Reports

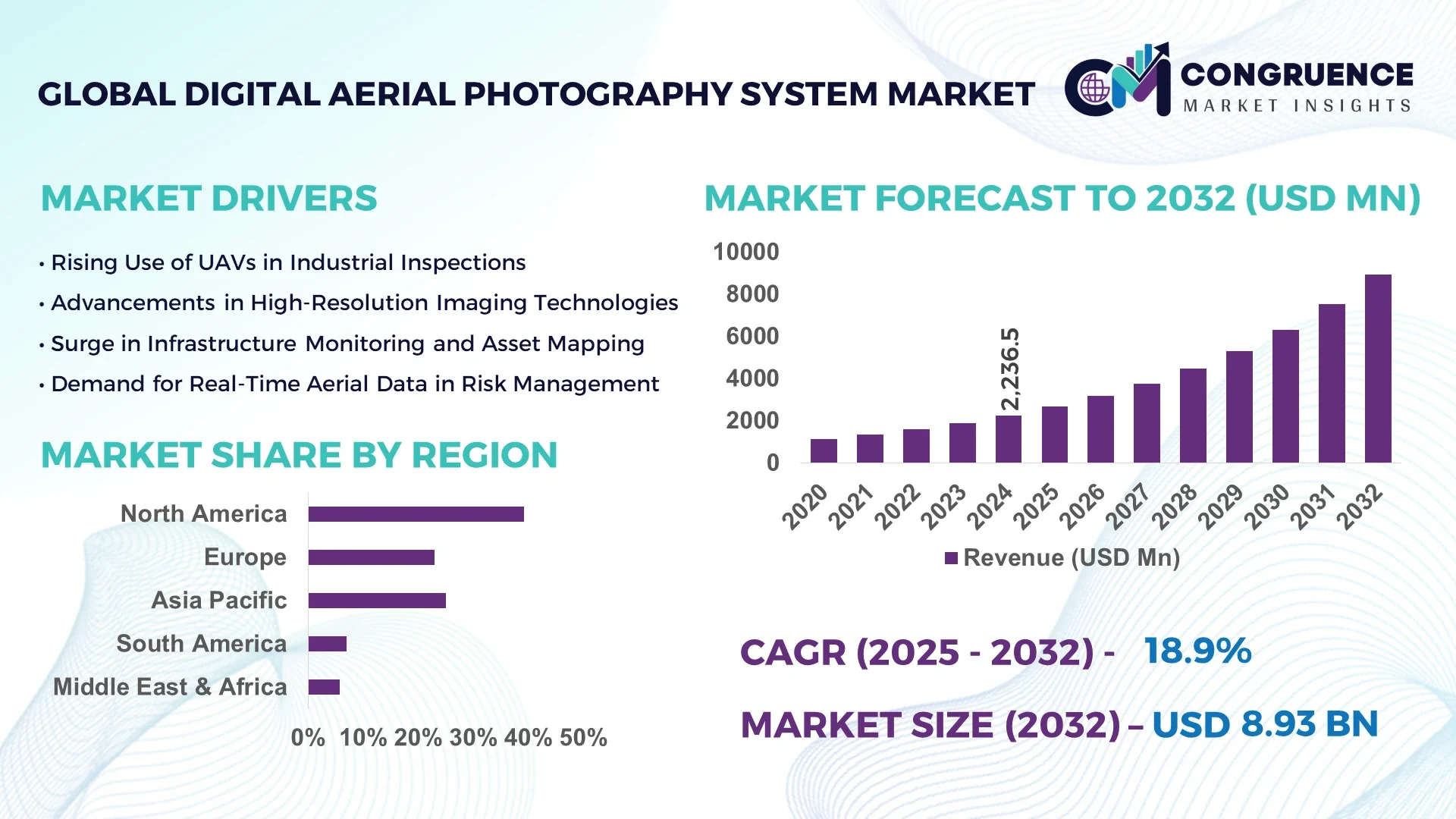

The Global Digital Aerial Photography System Market was valued at USD 2236.5 Million in 2024 and is anticipated to reach a value of USD 8933.57 Million by 2032 expanding at a CAGR of 18.9% between 2025 and 2032.

In the United States, which leads the global landscape in the digital aerial photography system industry, significant investments in geospatial intelligence, high-resolution imaging platforms, and defense-grade surveillance solutions have led to remarkable advances in production capabilities. U.S.-based manufacturers have pioneered scalable aerial imaging technologies integrated with advanced GPS and LiDAR systems across applications including precision agriculture, environmental monitoring, and urban planning.

The Digital Aerial Photography System Market is witnessing substantial growth across sectors such as defense and security, agriculture, construction, mining, and disaster management. These systems are being increasingly adopted for their ability to capture ultra-high-definition orthophotos, thermal maps, and 3D terrain models. Regulatory shifts favoring drone-based imaging in civil aviation frameworks and rapid technological evolution—like integration with AI, real-time cloud syncing, and autonomous navigation—are enhancing operational capabilities. Additionally, economic incentives in emerging markets and sustainability efforts are encouraging the use of aerial imaging in smart city planning and land-use monitoring. Regional consumption is driven by demand in Asia-Pacific and Europe, especially for environmental assessment and infrastructure planning. The future outlook remains positive, with increased focus on long-range imaging drones, multispectral cameras, and AI-powered image processing.

Artificial Intelligence is reshaping the Digital Aerial Photography System Market by enabling automated image recognition, real-time analytics, and enhanced decision-making capabilities across industries. Through AI-powered aerial imaging platforms, organizations can now extract actionable insights from vast volumes of visual data in near real-time, eliminating the traditional reliance on manual interpretation. This has drastically improved operational efficiency, especially in time-sensitive sectors such as emergency response, military surveillance, and infrastructure inspection.

For instance, AI-driven object detection algorithms can now identify damaged rooftops post-natural disasters, detect illegal land encroachments, or monitor crop health through spectral image interpretation. These capabilities allow faster turnaround times, reduce human error, and increase spatial accuracy. Furthermore, AI-based path planning and obstacle avoidance systems enable autonomous drones to execute complex aerial surveys without manual intervention. This has been especially valuable in hard-to-reach terrains and high-risk industrial zones.

AI is also advancing image stitching and 3D reconstruction processes, which are critical for construction site modeling, mining evaluations, and archaeological mapping. In agriculture, AI-integrated aerial photography systems now assess soil health, detect pest infestations, and estimate yield with precision, transforming conventional farming practices. As industries increasingly integrate aerial intelligence with AI workflows, the Digital Aerial Photography System Market is poised for data-driven optimization and scalable deployment across diverse operational landscapes.

“In early 2024, a U.S.-based geospatial tech company deployed an AI-enhanced aerial photography system capable of processing over 3,000 high-resolution images per hour, reducing manual image sorting time by 75% and enabling real-time wildfire boundary mapping in California.”

The surge in unmanned aerial vehicle (UAV) deployments across both public and private sectors has become a crucial driver for the Digital Aerial Photography System Market. Governments are integrating drone-based imaging systems for surveillance, land mapping, and disaster response, while private industries are using them for real estate surveys, crop monitoring, and infrastructure inspections. According to industry figures, UAV usage in civil and commercial operations grew by over 25% between 2023 and 2024, directly boosting demand for integrated aerial photography systems. The versatility of drones, combined with advanced imaging sensors, enables data acquisition in hard-to-reach and large-scale areas without the need for costly manned aircraft operations. This efficiency, along with improved data precision and real-time streaming capabilities, continues to expand UAV-based aerial imaging deployments worldwide.

One of the significant restraints in the Digital Aerial Photography System Market is the complex regulatory environment surrounding airspace use and individual privacy rights. Various countries enforce strict drone flight limitations, altitude restrictions, and licensing protocols that can delay or inhibit aerial imaging operations. For instance, in several European Union member states, new GDPR-compliant rules have been introduced to address public surveillance and data protection, affecting drone-based image collection in urban areas. Moreover, in high-security zones or near airports, UAV deployment often requires multi-tiered approvals, significantly increasing operational lead times. Concerns over unauthorized data collection and potential misuse of sensitive imagery further compound the issue, necessitating strong compliance frameworks that add operational burdens and restrict market scalability in sensitive or densely populated areas.

The integration of artificial intelligence and edge computing technologies presents a major opportunity in the Digital Aerial Photography System Market. Edge-enabled aerial photography systems allow immediate data processing directly on the device, enabling faster insights without depending on cloud infrastructure. This is especially impactful for time-sensitive operations like disaster response, traffic monitoring, and precision agriculture. AI-based software enhances object recognition, predictive analysis, and anomaly detection, transforming static images into dynamic intelligence. As per 2024 industrial deployment reports, the use of edge-AI modules in aerial imaging platforms improved analysis turnaround by 60%, reducing reliance on data centers. This integration allows for enhanced autonomy, scalability, and localization in decision-making, opening avenues for deployment in remote or connectivity-constrained environments and expanding the scope of real-time geospatial intelligence solutions.

Despite technological advancements, the high upfront costs of digital aerial photography equipment remain a substantial barrier to widespread adoption, particularly in low-income or developing regions. Advanced aerial cameras, multispectral sensors, and drone systems require significant investment, often exceeding the budget capabilities of small enterprises or municipal bodies. Additionally, the need for skilled operators, data analysts, and system maintenance adds to the total cost of ownership. As a result, critical sectors such as rural land mapping, agricultural planning, and ecological conservation in developing nations struggle to access these advanced solutions. Furthermore, insufficient digital infrastructure and lack of government support limit the deployment of aerial imaging technologies, reinforcing the digital divide and slowing market penetration outside of economically advanced regions.

Increased Demand for High-Resolution Imaging in Precision Agriculture: The use of digital aerial photography systems in precision agriculture has surged due to the growing need for accurate crop monitoring, yield prediction, and soil health analysis. Multispectral and hyperspectral imaging technologies are being employed to detect nutrient deficiencies, pests, and irrigation issues. In 2024 alone, over 35% of large-scale farming operations in the U.S. Midwest integrated aerial imaging platforms into their seasonal cycles. This trend is being reinforced by smart farming initiatives and government incentives supporting advanced agri-tech deployments.

Adoption of Real-Time Geospatial Intelligence in Emergency Response: Emergency services and disaster response agencies are increasingly turning to aerial imaging systems for real-time assessment of crisis zones. From wildfire mapping to flood impact analysis, the ability to rapidly gather and process visual data is proving critical. In 2025, more than 60 regional emergency response teams in Europe adopted drone-based digital aerial photography tools equipped with AI-based scene recognition, resulting in faster decision-making and safer deployments.

Integration with Smart City Infrastructure Development Projects: Digital aerial photography systems are playing a vital role in smart city infrastructure planning. Urban planners are leveraging high-resolution aerial imagery to map utilities, monitor traffic patterns, and assess construction progress. In Asia-Pacific, over 50 metropolitan areas utilized aerial imaging platforms to support real-time urban analytics and optimize transport grids in 2024. This trend is being driven by increased investment in urban digitization and sustainable development.

Miniaturization and Cost-Reduction of Imaging Payloads: Recent advancements in optics and electronics have enabled the development of compact, lightweight imaging payloads suitable for smaller UAVs. These innovations are significantly reducing deployment costs and making digital aerial photography accessible to a wider range of users, including small businesses and academic institutions. As of early 2025, new camera modules weighing under 200 grams can now deliver 4K-resolution images, a shift that's expanding the market for short-range and tactical applications.

The Digital Aerial Photography System Market is segmented based on type, application, and end-user, reflecting a diverse range of operational requirements and technological deployments. From fixed-wing and rotary drones to manned aircraft systems with integrated high-resolution cameras, each type fulfills a specific niche. Application-wise, the market spans from precision agriculture and environmental monitoring to construction site planning and defense intelligence. Different end-users—ranging from government agencies and private enterprises to academic research institutions—utilize these systems based on operational scale and data needs. Technological integration, particularly with AI and GIS platforms, is further diversifying usage scenarios. This segmentation reflects a market that is rapidly evolving in both scope and sophistication, adapting to dynamic global demands in imaging precision, real-time data analysis, and aerial mobility.

The market includes various types of digital aerial photography systems such as fixed-wing aircraft systems, rotary-wing UAVs, balloon-based platforms, and manned helicopter systems. Among these, fixed-wing UAVs lead the market due to their extended flight endurance and suitability for large-area surveys. These systems are widely used in environmental studies and agricultural mapping where broader coverage is essential. The fastest-growing type is rotary-wing UAVs, driven by their maneuverability and ease of deployment in urban and congested areas. Their vertical takeoff and landing capability makes them ideal for real estate, construction site inspection, and emergency response imaging. Balloon-based platforms are niche but useful in atmospheric studies and long-duration surveillance. Manned helicopters still find use in high-risk zones requiring heavy imaging equipment. As drone regulations become more favorable and imaging payloads become lighter, rotary-wing UAVs are expected to grow in utility across civilian and commercial applications.

The Digital Aerial Photography System Market serves a wide range of applications including precision agriculture, environmental monitoring, urban planning, infrastructure development, and disaster management. Precision agriculture is currently the leading application due to its reliance on multispectral aerial data to improve crop health, water efficiency, and field productivity. The fastest-growing application is disaster management, fueled by the need for real-time data to assess damage, coordinate rescue efforts, and monitor hazard progression. Environmental monitoring continues to hold strong demand, especially in regions implementing carbon footprint tracking and deforestation control. Urban planning and smart infrastructure development are also rising as cities integrate aerial intelligence to optimize traffic flow, monitor urban sprawl, and manage utilities. Construction firms are increasingly incorporating digital aerial photography systems into project lifecycle management to improve accuracy in site surveys and progress tracking.

Government and defense agencies dominate the end-user landscape in the Digital Aerial Photography System Market due to their extensive use in surveillance, border monitoring, and large-scale mapping projects. Their adoption of high-resolution aerial photography is essential for national security, geospatial intelligence, and disaster mitigation planning. The fastest-growing end-user segment is private commercial enterprises, including construction firms, agribusinesses, and logistics providers. These organizations are adopting digital aerial imaging for project management, resource optimization, and supply chain mapping. Academic and research institutions also form a notable segment, leveraging aerial systems for environmental research, archaeological exploration, and climate change studies. Meanwhile, non-governmental organizations (NGOs) are increasingly using drone photography for humanitarian missions and environmental advocacy, especially in remote regions. The diversity of end-user needs is driving innovation in system design, operational software, and image analytics across global markets.

North America accounted for the largest market share at 39.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22.1% between 2025 and 2032.

North America's leadership is underpinned by established defense, construction, and agricultural sectors integrating advanced aerial imaging for precision mapping and surveillance. Meanwhile, Asia-Pacific’s rapid infrastructure growth and increasing government investments in smart city and environmental monitoring projects are fueling its accelerated expansion. Across all regions, rising demand for high-resolution data and real-time geospatial intelligence is redefining the landscape of the Digital Aerial Photography System Market. The market’s regional evolution reflects dynamic geopolitical priorities, regulatory advancements, and technological innovation ecosystems that are increasingly influencing procurement and deployment patterns.

Expanding Industrial Applications Drive Imaging Technology Adoption

In 2024, this region held a commanding 39.2% market share, driven primarily by advanced defense contracts, real estate development, and precision agriculture applications. The integration of digital aerial photography systems in disaster management and climate monitoring has expanded, especially in wildfire-prone states. The Federal Aviation Administration’s ongoing updates to commercial drone regulations have made it easier for businesses to deploy UAVs for aerial data capture. Technological upgrades, including AI-driven image analytics and real-time data streaming platforms, are being rapidly adopted by U.S.- and Canada-based enterprises. These digital transformation efforts, coupled with strong federal and state-level funding in geographic information systems (GIS), are sustaining robust demand in both public and private sectors.

Environmental Monitoring and Smart Infrastructure Planning Fuel Demand

Europe represented approximately 26.4% of the global market in 2024, led by strong adoption across Germany, France, and the United Kingdom. These countries are using aerial photography systems extensively for sustainable urban planning, infrastructure modernization, and precision agriculture. The European Union's Green Deal and satellite-data integration initiatives are pushing local agencies to complement satellite imagery with drone-based aerial intelligence. Technological investments in AI and 3D mapping across France and Germany are enabling more accurate terrain modeling and land-use optimization. Regulatory support from EASA and other regional bodies is streamlining drone deployment frameworks, promoting broader use of advanced imaging systems across civil, environmental, and commercial sectors.

Infrastructure Boom and Smart Urbanization Accelerate Imaging Adoption

Asia-Pacific recorded the fastest regional growth in 2024 and ranked second in total volume, largely due to heavy investment in infrastructure development across China, India, and Japan. China, a dominant player, utilizes aerial photography systems for large-scale construction, mining, and environmental inspections. India has intensified drone usage in agriculture and rural development under national digitization schemes. Japan, leveraging its advanced tech landscape, is integrating AI-based image analytics for disaster resilience and urban management. Regional tech hubs like Shenzhen and Bengaluru are driving innovation in lightweight imaging sensors and automated data processing systems. This ecosystem of manufacturing strength, government backing, and technological advancement is rapidly propelling the region’s market performance.

Government Infrastructure Projects and Environmental Policies Drive Usage

Brazil and Argentina are the primary contributors to this region’s modest but expanding digital aerial photography system market, which represented around 4.6% of global share in 2024. Brazil has initiated aerial surveillance programs to combat illegal deforestation and monitor agricultural zones, while Argentina is utilizing UAV imaging for energy infrastructure assessments and land-use planning. Ongoing infrastructure reforms, coupled with improvements in digital connectivity, are encouraging adoption of high-resolution imaging systems. Government-backed trade incentives for smart agriculture technologies have also enhanced commercial use. Additionally, local drone manufacturers are beginning to emerge, enabling more affordable system deployment for smaller enterprises.

Geospatial Intelligence for Energy and Urban Growth Supports Market Demand

Countries like the UAE and South Africa are leading regional growth, driven by demand in oil & gas, construction, and smart urban development. In 2024, this region accounted for nearly 3.8% of global market volume. The UAE is leveraging aerial imaging systems for pipeline inspection, urban infrastructure mapping, and environmental protection projects. South Africa’s mining and agriculture sectors are adopting drone-based aerial photography for better operational efficiency and monitoring. Technological modernization initiatives, such as the integration of AI in surveillance systems and cloud-based geospatial platforms, are advancing rapidly. Regional collaborations and trade partnerships are further strengthening aerial imaging capabilities across Africa and the Middle East.

United States – 32.5% market share

High production capacity, widespread enterprise adoption, and strong military and civil infrastructure programs support dominance in the Digital Aerial Photography System Market.

China – 18.6% market share

Rapid infrastructure development, smart city investments, and large-scale agricultural digitization drive significant demand in the Digital Aerial Photography System Market.

The Digital Aerial Photography System market is characterized by a dynamic and evolving competitive landscape, with over 70 active participants globally, ranging from specialized drone manufacturers to enterprise-level geospatial intelligence providers. Market competition is intensifying due to rapid technological advancements in imaging sensors, AI-driven analytics, and UAV integration. Leading firms are focusing on developing compact, lightweight camera systems and scalable software platforms that deliver real-time geospatial insights. Strategic partnerships and joint ventures between aerospace firms and tech companies have become increasingly common, aimed at combining imaging hardware with cloud-based data solutions. In 2024, several firms launched multispectral and hyperspectral imaging platforms tailored for applications in precision agriculture and infrastructure planning. Product differentiation is a major competitive strategy, with players investing in 4K and 8K resolution cameras, edge computing integration, and AI-enhanced analytics modules. Companies are also expanding geographically, targeting emerging markets in Asia-Pacific and South America where infrastructure growth is fueling aerial imaging demand. Furthermore, compliance with evolving drone regulations and development of software with GDPR and data localization features have become critical to maintaining competitive positioning. This competitive environment reflects a high degree of innovation, collaboration, and market responsiveness, which continues to shape the future trajectory of the Digital Aerial Photography System market.

DJI Innovations

Phase One

Trimble Inc.

Hexagon AB

Teledyne FLIR LLC

Parrot Drones SAS

AeroVironment Inc.

AgEagle Aerial Systems Inc.

senseFly (a Wingtra AG company)

Quantum Systems GmbH

The Digital Aerial Photography System Market is undergoing rapid technological evolution driven by advancements in sensor resolution, autonomous flight capabilities, and data processing efficiency. Imaging sensors have progressed from traditional RGB to multispectral, hyperspectral, and thermal technologies, enabling deeper analytics across agriculture, mining, and environmental monitoring sectors. New imaging payloads now offer ultra-high-definition (UHD) resolutions up to 8K and integrate advanced stabilization features for clearer, distortion-free data acquisition, even in turbulent air conditions.

Autonomous flight systems have improved with real-time kinematic (RTK) GPS and inertial measurement units (IMUs), enhancing positional accuracy for survey-grade mapping. Additionally, integration of AI and edge computing has allowed onboard processing of image data, reducing reliance on cloud infrastructure and speeding up operational workflows. AI algorithms can now detect anomalies, classify land use, and generate 3D models in near real-time.

Software platforms have also evolved to support end-to-end data management, from flight planning to post-processing. GIS integration, cloud-based data repositories, and real-time collaboration tools are enabling multi-sector enterprises to manage large aerial datasets effectively. Emerging technologies, such as LiDAR and photogrammetry fusion, are being tested for high-fidelity topographic mapping, especially in urban planning and infrastructure maintenance. Collectively, these innovations are elevating both the accessibility and performance of digital aerial imaging systems worldwide.

In February 2024, DJI unveiled its Zenmuse L2, a high-precision LiDAR and RGB camera system designed for drones, enhancing 3D mapping and offering improved penetration through vegetation, ideal for forestry and infrastructure projects.

In August 2024, Teledyne FLIR introduced the Boson+ thermal imaging camera core with significantly enhanced sensitivity and resolution, enabling superior performance in nighttime and low-visibility aerial surveillance missions.

In October 2023, Quantum Systems launched Trinity Pro, a fixed-wing UAV optimized for high-endurance aerial photography missions. The system integrates real-time kinematic positioning and advanced image stitching software for precise land surveys.

In December 2023, Phase One announced the release of PAS 280i, a large-format aerial camera system designed for country-wide mapping projects, featuring a 280-megapixel sensor and improved flight efficiency.

The Digital Aerial Photography System Market Report provides an extensive analysis of market components segmented by type, application, end-user industry, and region. Types analyzed include fixed-wing UAVs, rotary-wing drones, manned aircraft systems, and tethered platforms equipped with high-resolution imaging sensors such as RGB, multispectral, and thermal cameras. Applications span across sectors including precision agriculture, infrastructure planning, environmental monitoring, disaster response, defense intelligence, and urban development.

The geographic scope encompasses key regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with further insights into top-performing countries like the United States, China, Germany, and India. The report evaluates technology adoption rates, investment in R&D, regulatory frameworks, and end-user behavior across these territories.

Additionally, the report identifies emerging areas such as AI-integrated aerial imaging, real-time data analytics, and autonomous drone deployment. Niche market trends—such as balloon-based aerial photography for climate research or drone-enabled inspections in renewable energy projects—are also covered. Focused on actionable insights for business stakeholders, the report provides a forward-looking view of market trajectories, enabling informed decision-making across strategic planning, technology development, and market entry strategies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2236.5 Million |

|

Market Revenue in 2032 |

USD 8933.57 Million |

|

CAGR (2025 - 2032) |

18.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM Corporation, Siemens AG, GE Vernova, ABB Ltd., SAP SE, Emerson Electric Co., Bentley Systems Incorporated, Oracle Corporation, DNV AS, Aspen Technology Inc., Schneider Electric SE, Fluke Corporation, IFS AB, AVEVA Group plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |