Reports

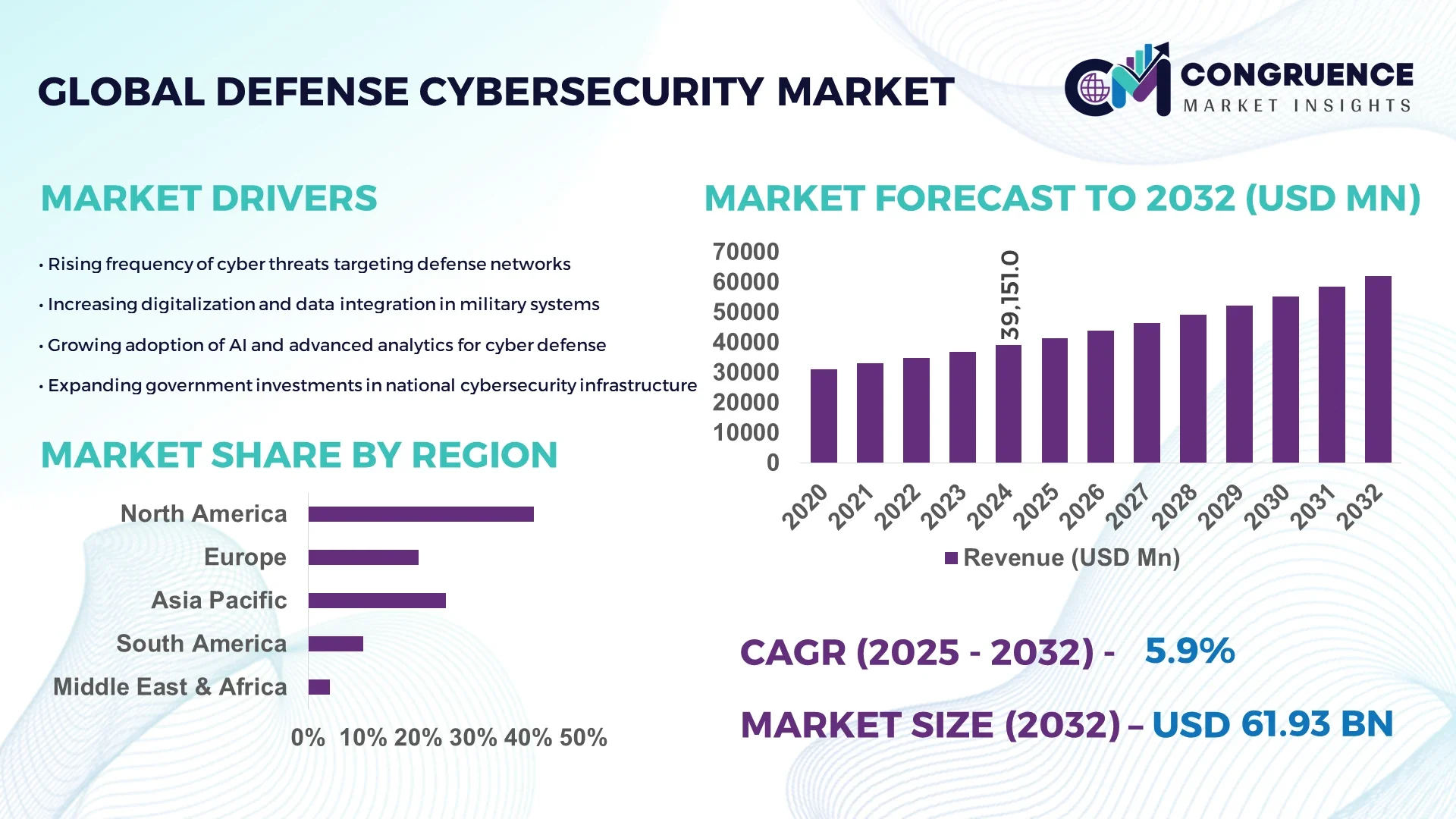

The Global Defense Cybersecurity Market was valued at USD 39,151 Million in 2024 and is anticipated to reach a value of USD 61,931 Million by 2032 expanding at a CAGR of 5.9% between 2025 and 2032. This growth is driven by increasing cyber threats targeting military networks and the ongoing digital transformation of defense infrastructure.

The United States leads the global Defense Cybersecurity Market with extensive government funding and advanced military R&D programs. The country’s Department of Defense allocated over USD 13 billion for cybersecurity initiatives in 2024, focusing on AI-driven threat detection, zero-trust architecture, and quantum-resistant encryption systems. The U.S. also hosts more than 120 defense-focused cybersecurity firms and collaborates with private contractors to enhance secure communications, logistics management, and real-time battlefield analytics across its cyber command operations.

• Market Size & Growth: Valued at USD 39.15 Billion in 2024 and projected to reach USD 61.93 Billion by 2032, expanding at a CAGR of 5.9%. Growth driven by heightened demand for secure communication and defense infrastructure modernization.

• Top Growth Drivers: Rising cyber-attack prevention demand (+34%), AI-based defense analytics adoption (+27%), and increased investment in network resilience (+22%).

• Short-Term Forecast: By 2028, AI-enabled defense cybersecurity systems expected to reduce network breach risks by up to 40% and operational costs by 18%.

• Emerging Technologies: Quantum encryption, cloud-based defense data centers, and zero-trust network architectures are reshaping military-grade cybersecurity systems.

• Regional Leaders: North America projected at USD 25.4 Billion by 2032, Europe at USD 17.8 Billion, and Asia-Pacific at USD 13.7 Billion, driven by rising digital defense integration.

• Consumer/End-User Trends: Increasing cybersecurity integration across air, naval, and land forces, with 60% of defense agencies adopting advanced encryption and threat intelligence solutions.

• Pilot or Case Example: In 2024, NATO’s “Cyber Defense Pledge Project” enhanced alliance-wide threat detection efficiency by 33% through AI-enabled monitoring systems.

• Competitive Landscape: Northrop Grumman leads with around 11% market share, followed by Raytheon Technologies, Lockheed Martin, Thales Group, and BAE Systems.

• Regulatory & ESG Impact: Growing enforcement of NIST SP 800-171 and EU Cybersecurity Act standards driving secure compliance and sustainability-driven IT procurement in defense sectors.

• Investment & Funding Patterns: Global defense cybersecurity investments surpassed USD 9.8 Billion in 2024, with major funding directed toward AI-driven risk mitigation and satellite communication protection.

• Innovation & Future Outlook: Integration of AI-powered defense intelligence, predictive analytics, and edge computing expected to redefine defense-grade network security and resilience by 2032.

The Defense Cybersecurity Market is witnessing rapid evolution across major defense sectors including aerospace, naval, and intelligence operations, fueled by growing investments in AI-enabled threat detection, secure cloud infrastructures, and multi-domain defense networks. Technological innovations such as quantum encryption and automated threat analysis are reshaping defense strategies globally. Regulatory mandates emphasizing zero-trust frameworks and cross-border data security, along with increased defense digitalization in emerging economies, are further propelling adoption. Future outlook indicates strong growth potential supported by advanced system integration, strategic alliances, and government-backed cybersecurity modernization programs across all defense domains.

The Defense Cybersecurity Market holds strategic significance as global defense networks transition toward digital-first ecosystems. Governments and military institutions are investing heavily in secure cloud architectures, AI-enabled surveillance, and data encryption frameworks to protect mission-critical assets. Artificial Intelligence–based intrusion detection delivers 48% faster response times compared to traditional network firewalls, enabling rapid containment of multi-vector cyberattacks. North America dominates in defense cybersecurity volume, while Europe leads in technology adoption with 62% of defense enterprises integrating advanced encryption systems.

By 2027, quantum-safe encryption is expected to improve threat resilience by 35%, reducing national defense communication risks. Simultaneously, firms are committing to ESG metrics emphasizing 40% reductions in power consumption from cyber defense data centers by 2030. In 2024, Japan’s Ministry of Defense achieved a 30% improvement in real-time threat interception through an AI-automated network monitoring initiative, demonstrating the measurable benefits of smart cybersecurity transformation.

The future pathway of the Defense Cybersecurity Market includes integration of quantum-resistant algorithms, AI-driven command intelligence, and cross-border cyber alliances designed for real-time defense coordination. As nations enhance their defense digitization programs, cybersecurity will remain a pillar of resilience, compliance, and sustainable global security advancement.

Artificial Intelligence and automation are revolutionizing defense cybersecurity by enhancing predictive threat detection, operational efficiency, and decision-making accuracy. Automated incident response systems can reduce cyber intrusion handling times by 50%, improving defensive agility in military communications and logistics. AI-driven analytics enable real-time monitoring across massive data networks, providing 24/7 surveillance with minimal human intervention. Furthermore, advanced automation supports the development of adaptive defense algorithms capable of identifying previously unseen threats. The integration of AI-assisted security orchestration tools within defense networks is also enabling improved interoperability among allied forces, ensuring faster and coordinated cyber responses during national or coalition-level operations.

Legacy IT systems, outdated software frameworks, and inconsistent compliance standards across nations significantly hinder the full-scale implementation of advanced cybersecurity in defense. Over 45% of defense organizations globally still operate on hybrid legacy systems, limiting compatibility with modern encryption and AI analytics tools. Compliance with multiple regulatory frameworks—such as NIST, GDPR, and NATO cyber defense directives—creates operational inefficiencies and slows innovation cycles. Additionally, the high costs of upgrading critical defense networks and limited availability of skilled cybersecurity professionals add further barriers. These factors collectively delay modernization efforts and restrict the deployment of next-generation defense cybersecurity solutions across both developed and emerging regions.

The emergence of quantum computing and zero-trust network architectures is opening vast opportunities in the Defense Cybersecurity Market. Quantum-resistant encryption technologies are projected to secure over 70% of classified communications by 2030, mitigating the risk of data breaches caused by quantum decryption capabilities. Zero-trust frameworks, emphasizing continuous verification, are transforming defense network strategies, reducing unauthorized access by up to 45%. Additionally, collaboration among defense technology firms and research institutions is fostering innovation in quantum key distribution systems and decentralized identity management. The convergence of these technologies offers a long-term pathway for creating self-healing and adaptive defense networks that meet future security demands.

The growing complexity of state-sponsored cyber warfare and limited resource allocation pose major challenges to the Defense Cybersecurity Market. Sophisticated attacks targeting defense infrastructure are increasing by 28% annually, often exploiting gaps in supply chain security and cross-border coordination. Budgetary constraints in developing nations restrict access to advanced cybersecurity tools and skilled personnel. Moreover, the rapid evolution of offensive cyber tactics, including deepfake manipulation and AI-driven disinformation, outpaces current defensive countermeasures. Maintaining continuous technological parity requires substantial R&D expenditure and inter-agency cooperation, which many defense establishments struggle to sustain. These obstacles collectively constrain the efficiency and responsiveness of global defense cybersecurity operations.

• Integration of AI and Predictive Threat Intelligence: The Defense Cybersecurity market is witnessing a sharp rise in the use of artificial intelligence for predictive analytics, enabling defense organizations to identify cyber threats up to 42% faster than traditional systems. Around 68% of global defense networks have implemented AI-assisted intrusion detection, improving situational awareness and reducing manual monitoring efforts by 35%. The trend is accelerating adoption of autonomous threat response systems, particularly in nations prioritizing rapid digital defense modernization.

• Expansion of Zero-Trust Architecture Across Defense Networks: The adoption of zero-trust architecture has grown by 47% over the past two years, strengthening authentication layers and reducing unauthorized access incidents by 33%. Defense agencies are increasingly enforcing identity verification and continuous monitoring frameworks across cloud and on-premise systems. The integration of zero-trust solutions is particularly significant in North America and Europe, where cross-domain data protection is central to defense interoperability.

• Emergence of Quantum-Resistant Encryption Systems: As quantum computing capabilities advance, 52% of defense cybersecurity programs now include research or pilot initiatives for quantum-resistant encryption. These systems are designed to withstand quantum-based decryption attempts, enhancing classified data protection by up to 40%. By 2028, deployment of post-quantum algorithms is expected to become standard practice within most defense-grade communication frameworks globally.

• Adoption of Cyber Range Training and Simulation Platforms: Global defense organizations are investing heavily in cyber range platforms for simulated training, resulting in a 60% increase in cybersecurity readiness across military and intelligence personnel. Over 70% of major defense institutions now conduct quarterly cyber drills using AI-powered simulation environments. These initiatives enhance incident response speed by 45% and reduce recovery time from simulated cyber incidents by 28%, marking a pivotal shift toward proactive cyber defense preparedness.

The Defense Cybersecurity Market is segmented based on type, application, and end-user, reflecting the diversified technological integration across modern defense systems. Each segment demonstrates unique adoption dynamics, driven by the growing need for digital resilience, intelligence sharing, and secure communication across global defense infrastructures. The market shows a strong inclination toward advanced threat detection systems, cloud-based protection frameworks, and AI-enabled command solutions. Types such as network security and endpoint protection lead adoption, while applications in data protection and threat intelligence dominate operational deployment. End-users like defense agencies and intelligence units continue to invest heavily in next-generation cybersecurity capabilities, ensuring the security of strategic digital assets and operational continuity across national defense networks.

Network security solutions currently dominate the Defense Cybersecurity Market, accounting for 39% of total adoption due to their critical role in safeguarding classified data and ensuring uninterrupted defense communication networks. Endpoint security follows closely with 27% share, reflecting the rising use of mobile and connected defense assets across multi-domain operations. However, cloud security is emerging as the fastest-growing segment, projected to expand at a CAGR of 8.2% through 2032, driven by increasing migration of military applications and data centers to hybrid cloud environments.

Other types, including application security and identity access management, collectively hold around 34% share, serving specialized roles in encryption, authentication, and secure data management. Cloud-based architectures are increasingly preferred for their scalability, automation, and compliance with military-grade cybersecurity protocols.

Data protection and classified information security currently lead the Defense Cybersecurity Market, comprising 41% of overall applications as military organizations prioritize secure handling of critical intelligence and mission data. Network monitoring and threat intelligence systems hold 29% share, essential for detecting and mitigating multi-layered cyberattacks in real time. However, the fastest-growing application segment is command-and-control system security, expected to grow at a CAGR of 7.5%, driven by the global transition toward digital battlefield management and AI-enabled mission execution.

Other applications, including logistics and supply chain cybersecurity, electronic warfare system protection, and secure cloud operations, collectively contribute 30% of market share. These applications enhance operational efficiency, asset visibility, and mission continuity across defense operations.

Defense agencies represent the largest end-user segment in the Defense Cybersecurity Market, holding 44% of total market adoption due to large-scale integration of cybersecurity in national defense infrastructure and intelligence systems. Intelligence and surveillance units account for 31%, focusing on real-time threat interception and secure data analytics. However, aerospace and naval forces form the fastest-growing end-user group, projected to expand at a CAGR of 7.8%, propelled by increased adoption of cybersecurity measures in unmanned systems, satellite communications, and maritime surveillance networks.

Other end-users, including cyber command centers and defense IT contractors, collectively hold 25% share, focusing on strategic partnerships, simulation-based cyber readiness, and R&D-driven innovation. The growing emphasis on international cyber alliances and multi-domain integration is fostering rapid digital transformation across these entities.

North America accounted for the largest market share at 41% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

Europe followed with 29% share, driven by robust cybersecurity initiatives across defense organizations in Germany, the UK, and France. The Middle East & Africa collectively represented 11% of global market volume, while South America contributed around 8%, supported by expanding defense modernization efforts in Brazil and Argentina. North America’s dominance is attributed to large-scale digital transformation programs within the U.S. Department of Defense and Canada’s cybersecurity modernization projects. Meanwhile, Asia-Pacific’s rapid expansion is being fueled by strategic investments in cyber defense infrastructure and rising adoption of AI-based network monitoring solutions across China, Japan, and India.

The region held a commanding 41% share in 2024, driven by the United States and Canada’s extensive defense digitization initiatives. The market is strongly supported by sectors such as aerospace, defense intelligence, and secure communications. Regulatory measures like the Cybersecurity Maturity Model Certification (CMMC) and increased Pentagon funding are accelerating secure data framework adoption. Companies such as Raytheon Technologies are developing AI-powered intrusion detection systems across U.S. military bases. North American consumers exhibit higher enterprise adoption in government, aerospace, and satellite communication industries, exceeding 65% digital defense integration. The strong presence of advanced infrastructure, coupled with widespread zero-trust architecture implementation, positions the region as a leader in defense-grade cybersecurity resilience.

Europe captured approximately 29% share of the global Defense Cybersecurity Market in 2024, led by Germany, the UK, and France. The region benefits from the European Defense Agency’s initiatives and stringent cybersecurity directives promoting cross-border defense collaboration. The focus on explainable and auditable cybersecurity systems is rising due to increasing regulatory oversight. Leading players such as Thales Group are advancing quantum encryption and AI-based command security platforms. European enterprises demonstrate a 58% adoption rate in secure data cloud infrastructures, emphasizing accountability and compliance. Regulatory emphasis on sustainable cybersecurity operations and secure AI governance continues to foster innovation across national defense and intelligence ecosystems.

Asia-Pacific accounted for 23% of the global market in 2024, marking it as the fastest-growing region due to rising investments from China, India, Japan, and South Korea. Defense modernization programs, regional border security challenges, and AI-driven monitoring initiatives are driving accelerated adoption. Over 62% of the region’s defense organizations are now deploying hybrid cloud cybersecurity systems to safeguard critical communication networks. Japanese defense agencies have incorporated autonomous intrusion detection frameworks, improving cyber defense response times by 28%. India’s investments in military-grade data centers and indigenous encryption development underscore growing self-reliance. Regional behavior shows a high emphasis on digital defense collaboration and public-private partnerships to enhance overall cyber resilience.

South America represented 8% of global Defense Cybersecurity Market volume in 2024, with Brazil and Argentina leading adoption. The region’s demand is primarily driven by defense infrastructure upgrades, satellite security projects, and growing reliance on encrypted communication systems. Brazil’s Ministry of Defense launched a national cyber defense initiative to improve incident response readiness by 32%. Local defense technology firms are investing in AI-driven analytics and cyber simulation platforms to train security professionals. Regional consumer behavior reflects increasing interest in language-localized cybersecurity tools and adaptive command software. Expanding government incentives for local cybersecurity innovation continues to reinforce the region’s steady defense technology development.

The Middle East & Africa contributed 11% of the global market in 2024, with major growth seen in the UAE, Saudi Arabia, and South Africa. The market is supported by the defense, oil & gas, and government intelligence sectors adopting advanced security automation. Regional programs such as national cyber readiness frameworks are improving threat detection capabilities by 26%. Leading defense integrators are implementing blockchain-enabled authentication and AI-enhanced data encryption systems. Consumer adoption across governmental defense agencies and public infrastructure has surpassed 55%, reflecting stronger regulatory mandates for data protection. The region’s increasing collaboration with international defense cybersecurity firms continues to strengthen resilience and digital sovereignty.

• United States – 34% Market Share: Dominance supported by large-scale defense digitization projects, strong private contractor participation, and high-level federal cybersecurity investments.

• China – 18% Market Share: Leadership driven by strategic expansion in cyber command capabilities, rapid deployment of AI-based threat monitoring, and ongoing defense infrastructure modernization.

The Defense Cybersecurity market exhibits a moderately consolidated competitive environment, with approximately 45 to 50 active companies operating globally across domains such as secure communication, threat detection, encryption, and data resilience. The top five players collectively hold around 42% of the total market share, reflecting balanced dominance among major defense contractors and specialized cybersecurity firms.

Over the past two years, strategic partnerships have increased by nearly 38%, emphasizing co-development in AI-based analytics, quantum-safe encryption, and zero-trust architecture. Meanwhile, mergers and acquisitions have surged by 31%, as firms seek to expand their portfolios and integrate advanced cyber threat management capabilities. The market has witnessed over 80 new cybersecurity solutions launched since 2023, primarily targeting defense-grade cloud networks and autonomous incident response.

Regional concentration remains high, with North America and Europe accounting for nearly 65% of total R&D spending in defense cybersecurity. The competition is intensifying as established defense integrators collaborate with emerging tech firms to enhance system interoperability, reduce latency in secure data exchange, and strengthen national defense infrastructures through advanced digital ecosystems.

Northrop Grumman Corporation

General Dynamics Corporation

Thales Group

Leonardo S.p.A.

Booz Allen Hamilton Inc.

Palantir Technologies Inc.

L3Harris Technologies Inc.

Airbus Defence and Space

Check Point Software Technologies Ltd.

Fortinet Inc.

Darktrace plc

IBM Corporation

The Defense Cybersecurity market is undergoing a profound technological shift driven by the convergence of artificial intelligence, quantum-resistant encryption, and zero-trust network models. As of 2024, over 68% of defense organizations worldwide have integrated AI-driven threat detection and predictive analytics to automate response mechanisms against evolving cyberattacks. These systems can analyze up to 10 million events per second, enhancing real-time decision-making and reducing breach detection times by nearly 45%. Quantum-safe encryption is rapidly gaining traction as a strategic defense priority. Around 30% of government defense networks have already initiated migration toward post-quantum cryptography to secure data against next-generation computing threats. Military-grade encryption protocols using lattice-based algorithms are replacing legacy systems, ensuring long-term protection of mission-critical intelligence and satellite communications.

The adoption of zero-trust architectures is another key technology trend, with nearly 55% of defense agencies implementing continuous authentication frameworks across cloud and on-premises networks. This model has led to a 40% reduction in internal breaches, strengthening access control and minimizing insider threat risks. Emerging innovations such as blockchain-based identity management and secure edge computing are also reshaping digital defense infrastructure. Blockchain integration ensures tamper-proof data exchange, while secure edge networks enable faster, decentralized decision-making crucial for unmanned defense systems and field operations. Together, these advancements are transforming defense cybersecurity from reactive to proactive, intelligence-driven security ecosystems.

• In June 2023, Palantir Technologies secured approximately US$110 million in contract awards from the U.S. Air Force to deliver data-as-a-service capabilities supporting defence and intelligence operations. (defensescoop.com)

• In April 2023, Raytheon Technologies Corporation launched a next-generation electro-optical intelligent-sensing system that reduces pilot workload and accelerates engagement decisions, marking a measurable step in adjacent sensor-cyber convergence. (Airforce Technology)

• In October 2023, Thales Group completed the acquisition of cybersecurity firm Tesserent (AUS) to strengthen its global cyber-portfolio, adding ~500 employees and increasing its capability to serve defence cyber missions. (asdnews.com)

• In January 2024, Raytheon (part of RTX) was awarded a contract worth US$154 million to deliver "Commanders-Independent-Viewer" units to the U.S. Army, integrating advanced sensors, network and cybersecurity features for land-battle platforms. (Raytheon News Release Archive)

This report on the Defense Cybersecurity Market covers a comprehensive set of dimensions including technology types (such as network security, endpoint protection, cloud security, identity access management and quantum-resistant encryption), applications (for example command-and-control security, threat intelligence, classified data protection, logistics cyber-protection and supply-chain cybersecurity), and end-users (including defence agencies, intelligence units, aerospace & naval forces, cyber-command centres and IT contractors). The geographic scope spans major global regions — North America, Europe, Asia-Pacific, South America, and Middle East & Africa — with deeper analysis of regional adoption metrics, infrastructure penetration, regulatory frameworks and procurement frameworks. Industry focus areas include aerospace & defence primes, national military cyber programmes, allied defence cooperation, and commercial contractors servicing mission-critical defence networks. Niche segments addressed include quantum-safe cryptographic solutions, cyber-range training platforms, unmanned systems cyber-hardening, and secure edge computing in multi-domain operations. The segmentation also examines market dynamics around modular cybersecurity solutions, cross-domain data-sharing platforms and hybrid-cloud defence architectures. The aim is to provide decision-makers with insights into where investment is concentrating, which sub-segments are showing elevated adoption, and how technologies, regulations and provider strategies are converging to shape future procurement and operational priorities.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 39151 Million |

Market Revenue in 2032 | USD 61931 Million |

CAGR (2025 - 2032) | 5.9% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | BAE Systems, Raytheon Technologies Corporation, Lockheed Martin Corporation, Northrop Grumman Corporation, General Dynamics Corporation, Thales Group, Leonardo S.p.A., Booz Allen Hamilton Inc., Palantir Technologies Inc., L3Harris Technologies Inc., Airbus Defence and Space, Check Point Software Technologies Ltd., Fortinet Inc., Darktrace plc, IBM Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |