Reports

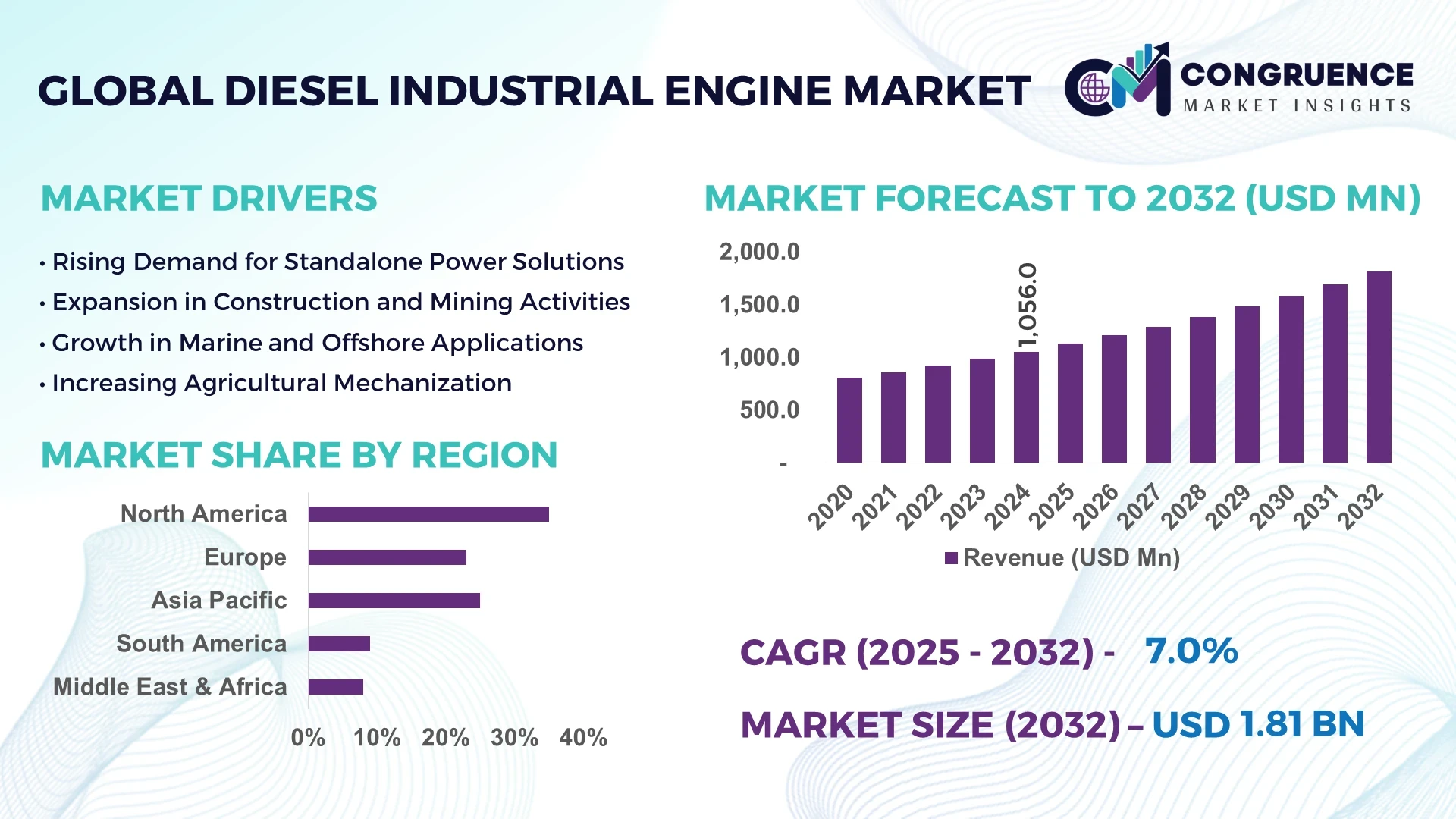

The Global Diesel Industrial Engine Market was valued at USD 1,056.0 Million in 2024 and is anticipated to reach a value of USD 1,814.4 Million by 2032 expanding at a CAGR of 7% between 2025 and 2032.

In this segment, China leads the global marketplace, with its extensive industrial manufacturing base and robust infrastructure development. Chinese manufacturers dominate by supplying high-capacity diesel engines for power generation, mining, and construction, catering to both domestic demand and large export markets.

In India, the Diesel Industrial Engine Market is gaining momentum, driven by accelerating rural electrification, expanding construction projects, and growing demand for diesel gensets. Manufacturers are increasingly adopting advanced control systems and localized production to reduce costs. There is also rising usage in agricultural irrigation pumps and remote industrial setups, where grid connectivity remains unreliable. This diversification across end‑use sectors is boosting sales volumes and encouraging enhancements in engine efficiency and after‑sales services.

AI is dramatically reshaping the Diesel Industrial Engine Market by enabling factories and fleet operators to drive efficiency, reliability, and performance to new heights. Through predictive maintenance, AI platforms continuously monitor sensor data—vibration, temperature, pressure, and exhaust composition—to forecast anomalies and schedule proactive repairs, drastically reducing unplanned downtime and maintenance costs. Meanwhile, AI-driven combustion optimization systems analyze real-time operating conditions to fine‑tune fuel injection, timing, and air‑fuel mix, resulting in smoother performance and lower emissions.

Another game-changer is the use of digital twins, virtual engine replicas powered by AI and IIoT. These twins simulate engine behavior under diverse scenarios—load changes, environmental conditions, or wear‑and‑tear—allowing engineers to optimize engine control strategies and diagnostics remotely. As a result, engine lifecycle reliability has significantly improved across gensets, marine diesel units, and heavy‑duty applications.

In fleets, AI-enabled DPF regeneration monitoring tools analyze filter soot levels and regeneration cycles, alerting operators when forced regeneration is necessary. This ensures optimal filter performance, reduces fuel penalties, and extends part lifespan. Such solutions are already deployed by logistics and mining companies to maintain fleet productivity and compliance.

AI also enhances manufacturing quality through automated defect detection, using computer vision to inspect engine components for cracks, misalignments, or casting flaws—ensuring higher build standards and reducing rejects.

With supply‑chain intelligence, AI systems forecast spare‑parts demand and optimize inventory stocking across regional service centers. Manufacturers can now anticipate demand spikes, avoid stockouts, and cut excess warehousing costs, improving service readiness and customer satisfaction.

Taken together, these AI‑infused innovations are transforming the diesel industrial engine sector into a smarter, more efficient ecosystem—fueling reliability, performance, and sustainability gains for operators worldwide.

"On April 7, 2025, Cummins announced at Bauma 2025 the global release of its enhanced PrevenTech® platform—an AI-driven remote monitoring and predictive analytics solution designed for mining diesel engines. Across two mine sites with 340 PrevenTech‑equipped engines in 2024, the platform prevented over 45 hours of downtime and saved approximately USD 70,000 per engine in maintenance and repair costs."

The surge in industrial automation, remote mining projects, and infrastructure development across Asia and Africa has escalated demand for diesel engines with extended durability and remote operability. Engine makers are responding with robust units featuring advanced filtration, enhanced thermal management, and remote telemetry. Over the past 18 months, sales of 500+ kVA gensets equipped with remote monitoring climbed by nearly 25% in these regions, reflecting rising off‑grid power resilience requirements and reduced on-site visitation needs.

Tightening emissions standards (e.g., EU Stage V, EPA Tier 4, Bharat Stage VI) require engines to incorporate after-treatment systems like SCR and DPF. This has increased production complexity and costs. More than 60% of newly sold industrial engines in developed markets now include these systems. Buyers often delay upgrades due to higher capital and maintenance expenses. For small-scale engine users in emerging economies, compliance costs have increased average purchase prices by 15–20% in the last two years.

There’s growing interest in engines capable of running on diesel and alternative fuels such as methanol or hydrogen. Dual-fuel engines enable significant emission reductions and lower reliance on diesel. Tier-1 OEMs have introduced retrofit kits for 175D-class engines to run on methanol blends. Within 12 months, pilot dual-fuel gensets in Europe achieved up to 30% drop in CO₂ output, and retrofit kit inquiries rose by 40% among power-generation contractors.

Global supply chains continue to face volatility due to geopolitical tensions, semiconductor shortages, and raw material constraints. For instance, shipments of crankshafts and turbochargers were delayed by 3–4 months in Q1 2025. OEMs have resorted to buffer inventories, driving up costs by an average of 12%. In India, engine delivery backlogs reached 6–8 weeks in early 2025, impacting project timelines and rental fleet availability.

Shift Toward Modular and Prefabricated Engine Units: Demand is increasing for modular engine packages—self-contained diesel gensets with integrated control panels, exhaust, and sound attenuation—optimized for plug-and-play deployment. In North America and Europe, the modular genset market grew nearly 18% in 2024, driven by data center power and rental applications. Prefabricated units reduce installation time by up to 40% and standardize quality, boosting appeal among rental service providers and emergency responders.

Growth of Digital Twin–Based Lifecycle Management: Manufacturers and end-users are adopting digital twin solutions to simulate engine behavior through design, operation, and maintenance. This enables precise predictive insights, reducing component wear and lifecycle costs. In 2024, digital twins were used in over 20% of newly commissioned industrial engines above 800 kW. The resulting predictive maintenance schedules have lowered unplanned downtime by around 15%, according to case studies in Europe and Asia.

Emergence of Compact, High‑Efficiency Engines: OEMs are introducing compact, high‑power‑density engines—for example, 53% thermal efficiency models launched in 2024 reduce fuel consumption by 10–14%. These engines are optimized for mining, marine, and rail sectors, providing similar outputs in smaller footprints. The advanced thermal performance allows fleet operators to reduce fuel expense and greenhouse gas intensity, aligning with corporate sustainability goals.

AI‑Enabled Filtration and Emissions Control: Beyond predictive maintenance, AI is increasingly applied in active emissions control. Intelligent filtration systems track particulate loading and adjust regeneration cycles dynamically. One 2024 pilot with fleets using AI‑powered DPF modules saw increased regeneration efficiency and reduced operator intervention. Deployment rates of such systems grew by over 30% across North American commercial fleets last year, improving uptime and emissions compliance.

The Diesel Industrial Engine Market is categorized across three fundamental dimensions: type, application, and end‑user. Each segment reveals unique dynamics shaped by performance needs, regulatory environments, and technological trends. Manufacturers tailor their offerings—from high-speed portable units to robust stationary engines—to meet diverse requirements in power generation, construction, marine, agriculture, and mining. This granularity helps stakeholders understand demand drivers, growth pockets, and competitive pressures. Regional preferences also play a major role—while developing economies lean toward affordable, indigenous engine types, advanced markets prioritize compliance-ready and ultra-efficient models. Against this backdrop, we provide an in-depth look at each segmentation axis and the key performers driving market evolution.

The market is split into high-speed diesel engines (<1000 RPM), medium-speed engines (1000–3000 RPM), and low-speed engines (<300 RPM). As of 2024, high-speed engines are the dominant segment, accounting for approximately 52% of the installed base. Their popularity stems from compact designs, cost efficiency, and ease of integration in mobile and standby power systems. High-speed models also saw around 12% year-over-year volume growth in portable gensets and irrigation pumps. Medium-speed engines represent roughly 30% of the market and are the fastest-growing segment, expanding at an estimated 14% annual pace. Growth is driven by rising demand in industrial power generation, mid-capacity marine drives, and hybrid power systems. These engines bridge performance and size, making them ideal for remote site applications with load variability. Low-speed engines, while more niche, serve heavy-duty marine propulsion and base-load power requirements. Their share is around 18%, but growth remains steady at 6–7%, supported by infrastructure projects and large ships requiring high torque and longevity. However, capital intensity and longer manufacturing lead times limit faster expansion compared to medium-speed units.

Applications of diesel industrial engines cover power generation, construction and mining equipment, marine propulsion, oil & gas, and agricultural machinery. In 2024, power generation emerged as the leading application, responsible for about 45% of global engine sales. Backup power for data centers, hospitals, telecom towers, and remote installations drove this segment, with shipment volumes increasing by nearly 10% compared to 2023. The construction and mining equipment segment accounted for approximately 25% of the market. These engines power excavators, loaders, and drills. Demand growth, paced at around 9% annually, aligns with global infrastructure expansion in developing regions where diesel remains the parsimonious choice over electric alternatives. Marine propulsion holds roughly 15% of the share, supported by coastal and inland vessel operations. Growth of about 7% is influenced by new emission norms encouraging engine retrofits and replacements. Oil & gas sectors account for close to 8%, supplying engines for drilling rigs, compressors, and generators; this niche grows at about 6% owing to fluctuating upstream activities. Finally, agricultural machinery constitutes around 7% of the market, driven by irrigation pumps and compact tractors, growing near 8% as mechanization spreads in emerging economies.

End‑users of diesel industrial engines include industrial OEMs, power infrastructure operators, rental & leasing companies, and government/public utilities. In 2024, power infrastructure operators dominated double-digit market purchases, capturing nearly 40% of sales by volume. Their ongoing requirement for reliable grid support and demand-side continuity—with units rated from 500 kVA to multi-MW—continues to fuel orders and long-term contracts. Industrial OEMs, which integrate engines into heavy machinery, accounted for roughly 25% of demand. Growth rose by around 11% year-over-year, as advanced hydraulic systems and factory automation rolled out in manufacturing and material handling. Rental & leasing companies formed about 20% of the market, with approximately 15% growth in units deployed during peak construction seasons. Their flexibility and CapEx avoidance appeal to temporary infrastructure projects and event power markets. Government and public utilities made up the remaining 15%, relying on diesel units for emergency backup and rural electrification schemes. Installation growth hovered at 8%, driven by regional electrification pushes and rural resilience programs, particularly in Southeast Asia and Sub-Saharan Africa. The balance across end-users demonstrates a strong tilt toward critical infrastructure players, with rental markets gaining rapid momentum from temporary project cycles.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2025 and 2032.

In 2024, Asia-Pacific captured roughly US $370 million in diesel industrial engine sales due to booming infrastructure, agriculture mechanization, and strong mining activity. North America held about 28% share, with significant use in backup power and rental fleets. Europe maintained close to 20% share, driven by regulatory compliance and industrial upgrades. Middle East & Africa and South America leveled up the remaining 17%, bolstered by remote-site construction and energy projects. Looking ahead, Asia-Pacific’s industrial expansion and push toward rural electrification position it for high growth, while North America and Europe will continue steady modernization.

North America’s diesel industrial engine market is witnessing a surge in modular, easy-to-deploy gensets tailored for data centers, hospitals, and telecom backup. In 2024 alone, shipments of plug-and-play 750–1500 kVA gensets increased by nearly 14% compared to the previous year. Additionally, rental fleets for large events and construction sites expanded their diesel-powered capacity by approximately 10%, driven by post-pandemic logistics rebound. The region also saw rising investment in remote telemetry systems across utility fuel stations and oilfields, with installations of onboard sensors jumping by roughly 18%.

Europe is advancing toward cleaner and more efficient diesel engines in light of stringent emissions mandates. Industrial engine producers introduced 1200+ units with SCR and low-NOx outputs in 2024, representing a 9% increase in ultra-low emission orders. Meanwhile, remote industrial installations deployed filtration and AI-based regeneration modules across 40% of newly commissioned gensets. Demand for compact medium-speed units—used in hybrid energy setups—rose 11%, especially in offshore applications. Additionally, there was a 7% year-on-year increase in marine retrofit orders replacing older low-speed engines to comply with Stage V requirements.

Asia-Pacific is undergoing a diesel-engine surge fueled by rural grid-connectivity gaps, large irrigation demands, and infrastructure projects. Sales of small-to-mid-capacity (<750 kVA) gensets rose about 16% in 2024, with strong uptake across India, Southeast Asia, and Indonesia. Mega-projects like rail, ports, and mining contributed to a 13% growth in medium-speed engine deployments in Australia and China. India and Vietnam witnessed a 14% hike in agricultural pump engine sales, while OEMs ramped up localization, boosting regional diesel engine assembly volumes by nearly 20%.

South America’s diesel industrial engine market continues to grow in lockstep with mining and remote electrification. In 2024, diesel gensets for mining operations increased by approximately 12%, especially in Chile and Peru, where off-grid remote mines adopted higher-capacity modules. Agricultural demand in Brazil and Argentina drove small-engine sales up by about 9%. Rental fleets serving temporary infrastructure and event power saw an 11% boost. Regional engine manufacturers reported filling production gaps, with mid-speed engine capacity expanding by 15% to accommodate local delivery timelines.

In the Middle East & Africa region, diesel engines are at the core of power solutions, especially for oil & gas, construction, and rural electrification. In 2024, oilfield genset deployments rose by around 13%, particularly in Nigeria and Saudi Arabia. Infrastructure projects across the UAE and South Africa led to a 10% increase in medium-speed engine orders. On-grid backup demand for hospitals and telecom infrastructure climbed by 8%. Remote tracking and telematics installations reached 30% penetration in new units, driven by desert site management requirements. Manufacturers adapted with robust cooling systems and high-capacity air filtration to suit harsh climates, resulting in ~15% adoption of climate-benchmarked engine specifications.

China – ~20% share, led by strong infrastructure, construction, and manufacturing sectors.

United States – ~18% share, driven by data center growth, rental fleets, and backup power systems.

The global diesel industrial engine market is intensely competitive, with key players striving to balance performance, technological integration, and regulatory compliance. Major firms such as Cummins, Volvo Penta, Caterpillar, and MAN vie for dominance through continuous innovations in engine architecture, emissions control, and digital capabilities. Cummins leads in fuel-agnostic platforms like X10 and X15N, achieving higher market penetration through versatile fuel compatibility and enhanced diagnostics. Volvo Penta gained significant traction in marine and genset applications with its D17 series and compact IMO III solutions. Meanwhile, Caterpillar and MAN uphold strong positions in heavy-duty, off-highway, and industrial applications by investing in durable high-performance engines and global service networks. Partnerships and acquisitions—such as Volvo Penta expanding its aftermarket through alliances—further strengthen market positions. The strategic push toward low-carbon fuels, electrification support systems, and AI-based engine management is shaping the competitive landscape, with each player emphasizing cost-effective compliance and operational efficiency across diverse sectors.

Cummins Inc.

Volvo Penta

Caterpillar Inc.

MAN Energy Solutions

Perkins Engines Company Limited

Yanmar Co., Ltd.

Kubota Corporation

Mitsubishi Heavy Industries, Ltd.

John Deere Power Systems

Doosan Infracore Co., Ltd.

DEUTZ AG

Liebherr Group

Kohler Co.

FPT Industrial S.p.A. (a CNH Industrial company)

Recent technological advancements are defining the future of diesel industrial engines. Manufacturers increasingly incorporate fuel-agnostic platforms, capable of optimizing for diesel, natural gas, hydrogen, or biomethane, like Cummins’ X10 and X15N series, enabling versatile deployment across applications. Advanced combustion systems featuring high-pressure common-rail injection, variable geometry turbochargers, and electronic control modules further enhance power density and operational flexibility. For example, Volvo Penta’s D13 engines now include variable-geometry turbos that refine throttle response across multiple engine calibrations. Emissions aftertreatment systems, including SCR, DPF, and low-NOx configurations, are now integrated into compact modular sub-systems, reducing installation complexity and emissions footprint. Volvo Penta’s IMO III-capable D8 and D17 gensets exemplify this trend, featuring compact solutions for marine applications. Digital integration is accelerating, with AI-driven controls, remote monitoring, and telemetry embedded in engine platforms. Cummins’ HELM X15N and X10 platforms exemplify fully connected, fuel-flexible units optimized via predictive analytics and condition-based control. Furthermore, component electrification, such as the 650 V e-compressor for fuel cells launched by Cummins, signals manufacturers’ strategic pivot towards hybrid and hydrogen ecosystems. This electrification trend is bolstered by deeper integration of hybrid assistance systems, like starter-generators and electric superchargers, improving transient response and idle efficiency. Collectively, these technologies enhance performance, downtime resilience, emissions control, and adaptability to low-carbon fuels—all while supporting a modular and digitally empowered engine ecosystem.

In December 2023, Cummins inaugurated a new production line and Pilot Test Center in Marktheidenfeld, Germany, expanding capacity for advanced emissions components and creating testbeds for European regulation compliance.

In January 2024, Volvo Penta launched its powerful D17 genset engine into the North American market alongside scalable IMO III configuration—a compact, emissions-compliant solution for marine and industrial users.

In February 2024, Cummins unveiled its 650 V e-compressor for fuel-cell engines and hydrogen loop BOP systems at the ACT Expo, marking a strategic move into complementary electrification components.

In July 2024, Brazilian miner Vale partnered with Komatsu and Cummins to retro‑fit haul trucks with dual-fuel engines capable of using up to 70% ethanol, achieving reductions of up to 70% in CO₂ emissions during mine operations.

The scope of the Diesel Industrial Engine Market report encompasses a comprehensive examination of engine types, applications, end-users, regional markets, competitive players, and technological trends. It provides segmented insights across high‑, medium‑, and low‑speed engines, addressing power generation, construction, marine, oil & gas, and agriculture sectors. The report delivers granular end‑user analysis—covering infrastructure operators, OEMs, rental/leasing firms, and government utilities—highlighting adoption patterns and investment drivers. It delves into regional dynamics including North America, Europe, Asia-Pacific, South America, and MEA, with country-level performance metrics, policy contexts, and macroeconomic drivers. With a strong emphasis on innovation, the report analyzes emerging technologies: fuel-agnostic platforms, hybrid solutions, digital integrations, aftertreatment systems, and component electrification. Competitive profiles summarize leading players’ strategic initiatives, product portfolios, partnerships, and technical capabilities. Lastly, it incorporates market drivers, restraints, opportunities, challenges, and five-year forecasts—offering stakeholders a roadmap for positioning, valuation, and scenario planning in a transforming diesel engine ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Diesel Industrial Engine Market |

| Market Revenue (2024) | USD 1,056.0 Million |

| Market Revenue (2032) | USD 1,814.4 Million |

| CAGR (2025–2032) | 7.0 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country‑wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Cummins Inc., Volvo Penta, Caterpillar Inc., MAN Energy Solutions, Perkins Engines Company Limited, Yanmar Co., Ltd., Kubota Corporation, Mitsubishi Heavy Industries, Ltd., John Deere Power Systems, Doosan Infracore Co., Ltd., DEUTZ AG, Liebherr Group, Kohler Co., FPT Industrial S.p.A. (a CNH Industrial company) |

| Customization & Pricing | Available on Request (10 % Customization is Free) |