Reports

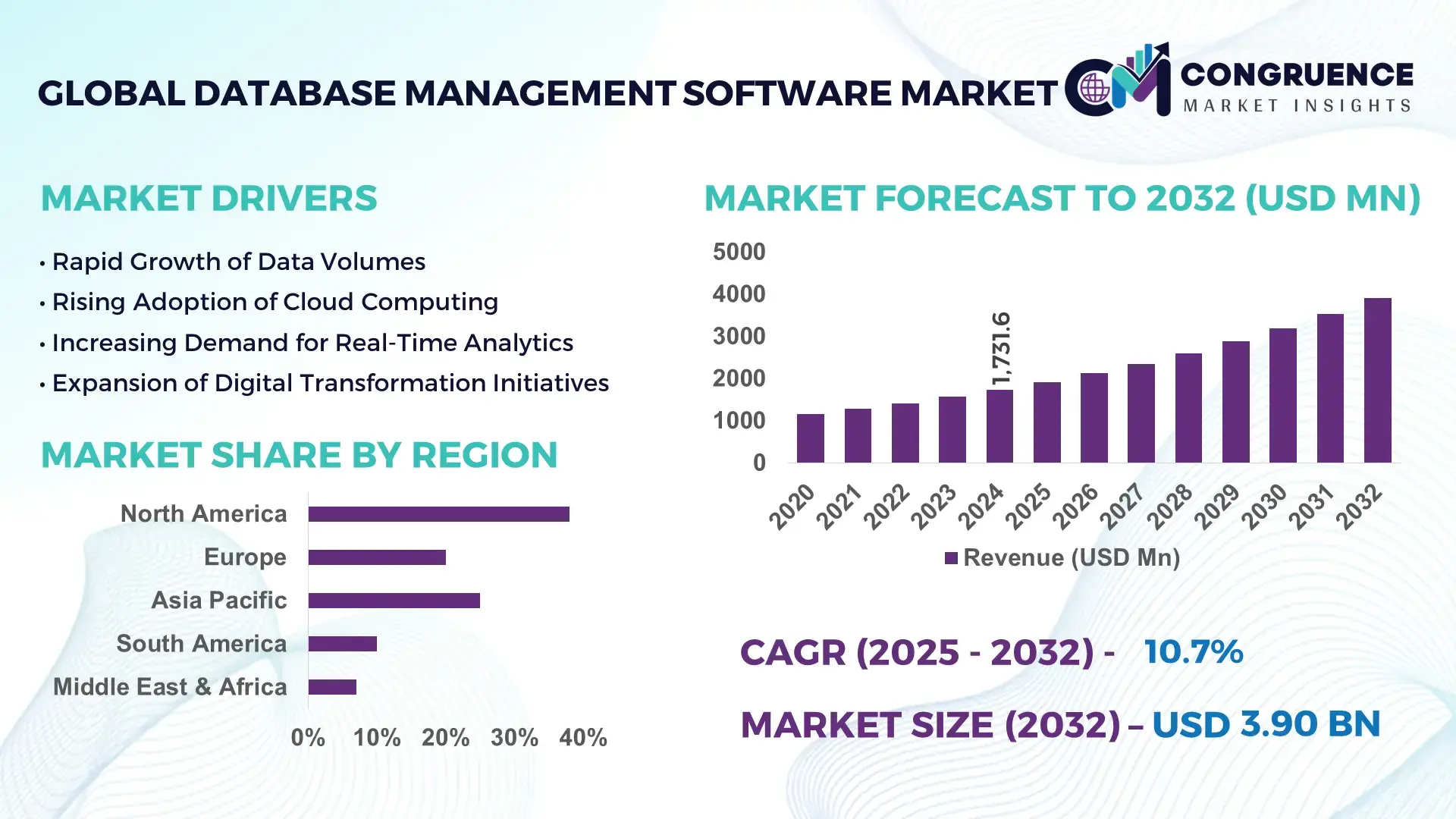

The Global Database Management Software Market was valued at USD 1731.55 Million in 2024 and is anticipated to reach a value of USD 3904.97 Million by 2032 expanding at a CAGR of 10.7% between 2025 and 2032. This growth is primarily driven by rising enterprise data volumes, cloud migration, and the increasing need for real-time analytics and data security across industries.

The United States dominates the Database Management Software market in terms of enterprise deployment scale, innovation output, and investment activity. In 2024, U.S.-based vendors supported over 60% of global enterprise DBMS deployments, with more than 85% of Fortune 500 companies using U.S.-developed platforms. Annual investment in U.S. data infrastructure exceeded USD 95 billion, covering hyperscale data centers, AI-enabled data platforms, and cybersecurity integration. Key application sectors include financial services at around 28% of enterprise DBMS spending, healthcare at 17%, retail and eCommerce at 15%, and manufacturing and logistics at 14%. More than 70% of large U.S. enterprises have adopted cloud-native or hybrid database architectures, and over 40% have implemented AI-based optimization and automation tools.

• Market Size & Growth: USD 1731.55 Million in 2024, projected to reach USD 3904.97 Million by 2032, CAGR of 10.7%, driven by cloud adoption and real-time analytics demand.

• Top Growth Drivers: Cloud database adoption 64%, automation efficiency gains 38%, data security spending increase 41%.

• Short-Term Forecast: By 2028, enterprises are expected to achieve up to 32% reduction in data management costs through automation and cloud migration.

• Emerging Technologies: AI-driven query optimization, serverless databases, real-time streaming databases.

• Regional Leaders: North America USD 1450 Million by 2032 with strong cloud-native adoption, Europe USD 980 Million with regulatory-driven data governance, Asia-Pacific USD 1020 Million with rapid SME digitalization.

• Consumer/End-User Trends: BFSI, healthcare, and retail increasingly adopt hybrid and multi-cloud database strategies for scalability and compliance.

• Pilot or Case Example: In 2024, a global retail chain implemented a cloud-native DBMS and achieved 29% faster transaction processing and 21% lower downtime.

• Competitive Landscape: Oracle approximately 28% share, followed by Microsoft, IBM, SAP, Amazon Web Services, and MongoDB.

• Regulatory & ESG Impact: Data privacy laws, carbon reporting requirements, and digital sovereignty regulations are influencing database architecture decisions.

• Investment & Funding Patterns: Over USD 45 billion invested globally in database, cloud, and data infrastructure projects since 2023, with rising venture funding in AI-native data platforms.

• Innovation & Future Outlook: Strong focus on autonomous databases, AI-integrated data governance, and cross-platform interoperability.

The Database Management Software market is supported by strong demand from BFSI, healthcare, retail, telecommunications, and manufacturing, with BFSI contributing roughly 30% of total enterprise spending due to regulatory compliance and transaction processing needs. Healthcare adoption is rising due to digital health records and analytics, while retail growth is driven by personalization and omnichannel data integration. Innovations such as autonomous databases, AI-based anomaly detection, and real-time streaming integration are reshaping product offerings. Regulatory frameworks around data privacy, cybersecurity, and digital resilience are accelerating platform modernization. Asia-Pacific is witnessing the fastest growth due to SME digitalization, while Europe emphasizes compliance-driven upgrades. Future growth will be driven by serverless databases, edge data processing, and deeper integration with AI and analytics platforms.

The Database Management Software Market is strategically positioned at the core of digital transformation, enabling enterprises to manage, secure, and extract value from rapidly expanding data volumes across cloud, edge, and on-premise environments. Over 65% of large enterprises now operate hybrid or multi-cloud data architectures, making database platforms a central layer for business continuity, analytics, regulatory reporting, and AI deployment. From a technology benchmark perspective, cloud-native distributed databases deliver approximately 45% faster query processing compared to traditional on-premise relational database systems, while also improving scalability and uptime. Regionally, North America dominates in deployment volume, while Asia-Pacific leads in new adoption with around 58% of enterprises actively migrating workloads to modern cloud and open-source database platforms.

By 2028, AI-driven autonomous database management is expected to reduce manual administration effort by 35% and improve system availability by over 25%, enabling IT teams to shift resources toward innovation and governance rather than maintenance. From a compliance and ESG perspective, firms are committing to measurable sustainability improvements such as 30% reductions in data center energy intensity and increased use of renewable-powered cloud infrastructure by 2030. In 2024, a leading U.S. cloud provider achieved a 22% reduction in database infrastructure energy consumption by deploying AI-based workload optimization and automated resource scaling across its data centers.

Looking ahead, the Database Management Software Market will function as a pillar of enterprise resilience, regulatory compliance, and sustainable growth by supporting secure data sharing, real-time decision-making, cross-border data governance, and environmentally responsible IT operations across global industries.

The rapid expansion of cloud computing and digital business models is a primary driver of demand for Database Management Software. More than 70% of enterprises now run at least one mission-critical workload in the cloud, and over half operate in hybrid or multi-cloud environments, creating demand for platforms that can manage data consistently across infrastructures. Digital services in banking, retail, healthcare, and logistics rely on real-time data availability, transaction integrity, and high system uptime, which modern database platforms are designed to deliver. For example, online retail platforms process millions of transactions per hour, requiring horizontally scalable databases that can expand capacity automatically. The shift toward data-driven decision-making, customer personalization, and AI-enabled operations further increases the need for high-performance, integrated, and secure database environments that support analytics and machine learning workloads alongside traditional transactions.

Security, regulatory compliance, and migration complexity represent significant restraints on the Database Management Software market. Enterprises handling financial, healthcare, and government data must comply with strict regulations related to data residency, privacy, encryption, and auditability, which can slow adoption of new platforms. Data migration from legacy systems is technically complex and operationally risky, with potential downtime, data loss, or application incompatibility. Large organizations often manage petabytes of data accumulated over decades, making transitions costly and time-consuming. Additionally, cybersecurity threats continue to rise, and any perceived vulnerability in new platforms can delay procurement decisions. These factors make some organizations cautious, leading to extended evaluation cycles and slower modernization despite clear long-term benefits.

AI integration and real-time analytics represent major growth opportunities for the Database Management Software market. Enterprises increasingly seek platforms that can not only store data but also analyze and optimize it in real time. AI-enabled databases can automatically tune performance, detect anomalies, predict failures, and optimize resource usage, reducing operational overhead and improving reliability. Real-time analytics supports use cases such as fraud detection, dynamic pricing, predictive maintenance, and personalized customer engagement. As organizations embed AI into business processes, demand is rising for databases that integrate seamlessly with machine learning pipelines and streaming data platforms. This creates opportunities for vendors to offer differentiated, high-value solutions that go beyond traditional data storage into intelligent data management.

A key challenge for the Database Management Software market is the shortage of skilled professionals capable of managing complex, distributed, and cloud-based data environments. Demand for data architects, cloud engineers, and cybersecurity specialists exceeds supply, raising labor costs and slowing project execution. Vendor lock-in is another concern, as enterprises fear becoming dependent on proprietary platforms that limit future flexibility and increase long-term costs. Additionally, while cloud databases reduce upfront infrastructure investment, ongoing operational costs can become unpredictable if workloads are not properly optimized. Managing performance, security, and cost simultaneously across hybrid and multi-cloud environments remains complex, requiring advanced governance and monitoring capabilities that many organizations are still developing.

• Rapid shift toward autonomous and self-managing databases (over 48% of enterprises piloting automation) Enterprises are increasingly adopting autonomous database capabilities such as automatic tuning, patching, and workload balancing to reduce operational overhead and human error. Around 48% of large enterprises have already implemented or are piloting self-managing database features, reporting up to 30% lower administrative effort and 22% fewer system incidents. These platforms continuously optimize indexing, memory usage, and query routing, improving transaction latency by 18–25% and increasing system availability beyond 99.95%, making them highly attractive for mission-critical workloads in banking, retail, and telecommunications.

• Accelerated migration to hybrid and multi-cloud database architectures (over 67% of enterprises operating hybrid models) More than 67% of medium and large organizations now operate hybrid or multi-cloud database environments to balance scalability, compliance, and resilience. Enterprises report 28% improvement in disaster recovery performance and 35% faster deployment of new applications when using multi-cloud strategies. Data replication across regions has increased by over 40%, enabling lower latency for global users and improved business continuity while supporting local data residency and regulatory requirements.

• Expansion of real-time and streaming data platforms (around 44% growth in real-time workload adoption) Real-time data processing is becoming central to digital operations, with approximately 44% of enterprises now running streaming or near-real-time workloads for fraud detection, dynamic pricing, and predictive maintenance. Organizations using real-time platforms report up to 26% faster decision cycles and 19% improvement in customer experience metrics. This trend is driving adoption of databases optimized for low-latency ingestion, in-memory processing, and continuous analytics.

• Rising focus on security, privacy, and data governance automation (over 52% increase in automated compliance deployments) Automated security and governance tools are increasingly embedded within database platforms, with over 52% of enterprises deploying automated encryption, access control, and audit logging. Organizations report 33% reduction in security incidents and 29% faster compliance reporting cycles. Privacy-by-design architectures, data masking, and sovereign cloud deployments are also expanding, particularly in regulated industries such as finance and healthcare, to reduce regulatory risk and strengthen trust in digital ecosystems.

The Database Management Software market is segmented by type, application, and end-user, reflecting the diverse technical and operational needs across industries. By type, relational, NoSQL, and cloud-native distributed databases dominate enterprise deployments, while specialized platforms such as in-memory and graph databases serve high-performance and relationship-centric use cases. By application, transaction processing and data warehousing remain foundational, but real-time analytics and AI/ML data pipelines are expanding rapidly as organizations pursue faster decision cycles and automation. By end-user, large enterprises account for the majority of complex, mission-critical deployments, while SMEs increasingly adopt managed and cloud-based platforms for cost efficiency and scalability. Regulated industries such as banking and healthcare emphasize security, auditability, and data sovereignty, whereas retail and telecommunications prioritize scalability and real-time performance. This segmentation highlights a market shifting from infrastructure-centric deployments toward intelligent, integrated, and compliance-ready data platforms aligned with digital business models.

Relational databases currently account for approximately 46% of enterprise deployments due to their maturity, standardized query languages, and reliability in transaction-heavy environments such as banking and ERP systems. NoSQL databases hold around 27% of adoption, driven by their ability to manage unstructured data, high write volumes, and horizontal scalability for digital platforms. Cloud-native distributed databases are the fastest-growing type, expanding at an estimated 18% CAGR, as organizations migrate workloads to cloud and require elastic scaling, geographic replication, and built-in resilience. These platforms are increasingly favored for global applications, digital services, and data-intensive workloads. In-memory and graph databases together represent roughly 12% of the market, serving niche use cases such as fraud detection, recommendation engines, and network analysis where low latency and complex relationship mapping are critical.

Online transaction processing accounts for about 38% of database usage, reflecting the continued importance of transactional integrity in banking, retail, and enterprise operations. Data warehousing and business intelligence represent around 29% of adoption, supporting reporting, compliance, and strategic planning. Real-time analytics and streaming data applications are the fastest-growing, expanding at approximately 20% CAGR, fueled by demand for instant insights in fraud detection, dynamic pricing, and predictive maintenance. These applications require low-latency ingestion and processing, pushing adoption of in-memory and streaming-optimized databases. Other applications, including archival storage, content management, and IoT data management, together contribute about 13% of usage, often tied to specific industry needs.

Large enterprises represent roughly 52% of database deployments due to their complex data environments, regulatory obligations, and need for high availability across global operations. SMEs account for about 31% of adoption, increasingly favoring managed cloud databases to avoid high upfront infrastructure and skills costs. The fastest-growing end-user segment is digital-native companies, including fintech, e-commerce, and SaaS providers, expanding at around 22% CAGR as they rely heavily on scalable, real-time data platforms. Other end-users such as government, education, and utilities together contribute about 17%, often driven by digital public services and smart infrastructure programs. Adoption rates are particularly high in BFSI at around 78%, healthcare at 64%, and retail at 59%, reflecting strong data dependency.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.8% between 2025 and 2032.

North America benefits from over 72% enterprise penetration of cloud and hybrid databases, with more than 85% of Fortune 1000 firms running mission-critical workloads on advanced database platforms. Europe represents around 27% of global deployments, driven by regulatory compliance, data sovereignty, and strong adoption in financial services and manufacturing. Asia-Pacific accounts for approximately 25% of the market, supported by rapid digitalization across SMEs, over 1.2 billion mobile internet users, and strong investment in hyperscale data centers. South America contributes about 6%, while the Middle East & Africa together account for roughly 4%, primarily driven by government digital transformation, smart city programs, and energy-sector digitization. Cross-border data flows have increased by over 40% globally, pushing demand for compliant, resilient, and geographically distributed database architectures.

North America holds approximately 38% of the Database Management Software market, supported by strong demand from BFSI, healthcare, retail, and government sectors. Financial services and healthcare together account for over 45% of regional deployments due to regulatory reporting, fraud detection, and patient data management needs. Regulatory frameworks around data privacy, cybersecurity, and digital resilience are driving upgrades toward encrypted, audit-ready platforms. Enterprises in this region show high adoption of autonomous and AI-driven databases, with about 49% piloting self-managing features. A leading regional provider expanded its autonomous database services in 2024, enabling clients to reduce administrative workloads by 30% and improve uptime beyond 99.95%. Consumer behavior shows higher adoption in healthcare and finance, where data accuracy, security, and availability are mission-critical.

Europe accounts for around 27% of the Database Management Software market, with Germany, the UK, and France collectively representing over 60% of regional demand. Regulatory pressure around data privacy, digital sovereignty, and cybersecurity is a primary driver, pushing organizations toward localized, compliant, and transparent database platforms. Sustainability initiatives are also influencing technology choices, with many enterprises prioritizing energy-efficient cloud and green data center solutions. Adoption of privacy-preserving analytics, encryption-by-default, and explainable data management tools is rising. A regional enterprise software vendor expanded sovereign cloud database services in 2024 to support public sector and regulated industries. Consumer behavior reflects a strong preference for compliant, auditable, and transparent Database Management Software solutions.

Asia-Pacific represents about 25% of global deployments and is ranked as the fastest-growing regional market by volume expansion. China, India, and Japan together account for over 65% of regional demand, supported by large-scale digital commerce, fintech, and government digitization programs. Over 60% of new enterprise applications in the region are cloud-native, driving adoption of scalable and distributed database platforms. Innovation hubs across Shenzhen, Bangalore, Tokyo, and Singapore are advancing AI-integrated and real-time data platforms. A major regional cloud provider expanded its managed database services in 2024 to support SMEs, enabling faster onboarding and reduced operational complexity. Consumer behavior is driven by e-commerce, mobile services, and digital payments.

South America accounts for approximately 6% of the global Database Management Software market, with Brazil and Argentina as key contributors. Digital banking, media, and telecommunications are major demand drivers as organizations modernize legacy systems to support online services and localized content delivery. Government incentives for digital infrastructure and cloud adoption are supporting modernization efforts, particularly in urban centers. A regional IT services firm expanded cloud database migration services in 2024, supporting financial institutions and telecom providers in transitioning to hybrid platforms. Consumer behavior shows higher demand tied to media streaming, language localization, and mobile service expansion.

The Middle East & Africa region represents about 4% of global deployments, with the UAE and South Africa as primary growth hubs. Oil and gas, construction, government services, and logistics are key demand sectors, requiring secure and scalable data platforms. Smart city initiatives and national digital transformation programs are accelerating adoption of cloud and AI-enabled databases. Local regulations around data residency and cross-border data transfer are shaping deployment models. A regional telecom and cloud provider expanded sovereign cloud database offerings in 2024 to support public sector digitization. Consumer behavior reflects growing trust in digital government, mobile banking, and online public services.

• United States Database Management Software Market: 29% share, driven by high enterprise digitalization, strong cloud infrastructure, and advanced regulatory and cybersecurity frameworks.

• China Database Management Software Market: 17% share, supported by large-scale e-commerce, fintech expansion, and government-led digital transformation programs.

The Database Management Software market is moderately consolidated, with more than 120 active global and regional vendors competing across enterprise, mid-market, and cloud-native segments. The top five companies together account for approximately 64% of total enterprise deployments, indicating a strong presence of established vendors alongside a long tail of specialized and open-source providers. Market leaders differentiate through scale, integrated ecosystems, and advanced automation, while challengers compete on flexibility, cost efficiency, and specialization in real-time, open-source, or industry-specific solutions.

Strategic initiatives are increasingly focused on cloud partnerships, AI integration, and vertical-specific offerings. Over 35 major product upgrades and new database services were launched in 2023–2024, primarily around autonomous management, real-time analytics, and enhanced security. Partnerships between hyperscale cloud providers and enterprise software firms now cover over 70% of new enterprise database deployments, reflecting the shift toward managed and platform-integrated solutions. Mergers and acquisitions remain selective, with around 14 notable acquisitions in the past two years aimed at acquiring AI capabilities, cybersecurity features, or industry expertise.

Innovation competition centers on autonomous databases, multi-cloud interoperability, data sovereignty compliance, and performance optimization. More than 45% of vendors now embed AI-based monitoring, tuning, or anomaly detection into their platforms. Customer switching remains relatively low at around 12% annually, reflecting high integration costs and mission-critical reliance, which further strengthens incumbent positions. Overall, competition is driven by technological differentiation, ecosystem partnerships, and the ability to support compliance, scalability, and sustainability objectives simultaneously.

Oracle

Microsoft

IBM

SAP

Amazon Web Services

MongoDB

Snowflake

Teradata

Database Management Software is undergoing rapid technological evolution as enterprises seek platforms that are scalable, intelligent, secure, and interoperable across cloud, edge, and on-premise environments. One of the most impactful shifts is the move toward cloud-native and distributed database architectures, now used by more than 68% of large enterprises for at least one mission-critical workload. These platforms enable geographic data replication across 3–5 regions on average, improving disaster recovery times by up to 40% and reducing latency for global users by 20–30%. Containerized deployment models and Kubernetes-native databases are also gaining traction, with around 46% of new deployments now container-based, enabling faster application scaling and simplified lifecycle management.

Artificial intelligence is becoming embedded within database platforms to support autonomous operations, predictive performance tuning, and anomaly detection. Approximately 44% of enterprises are piloting or using AI-assisted database management features, reporting up to 28% reductions in manual administrative effort and 22% fewer performance incidents. In parallel, real-time and streaming data technologies are expanding, with about 41% of digital-native companies running low-latency ingestion and analytics pipelines for fraud detection, dynamic pricing, and IoT monitoring. In-memory processing and columnar storage are increasingly used to support sub-second analytics on high-volume datasets.

Security and governance technologies are also advancing, with over 52% of organizations deploying automated encryption, role-based access control, continuous auditing, and data masking directly within database layers. Privacy-preserving techniques such as tokenization and confidential computing are being adopted to protect sensitive data while enabling analytics. Interoperability and multi-cloud management tools are improving, allowing enterprises to manage up to four different database platforms through unified control layers. Together, these technologies are transforming Database Management Software from passive data repositories into intelligent, adaptive, and compliance-ready digital infrastructure supporting enterprise resilience and long-term growth.

• In March 2025, Microsoft and SAP announced a strategic partnership to accelerate data integration and governance across Microsoft Azure and SAP HANA Cloud, enhancing joint reference architectures and simplifying enterprise database management and analytics deployments across hybrid cloud environments.

• In July 2024, MongoDB expanded its Atlas platform with real-time analytics and enhanced search capabilities, simplifying cloud data ingestion and multi-cloud integration for enterprises managing unstructured and semi-structured data.

• In July 2024, Oracle made its Exadata Database Service available across Microsoft Azure, Google Cloud, and AWS as part of multicloud partnerships, enabling unified high-performance transaction and analytics workloads across leading public cloud infrastructures. (Wikipedia)

• Between September and November 2023, Snowflake released a suite of product enhancements including support for Apache Iceberg Tables, more granular security controls, and intuitive UI for replication and client redirect, improving platform governance and operational efficiency. (Snowflake)

The Database Management Software Market Report provides a comprehensive overview of the global landscape, encompassing product types, deployment models, applications, technologies, and regional insights. The report examines core database types such as relational, NoSQL, distributed, in-memory, and specialized platforms including graph and time-series databases. It details how cloud-native and hybrid architectures are reshaping enterprise priorities, with analyses of geographic regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, supported by market penetration figures, regulatory context, and consumer behavior variations.

Application segments covered in the report include transaction processing, data warehousing and business intelligence, real-time analytics and streaming, and data governance. Each application area is assessed for adoption patterns among verticals such as BFSI, healthcare, retail, telecommunications, and government services. The report also provides a technology landscape section that explores current innovations like autonomous database operations, AI and machine learning integration, real-time data ingestion, and compliance-oriented security frameworks. Emerging niches such as explainable multimodal query engines and semantic SQL optimization are addressed.

Regional consumption patterns, regulatory pressures, and infrastructure trends are highlighted alongside competitive dynamics, profiling leading global players and their strategic initiatives. The report concludes with forward-looking insights into innovation trends, industry best practices, and strategic recommendations to support enterprise decision-making in an evolving data management ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 10.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Oracle , Microsoft , IBM , SAP, Amazon Web Services, MongoDB, Snowflake, Teradata |

Customization & Pricing | Available on Request (10% Customization is Free) |