Reports

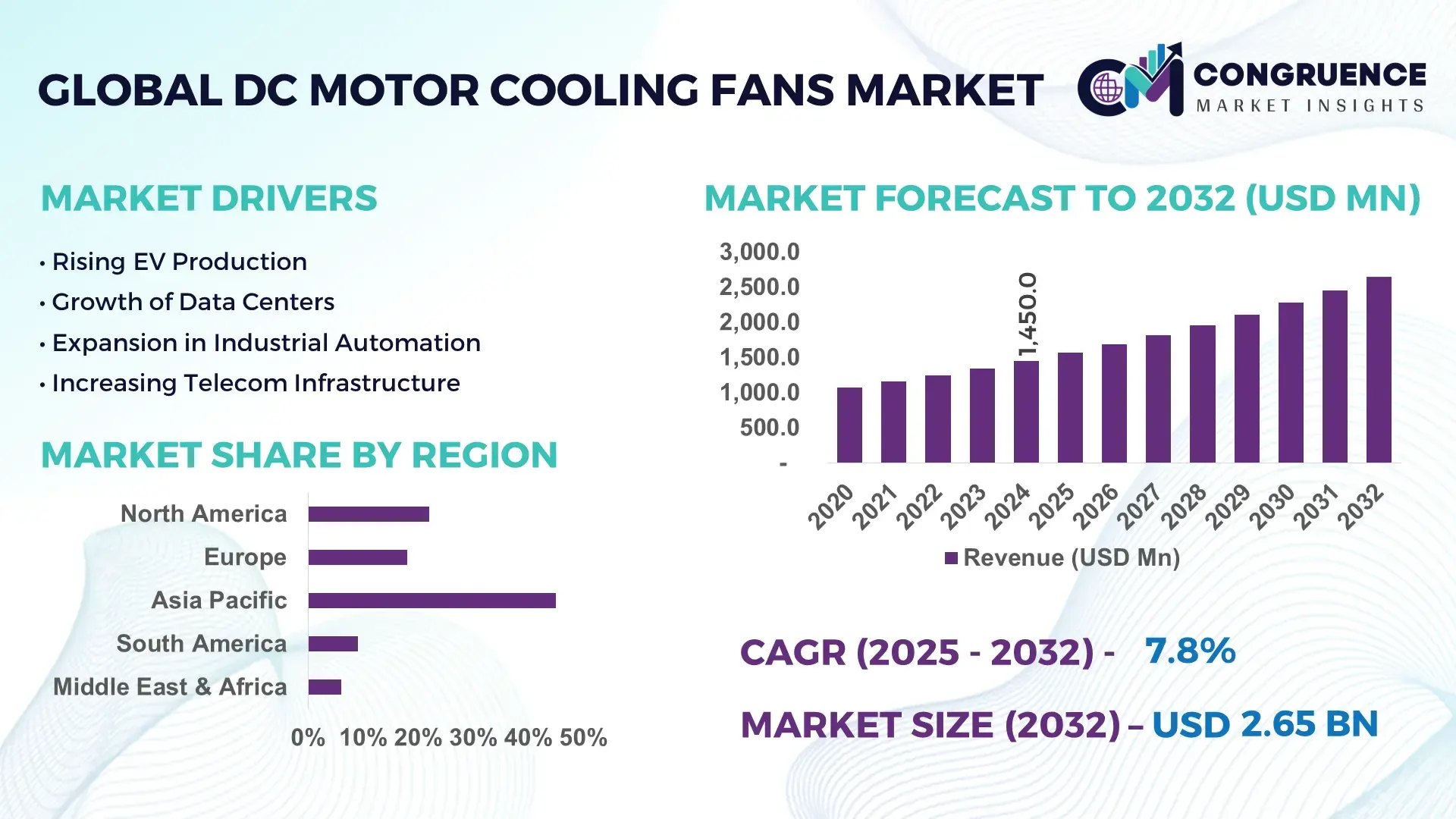

The Global DC Motor Cooling Fans Market was valued at USD 1,450.0 Million in 2024 and is anticipated to reach USD 2,648.3 Million by 2032, expanding at a CAGR of 7.82% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by the rising demand for efficient thermal management solutions in compact electronic devices.

In China, which dominates the DC motor cooling fans industry, manufacturers have ramped up production capacity to over 800 million units annually, supported by investments of around USD 2.2 billion in automation and brushless DC (BLDC) technology. The country’s strong manufacturing base services key applications in telecommunications, data centers, and electric vehicles, and innovation is ongoing — Chinese firms are introducing PWM-controlled and high-airflow axial fans that reduce power consumption by up to 15% while improving service life.

Market Size & Growth: Valued at USD 1,450 M in 2024, projected to reach USD 2,648 M by 2032, with a CAGR of 7.82%, underpinned by growing electronics and EV applications.

Top Growth Drivers: Energy efficiency improvements (~60 %), miniaturization of electronic devices (~45 %), and rising EV adoption (~35 %).

Short-Term Forecast: By 2028, performance gains are expected to result in a 12% reduction in power consumption for next-generation DC cooling fans.

Emerging Technologies: Brushless DC (BLDC) motors; PWM speed control; integration with IoT/smart thermal control systems.

Regional Leaders: Asia-Pacific: ~USD 1,100 M by 2032 due to electronics manufacturing; North America: ~USD 850 M by 2032 led by data center deployments; Europe: ~USD 450 M by 2032 fueled by industrial automation.

Consumer/End‑User Trends: High adoption in telecom (35%), data centers (30%), EV thermal systems (20%), and industrial electronics (15%).

Pilot / Case Example: In 2023, a major data‑center operator in the U.S. tested BLDC fans, achieving a 9% reduction in server rack cooling power consumption.

Competitive Landscape: Leading company holds ~18% share; other major players include Delta Electronics, Nidec, Sunon, and Sanyo Denki.

Regulatory & ESG Impact: Stricter energy-efficiency standards and carbon‑reduction targets are pushing adoption of low-power DC fans.

Investment & Funding Patterns: Over USD 330 M invested in R&D and capacity expansion globally in 2023, with rising venture funding for smart cooling technologies.

Innovation & Future Outlook: Trends include integration with AI-based thermal control, high-speed compact BLDC motors, and modular fan assemblies for scalable cooling.

DC motor cooling fans are increasingly used in telecom, data centers, EVs, and industrial automation. Technological advances like BLDC motors and speed control are driving innovation, while regulatory push toward energy efficiency and regional manufacturing growth are supporting strong future prospects.

The strategic relevance of the DC Motor Cooling Fans Market lies in its critical role in thermal management for high-growth sectors such as data centers, telecommunications infrastructure, and electric vehicles. As electronics shrink and power densities escalate, efficient DC cooling fans ensure reliability, reduce downtime, and extend the lifespan of sensitive components.

Emerging PWM‑controlled BLDC fans deliver up to 12% improvement in energy efficiency compared to traditional brushed DC fans. Regionally, Asia-Pacific dominates in volume, powered by large-scale electronics manufacturing, while North America leads in adoption, with over 40% of enterprise data centers already integrating advanced DC cooling solutions.

In the short term, by 2027, smart fan systems using IoT and AI-based thermal control are projected to improve cooling performance metrics—like airflow precision—by 15–20%, reducing overcooling and power waste. From an ESG perspective, leading firms are targeting a 30% reduction in lifecycle carbon emissions in fan production by 2030, leveraging recyclable materials and energy-efficient motor architectures.

A real-world example: in 2024, a major EV OEM in Europe deployed a novel BLDC fan design that reduced in-vehicle thermal management power draw by 8%, improving overall energy efficiency of their battery cooling module. Such micro-optimizations can translate to significant gains at scale.

Looking ahead, the DC Motor Cooling Fans Market is poised to be a pillar of resilience and sustainable growth, enabling companies to comply with tight energy regulations, support high-performance electronics, and scale thermal systems in a resource-constrained world.

The DC Motor Cooling Fans Market is evolving rapidly, driven by increasing demand for compact, energy-efficient cooling solutions across sectors such as telecom, EVs, data centers, and industrial electronics. Miniaturization of electronic devices and rising power densities are pushing thermal management challenges higher, making DC fans more critical for maintaining system reliability. On the supply side, manufacturers are pushing innovation in BLDC motor designs, intelligent control systems, and noise-optimized blades. These dynamic forces combine to propel market growth, but competition is intensifying, regulatory pressure on energy efficiency is mounting, and cost pressures remain non-trivial as companies scale up production globally.

Data centers are among the most temperature-sensitive environments, and as cloud computing expands, their cooling needs have surged. DC cooling fans offer precise speed control, low noise, and higher energy efficiency compared to AC alternatives. Many data centers now deploy BLDC fans to manage airflow in server racks, shrinking cooling overhead. With rack power densities increasing to over 30 kW per rack, DC fans become indispensable. Their ability to regulate speed dynamically based on temperature enables up to 15% energy savings on cooling power, improving overall PUE (Power Usage Effectiveness) for operators. This rising demand from the data center sector is a major driver for the DC Motor Cooling Fans Market.

Although DC cooling fans, especially those with BLDC motors and PWM control, provide long-term efficiency benefits, their upfront costs remain significantly higher than traditional AC fans. For small and mid‑sized manufacturers or low-margin applications, this cost premium can be a barrier. In addition, integration with smart control electronics adds BOM (bill of materials) complexity and requires added design validation. In cost-sensitive sectors like consumer appliances or entry-level telecom equipment, the value proposition of lower energy draw is often offset by longer payback periods. These factors slow down the pace of adoption, particularly in regions where CAPEX constraints are tight and price sensitivity is high.

Electric vehicles (EVs) are emerging as a high-potential opportunity for DC motor cooling fans. As EV battery packs and power electronics generate more heat, they require compact, high-efficiency fans to maintain optimal operating temperatures. DC cooling fans, especially BLDC models, can offer up to 10–12% better energy efficiency compared to brushed alternatives, reducing parasitic power loss in battery thermal systems. Furthermore, integration of smart control (e.g., via PWM or IoT sensors) enables dynamic thermal regulation based on driving condition and ambient temperature, extending battery life and improving vehicle range. As the global EV fleet continues to scale, demand for these advanced cooling solutions could grow sharply.

The DC Motor Cooling Fans Market faces significant supply-chain challenges due to reliance on specialized components such as high-grade magnets, precision motor bearings, and electronic control modules. Manufacturing BLDC motors at scale requires tight tolerances and consistent materials, which can be disrupted by raw material volatility (e.g., rare earth magnet supply) or geopolitical risks. In addition, variability in component sourcing can increase lead times and manufacturing costs. For manufacturers scaling globally, aligning suppliers across regions—and ensuring quality—adds logistical and financial complexity. These challenges contribute to production bottlenecks and may delay capacity build-out in new geographies.

Increasing adoption of BLDC with PWM control: The use of brushless DC motors along with PWM (pulse width modulation) for variable-speed control has surged, leading to up to 14% reduction in average electricity consumption in telecom and data center applications.

Smart & predictive thermal management systems: Integration of IoT-enabled temperature sensors and AI-based predictive control logic is becoming mainstream; up to 25% of new DC fan systems now include smart feedback loops that optimize speed and reduce overcooling.

Miniaturization for high-density electronics: As devices shrink and power density increases, demand for mini DC cooling fans (under 50 mm) has risen by 20% year-on-year, especially in edge computing and micro‑datacenter segments.

Sustainability-driven design: More than 30% of new DC cooling fans launched in 2024 used recyclable plastic housings and energy-efficient motor materials, in line with ESG goals and stricter regulatory standards.

The DC Motor Cooling Fans Market is organized into multiple layers of segmentation that provide insights into product types, applications, and end-user utilization. By type, the market is primarily divided into axial, centrifugal, and mixed-flow DC cooling fans, each designed to meet specific airflow, pressure, and efficiency requirements. Application-wise, segments include telecommunications, data centers, electric vehicles, industrial automation, and consumer electronics, reflecting the varied thermal management demands across industries. End-users range from large-scale data centers and EV manufacturers to industrial facilities and telecom operators, highlighting the diverse adoption patterns. Notably, adoption in high-density electronics is increasing, while industrial automation shows steady integration. Regional preferences further influence market segmentation, with Asia-Pacific showing higher production volumes and North America leading in advanced application adoption. Consumer trends such as demand for energy efficiency and compact fan designs are increasingly shaping product offerings and influencing manufacturing priorities.

Axial DC cooling fans currently lead the market, accounting for approximately 55% of adoption due to their simple design, high airflow efficiency, and broad applicability across electronics, telecom, and automotive sectors. Centrifugal fans hold roughly 25% of the market, preferred in high-pressure, compact applications requiring targeted airflow. Mixed-flow fans contribute the remaining 20%, offering a balance of airflow and pressure for niche applications such as precision cooling in specialized industrial electronics. The fastest-growing type is centrifugal fans, driven by increasing deployment in electric vehicles and high-density server racks, which require precise airflow management to optimize cooling efficiency and reduce energy consumption.

The telecommunications segment currently dominates, accounting for approximately 40% of adoption of DC motor cooling fans, driven by growing infrastructure expansion and increased equipment density. The fastest-growing application is electric vehicles (EVs), which require high-efficiency, compact cooling solutions for battery packs and power electronics, with adoption projected to rise rapidly over the next several years. Data centers contribute 30%, while industrial automation and consumer electronics together make up the remaining 30%. In 2024, more than 38% of global enterprises reported piloting DC cooling fans in advanced telecom and data infrastructure to optimize thermal performance.

Large-scale data centers currently represent the leading end-user segment, accounting for 35% of adoption, due to the high thermal demands of densely packed server racks and network equipment. The fastest-growing end-user segment is electric vehicle manufacturers, supported by increasing EV production and the need for efficient battery and power electronics cooling, currently representing 25% adoption. Other end-users, including industrial plants, consumer electronics producers, and telecom operators, make up the remaining 40%, reflecting diverse integration of DC cooling fan solutions. In 2024, over 60% of telecom operators in Asia-Pacific upgraded to energy-efficient DC fans for network hubs to reduce operational energy consumption.

Asia-Pacific accounted for the largest market share at 45% in 2024, however, Region North America is expected to register the fastest growth, expanding at a CAGR of 7.5% between 2025 and 2032.

In 2024, Asia-Pacific recorded a production volume of over 820 million DC motor cooling fans, driven by high manufacturing density in China, Japan, and India. North America deployed approximately 150 million units, led by data centers and EV battery cooling systems. Europe contributed 20% of the total market volume, with Germany, the UK, and France as key adopters. South America and the Middle East & Africa combined accounted for 15%, fueled by telecom expansion and industrial modernization. Regional infrastructure upgrades, regulatory energy-efficiency mandates, and increasing demand for thermal management in high-density electronics are driving deployment across all regions.

North America captured approximately 25% market share in 2024. Key industries driving demand include data centers, telecommunications, EVs, and industrial automation. Regulatory support, such as stricter energy-efficiency standards for electronic equipment, has accelerated adoption. Technological advancements like BLDC motors with IoT-enabled predictive control are prominent, with leading players like Delta Electronics U.S. investing in smart fan systems to optimize airflow and energy efficiency. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, with organizations prioritizing low-noise, high-efficiency thermal solutions. Digital transformation in manufacturing and intelligent thermal monitoring are further increasing deployment in commercial and industrial applications.

Europe accounted for 20% of the DC motor cooling fans market in 2024, with Germany, the UK, and France as the primary markets. Regulatory pressure from EU energy efficiency directives and sustainability initiatives has driven the adoption of energy-efficient fans. Emerging technologies like PWM-controlled BLDC fans and AI-integrated thermal management are being increasingly implemented. European players, such as Ebmpapst Germany, focus on developing high-efficiency axial fans for industrial and data center applications. Regional consumer behavior demonstrates a strong preference for compliance-driven, explainable cooling solutions in industrial and commercial sectors, enhancing market uptake and innovation.

Asia-Pacific leads the market with a 45% share in 2024, with top consuming countries including China, Japan, and India. The region shows strong infrastructure and manufacturing growth, supporting the production of over 820 million DC motor cooling fans annually. Technology innovation hubs in China and Japan are introducing BLDC fans with higher airflow efficiency and lower energy consumption. Local players, such as Sunon Group, are investing in smart, IoT-enabled cooling systems for telecom, data centers, and automotive sectors. Regional consumer trends indicate growth driven by e-commerce, mobile AI applications, and rapidly expanding industrial electronics, fueling consistent demand.

South America accounted for 9% of market share in 2024, with Brazil and Argentina as leading countries. Infrastructure upgrades, energy sector expansion, and industrial modernization are key growth drivers. Government incentives for energy-efficient solutions have promoted adoption in telecom and industrial manufacturing. Local player Ventisol Brazil has introduced high-efficiency axial fans for industrial cooling applications, enhancing system reliability. Consumer behavior shows preference for media and localized telecom solutions, which is boosting demand for compact, efficient DC cooling fans tailored to regional applications and environmental conditions.

Middle East & Africa accounted for 6% of the global market in 2024, with major growth countries including UAE and South Africa. Regional demand is driven by oil & gas, construction, and industrial applications requiring high-efficiency thermal management. Technological modernization includes BLDC fans and smart airflow monitoring systems. Companies such as Delta Electronics UAE are deploying advanced cooling solutions in large industrial plants. Consumer behavior reflects the adoption of durable, low-maintenance fans to handle high temperatures and industrial workloads, supporting consistent regional market growth and modernization.

China – 35% Market Share: High production capacity and strong demand from electronics, EV, and industrial sectors.

United States – 25% Market Share: Strong end-user demand in data centers, EVs, and industrial automation, supported by regulatory incentives and technological adoption.

The DC Motor Cooling Fans Market exhibits a moderately fragmented competitive environment, with over 120 active global competitors engaged in production, R&D, and regional expansion. The top five companies collectively account for approximately 58% of the global market, indicating a competitive yet concentrated presence among leading players. Market leaders emphasize technological innovation, strategic partnerships, and product portfolio expansion to maintain their positions. For instance, leading manufacturers are increasingly focusing on BLDC fans, IoT-enabled smart cooling systems, and energy-efficient axial and centrifugal designs. Strategic initiatives include collaborations between component suppliers and data center operators, regional production facility expansions, and launch of specialized EV battery cooling fans. Innovation trends include integration of predictive thermal management systems, quieter operation designs for commercial use, and high-speed miniature fans for telecom and industrial automation. New entrants are leveraging niche applications, including precision cooling in edge computing, to gain footholds, while incumbents strengthen their brand presence through sustainable and energy-efficient product offerings. Overall, competition is defined by rapid technological evolution, regional production capacity, and adoption of smart thermal solutions.

Sanyo Denki Co., Ltd.

Ebmpapst Germany

EBM-Papst North America

Orion Fans

The DC Motor Cooling Fans Market is increasingly shaped by advanced technological developments aimed at enhancing energy efficiency, airflow precision, and digital integration. Brushless DC (BLDC) motors dominate high-performance applications, offering superior reliability and reduced maintenance compared to brushed motors. Pulse Width Modulation (PWM) control systems allow precise fan speed adjustments based on real-time thermal load, reducing power consumption by up to 15% in high-density server racks. IoT-enabled smart fans equipped with temperature and humidity sensors provide predictive thermal management, enabling automated airflow adjustments in telecom and data center environments. Miniaturized axial and centrifugal fans are gaining traction for compact devices, with over 20% year-on-year adoption in edge computing and EV battery modules. Emerging technologies include integration with AI-based predictive maintenance systems and hybrid cooling solutions combining liquid-assisted and air-cooled modules. Furthermore, high-speed, low-noise fan designs are increasingly used in industrial automation and healthcare equipment. Industry players are also exploring eco-friendly materials, such as recyclable plastics and low-friction bearings, to improve sustainability while maintaining performance standards.

In March 2024, Delta Electronics launched a new series of industrial DC fans optimized for Industry 4.0 and AIoT systems. These fans deliver IP68 protection for harsh environments (salt spray & high temperature) and are designed for applications such as EV charging stations, solar inverters, factory automation, and CNC machines. Source: www.deltaww.com

In October 2024, Delta revealed its energy‑saving liquid- and air‑cooling solutions for AI and HPC data centers at OCP Global Summit. The company unveiled a 1.5 MW coolant distribution unit (CDU) with a DC‑fan array, as well as a 4,000 W DC‑DC converter tailored for GPU-based server power delivery. Source: www.deltaww.com

In November 2024, Delta Electronics showcased its power and cooling innovations at Supercomputing 2024, including a 1.5 MW liquid cooling CDU, high-power “High Power Air Mover” (HPAM) fans using EC technology, and DC fan arrays paired with 3D vapor chambers for GPU cooling. Source: www.deltaww.com

In October 2024, Sunon Group (Sunonwealth Electric) introduced advanced cooling modules at the OCP Global Summit, including an Advanced Air‑Liquid Cooling (AALC) sidecar that integrates both liquid- and air-cooled modules, and immersion fans that achieved an in‑system temperature reduction of 17°C in high-performance servers. Source: www.sunon.com

The DC Motor Cooling Fans Market Report provides a comprehensive overview of product types, applications, end-user segments, and regional insights, offering a strategic guide for industry decision-makers. The report covers axial, centrifugal, and mixed-flow fan types, highlighting technological differentiators such as BLDC motors, PWM control, IoT integration, and energy-efficient designs. Applications analyzed include telecommunications, data centers, electric vehicles, industrial automation, and consumer electronics, with end-user focus on enterprises, OEMs, and infrastructure operators. Regionally, the report spans Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, emphasizing production volumes, technological hubs, and infrastructure trends. Additionally, the report explores emerging niches, including micro-fans for edge computing, AI-enabled predictive cooling, and hybrid thermal management systems, alongside regulatory influences, ESG-driven initiatives, and sustainability-focused product development. This scope ensures a detailed understanding of market drivers, opportunities, and technological advancements for stakeholders planning strategic investments, production expansion, or competitive positioning across global markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,450.0 Million |

| Market Revenue (2032) | USD 2,648.3 Million |

| CAGR (2025–2032) | 7.82% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Delta Electronics, Nidec Corporation, Sunon Group, Sanyo Denki Co., Ltd., Ebmpapst Germany, EBM-Papst North America, Orion Fans |

| Customization & Pricing | Available on Request (10% Customization is Free) |