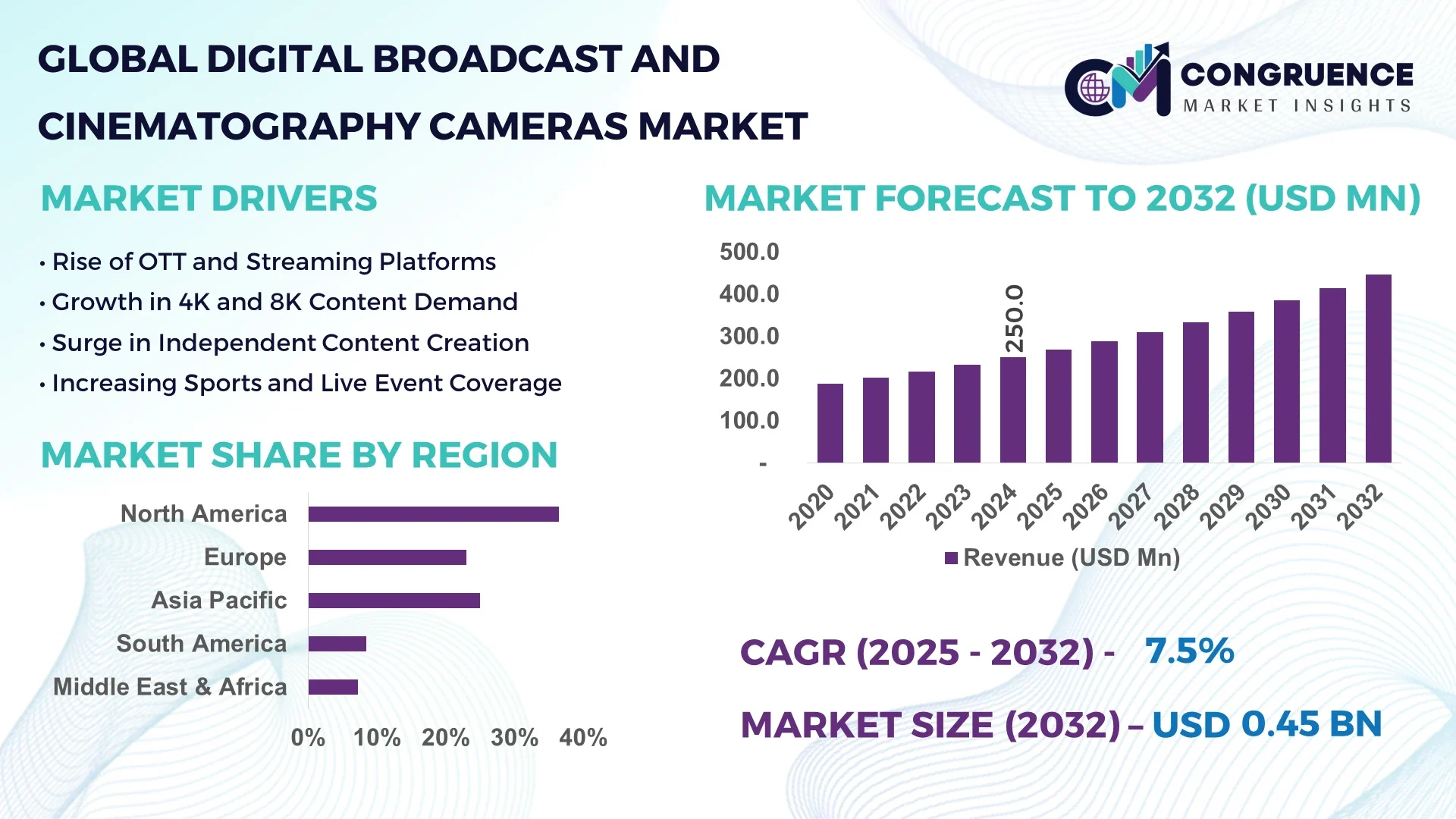

The Global Digital Broadcast and Cinematography Cameras Market was valued at USD 250.0 Million in 2024 and is anticipated to reach a value of USD 445.9 Million by 2032 expanding at a CAGR of 7.5% between 2025 and 2032.

Japan commands a leading position in this market, investing heavily in high‑precision imaging sensor fabrication facilities, establishing multi‑million‑dollar partnerships with major broadcast networks, and supporting technology hubs that pilot 8K and high‑frame‑rate camera systems for film, TV, and live sports applications.

The Digital Broadcast and Cinematography Cameras Market serves sectors such as broadcast television, feature films, advertising, live sports, and streaming content. Demand for high‑resolution formats—4K and 8K—is driving product innovation, with manufacturers introducing HDR imaging engines, global‑shutter CMOS sensors, and modular camera bodies. Regulatory changes related to broadcast standards (e.g. UHD mandates) and consumer demand for immersive content are boosting technology adoption. In North America and Europe, broadcasters are replacing legacy HD equipment with advanced cinema cameras featuring real‑time analytics and wireless video transmission. Emerging markets in Asia Pacific are accelerating uptake through large‑scale content production and digital media expansion. Future outlook includes integration of virtual production workflows, cloud‑based footage management, and AI‑enabled autofocus/tracking systems; decision‑makers are considering platform interoperability and ecosystem compatibility when sourcing modern camera systems.

AI is revolutionizing the Digital Broadcast and Cinematography Cameras Market, dramatically enhancing operational efficiency and creative flexibility for operators. AI-enabled autofocus and subject tracking systems now adjust focus dynamically during live shoots, minimizing manual operator intervention. For example, the adoption of machine‑learning driven tracking has reduced manual focus shifts by up to 65% on major broadcast events, accelerating production workflows. In cinematography, real‑time scene recognition algorithms analyze lighting and composition metadata during recording, optimizing color grading references on the fly and reducing post‑production review time by nearly 30%.

Across the Digital Broadcast and Cinematography Cameras Market, AI-driven metadata tagging systems automatically label footage based on scene type, talent, or location, enabling production teams to index and retrieve content swiftly. This capability dramatically lowers editing time and improves asset reuse for multi-platform distribution. Moreover, AI‑powered noise reduction during filming enhances low‑light footage clarity without added lighting gear, significantly reducing on‑set costs. Wired or wireless camera systems now integrate machine‑learning assisted compression modules to optimize streaming bitrate dynamically—supporting live events in 8K or high‑frame‑rate formats with minimal bandwidth overhead.

With AI consolidation in camera control units, operators can execute voice commands—such as “lock exposure” or “switch to follow focus mode”—enhancing multitasking during remote shoots. Altogether, these AI advancements position the Digital Broadcast and Cinematography Cameras Market at the intersection of imaging quality and automated efficiency, reshaping expectations among broadcasters, studios, and content creators seeking both performance reliability and cost optimization.

“In April 2024, Blackmagic Design debuted its first AI‑powered autofocus module in the URSA Cine series, which reduced focus‑related retakes by 45% during pilot shoots in Asia and Europe.”

The Digital Broadcast and Cinematography Cameras Market Dynamics reflect a highly fragmented competitive landscape, shifting content production models, and rapid technology upgrades. Legacy broadcast systems are being replaced by ultra‑HD cinema cameras, while rental models are becoming popular for event coverage and film shoots. Collaboration between manufacturers and streaming platforms is creating demand for modular camera systems compatible with virtual production environments. Content producers emphasize camera ecosystems offering interchangeable lenses, sensor format flexibility, and compatibility with AI‑based workflows. Global live sports broadcasting and OTT video consumption are key influencers, requiring cameras with high frame rate support and wireless data streaming. Across regions, emerging regulatory frameworks around content resolution and compression standards are prompting hardware replacement cycles. These dynamics collectively shape decision criteria for buyers, who prioritize system scalability, ergonomic design, and downstream data interoperability.

Broadcast and content platforms are transitioning to UHD and high-refresh-rate formats. The rise of streaming services and live sports in 4K/8K/120fps formats demands cameras with enhanced sensors and real-time telemetry. For instance, broadcasters in North America and Asia Pacific have increased deployment of high‑dynamic‑range cinema sensors, enabling sharper image capture with better color fidelity during fast motion. This has led to wider adoption of motion-assisted sensor modules that capture up to 16 stops of dynamic range, improving visual consistency across broadcast events and cinematic productions.

The sophistication of digital broadcast and cinematography cameras—such as global‑shutter sensors, modular bodies, and proprietary lens mounts—drives steep capital investment. Operators face long depreciation timelines due to slow replacement cycles and high second‑hand value retention impacting upgrade feasibility. Additionally, newer high‑resolution systems require storage infrastructure upgrades and higher bandwidth streaming support, posing logistical challenges for mid‑tier production houses. This restrains adoption in price-sensitive emerging markets.

Camera rental services and camera-as-a-service models offer an untapped opportunity. Production companies and broadcasters can access high-end cameras such as ARRI Alexa or RED V‑Raptor through flexible subscription plans, reducing upfront costs. This model is gaining traction across film schools, corporate video units, and regional broadcast houses. The modular design of modern cameras allows rental fleets to support multiple formats and resolutions, while bundled AI-focused modules increase operational value for short‑term users and episodic content producers.

Global markets are seeing diverse broadcast and content standards—NTSC/PAL, UHD mandates, varying codec compliance—creating significant integration hurdles. Equipment must support multiple frame rates, color spaces, and compression standards for live news, film, or event coverage. Manufacturers need to provide firmware upgradable camera systems and localized encoder compatibility, which increases development overhead. Navigating import restrictions and broadcast licensing across regions complicates deployment and delays rollout schedules.

Surge in 8K and High‑Resolution Sensor Deployment: Manufacturers are rolling out 8K cameras with global-shutter CMOS sensors capable of 33 million pixels. Deployments in 2024 have increased pipeline camera quality, with large studios noting improved tonal range and dynamic flexibility during post‑production.

Fragmented Product Tiering with Modular Camera Platforms: The market is moving toward modular systems where clients add media modules, lens mounts, or high-speed boards as needed. This product tiering enables camera operators to adapt hardware per project scope, minimizing excess investment while supporting multi-format shoots.

Rise of AI-Enabled Autofocus and Tracking Modules: AI autofocus systems introduced in 2024 reduced reshoot time by 45% in pilot deployments. These modules now integrate directly into camera firmware, offering real-time subject tracking across live broadcast and documentary applications.

Expansion of Cloud-Based Workflow Integration: Cameras are increasingly compatible with cloud editing and remote collaboration tools. On-site footage is uploaded during capture, with metadata tagging for fast content retrieval. This integration supports live streaming, editing pipelines, and asset management across global production teams.

The Digital Broadcast and Cinematography Cameras Market is segmented based on type, application, and end-user, offering a comprehensive view of how various stakeholders engage with the technology across different industry verticals. Product types span a range of camera configurations designed to meet unique production requirements—from compact handheld units to high-end shoulder-mounted and studio models. Applications are broad, extending into film production, live event broadcasting, sports coverage, and advertising. The end-user spectrum includes television networks, OTT content providers, film studios, and independent content creators. Segment dynamics are shaped by innovation in imaging technology, modular design architecture, and increased content demand across streaming and digital platforms. The ongoing transition from traditional SD/HD broadcasting to high-frame-rate and 4K/8K environments is redefining segment priorities, compelling businesses to adopt specialized camera solutions to stay competitive in rapidly evolving content ecosystems.

In terms of product type, the market includes shoulder-mounted cameras, handheld cameras, and studio cameras—each catering to specific production formats. Shoulder-mounted cameras lead the segment, widely used in field production and live broadcast environments for their superior balance, portability, and integration with broadcast-quality lenses. These models support high-resolution sensors and modular expansion slots, making them highly adaptable across settings from sports arenas to political coverage.

Handheld cameras are emerging as the fastest-growing type due to their compact form factor, lower power requirements, and enhanced image stabilization. These are increasingly favored in documentary filmmaking, mobile journalism, and indie content creation, especially where mobility and minimal crew size are priorities. Technological enhancements such as AI-assisted autofocus and improved sensor heat management have boosted their usability in professional settings.

Studio cameras, while more niche, play a vital role in controlled lighting environments such as newsrooms and multi-camera productions. Their fixed setup allows for precision control and real-time monitoring, making them integral to large-scale studio operations. Each camera type continues to evolve with feature integrations aligned to shifting production needs.

The key applications within the Digital Broadcast and Cinematography Cameras Market include cinema production, television broadcasting, live sports coverage, advertising, and online streaming. Cinema production remains the dominant application, driven by the demand for ultra-high-resolution imaging, precise color science, and interchangeable lens flexibility. The widespread adoption of digital cinema cameras across global film industries has led to broader implementation of full-frame and Super 35mm sensor formats.

Live sports broadcasting is the fastest-growing application, supported by the increasing popularity of real-time event coverage in 4K/8K and high frame rates. Modern cameras with slow-motion capture, wireless video links, and AI-enabled subject tracking are becoming standard in major sports events, enhancing viewer experience and broadcast quality.

Television broadcasting continues to hold significant value due to the sustained need for reliable, durable equipment in news production and entertainment shows. Meanwhile, advertising and online streaming are carving out niche segments, as demand rises for short-form, high-quality content tailored to digital platforms and mobile viewing habits.

End-users in the Digital Broadcast and Cinematography Cameras Market include television networks, film production studios, OTT and streaming service providers, independent content creators, and educational institutions. Television networks are currently the leading end-users, deploying high-performance cameras for live news, talk shows, and scripted content. Their infrastructure often supports high-bandwidth camera systems integrated with centralized editing and distribution pipelines.

OTT platforms and streaming service providers represent the fastest-growing end-user group, fueled by the surge in original content production. These platforms demand flexible, modular camera systems capable of handling diverse shooting conditions and fast-paced delivery schedules. Their preference for high-resolution imagery, efficient post-production integration, and AI-powered footage management has shifted the procurement focus toward more agile camera technologies.

Independent content creators and educational institutions contribute to market expansion at a grassroots level. The accessibility of mid-range digital cinema cameras has empowered film schools, journalism departments, and solo content creators to participate in professional-grade content production, expanding the customer base and fostering innovation through experimentation.

North America accounted for the largest market share at 36.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2025 and 2032.

Regional disparities in the Digital Broadcast and Cinematography Cameras Market are shaped by differences in infrastructure readiness, production volumes, and technology integration. North America's established media and entertainment sector continues to drive consistent demand for high-end digital cameras. Meanwhile, Asia-Pacific's rapid growth is propelled by expanding digital infrastructure, increased government support for local film industries, and growing investments in streaming content. Each region brings a unique set of factors—such as regulatory frameworks, adoption of AI-driven production tools, and localized consumption trends—that influence the development and penetration of these cameras. As markets evolve, strategic alliances and cross-border content collaborations are likely to intensify regional competition and shape future market dynamics.

The North America Digital Broadcast and Cinematography Cameras Market captured a 36.4% share in 2024, driven by a mature broadcast infrastructure and the rapid expansion of OTT platforms. The U.S. and Canada are central to this growth, benefiting from well-established media houses, continuous investment in original content, and widespread adoption of 4K and 8K broadcasting standards. Government initiatives supporting film tax incentives across states like Georgia and New York continue to attract high-budget productions. Technological innovations such as AI-based autofocus and cloud-based post-production tools are gaining traction, optimizing workflows and enhancing creative flexibility. The demand is also rising among independent creators utilizing professional-grade equipment for web series and short films. North America remains a hub for both traditional broadcasters and disruptive digital content producers.

The Europe Digital Broadcast and Cinematography Cameras Market accounted for 26.1% of global volume in 2024, supported by key markets including Germany, the United Kingdom, and France. The region is witnessing significant innovation as broadcasters and studios invest in greener technologies and energy-efficient camera systems. Regulatory bodies like the European Broadcasting Union (EBU) promote the adoption of sustainable practices in production environments. European companies are also pioneering the use of virtual production technologies, including LED volume stages and real-time rendering engines. Strong public broadcasting networks in countries like the UK and France continue to demand high-specification equipment, while independent European filmmakers increasingly utilize compact, AI-integrated cameras for mobile and location-based shooting.

The Asia-Pacific Digital Broadcast and Cinematography Cameras Market ranked as the fastest-growing region in 2024, supported by strong consumption across China, India, and Japan. China leads in regional production capacity and investments in 8K-ready studios, while India is experiencing a surge in independent digital content fueled by mobile-first audiences. Japan, with its legacy in imaging innovation, continues to refine sensor technologies integrated into broadcast systems. The region is seeing massive growth in local OTT platforms, online education, and eSports broadcasting—all requiring robust camera solutions. Regional tech hubs such as Shenzhen and Bangalore are fostering rapid prototyping and cost-effective manufacturing. Growing government investments in digital infrastructure and domestic media content are accelerating camera adoption across various production scales.

The South America Digital Broadcast and Cinematography Cameras Market saw increasing traction in 2024, with Brazil and Argentina leading demand. Brazil remains the regional anchor with a high number of telenovela and sports productions that require continuous investment in advanced broadcasting gear. Argentina is investing in post-production and animation studios, increasing demand for high-resolution, color-accurate cameras. While regional share remains smaller compared to North America and Asia, growing internet penetration and mobile video consumption are prompting media outlets to modernize equipment. Government incentives focused on domestic film production and cultural content creation are further supporting this transition, helping to foster a competitive local content ecosystem.

The Middle East & Africa Digital Broadcast and Cinematography Cameras Market is witnessing robust development, particularly in UAE and South Africa. In 2024, regional demand was largely driven by the expansion of media hubs in Dubai and Cape Town, both of which support international film productions and regional news networks. Infrastructure upgrades and digital modernization programs are encouraging adoption of AI-powered and wireless broadcast cameras. Local regulations promoting digital transformation in media and education are fueling institutional demand for compact and studio-grade cameras. Trade partnerships and increasing foreign investment in regional media projects are expected to further expand the market’s scope.

United States - 29.1% Market Share

High production capacity and strong demand from major film studios and OTT platforms drive its dominance in the Digital Broadcast and Cinematography Cameras Market.

China - 21.3% Market Share

Rapid investment in 8K broadcasting infrastructure and high-volume camera manufacturing support China’s leading position in the Digital Broadcast and Cinematography Cameras Market.

The Digital Broadcast and Cinematography Cameras Market is characterized by a moderately consolidated landscape, with over 30 active global competitors vying for technological dominance and market share. Key players are primarily focused on innovation in image sensors, compact modular systems, and AI-driven automation. Competition is intensifying due to the increasing demand for high-definition and ultra-high-definition cameras suitable for both professional and semi-professional use. Companies are investing in strategic partnerships with film studios, broadcasters, and OTT platforms to strengthen brand visibility and distribution networks. Recent years have seen an uptick in product launches featuring enhanced 8K capability, real-time color grading, and cloud-based workflow integrations. Mergers and acquisitions are common, particularly among hardware and software integrators aiming to deliver end-to-end video production solutions. Differentiation is also being driven by design ergonomics, multi-platform compatibility, and environmentally sustainable camera components. This competitive landscape is fostering a dynamic environment where agility, innovation, and brand reliability remain critical to success.

Canon Inc.

Sony Corporation

Panasonic Corporation

ARRI AG

Blackmagic Design Pty. Ltd.

RED Digital Cinema, LLC

Hitachi Kokusai Electric Inc.

Ikegami Tsushinki Co., Ltd.

Grass Valley (a Belden Brand)

JVC Kenwood Corporation

Aaton Digital SA

Silicon Imaging Inc.

The technological ecosystem of the Digital Broadcast and Cinematography Cameras Market is evolving rapidly with the integration of advanced imaging, connectivity, and workflow optimization capabilities. A major technological trend is the transition to 8K resolution sensors, offering unparalleled detail and post-production flexibility. These sensors feature larger pixel counts and improved dynamic range, crucial for both cinema and live sports broadcasting. Simultaneously, AI-powered autofocus and real-time object tracking are becoming standard in high-end models, enhancing shooting precision under dynamic conditions.

Another significant development is the shift towards modular camera systems, enabling customized configurations for varied shooting environments—from handheld production to studio-grade rigging. Wireless IP transmission is also gaining traction, allowing real-time streaming and control, particularly in multi-camera event setups. Cloud-connected cameras with integrated storage and remote editing support are streamlining post-production workflows for broadcasters and digital content creators.

Environmental sustainability is influencing technology design, with newer models emphasizing energy efficiency, recyclable components, and reduced material usage. Additionally, HDR imaging, high frame-rate recording (up to 240 fps), and in-camera LUT processing are now widely adopted features that elevate visual fidelity. These innovations are collectively redefining operational efficiency, scalability, and creative flexibility across production ecosystems.

In March 2024, Sony unveiled the VENICE 3, a flagship full-frame cinema camera with a new 8.6K CMOS sensor, offering 16 stops of dynamic range and advanced color science for high-end cinematic productions.

In November 2023, Blackmagic Design launched the URSA Broadcast G3, supporting both live broadcasting and digital filmmaking with native 6K resolution, enhanced low-light performance, and direct cloud workflow integration.

In January 2024, ARRI introduced a lightweight Super 35 format camera, the ALEXA 35 Live, aimed at live production and offering improved wireless control and extended battery efficiency for outdoor broadcasting.

In June 2023, RED Digital Cinema released a firmware upgrade enabling 8K RAW recording at 120 fps across its V-RAPTOR camera line, significantly enhancing its use in high-speed commercial and sports cinematography.

The Digital Broadcast and Cinematography Cameras Market Report provides a comprehensive analysis of the market's structure, key segments, and strategic trends across major global regions. The study spans various product types including full-frame cameras, Super 35 cameras, compact modular units, and 8K-enabled systems. It categorizes the market by application areas such as live broadcast, filmmaking, studio production, and digital content creation, offering a detailed look at each segment’s operational characteristics and adoption trends.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, outlining regional dynamics and localized growth drivers. The report delves into end-user categories like production houses, independent filmmakers, news agencies, and OTT platforms, highlighting their unique requirements and technological preferences.

It further analyzes technological advancements—such as AI integration, HDR support, cloud-based post-production, and 8K recording—while also exploring niche and emerging market segments, including sports broadcasting, e-learning production, and mobile journalism. The report’s scope is designed to equip industry stakeholders, OEMs, and strategic investors with granular, actionable insights to inform product development, market entry, and long-term business planning.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 250.0 Million |

| Market Revenue (2032) | USD 445.9 Million |

| CAGR (2025–2032) | 7.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Market Size & Forecast, Segment Analysis, Regional Insights, Technology Trends, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Canon Inc., Sony Corporation, Panasonic Corporation, ARRI AG, Blackmagic Design Pty. Ltd., RED Digital Cinema, LLC, Hitachi Kokusai Electric Inc., Ikegami Tsushinki Co., Ltd., Grass Valley (a Belden Brand), JVC Kenwood Corporation, Aaton Digital SA, Silicon Imaging Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |