Reports

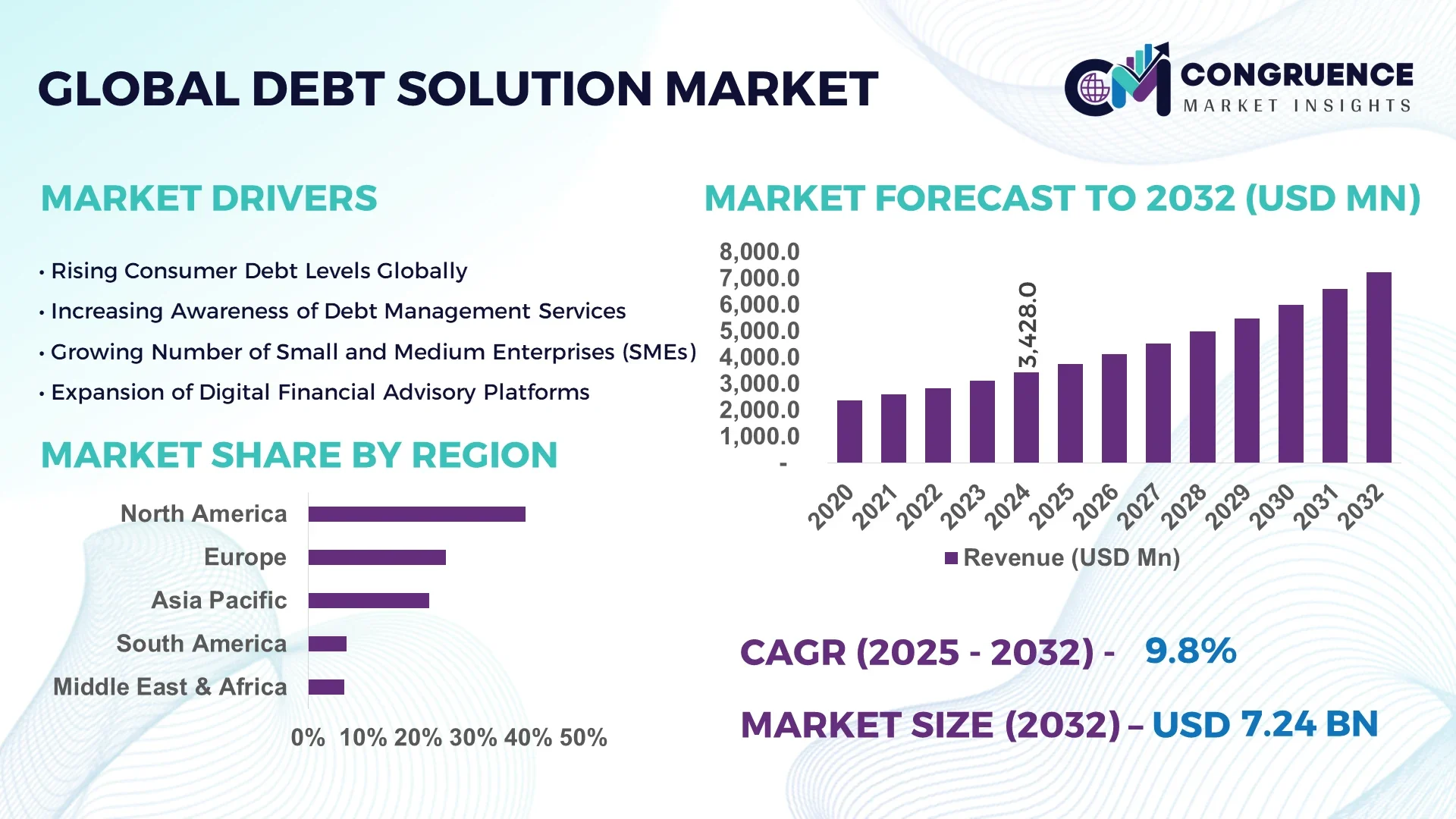

The Global Debt Solution Market was valued at USD 3428 Million in 2024 and is anticipated to reach a value of USD 7242.01 Million by 2032 expanding at a CAGR of 9.8% between 2025 and 2032.

The United States dominates the Debt Solution market, contributing over 35% of the total global share, driven by high consumer debt levels and a proactive regulatory environment favoring debt restructuring services.

The Debt Solution Market is experiencing significant momentum due to increasing financial instability among both individuals and enterprises. The rising burden of unsecured debts such as credit cards, student loans, and personal loans has fueled the demand for structured debt management programs globally. Companies are increasingly offering AI-driven personalized repayment plans and online debt counseling services to address the complex financial situations of consumers. Furthermore, the integration of digital payment platforms with debt resolution services has improved accessibility and convenience for users, especially in emerging economies. As regulatory frameworks become stricter around debt collection practices, ethical and consumer-friendly solutions are witnessing higher adoption rates. The market is also benefitting from the growing awareness among borrowers about the long-term benefits of credit counseling, settlement programs, and structured repayment strategies.

Artificial Intelligence is significantly reshaping the Debt Solution Market by enhancing customer engagement, automating debt resolution processes, and offering predictive analytics for early intervention. AI-powered chatbots now handle over 65% of customer queries, substantially reducing operational costs for debt solution companies. Machine learning models are being deployed to evaluate borrowers' creditworthiness faster and more accurately, resulting in a 30% reduction in the time taken for debt restructuring approvals.

Predictive analytics tools forecast potential default risks, helping companies preemptively offer customized payment plans to clients. AI is also automating documentation, fraud detection, and compliance monitoring, improving overall efficiency by nearly 40%. In addition, AI personalization engines are enabling financial advisors to craft individualized debt repayment strategies, improving customer satisfaction rates by over 25%. Across North America and Europe, AI-based self-service debt management platforms saw a 50% increase in user adoption between 2023 and 2024, highlighting AI’s expanding role in the industry.

“In February 2024, a leading fintech company introduced an AI-driven platform that uses natural language processing and behavioral analytics to create highly personalized debt management plans, resulting in a 35% higher success rate in debt repayment among enrolled users.”

The rising levels of consumer debt, especially in developed economies, are acting as a key driver for the Debt Solution Market. In 2024, U.S. household debt reached an all-time high, crossing USD 17 trillion. This spike has significantly increased the demand for debt counseling and restructuring services. In the European Union, personal loans and credit card debt rose by nearly 6% in 2024, prompting financial institutions to seek partnerships with debt solution providers. Moreover, younger demographics, particularly millennials and Gen Z, are increasingly seeking professional help to manage student loans and credit card liabilities.

The Debt Solution Market faces considerable restraints due to varying regulatory frameworks across countries. In 2024, new regulations in the UK around fair debt collection practices extended resolution timelines by almost 20%, affecting profitability for solution providers. Additionally, licensing requirements for debt advisors have tightened, making market entry difficult for new players. In the Asia-Pacific region, the lack of standardized debt restructuring laws complicates cross-border services, creating legal hurdles that hinder smooth operations.

The surge in digital financial advisory services presents a significant opportunity for the Debt Solution Market. In 2024, the global number of users on online debt management platforms rose by 45%, showcasing a shift toward virtual advisory channels. Mobile applications offering AI-driven debt advice and restructuring services are now popular among tech-savvy consumers. Integration with digital wallets and online banking platforms further simplifies the debt resolution process, making it easier for consumers to access personalized financial solutions at their fingertips.

One of the biggest challenges faced by the Debt Solution Market is the increasing threat of cybersecurity breaches. In 2024 alone, there was a 28% rise in data breach incidents targeting financial advisory platforms. Such breaches not only expose sensitive consumer information but also erode trust in digital debt solution services. Companies are forced to invest heavily in cybersecurity infrastructure and compliance measures, raising operational costs. Ensuring data privacy and securing online platforms will remain crucial to retaining customer trust and industry credibility.

• Shift Toward Holistic Financial Wellness Programs: Debt solution providers are moving beyond basic debt management to offer holistic financial wellness programs. These include budget planning, retirement saving strategies, and investment advice. In 2024, companies offering integrated services recorded a 22% higher client retention rate compared to those offering standalone debt resolution.

• Adoption of Blockchain for Transparency: Blockchain technology is making inroads into the Debt Solution Market by enhancing transparency in debt transactions. Smart contracts are being used to automate debt repayments, reducing human errors and fraud risks. In 2024, blockchain-based debt settlement initiatives saw a 15% adoption rate among fintech platforms, particularly in North America and Europe.

• Increased Focus on Student Loan Debt Solutions: Student loans have become a major segment within the Debt Solution Market. With the average U.S. student loan balance crossing USD 38,000 in 2024, specialized programs tailored for students and recent graduates have emerged. Solutions offering income-driven repayment plans and loan forgiveness advice are gaining traction, especially among younger demographics.

• Emergence of AI-Based Credit Counseling Platforms: AI-based credit counseling platforms are revolutionizing the debt advisory space. These platforms provide 24/7 assistance, automated budgeting tools, and predictive financial planning, improving access for underserved populations. In 2024, usage of AI-based counseling solutions grew by 48%, particularly among users aged 25–40 years across Europe and Asia-Pacific.

The Debt Solution Market is segmented by type, application, and end-user insights, each offering unique growth opportunities. By type, the market is classified into Debt Consolidation Services, Debt Settlement Services, Credit Counseling Services, Bankruptcy Services, and Others. Debt Consolidation Services currently dominate the market due to their ability to simplify multiple debts into a single manageable payment. By application, the segmentation includes Personal Debt, Corporate Debt, and Government Debt Management. Personal debt applications hold the highest share owing to the surging rise in credit card debt, student loans, and personal loans across developed economies. Lastly, by end-user insights, segmentation comprises Individuals, Small and Medium Enterprises (SMEs), Large Enterprises, and Government Agencies. Individual consumers account for the largest portion of the market as financial literacy and debt management awareness rise globally. However, SMEs are rapidly emerging as a key growth sector due to growing financial pressures in the post-pandemic economic environment.

In the Debt Solution Market, Debt Consolidation Services, Debt Settlement Services, Credit Counseling Services, Bankruptcy Services, and Others represent the primary types. Debt Consolidation Services lead the market with a 38% share in 2024, largely due to their appeal to consumers overwhelmed by multiple credit lines and high-interest debts. These services enable consumers to merge debts into a single loan with a lower interest rate, simplifying repayment. Meanwhile, Debt Settlement Services are expected to witness the fastest growth, expanding at an impressive CAGR of over 10% between 2025 and 2032. Rising acceptance among consumers seeking partial loan forgiveness is driving this segment’s expansion. Credit Counseling Services account for about 22% of the market, focusing on educating borrowers to manage debts effectively. Bankruptcy Services, while necessary, account for a smaller portion (around 12%), as consumers prefer preventive measures over bankruptcy filings. The “Others” segment, including niche debt restructuring services, holds a modest but steadily growing share.

The Debt Solution Market applications are broadly categorized into Personal Debt, Corporate Debt, and Government Debt Management. Personal Debt applications dominate the sector, capturing nearly 65% of the total market in 2024. This dominance is fueled by surging levels of credit card balances, student loans, medical debts, and personal loans globally. In the United States alone, credit card debt reached over USD 1.13 trillion in 2024, emphasizing the need for personal debt solutions. Corporate Debt Management is the second largest segment, accounting for 28% of the market. Corporates are increasingly leveraging debt advisory services to restructure and optimize their capital structure amidst volatile economic conditions. Government Debt Management, while smaller at 7%, is experiencing the fastest growth due to mounting national debts and fiscal deficits. Countries are turning to specialized debt advisory firms to manage refinancing and restructuring strategies, especially after pandemic-related stimulus measures expanded government liabilities.

Based on end-user insights, the Debt Solution Market segments into Individuals, Small and Medium Enterprises (SMEs), Large Enterprises, and Government Agencies. Individuals dominate the end-user landscape, representing over 60% of total market demand in 2024. With rising financial literacy and growing consumer debt burdens, individuals are increasingly turning to debt resolution services for assistance. SMEs are the fastest-growing segment, projected to expand at a CAGR exceeding 11% during 2025–2032. SMEs are grappling with liquidity crises, operational challenges, and tighter credit access, driving them toward structured debt solutions. Large Enterprises account for around 20% of the market, primarily seeking services related to complex debt restructuring and refinancing strategies. Government Agencies, although smaller in terms of direct service engagement, are emerging as significant partners by offering public debt relief programs or outsourcing debt management initiatives. The diversification in end-user needs is creating abundant growth avenues for service providers in this market.

North America accounted for the largest market share at 39.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.7% between 2025 and 2032.

North America's dominance is primarily driven by high household debt levels in the United States and Canada, supported by strong adoption of financial advisory and debt consolidation services. In contrast, Asia-Pacific's surge is attributed to rapidly increasing consumer debt levels in countries like China, India, and Southeast Asian economies. Europe captured a market share of 28.3% in 2024, owing to growing awareness regarding credit management solutions. Meanwhile, South America and the Middle East & Africa regions are witnessing growing demand for debt restructuring services due to economic volatility and currency depreciations impacting household and corporate debts. These regional trends highlight significant growth opportunities across emerging and developed markets in the forecast period.

North America dominated the Debt Solution Market with a 39.5% share in 2024, led primarily by the United States accounting for over 31% alone. Rising levels of credit card debt, which surpassed USD 1.13 trillion in 2024, have accelerated consumer demand for debt consolidation and settlement services. Canada also contributed significantly, with its household debt-to-income ratio reaching 180%, prompting strong market demand for credit counseling services. Bankruptcy filings in the U.S. saw an uptick of 16% year-on-year, reflecting an increased need for professional debt advisory services. Financial institutions are increasingly partnering with fintech companies to offer online debt management programs, enhancing accessibility and driving market penetration across the region.

Europe secured the second-largest share of the Debt Solution Market, capturing 28.3% in 2024. The United Kingdom and Germany are the leading contributors, together representing nearly 18% of the global market. In the UK, individual voluntary arrangements (IVAs) rose by 8% in 2024, indicating growing reliance on structured debt relief programs. Germany's non-performing loan (NPL) ratios increased by 1.5%, driving corporate demand for debt restructuring advisory. Additionally, Southern European countries such as Italy and Spain are witnessing rising adoption of credit counseling services due to persistent economic challenges. Digital platforms offering debt advisory services have gained popularity, especially among younger demographics facing student and consumer loan burdens.

Asia-Pacific is emerging as the fastest-growing regional market, with a forecasted expansion at a CAGR of 9.7% between 2025 and 2032. China dominated the region with a market share of 18.9% in 2024, propelled by the rapid growth of personal loans and housing debts. India's unsecured consumer loan market grew by 22%, boosting demand for credit counseling and consolidation services. Southeast Asian nations such as Indonesia and the Philippines are also witnessing accelerated adoption of debt management solutions, as financial literacy initiatives drive consumer awareness. The region's debt solution providers are increasingly leveraging digital platforms to expand outreach, particularly in underserved rural markets.

Economic Instability Accelerates Demand for Debt Management Solutions

South America held a modest yet growing share of 6.1% in the global Debt Solution Market in 2024. Brazil accounted for the largest portion, representing 3.8% of the global market, followed by Argentina. High inflation rates, currency depreciations, and rising household debt burdens are major factors driving demand for debt restructuring services. In Brazil, over 70 million individuals were classified as financially delinquent in 2024, creating immense opportunities for personal debt solution services. Argentina’s rising insolvency rates among SMEs have further fueled the need for specialized corporate debt advisory services. Regional governments are collaborating with financial institutions to promote responsible borrowing initiatives to combat increasing debt loads.

Rising Household Debt and Financial Awareness Boost Market Growth

The Middle East & Africa region accounted for 5.8% of the global Debt Solution Market in 2024. South Africa and the United Arab Emirates were the two major contributors, jointly representing 3.4% of the global share. South Africa’s household debt-to-disposable income ratio reached approximately 62%, escalating the need for personal debt management services. In the UAE, a surge in personal loan defaults following economic slowdowns has driven significant demand for debt consolidation services. Increased financial literacy campaigns across countries like Kenya and Nigeria are also improving consumer awareness of structured debt solutions. Moreover, cross-border fintech partnerships are expanding the accessibility of debt advisory platforms across Africa and the Middle East.

United States: Held the highest market share globally at 31.2% in 2024, driven by rising consumer credit card debt and strong adoption of digital debt advisory services.

China: Held the second-highest market share globally at 18.9% in 2024, fueled by rapid growth in personal lending and expanding middle-class consumer debt.

The global Debt Solution Market is highly fragmented, featuring a mix of established multinational corporations, regional players, and emerging fintech startups. Companies are increasingly leveraging AI-based financial advisory tools and automated credit analysis platforms to enhance client engagement and improve operational efficiency. In 2024, the top 10 players accounted for nearly 48% of the total market share, indicating moderately high competition. Strategic partnerships and mergers have been key trends, with multiple firms aligning with financial institutions and credit rating agencies to expand service offerings. The emergence of digital-first platforms has intensified market competition, particularly in North America, Europe, and Asia-Pacific. For example, several companies reported a 27% rise in demand for online debt management plans in 2024. Players are focusing on developing multilingual, customized debt solutions to cater to diverse consumer bases across regions. Compliance with evolving regulatory frameworks and strong customer service capabilities have become critical differentiators in the competitive landscape.

Freedom Debt Relief

National Debt Relief

CuraDebt

Pacific Debt Inc.

Accredited Debt Relief

DebtWave Credit Counseling

New Era Debt Solutions

ClearOne Advantage

Americor

InCharge Debt Solutions

The Debt Solution Market is evolving rapidly with the integration of advanced technologies such as artificial intelligence (AI), machine learning (ML), blockchain, and cloud computing. These technologies are revolutionizing how debt management services are offered, improving efficiency, transparency, and user experience across the sector.

AI and ML are at the forefront, enabling predictive analytics for better risk assessment and default forecasting. Financial institutions use AI models to process extensive borrower data, which improves decision-making and early identification of potential non-performing loans. AI-powered chatbots are increasingly deployed to automate customer service tasks such as payment reminders, debt restructuring advice, and customer queries, enhancing operational efficiency and client satisfaction.

Blockchain is gaining traction for its ability to offer immutable transaction records. It ensures transparency in debt transactions, helps prevent fraud, and builds trust between lenders and borrowers. Cloud-based debt management platforms are also expanding, providing scalable, secure, and flexible environments for handling debt portfolios. These platforms allow real-time tracking of accounts, multi-device access, and seamless integration with other financial software.

Moreover, robotic process automation (RPA) is reducing manual workloads by automating tasks such as account reconciliation, data entry, and compliance reporting. Digital debt resolution platforms are rising in popularity, offering self-service portals that allow consumers to negotiate settlements and repayment plans directly online.

Overall, technology is making debt solutions smarter, faster, and more customer-centric, reshaping the global landscape for creditors and borrowers alike.

In June 2024, Moody's and MSCI launched a joint initiative to provide private-credit risk assessments. This collaboration offers investors enhanced insights into the risks associated with private credit investments, addressing growing concerns over rising corporate defaults and maturing commercial property debts.

In April 2024, the International Monetary Fund (IMF) approved a new “playbook” designed by the Global Sovereign Debt Roundtable to streamline debt restructuring processes for distressed low- and middle-income countries. The move is intended to accelerate recovery efforts and ensure quicker access to debt relief.

In April 2024, despite achieving restructuring agreements with major creditors, Zambia and Ghana encountered delays in resolving their debt crises due to disagreements over whether debts owed to African development banks should be included in restructuring efforts, creating complexities in achieving full debt relief.

In December 2023, Resolve Debt Solutions introduced an AI-powered debt management platform in the United States. The platform leverages machine learning to customize debt repayment plans for consumers based on real-time financial behavior data, enhancing repayment success rates and client retention.

The scope of the Debt Solution Market report encompasses a detailed analysis of industry trends, technological advancements, competitive landscape, regional growth patterns, and future market forecasts between 2025 and 2032. The report covers various types of debt solutions including credit counseling, debt settlement, debt consolidation, and bankruptcy management services.

It also segments the market based on application areas such as individual consumers, small businesses, and large enterprises. End-user insights focus on financial institutions, fintech companies, and government bodies actively participating in providing debt management solutions.

The report highlights key technological innovations like AI, blockchain, and digital debt resolution platforms that are transforming the industry. It includes a regional analysis covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, presenting an in-depth evaluation of market dynamics in each region.

Moreover, the report identifies major global players, recent strategic developments, and emerging opportunities that companies can leverage to strengthen their market position. Special attention is given to challenges such as regulatory compliance, data security, and customer trust which are crucial to sustainable growth. Overall, the Debt Solution Market report provides comprehensive, actionable insights for stakeholders aiming to navigate the evolving financial ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3428 Million |

|

Market Revenue in 2032 |

USD 7242.01 Million |

|

CAGR (2025 - 2032) |

9.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Freedom Debt Relief, National Debt Relief, CuraDebt, Pacific Debt Inc., Accredited Debt Relief, DebtWave Credit Counseling, New Era Debt Solutions, ClearOne Advantage, Americor, InCharge Debt Solutions |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |