Reports

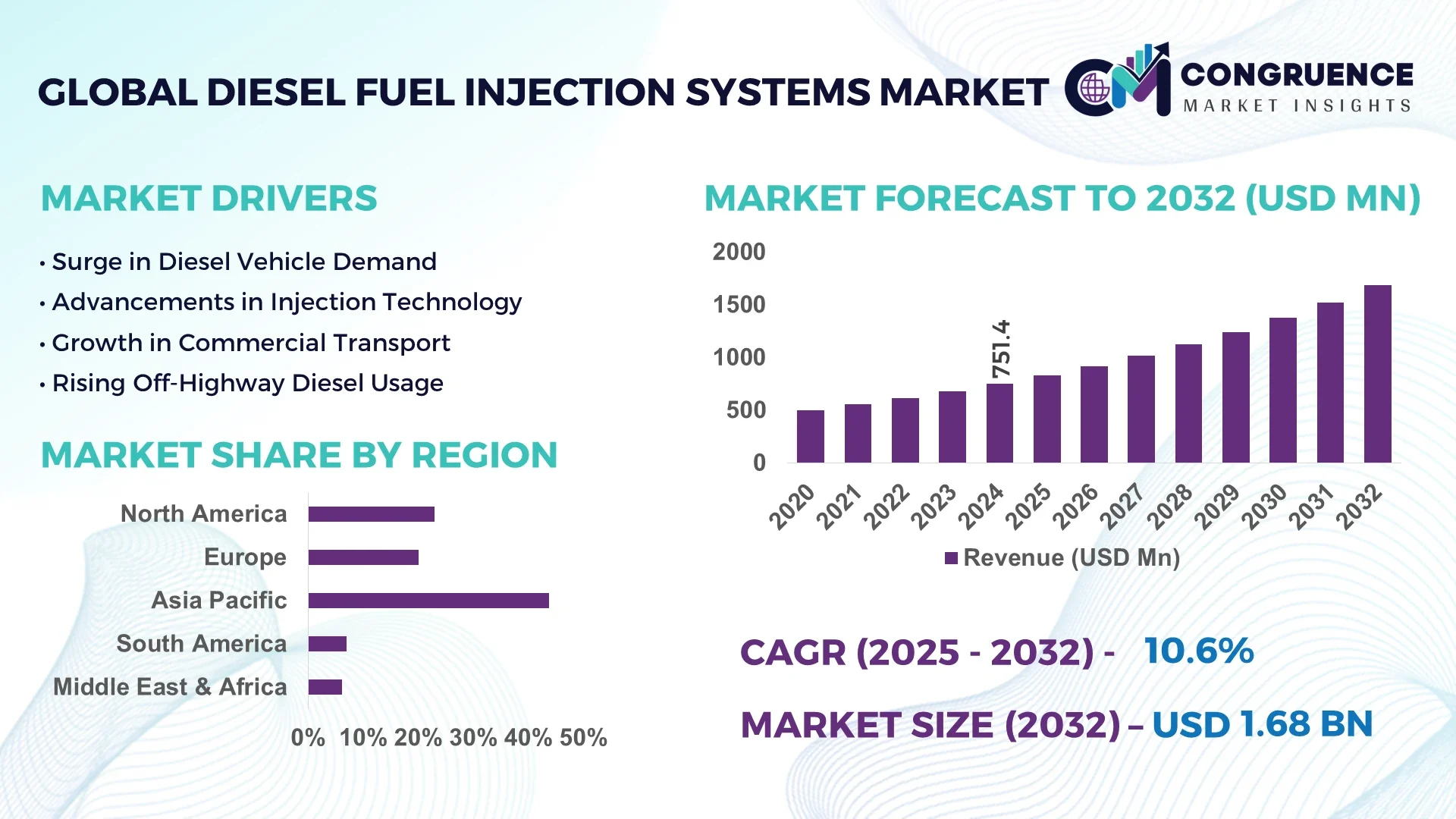

The Global Diesel Fuel Injection Systems Market was valued at USD 751.4 million in 2024 and is anticipated to reach a value of USD 1,682.3 million by 2032, expanding at a CAGR of 10.6% between 2025 and 2032.

China stands out as a dominant force in the diesel fuel injection systems market, primarily due to its robust manufacturing infrastructure and significant investments in advanced diesel technologies. In 2024, a leading Chinese engine manufacturer unveiled a diesel engine achieving a record-breaking thermal efficiency of 53.09%. This innovation not only underscores China’s commitment to enhancing engine performance but also positions the country at the forefront of diesel technology advancements.

The diesel fuel injection systems market is experiencing a transformative phase, driven by stringent emission regulations and the global push for fuel-efficient vehicles. Manufacturers are increasingly focusing on integrating electronic control units (ECUs) and advanced sensor technologies to optimize fuel delivery and combustion processes. Additionally, the rise of alternative fuels, such as hydrogen and biodiesel, is prompting the development of versatile injection systems capable of handling diverse fuel types. This evolution reflects the industry's commitment to sustainability and adaptability in a rapidly changing automotive landscape.

Artificial Intelligence (AI) is revolutionizing the diesel fuel injection systems market by introducing advanced diagnostics, predictive maintenance, and real-time optimization capabilities. AI-driven models analyze vast amounts of engine data to detect anomalies, predict potential failures, and optimize fuel injection parameters for enhanced performance and reduced emissions. For instance, transformer-based AI models have been developed to predict faults in diesel engines with an accuracy of 70.01%, enabling proactive maintenance and minimizing downtime.

Moreover, the integration of AI with physics-informed neural networks (PINNs) allows for the creation of digital twins of diesel engines. These digital replicas simulate engine behavior under various conditions, facilitating real-time monitoring and adaptive control strategies. Such advancements not only improve engine efficiency but also extend the lifespan of components by ensuring optimal operating conditions.

In the realm of fuel injection, AI algorithms are being employed to fine-tune injection timing and pressure, adapting to changing engine loads and environmental conditions. This dynamic adjustment leads to better fuel atomization, complete combustion, and lower pollutant emissions. As the automotive industry continues to embrace digital transformation, the role of AI in diesel fuel injection systems is set to become even more pivotal, driving innovations that align with global sustainability goals.

“In March 2024, Volvo announced a joint venture with Westport Fuel Systems to commercialize high-pressure direct-injection fuel system technology. This collaboration aims to enable internal combustion engines to utilize carbon-neutral fuels like biogas or hydrogen, significantly reducing CO₂ emissions in long-haul transport.”

The global emphasis on reducing vehicular emissions and improving fuel economy is propelling the demand for advanced diesel fuel injection systems. Modern injection technologies, such as common rail systems and piezoelectric injectors, offer precise fuel delivery, leading to complete combustion and reduced pollutants. This shift is particularly evident in regions with stringent emission norms, where manufacturers are compelled to adopt cutting-edge injection solutions to comply with regulations and meet consumer expectations for efficient performance.

The development of sophisticated diesel fuel injection systems involves substantial research and investment. High-pressure components, advanced materials, and integration with electronic control units contribute to elevated production costs. These expenses can be a barrier for manufacturers, especially in price-sensitive markets, limiting the widespread adoption of advanced injection technologies. Additionally, the need for specialized maintenance and potential challenges in retrofitting older engines further restrain market growth.

The growing interest in sustainable and alternative fuels presents a significant opportunity for the diesel fuel injection systems market. Developing injection systems compatible with fuels like biodiesel, hydrogen, and synthetic alternatives can cater to the evolving energy landscape. Such adaptability not only aligns with global decarbonization efforts but also opens new avenues for manufacturers to innovate and capture emerging market segments focused on eco-friendly transportation solutions.

The rapid advancement and adoption of electric vehicles pose a substantial challenge to the diesel fuel injection systems market. As consumers and governments prioritize zero-emission transportation, the demand for traditional diesel-powered vehicles may decline. This shift necessitates strategic adaptations by diesel system manufacturers, including diversification into hybrid technologies or alternative fuel systems, to remain relevant in a transforming automotive industry.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping the demand dynamics in the diesel fuel injection systems market. Pre-assembled engine modules with integrated injection systems are being developed off-site, reducing on-site assembly time and ensuring consistent quality. This trend is particularly prominent in commercial vehicle manufacturing, where efficiency and scalability are paramount.

Advancements in Piezoelectric Injector Technology: Piezoelectric injectors are gaining traction due to their ability to deliver rapid and precise fuel injections. These injectors respond faster than traditional solenoid-based systems, allowing for multiple injections per combustion cycle. The result is improved fuel atomization, better combustion efficiency, and reduced emissions, aligning with stringent environmental regulations.

Integration of Smart ECUs and Sensor Technologies: Modern diesel engines are increasingly equipped with intelligent electronic control units (ECUs) that process data from various sensors to optimize fuel injection parameters in real-time. This integration enhances engine performance, adapts to varying driving conditions, and facilitates predictive maintenance by identifying potential issues before they escalate.

Development of Multi-Fuel Injection Systems: To accommodate the shift towards alternative fuels, manufacturers are developing injection systems capable of handling multiple fuel types, including biodiesel and hydrogen. These versatile systems ensure compatibility with various fuels, providing flexibility and future-proofing for both manufacturers and consumers in an evolving energy landscape.

The global diesel fuel injection systems market is segmented based on type, application, and end-user. Each of these segments plays a crucial role in shaping the market landscape, offering varied growth opportunities and demand dynamics. By type, the market includes common rail, rotary pump, and inline pump systems. Applications primarily span across light commercial vehicles, heavy commercial vehicles, and passenger vehicles. End-user industries include automotive, agriculture, construction, marine, and others. Understanding the segmentation of this market helps stakeholders target specific demand areas, allocate resources effectively, and forecast trends with greater accuracy. Differences in technological preferences, emission regulations, and infrastructure development levels also influence the penetration of these segments across regions.

The diesel fuel injection systems market is categorized into three major types: common rail, rotary pump, and inline pump systems. Among these, common rail fuel injection systems dominate the market due to their superior fuel efficiency, high-pressure delivery, and compliance with stringent emission norms. These systems are widely adopted in both passenger and commercial vehicles because they enable precise fuel atomization, resulting in cleaner combustion and enhanced engine performance.

Rotary pump systems continue to serve older diesel vehicle models and small commercial vehicles, but their share is gradually declining due to the shift toward electronic and high-performance systems. On the other hand, inline pump systems are still prevalent in heavy-duty trucks and off-road vehicles, especially in developing markets, due to their rugged design and ease of maintenance.

The fastest-growing segment is the common rail system, which is witnessing significant adoption across emerging economies as automakers upgrade vehicles to meet emission standards. As manufacturers push for fuel-efficient and eco-friendly engine designs, the demand for common rail systems is expected to surge further.

In terms of application, the diesel fuel injection systems market is segmented into passenger vehicles, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs). Passenger vehicles currently hold the largest share of the market. The growth in urbanization, increasing vehicle ownership, and consumer demand for fuel-efficient personal transportation are driving the demand in this segment. In particular, diesel-powered SUVs and crossovers have gained popularity due to their superior mileage and torque.

Heavy commercial vehicles account for a significant portion of diesel fuel injection system usage due to their reliance on diesel engines for hauling heavy loads over long distances. Although the segment's growth is stable, it continues to be a vital revenue stream, especially in logistics and construction industries.

Light commercial vehicles, however, represent the fastest-growing application segment, driven by the growth of e-commerce, last-mile delivery services, and urban transportation needs. The demand for fuel-efficient and durable LCVs has boosted the adoption of advanced diesel injection systems tailored to meet efficiency and emission standards.

Based on end-user, the diesel fuel injection systems market is segmented into automotive, agriculture, construction, marine, and others. The automotive sector is the leading end-user, accounting for the majority of system installations globally. As passenger and commercial vehicle production continues to rise, especially in Asia-Pacific and Latin America, the demand from this segment remains strong. Regulatory mandates around emissions and fuel economy also push automakers to adopt advanced injection systems.

The fastest-growing end-user segment is the agriculture sector, where modern diesel-powered tractors, harvesters, and irrigation pumps increasingly utilize efficient fuel injection systems. With precision farming gaining traction and governments offering subsidies for mechanization, diesel engine upgrades are on the rise in rural markets.

Meanwhile, the construction and marine sectors remain stable contributors. Diesel fuel injection systems are favored in construction machinery due to their high torque delivery, while in marine applications, they support propulsion and auxiliary systems in small- to mid-sized vessels. However, innovation and demand growth are most evident in the agriculture and automotive sectors.

Asia-Pacific accounted for the largest market share at 43.8% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

The dominance of Asia-Pacific is attributed to its massive automotive production, increasing demand for commercial vehicles, and technological advancements in fuel injection systems across countries like China, India, and Japan. Meanwhile, North America's growth is being fueled by rising emission regulations and technological innovation, especially in the U.S. and Canada. Increasing adoption of high-performance diesel engines in logistics, agriculture, and construction sectors is also contributing to growth in this region.

Emission Standards Fuel Innovation in Diesel Technologies

In North America, the diesel fuel injection systems market is witnessing significant evolution driven by tightening emission norms and demand for improved engine performance. The United States remains a key contributor, with diesel engines still prominent in sectors like heavy-duty trucks, construction, and agriculture. Technological adoption is high, with OEMs integrating advanced common rail systems and smart ECUs to comply with evolving regulations. There’s also a surge in research for injection systems that support low-carbon fuels such as biodiesel and renewable diesel. Canada’s market is also growing, supported by infrastructure projects and agricultural modernization using fuel-efficient diesel engines.

Transition Towards Hybrid Systems with Diesel Efficiency

Europe is focusing on emission reductions while still maintaining diesel engine usage in commercial and off-road applications. Countries such as Germany, France, and Italy are emphasizing cleaner combustion through advanced diesel injection systems. Manufacturers are investing in R&D to enhance injection pressure and precision, improving fuel economy. The adoption of plug-in diesel hybrids is growing in some segments, leveraging the torque and efficiency of diesel with the benefits of electric drive. Additionally, the construction and logistics sectors remain large consumers of diesel engines across the EU, where Euro VI regulations continue to shape system designs.

China and India Lead Surge in High-Performance Diesel Systems

Asia-Pacific dominates the global market, primarily due to the vast production of diesel-powered vehicles and off-highway equipment. China leads the region, investing heavily in thermal efficiency improvements, while India is rapidly upgrading its commercial vehicle fleet to meet Bharat Stage VI norms. In Japan and South Korea, technology-heavy markets, the trend is towards low-emission and intelligent diesel fuel systems. OEMs in the region are deploying common rail systems in mid-range vehicles to balance cost and performance. The booming e-commerce sector and infrastructure investments across Southeast Asia are also fueling demand for advanced diesel injection technologies.

Agriculture and Mining Drive Diesel Engine Investments

South America’s diesel fuel injection systems market is significantly driven by the agricultural and mining sectors, particularly in Brazil and Argentina. Diesel remains the preferred fuel due to its energy density and cost efficiency. In 2024, the demand for diesel engines in tractors, harvesters, and mining trucks surged, pushing suppliers to introduce more reliable and high-pressure fuel systems. While the adoption of advanced injection technologies is slower than in other regions, there is steady growth in the implementation of electronic diesel control units in response to rising fuel costs and productivity requirements.

Oil & Gas Logistics and Construction Fueling Diesel Growth

In the Middle East & Africa, diesel injection systems are in high demand for industrial applications, including oil & gas logistics, construction, and mining operations. Countries like Saudi Arabia and South Africa are witnessing an uptick in infrastructure projects, creating strong demand for diesel-powered equipment. The region continues to use mechanical and inline pump systems for cost-efficiency, although there's growing interest in upgrading to common rail systems for better fuel economy. The harsh environmental conditions have also driven demand for rugged and durable injection systems capable of operating under extreme heat and dust.

China – USD 204.6 Million, China leads due to its massive commercial vehicle production and rapid integration of high-efficiency diesel systems.

United States – USD 139.2 Million, The U.S. holds a strong position thanks to its advanced diesel technologies in transportation, agriculture, and construction equipment markets.

The diesel fuel injection systems market is characterized by intense competition, driven by technological advancements and the need for compliance with stringent emission regulations. Leading companies are investing heavily in research and development to innovate and offer more efficient and environmentally friendly solutions. The market is witnessing a shift towards high-pressure common rail systems and electronic control units (ECUs) that enhance fuel efficiency and reduce emissions. Companies are also focusing on expanding their global footprint through strategic partnerships and acquisitions to cater to the growing demand in emerging markets. The emphasis on sustainability and the transition towards alternative fuels are further influencing the competitive dynamics, prompting companies to adapt and innovate continually.

Robert Bosch GmbH

Denso Corporation

Delphi Technologies

Continental AG

Stanadyne LLC

Woodward L'Orange GmbH

Weichai Power Co., Ltd.

Cummins Inc.

Zexel

Weifu Group

Shandong Kangda

PurePower Technologies

The diesel fuel injection systems market is undergoing significant technological transformations aimed at enhancing engine performance, fuel efficiency, and emission control. One of the prominent advancements is the widespread adoption of high-pressure common rail systems, which allow precise control of fuel injection timing and quantity, leading to better combustion and reduced emissions. These systems are increasingly integrated with electronic control units (ECUs) that optimize engine performance under various operating conditions.

Another notable development is the implementation of piezoelectric injectors, which offer faster response times and more precise fuel delivery compared to traditional solenoid injectors. This technology contributes to improved engine efficiency and lower noise levels. Additionally, the market is witnessing the emergence of hybrid fuel injection systems capable of handling multiple fuel types, including biodiesel and hydrogen, aligning with the global shift towards cleaner energy sources.

Manufacturers are also exploring the integration of advanced materials and coatings to enhance the durability and lifespan of injection components, thereby reducing maintenance costs and downtime. Furthermore, the incorporation of real-time monitoring and diagnostics through IoT-enabled sensors is enabling predictive maintenance and minimizing the risk of unexpected failures. These technological innovations are collectively driving the evolution of diesel fuel injection systems toward more sustainable and efficient solutions.

In March 2024, a major fuel systems provider announced a joint venture with a leading truck manufacturer to commercialize high-pressure direct-injection technology for long-haul transportation. This collaboration aims to support the use of carbon-neutral fuels like biogas and hydrogen in diesel engines.

In August 2024, multiple European truck manufacturers increased investments in hydrogen combustion engines as a cost-effective alternative to diesel. One firm plans to deliver 200 hydrogen trucks for field testing, with another initiating hydrogen combustion engine tests by 2026.

In December 2023, a global auto component supplier launched mass production of a multi-fuel injection system tailored for hydrogen-powered internal combustion engines. The system includes newly designed injectors and advanced ECUs.

In September 2024, a major fuel systems company unveiled a modular hydrogen injector platform compatible with a wide range of power outputs. The platform supports high-pressure and high-flow hydrogen fuel delivery, addressing needs across commercial and industrial vehicle applications.

The diesel fuel injection systems market report offers a comprehensive outlook on industry dynamics, capturing developments in technology, segmentation, and regional performance. The analysis includes segmentation by type, application, and end-user, outlining trends, leading segments, and emerging opportunities in each category.

Technological innovation is a key growth enabler, with new advancements in high-pressure systems, hybrid fuel compatibility, and smart injector technologies reshaping market offerings. The report discusses how the industry is evolving in response to emission regulations, fuel efficiency requirements, and the push for decarbonization. Manufacturers are increasingly focusing on durability, performance optimization, and the integration of smart control systems to maintain competitiveness.

Regionally, the report highlights markets with strong current demand and those poised for rapid growth, providing strategic insights into expansion opportunities. It also includes a competitive analysis of leading companies, profiling their strategies, technological investments, and innovation capabilities. The insights are designed to help stakeholders understand market dynamics and align their strategies with future growth trajectories in the global diesel fuel injection systems market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Diesel Fuel Injection Systems Market |

| Market Revenue (2024) | USD 751.4 Million |

| Market Revenue (2032) | USD 1,682.3 Million |

| CAGR (2025–2032) | 10.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Advancements, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Robert Bosch GmbH, Denso Corporation, Delphi Technologies, Continental AG, Stanadyne LLC, Woodward L'Orange GmbH, Weichai Power Co., Ltd., Cummins Inc., Zexel, Weifu Group, Shandong Kangda, PurePower Technologies |

| Customization & Pricing | Available on Request (10% Customization is Free) |