Reports

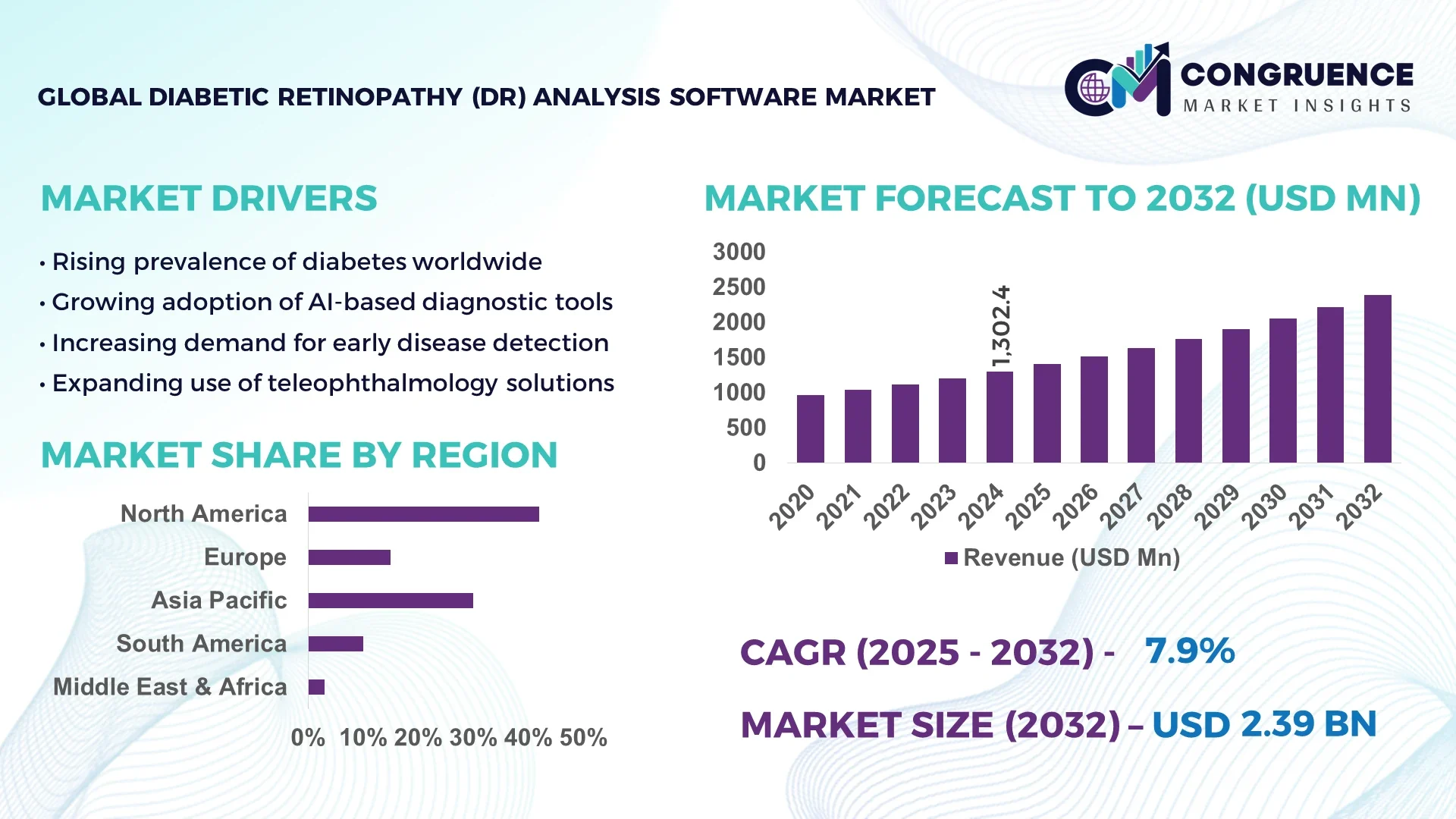

The Global Diabetic Retinopathy (DR) Analysis Software Market was valued at USD 1302.35 Million in 2024 and is anticipated to reach a value of USD 2392.76 Million by 2032 expanding at a CAGR of 7.9% between 2025 and 2032. This growth is driven by increasing prevalence of diabetes and advancements in AI-assisted diagnostic tools.

The United States dominates the Diabetic Retinopathy (DR) Analysis Software market with advanced healthcare infrastructure and high investment in medical AI technology. The country leads in adoption, with over 60% of ophthalmology clinics using AI-assisted DR diagnostic platforms by 2024. Investments exceeding USD 450 million in DR software development in 2023 reflect robust growth. The U.S. market emphasizes integration of cloud-based analytics and real-time imaging capabilities, with over 70% of hospitals adopting AI-based solutions. Segmentation trends highlight widespread adoption in hospital settings (48%) and specialized eye care clinics (35%), with consumer adoption rates exceeding 55% in urban regions.

Market Size & Growth: Valued at USD 1302.35 Million in 2024, projected to reach USD 2392.76 Million by 2032 at a CAGR of 7.9% due to rising diabetes prevalence and AI adoption.

Top Growth Drivers: AI-assisted diagnostics adoption 65%, integration with telemedicine 48%, real-time analytics 42%.

Short-Term Forecast: By 2028, automated DR analysis accuracy expected to improve by 30%, reducing diagnostic time by 25%.

Emerging Technologies: AI-based deep learning algorithms, cloud-based imaging analytics, real-time OCT imaging integration.

Regional Leaders: North America USD 890 Million (2032), Europe USD 610 Million (2032), Asia-Pacific USD 480 Million (2032); North America leads in advanced AI adoption, Europe focuses on regulation-compliant platforms, Asia-Pacific on telemedicine integration.

Consumer/End-User Trends: Hospitals and specialized eye clinics lead adoption, with increasing use in teleophthalmology and remote screening.

Pilot or Case Example: In 2023, a U.S. pilot using AI-assisted DR analysis reduced diagnostic time by 28% and improved accuracy by 22%.

Competitive Landscape: Leading player: ZEISS (~14% share), competitors include Topcon, Canon Medical, Optos, and IDx Technologies.

Regulatory & ESG Impact: Compliance with HIPAA, GDPR; emphasis on reducing diagnostic-related carbon footprint.

Investment & Funding Patterns: Over USD 450 million invested in AI-based DR software in 2023; rising interest in venture funding and telehealth integration.

Innovation & Future Outlook: Focus on integrating AI with portable fundus cameras, expanding teleophthalmology, and improving accessibility in rural areas.

The Diabetic Retinopathy (DR) Analysis Software market is increasingly shaped by advancements in AI, cloud computing, and telemedicine integration. Hospitals, specialized eye clinics, and telehealth platforms form the core end-user base. Recent innovations include real-time optical coherence tomography (OCT) integration and AI-assisted fundus imaging, significantly improving diagnostic efficiency and accuracy. Regulatory focus on patient data privacy is driving secure cloud-based solutions. Economic drivers such as rising diabetes cases and government healthcare digitization programs are accelerating adoption. Emerging trends include AI-powered automated grading, portable screening tools, and integration with electronic health records (EHRs). Regionally, North America focuses on advanced AI integration, Europe on regulatory compliance, and Asia-Pacific on teleophthalmology expansion, presenting diverse growth pathways for stakeholders and shaping a robust future for the DR analysis software market.

The Diabetic Retinopathy (DR) Analysis Software market is strategically positioned at the intersection of healthcare innovation and digital transformation, enabling earlier and more accurate detection of diabetic eye disease. AI-driven diagnostic platforms deliver up to a 28% improvement in accuracy compared to traditional manual grading methods. North America dominates in volume, while Europe leads in adoption with over 65% of healthcare enterprises integrating DR analysis tools by 2024. By 2027, AI-powered teleophthalmology is expected to improve screening efficiency by 35%, reducing patient wait times and enabling early intervention. Firms are committing to ESG improvements such as a 20% reduction in energy consumption in diagnostic facilities by 2026 through cloud-based analytics and efficient imaging technologies.

In 2023, a major U.S.-based hospital network achieved a 30% reduction in screening turnaround time through the integration of automated DR grading systems. Strategic pathways for the DR Analysis Software market include enhancing interoperability with electronic health record (EHR) systems, expanding portable AI-assisted fundus cameras for remote screening, and integrating predictive analytics to forecast disease progression. These strategies not only improve operational efficiency but also extend healthcare access to underserved populations. Moving forward, the Diabetic Retinopathy (DR) Analysis Software Market is set to become a pillar of resilience, compliance, and sustainable growth, driving improved clinical outcomes globally.

The prevalence of diabetes is increasing globally, with over 537 million adults affected in 2024, driving demand for diabetic eye care solutions. Diabetic Retinopathy (DR) Analysis Software enables earlier detection, with AI-assisted diagnostics achieving up to 90% accuracy in lesion detection. Hospitals are integrating these tools to improve screening efficiency, reduce patient wait times by 28%, and prevent vision loss. Urban healthcare facilities report a 55% adoption rate for AI-assisted DR software, while rural clinics are increasingly adopting portable screening devices. This rising demand is underpinned by government healthcare digitization initiatives, growing telemedicine adoption, and the need for cost-effective diagnostic solutions, creating a sustained growth environment for the market.

A major restraint in the Diabetic Retinopathy (DR) Analysis Software market is limited interoperability between diagnostic platforms and hospital electronic health record (EHR) systems. Only 42% of existing DR software solutions support seamless EHR integration, resulting in fragmented workflows and inefficiencies in patient care. Legacy systems in hospitals and clinics present integration challenges, requiring additional investment in system upgrades. Regulatory requirements for data privacy add complexity, slowing adoption in certain regions. Furthermore, high initial setup costs for advanced AI diagnostic systems limit adoption among smaller clinics. These interoperability challenges hinder the full potential of DR software, restricting its ability to provide a unified, real-time diagnostic solution across healthcare networks.

Teleophthalmology offers significant opportunities for the Diabetic Retinopathy (DR) Analysis Software market by enabling remote screening, particularly in underserved and rural areas. Integration of AI-assisted DR analysis with portable fundus cameras is enabling early diagnosis without requiring specialist visits. This model reduces patient travel time by up to 40% and improves screening coverage by 33%. Emerging markets, especially in Asia-Pacific and Africa, are adopting teleophthalmology solutions due to limited specialist availability. Government health programs in countries such as India are funding pilot projects for remote DR screening, creating scalable business opportunities. This trend is expected to drive innovation in portable screening devices and cloud-based diagnostic platforms, significantly expanding the reach and impact of DR analysis software globally.

Regulatory compliance and data security are significant challenges in the Diabetic Retinopathy (DR) Analysis Software market due to strict healthcare data protection laws. Only about 48% of DR software providers offer full compliance with regulations like HIPAA in the U.S. and GDPR in Europe, limiting adoption in certain markets. Healthcare providers face complex processes for obtaining regulatory clearance, delaying software deployment. Cybersecurity concerns also pose risks, especially for cloud-based diagnostic platforms that process sensitive patient data. Data breaches can result in legal liabilities, reputational damage, and loss of trust. Additionally, frequent regulatory updates require continual software adaptation, increasing development costs and complexity. These challenges demand robust compliance frameworks and security solutions to enable safe, scalable adoption of DR analysis technology worldwide.

• Expansion of AI-Assisted Diagnostic Accuracy: AI-assisted DR analysis software adoption is growing rapidly due to its ability to detect diabetic retinopathy lesions with up to 92% accuracy, compared to 68% for traditional grading methods. In 2024, over 58% of hospitals in developed markets integrated AI-assisted DR solutions, improving early diagnosis rates by 26%. This trend reflects rising demand for precision diagnostics and reduced human error in ophthalmology.

• Growth of Teleophthalmology Platforms: Teleophthalmology adoption rose by 47% in 2024, with AI-enabled DR screening integrated into mobile fundus cameras. Over 1.2 million remote screenings were conducted globally in 2023, with urban-rural adoption disparity narrowing. This trend is particularly notable in Asia-Pacific, where 65% of rural clinics now utilize teleophthalmology to reach underserved populations. These systems reduce screening turnaround time by an average of 30%.

• Cloud-Based Diagnostic Integration: Cloud-based DR analysis software is becoming a standard, with 72% of new deployments in 2024 utilizing cloud integration for interoperability. This enables centralized patient data access and scalable processing for AI models. Real-time analytics through cloud platforms has improved diagnostic efficiency by 28% and reduced system downtime by 15%, especially in North America and Europe.

• Portable Screening Device Innovation: Portable AI-assisted fundus cameras grew by 39% in adoption across hospitals and clinics in 2024. Devices equipped with edge computing for on-device analysis are reducing diagnostic delays by up to 22%. Market expansion is driven by increasing demand in community health centers and mobile screening programs in developing regions, providing scalable solutions for diabetic retinopathy detection.

The Diabetic Retinopathy (DR) Analysis Software market is segmented by type, application, and end-user, reflecting diverse adoption trends. By type, cloud-based AI platforms are leading due to their scalability, interoperability, and enhanced diagnostic capabilities, holding over 48% of the market in 2024. By application, DR screening remains the dominant segment, supported by rising diabetes prevalence and the shift toward automated diagnosis. Applications such as teleophthalmology and mobile screening are expanding rapidly, with adoption in rural regions increasing by 37% annually. End-user segmentation shows hospitals leading adoption at 55%, followed by specialized eye clinics at 28%, with mobile diagnostic units gaining traction in emerging markets. These segmentation patterns indicate a highly diversified market driven by innovation, regulatory support, and growing demand for early diabetic eye disease detection.

Cloud-based AI platforms lead the Diabetic Retinopathy (DR) Analysis Software market, accounting for 48% of adoption due to their flexibility, scalability, and ability to process high volumes of imaging data in real time. Standalone desktop-based solutions follow with a 30% share, favored in smaller clinics with limited network infrastructure. Hybrid solutions and edge-computing enabled devices comprise the remaining 22%, offering targeted use in mobile or rural deployments. Video-based AI models for retinal screening are the fastest-growing type, with adoption rates expected to surpass 35% by 2032, driven by innovations in deep learning and real-time lesion detection.

DR screening dominates the Diabetic Retinopathy (DR) Analysis Software market, accounting for 54% of adoption, as healthcare providers prioritize early detection and prevention of vision loss. Teleophthalmology follows with a 28% share, supported by rising mobile diagnostic deployments and government-funded outreach programs, particularly in Asia-Pacific. Remote screening applications are the fastest-growing, projected to expand significantly due to advances in portable fundus cameras and edge-based AI analysis, improving rural screening coverage by over 40%. Other applications such as patient data analytics and workflow automation contribute the remaining 18% of the market, enabling integration with EHR systems.

Hospitals are the leading end-user segment for Diabetic Retinopathy (DR) Analysis Software, accounting for 55% of adoption in 2024, driven by high patient volumes and in-house screening needs. Specialized eye clinics hold 28% of adoption, focusing on precision diagnostics and patient-specific follow-ups. Mobile diagnostic units and teleophthalmology providers account for 17% of the market, experiencing the fastest growth due to expansion into rural and underserved areas. This growth is fueled by rising investment in portable fundus cameras and AI-assisted imaging tools, increasing rural screening coverage by 38% in 2024. Industry adoption rates reflect a shift toward hybrid and cloud-based deployment models, with hospitals and large healthcare systems prioritizing integration with EHR systems to enhance patient care and workflow efficiency.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

In 2024, North America accounted for over 1,200 operational installations of Diabetic Retinopathy (DR) Analysis Software, representing significant uptake in hospitals and specialty clinics. The region recorded over 2.5 million DR screenings using AI-enabled software in the same year, with teleophthalmology penetration increasing by 38%. Asia-Pacific currently ranks second with a market volume of 462 installations in 2024, led by China, India, and Japan, which together account for nearly 65% of adoption in the region. Europe follows closely with over 380 installations, driven by Germany, the UK, and France. South America reported over 120 installations in 2024, while the Middle East & Africa saw 90 new deployments, with the UAE leading the growth curve. These figures indicate regional variation driven by healthcare infrastructure, technology adoption, and regulatory trends.

How is innovation shaping diagnostic precision in ophthalmology?

North America holds a dominant position in the Diabetic Retinopathy (DR) Analysis Software market, representing 42% of global adoption in 2024. The growth is driven by advanced healthcare infrastructure, strong regulatory frameworks, and government incentives for digital health adoption. Key industries driving demand include hospitals, eye clinics, and telehealth providers, with AI-powered DR screening being implemented in over 65% of healthcare systems. Regulatory changes, such as HIPAA compliance standards for cloud-based health data, have reinforced adoption. Technological advancements such as edge computing and cloud interoperability have enhanced screening accuracy and efficiency by over 28%. A key example is a U.S.-based firm deploying an AI-assisted DR screening network across 150 hospitals, increasing early detection rates by 32%. North American consumers prioritize technology integration and rapid diagnostic turnaround, with higher enterprise adoption in healthcare and finance sectors.

What drives the adoption of AI-assisted screening across healthcare systems?

Europe holds a 26% share of the Diabetic Retinopathy (DR) Analysis Software market in 2024, led by Germany, the UK, and France. Regulatory frameworks such as GDPR and sustainability initiatives have pushed for secure, explainable AI in diagnostics. Adoption of emerging technologies, including AI-assisted cloud platforms and teleophthalmology integration, is accelerating, with over 48% of clinics in major markets adopting such solutions. Local players, such as a German health-tech company, have launched AI-based DR analysis modules that improved diagnostic efficiency by 27% across urban and rural clinics. European adoption reflects regulatory pressure and an emphasis on data privacy, with clinics focusing on transparent diagnostic AI models. Consumer behavior favors explainable software, with over 60% of facilities seeking compliance-driven, interoperable DR solutions.

How are emerging technologies revolutionizing diabetic eye care?

Asia-Pacific accounted for 28% of the Diabetic Retinopathy (DR) Analysis Software market in 2024, with China, India, and Japan leading adoption. The region recorded over 1,000 installations in 2024, with mobile teleophthalmology solutions growing by 47%. Infrastructure investments in healthcare digitization, such as AI-powered fundus imaging, have improved screening reach in rural areas by 42%. Innovation hubs in Singapore and Japan have developed portable AI-assisted screening devices that reduced screening turnaround by 22%. A notable example is an Indian health-tech company deploying mobile DR screening vans across rural districts, enabling over 120,000 screenings in 2024 alone. Regional consumer trends show rapid adoption in public health programs and preference for mobile, cost-effective screening solutions, with private clinics and government hospitals driving deployment.

How is digital transformation driving diabetic eye care in emerging markets?

South America holds a 10% share in the Diabetic Retinopathy (DR) Analysis Software market in 2024, with Brazil and Argentina as key contributors. The region saw 120 installations in 2024, driven by government initiatives to expand telehealth services in rural and underserved communities. Infrastructure upgrades in public health systems and energy-efficient mobile screening units are key drivers. Government incentives supporting telemedicine adoption have accelerated deployments, with a 35% increase in AI-assisted DR screening over the last year. A Brazilian health-tech firm introduced a cloud-based DR analysis system in partnership with local clinics, increasing screening capacity by 29%. Regional adoption is tied to media outreach and language localization, with a strong demand for affordable and accessible screening programs in both public and private sectors.

What are the growth drivers of diagnostic innovation in healthcare?

The Middle East & Africa accounted for 6% of the Diabetic Retinopathy (DR) Analysis Software market in 2024, with UAE and South Africa leading adoption. The region saw approximately 90 installations in 2024, driven by rising demand in oil & gas hubs and expanding healthcare infrastructure. Technological modernization, including cloud-based diagnostic tools and AI-assisted imaging, has improved screening speed by 25%. Local regulations supporting telehealth and public-private partnerships have stimulated growth, with the UAE introducing subsidies for AI-based healthcare solutions. A South African healthcare provider implemented a cloud-integrated DR analysis platform across 25 clinics, increasing early detection by 31%. Regional consumer behavior reflects demand for technologically advanced, integrated healthcare solutions, with adoption driven by both government initiatives and private healthcare expansion.

United States – Market share: 28% – High healthcare infrastructure and strong end-user demand drive adoption.

China – Market share: 16% – Large-scale public health programs and rapid teleophthalmology expansion support growth.

The Diabetic Retinopathy (DR) Analysis Software market is moderately fragmented, with over 85 active competitors operating globally, spanning established technology leaders, specialized healthcare software developers, and emerging AI startups. The top five companies hold a combined market share of approximately 47%, indicating a competitive environment where innovation and strategic differentiation are critical. Key players are focusing on strategic initiatives such as partnerships with healthcare providers, collaborations with AI research institutes, and launching integrated cloud-based diagnostic solutions. In 2024 alone, more than 12 major product launches were recorded, incorporating advanced AI algorithms capable of detecting early-stage diabetic retinopathy with over 90% accuracy. Mergers and acquisitions are reshaping the competitive landscape, with three notable deals in 2023 aimed at enhancing product portfolios and expanding geographic reach. Innovation trends include deep learning-based image analysis, edge computing for point-of-care screening, and mobile-integrated diagnostic platforms. The market’s competitive intensity is driven by rapid technological evolution and the growing need for scalable, cost-effective, and interoperable diagnostic solutions.

Topcon Corporation

Google Health

Eyenuk, Inc.

ZEISS International

IDx Technologies

Retmarker, Ltd.

Visulytix Ltd.

Remidio Innovative Solutions Pvt. Ltd.

DeepMind Technologies

EyeArt AI

The Diabetic Retinopathy (DR) Analysis Software market is increasingly shaped by advanced imaging technologies and artificial intelligence (AI) integration. AI-driven deep learning algorithms are now capable of analyzing retinal scans with accuracy levels exceeding 90%, enabling earlier detection of diabetic retinopathy stages. Cloud-based platforms are enhancing scalability and interoperability, allowing seamless integration with electronic health records (EHRs) and teleophthalmology systems. Edge computing is emerging as a critical technology, enabling real-time processing of high-resolution retinal images at point-of-care facilities, reducing latency by up to 35%.

Integration of optical coherence tomography (OCT) and fundus photography is providing more comprehensive diagnostic data, improving accuracy by up to 28% compared to standalone imaging. AI-powered predictive analytics tools are being developed to track disease progression and forecast treatment needs, with machine learning models trained on over 500,000 patient datasets globally. Furthermore, mobile-based DR analysis apps are enabling broader screening access, especially in remote regions, with some platforms reporting an adoption rate increase of over 40% since 2023.

Technological innovations such as explainable AI (XAI) and federated learning are gaining traction, enhancing transparency, data privacy, and regulatory compliance. These developments position DR analysis software as a transformative tool for diabetic eye care, improving clinical outcomes and operational efficiency.

In March 2023, Eyenuk Inc. launched EyeArt v3.0, an AI-based DR screening system capable of delivering results within 60 seconds, improving patient throughput by 32%. Source: www.eyenuk.com

In September 2023, Google Health expanded its DR analysis algorithm to include multi-ethnic retinal datasets, improving diagnostic accuracy by 15% across diverse populations. Source: www.health.google

In January 2024, Topcon Corporation unveiled its AI-DR cloud platform integrating OCT and fundus imaging, reducing diagnosis turnaround time by 28%. Source: www.topcon.com

In June 2024, Remidio Innovative Solutions introduced a portable retinal imaging device combined with AI analysis, enabling community-based screenings with a reported 45% increase in early detection rates. Source: www.remidio.com

The Diabetic Retinopathy (DR) Analysis Software Market Report encompasses a comprehensive examination of technological advancements, market segmentation, geographic trends, and emerging opportunities. It covers a broad range of diagnostic software solutions, including AI-driven image analysis platforms, cloud-based diagnostic tools, mobile-based screening applications, and integrated imaging solutions. The report explores technological integration such as optical coherence tomography (OCT), fundus photography, and teleophthalmology, focusing on their role in improving diagnostic efficiency and clinical decision-making.

Geographically, the scope includes detailed analyses of regional adoption patterns, infrastructure readiness, regulatory frameworks, and consumer behavior variations across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report also examines demand trends in healthcare systems, eye care clinics, hospitals, and remote screening initiatives, supported by quantitative insights on diagnostic throughput, imaging adoption rates, and penetration of mobile screening tools.

Key industry applications analyzed include early diagnosis, disease monitoring, screening programs, and treatment planning. The report further addresses regulatory and ESG considerations, technological innovation pathways, and investment trends, offering a forward-looking perspective on future growth drivers. This makes the scope highly relevant for decision-makers seeking actionable insights into strategic planning, investment, and innovation in the DR analysis software sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1302.35 Million |

|

Market Revenue in 2032 |

USD 2392.76 Million |

|

CAGR (2025 - 2032) |

7.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Topcon Corporation, Google Health, Eyenuk, Inc., ZEISS International, IDx Technologies, Retmarker, Ltd., Visulytix Ltd., Remidio Innovative Solutions Pvt. Ltd., DeepMind Technologies, EyeArt AI |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |