Reports

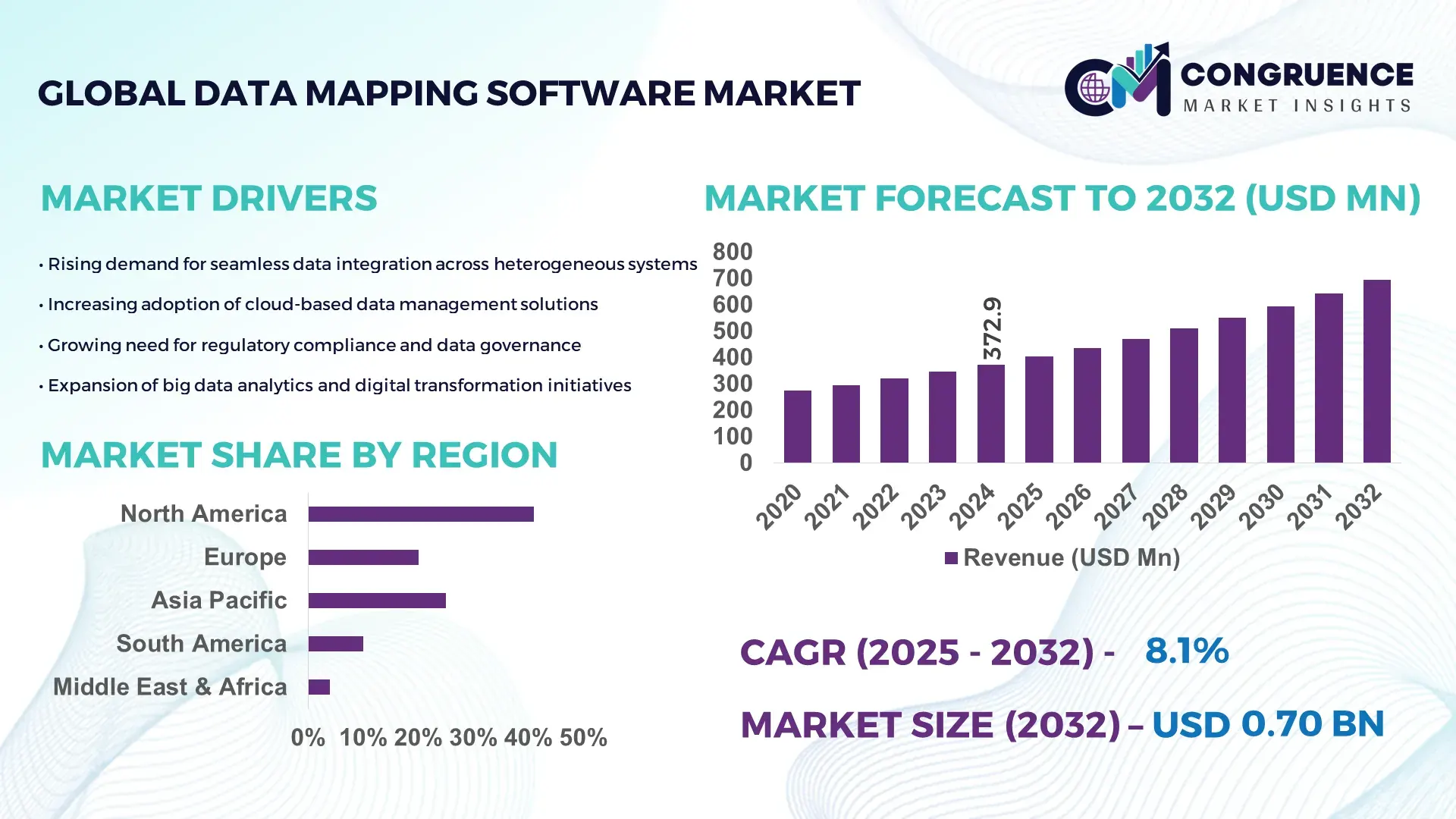

The Global Data Mapping Software Market was valued at USD 372.94 Million in 2024 and is anticipated to reach a value of USD 695.42 Million by 2032 expanding at a CAGR of 8.1% between 2025 and 2032. This growth is driven by accelerating digital transformation across data-intensive enterprises.

The United States remains the dominant country in the Data Mapping Software Market, supported by strong enterprise digitalization and one of the world’s largest cloud infrastructure ecosystems, with over 2,700 data centers and more than USD 220 billion in annual IT spending. The country also records high adoption rates of integration tools, with 63% of large enterprises using automated data mapping for analytics workflows. Ongoing investment in AI-driven integration platforms, along with rapid expansion in regulated industries such as BFSI and healthcare, continues to strengthen its leadership, supported by advanced R&D capabilities and strong vendor concentration.

• Market Size & Growth: Valued at USD 372.94 million in 2024, projected to reach USD 695.42 million by 2032 at an 8.1% CAGR, driven by accelerated cloud integration and automation.

• Top Growth Drivers: 62% adoption of cloud-native integration tools; 48% efficiency improvement from automation; 55% rise in API-led connectivity.

• Short-Term Forecast: By 2028, organizations are expected to achieve up to 37% cost reduction through automated data transformation workflows.

• Emerging Technologies: Growth of AI-driven schema mapping, low-code integration platforms, and automated lineage tracking.

• Regional Leaders: North America projected to reach USD 310 million by 2032 with high enterprise automation; Europe expected to hit USD 190 million with strong regulatory compliance adoption; Asia-Pacific projected at USD 165 million supported by cloud expansion.

• Consumer/End-User Trends: BFSI, healthcare, and retail sectors show increasing reliance on real-time data exchange and analytics-driven operations.

• Pilot or Case Example: In 2024, a major U.S. healthcare network deployed an AI-enabled mapping pilot achieving a 42% reduction in data preparation time.

• Competitive Landscape: Market leader holds approximately 18% share, followed by major players including Informatica, Talend, IBM, SAP, and Precisely.

• Regulatory & ESG Impact: Data privacy mandates, integration standards, and ESG-driven transparency requirements are accelerating structured data mapping adoption.

• Investment & Funding Patterns: Over USD 1.4 billion invested recently in data integration and automation platforms, driven by enterprise AI-readiness initiatives.

• Innovation & Future Outlook: Advancements in predictive mapping, automated metadata intelligence, and cloud-native interoperability are shaping next-generation platforms.

Unique insights into the Data Mapping Software Market indicate strong traction across BFSI, healthcare, telecommunications, and retail—together contributing more than 65% of total deployment volume. Recent innovations include AI-assisted schema detection and metadata intelligence that reduce manual effort by up to 50%. Regulatory frameworks promoting data standardization, such as interoperability mandates in healthcare and financial reporting, are influencing rapid adoption. Regionally, consumption growth is highest in Asia-Pacific due to cloud-native enterprise transitions, while mature markets continue to integrate advanced lineage and governance capabilities. Looking ahead, the market is poised for substantial evolution powered by automation, cross-platform interoperability, and increasing integration complexity across global digital ecosystems.

The strategic relevance of the Data Mapping Software Market continues to rise as enterprises accelerate data modernization programs, cloud migrations, and AI-driven analytics. Automated schema mapping, metadata intelligence, and lineage tracking are becoming essential for operational continuity, regulatory compliance, and data-driven decision-making. Technologies such as AI-assisted mapping deliver 45% improvement compared to traditional rule-based mapping, enabling faster integration and reducing manual workloads across complex data ecosystems. Regional demand patterns further reinforce this shift; North America dominates in volume, while Europe leads in adoption with 67% of enterprises using automated data governance and mapping tools.

By 2027, AI-driven metadata discovery is expected to improve data processing accuracy by 38%, directly enhancing operational efficiency across BFSI, healthcare, and manufacturing sectors. Compliance strategies are also being reshaped by global ESG commitments, with firms targeting 30% improvements in data transparency and reporting accuracy by 2028 to align with sustainability frameworks. In 2024, a major Asia-Pacific telecom operator achieved a 41% reduction in integration delays through a large-scale API-mapping automation initiative, demonstrating measurable value at enterprise scale.

Looking ahead, the Data Mapping Software Market is positioned as a pillar of resilience, compliance, and sustainable growth, supporting enterprises as they navigate expanding data volumes, regulatory intensity, and advanced analytics transformation.

Automation-driven transformation programs are significantly boosting the Data Mapping Software Market, with enterprises prioritizing tools that reduce manual mapping time and minimize integration errors. As organizations process growing datasets—expected to exceed 180 zettabytes globally by 2025—automated mapping platforms offer the scalability needed to maintain operational efficiency. Adoption of low-code integration frameworks has increased by 52% since 2022, and nearly 60% of large enterprises now leverage AI-based mapping to enhance speed and accuracy in data workflows. These technologies reduce dependency on high-cost technical resources, streamline migration cycles, and support multi-cloud data strategies. Automation also aligns with stringent compliance requirements across BFSI, healthcare, and government sectors, where precise data lineage and auditability are essential for regulatory submissions and quality assurance.

Increasing complexity of enterprise data ecosystems is emerging as a major restraint in the Data Mapping Software Market. Organizations today manage data from hundreds of sources—including APIs, SaaS applications, IoT devices, and legacy systems—resulting in structural inconsistencies and compatibility challenges. Over 47% of organizations report difficulties in mapping unstructured or semi-structured datasets at scale, leading to delays in analytics, governance, and cloud migration projects. Additionally, skills shortages in advanced data engineering roles contribute to slower adoption of sophisticated mapping technologies. Integration of AI and automation tools requires upfront configuration, training, and governance frameworks that smaller enterprises often struggle to implement. These challenges collectively restrict implementation velocity and increase overall operational risk during large-scale data transformation initiatives.

The rise of AI-integrated data governance presents substantial growth opportunities for the Data Mapping Software Market. As enterprises increase investments in data quality and compliance infrastructure, demand for intelligent mapping and lineage capabilities is expanding rapidly. AI-enabled tools can automate up to 55% of manual mapping tasks, opening opportunities for scalable analytics transformation across regulated industries. Sectors such as BFSI, healthcare, telecom, and retail are projected to see rapid adoption of predictive mapping that enhances accuracy and reduces integration cycle times. Additionally, government initiatives promoting data standardization and interoperability—such as digital health and financial reporting frameworks—are accelerating cloud-native mapping deployments. The emergence of real-time streaming architectures, combined with rising adoption of low-code and composable integration platforms, provides a strong foundation for long-term market expansion.

Escalating security and compliance requirements are creating substantial challenges for the Data Mapping Software Market, especially as organizations handle sensitive financial, health, and personal data across distributed environments. More than 58% of enterprises cite data privacy and governance risks as a major hurdle in mapping automation. Misconfigurations, inconsistent metadata standards, and cross-border data movement restrictions increase operational exposure during integration projects. Emerging regulations such as data residency laws and sector-specific compliance mandates require extensive documentation, lineage transparency, and process audits—placing additional burden on mapping tools and teams. Persistent cybersecurity threats also complicate cloud-based mapping deployments, necessitating advanced encryption, access controls, and monitoring systems. These challenges heighten implementation complexity and require significant investment in secure, compliant, AI-ready data mapping frameworks.

• Acceleration of AI-Driven Schema Automation: AI-based schema recognition and automated mapping engines are rapidly transforming enterprise integration workflows. More than 62% of large organizations now use AI-assisted mapping tools that reduce manual schema alignment time by up to 48%. These platforms analyze multiple datasets simultaneously, enabling faster onboarding of new data sources and minimizing human error. Additionally, AI-driven pattern detection enhances mapping accuracy by 37%, supporting mission-critical applications in BFSI, healthcare, and telecom environments where precision and real-time alignment are essential.

• Expansion of API-Led and Event-Driven Integration Architectures: API-driven ecosystems are increasing the need for scalable data mapping frameworks, with API call volumes rising by 44% year-over-year in enterprise environments. Event-driven systems now account for nearly 52% of newly implemented integration architectures, requiring advanced mapping engines capable of handling dynamic, high-frequency data flows. This shift supports real-time analytics and operational intelligence, enabling businesses to reduce processing delays by 33% and streamline data synchronization across cloud and on-premise platforms.

• Growth of Low-Code and No-Code Mapping Platforms: Adoption of low-code data mapping solutions is rising sharply, driven by the need to reduce IT dependency and accelerate transformation. Approximately 57% of mid-sized enterprises have integrated low-code mapping tools into their data operations, reporting implementation cycle reductions of up to 41%. These platforms enable non-technical users to manage data pipelines more efficiently, standardize workflows, and improve cross-department collaboration. As a result, organizations are achieving faster deployment of analytics applications and greater operational agility.

• Increasing Focus on Data Governance, Lineage, and Compliance Automation: Heightened regulatory scrutiny is pushing enterprises toward advanced lineage visualization and governance-driven mapping. Over 68% of organizations have prioritized automated lineage tracking to meet compliance requirements across financial, healthcare, and public-sector systems. These tools provide traceability across thousands of data elements, reducing audit preparation time by 29% and improving reporting accuracy by 34%. This trend is further strengthened by cross-border data regulations, prompting the adoption of mapping frameworks with built-in policy enforcement and privacy safeguards.

The Data Mapping Software Market is structured across three primary segmentation pillars—types, applications, and end-user categories—each demonstrating distinct adoption patterns and technological depth. Type-wise, intelligent and automated mapping solutions are gaining stronger traction due to increasing data volume and integration complexity across hybrid ecosystems. Application segmentation highlights rising adoption in data integration, governance, and cloud migration workflows, driven by enterprises prioritizing accuracy and interoperability. End-user analysis shows concentrated demand from highly regulated sectors requiring stringent data lineage and compliance management. Collectively, these segments underline an industry progressing toward automation, AI-enhanced accuracy, and domain-specific mapping capabilities, enabling organizations to streamline analytics and operational efficiency across multi-cloud and distributed architectures.

Intelligent Mapping Tools remain the leading type, accounting for approximately 46% of total adoption due to their advanced automation capabilities and ability to process complex datasets at scale. The rise of AI-enabled schema detection, which improves mapping accuracy by 37%, continues to strengthen this segment’s dominance. In comparison, rule-based mapping systems represent about 28% of adoption, mainly across legacy environments requiring predictable, structured workflows. Meanwhile, the fastest-growing segment is AI-driven adaptive mapping, expanding rapidly with modern enterprises and projected to grow at an estimated 11% CAGR due to increasing dependency on predictive automation and real-time lineage visibility. Other types—including cloud-native mapping modules and API-centric mapping engines—collectively contribute nearly 26%, adding flexibility for organizations implementing distributed architectures.

Data Integration stands as the leading application, accounting for nearly 48% of adoption, supported by enterprise needs for real-time interoperability across ERPs, CRMs, and analytics platforms. Data Governance applications represent around 27%, driven by increasing regulatory expectations for audit-ready lineage and traceability. In comparison, cloud migration applications hold about 21% share, but adoption is accelerating as enterprises modernize infrastructure; this segment is also the fastest growing, projected to expand at an approximate 10% CAGR due to large-scale transitions toward hybrid cloud and multi-cloud ecosystems. Remaining applications—including data quality enhancement and API lifecycle workflows—collectively contribute 14%, offering niche value in specialized data transformation pipelines.

The BFSI sector leads the end-user landscape with roughly 44% share owing to its high dependency on precise data lineage, regulatory reporting, and automated validation processes. Healthcare follows with 26% adoption, supported by interoperability mandates and rising deployment of electronic medical records requiring consistent data standardization. Telecom emerges as the fastest-growing end-user segment, projected to expand at an estimated 12% CAGR driven by rapid API ecosystem expansion and the need for real-time mapping of streaming datasets. Other sectors—including retail, manufacturing, and government—collectively account for 30%, contributing steady demand as digital transformation and automation initiatives scale globally. Retail alone has seen adoption levels rise by 18% over the past two years, reflecting increased application of customer analytics and unified data environments.

North America accounted for the largest market share at 41% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2025 and 2032.

The Data Mapping Software Market demonstrates strong geographic diversity, with Europe holding 29% share, Asia-Pacific reaching 22%, South America recording 5%, and the Middle East & Africa contributing nearly 3%. North America’s demand is strengthened by advanced digital infrastructure and mature cloud adoption, while Europe benefits from regulatory-driven compliance transformation. Asia-Pacific shows accelerating enterprise digitization across China, India, and Japan supported by rapid API ecosystem expansion and large-scale digital commerce. South America and MEA continue to expand gradually, driven by telecom modernization, fintech development, and increased public-sector digital initiatives.

North America holds nearly 41% of the Data Mapping Software Market, supported by strong digital transformation initiatives across BFSI, healthcare, and telecom. A significant portion of large enterprises—over 63%—use automated mapping to streamline governance and regulatory workflows. Government mandates related to data protection and interoperability in sectors such as healthcare continue to accelerate adoption. The region has seen powerful AI-integration trends, with more than 58% of enterprises deploying AI-driven mapping or lineage features. A notable example includes a major U.S.-based cloud provider expanding its metadata intelligence suite in 2024 to support cross-cloud data standardization for federal agencies. Consumer behavior in this region shows higher adoption of advanced mapping among healthcare and financial institutions due to strict compliance and high operational data volumes.

Europe accounts for approximately 29% of the Data Mapping Software Market, propelled by stringent regulations across Germany, the UK, France, and the Nordics. Regulatory frameworks related to digital governance and data transparency are driving demand for explainable and audit-ready mapping systems. Adoption of emerging technologies such as privacy-preserving analytics and AI-enhanced lineage engines has increased by nearly 34% since 2022. Local technology firms continue to introduce compliance-centric mapping tools tailored to GDPR alignment. For example, a leading European data integration vendor expanded its governance suite in 2024 to meet sector requirements in banking and public administration. Consumer behavior in the region prioritizes traceability, with enterprises using mapping tools to ensure responsible data handling and adherence to legal obligations.

Asia-Pacific represents 22% of the Data Mapping Software Market, ranking as the fastest-expanding region in volume and adoption. China, India, and Japan drive the highest consumption, supported by large-scale cloud expansion, e-commerce growth, and rapid proliferation of mobile-first applications. The region’s digital infrastructure investments surpassed significant thresholds in 2024, enabling enterprises to implement API-driven and real-time data mapping frameworks. Local innovation hubs in India and Singapore are accelerating AI-based mapping development. A prominent Asia-Pacific telecom giant deployed large-scale mapping automation in 2024 to optimize real-time network analytics. Consumer behavior trends indicate strong adoption driven by e-commerce, fintech, and mobile AI platforms that rely heavily on accurate, high-frequency data flows.

South America contributes nearly 5% of the Data Mapping Software Market, with Brazil and Argentina leading adoption due to increased enterprise modernization and digital services expansion. Regulatory reforms supporting fintech and digital public systems have accelerated demand for mapping and lineage tools. Infrastructure projects in energy, utilities, and telecommunications also require advanced data integration frameworks. Local SaaS companies are beginning to incorporate AI-enabled mapping capabilities to improve performance for cross-border digital services. For instance, a regional cloud provider in Brazil added automated metadata reporting features in 2024 for government clients. Consumer behavior trends show growing reliance on data mapping for language localization, media platforms, and streaming analytics across major markets.

The Middle East & Africa region holds roughly 3% share of the Data Mapping Software Market, supported by ongoing digital mandates in UAE, Saudi Arabia, and South Africa. The region’s oil & gas, construction, and utilities sectors are accelerating adoption as they integrate real-time data monitoring and operational analytics. Technological modernization—including cloud migration initiatives and national digital transformation strategies—has increased enterprise demand for mapping solutions by nearly 28% in the past two years. A leading Middle Eastern IT services firm introduced automated lineage auditing features in 2024 to support government digital compliance programs. Consumer behavior indicates rising adoption among public-sector and large enterprises prioritizing security, operational efficiency, and centralized data visibility.

United States – 34% share

Strong dominance driven by advanced digital infrastructure and high adoption across healthcare, finance, and cloud-native enterprises.

Germany – 11% share

Robust regulatory environment and strong industrial digitization programs accelerate demand for governance-centric data mapping solutions.

The Data Mapping Software market is characterized by a moderately fragmented competitive structure, with more than 45 active vendors operating across integration platforms, cloud data management suites, and enterprise automation ecosystems. The top five companies collectively account for an estimated 38% of the total market share, supported by diversified portfolios and strong enterprise penetration. Competition is driven by accelerated data modernization initiatives, with over 62% of enterprises reporting increased spending on mapping, transformation, and governance tools to support analytics pipelines and AI adoption. Vendors are expanding capabilities through workflow automation, schema-detection engines, zero-code mapping interfaces, and real-time API-based transformations.

Strategic initiatives remain a defining factor. In the last two years, the sector recorded over 30 product enhancements focused on ML-driven data classification, nearly 20 ecosystem partnerships with cloud hyperscalers, and more than 10 acquisitions targeting metadata management and integration IP. Cloud-native platforms hold a competitive advantage, with 54% of users preferring SaaS-based mapping suites for scalability and lower provisioning complexity. Innovation is further influenced by interoperability standards, where nearly 70% of major tools now support multi-source lineage tracking and cross-cloud deployment. This competitive landscape continues to intensify as vendors prioritize automation, governance, and AI-driven mapping accuracy to solidify market positions.

Talend

IBM

Microsoft

MuleSoft

Precisely

Tibco Software

Denodo

CloverDX

Adeptia

Technology advancement in the Data Mapping Software market is accelerating as enterprises prioritize automation, cross-environment interoperability, and AI-driven data intelligence to support large-scale digital transformation. Current platforms are increasingly adopting machine learning–based schema detection, with more than 58% of leading tools now integrating automated pattern recognition to reduce manual mapping time by up to 45%. Real-time data transformation capabilities have also expanded, supported by event-streaming frameworks and API-first architectures that enable continuous ingestion across hybrid and multi-cloud ecosystems, where over 65% of enterprises now operate.

A significant shift is occurring toward metadata-driven mapping engines, which account for nearly 52% of new deployments due to their ability to support end-to-end lineage, compliance tracking, and dynamic schema evolution. Cloud-native mapping technologies continue to dominate user adoption, with nearly 60% of organizations preferring containerized, auto-scalable data mapping services built on Kubernetes, enabling elastic handling of diverse and high-volume data structures. Additionally, low-code and no-code mapping interfaces are becoming mainstream, representing approximately 48% of enterprise implementations, as companies focus on reducing dependency on specialized integration teams.

Emerging technologies such as AI-powered semantic mapping are reshaping operational efficiencies, with early adopters reporting improvements of up to 35% in mapping accuracy for unstructured and semi-structured data. Knowledge-graph–driven mapping is also expanding, particularly in regulated industries, where demand for contextual data relationships and governance precision continues to rise. Interoperability standards—including automated lineage synchronization between mapping engines, data catalogs, and integration hubs—are being adopted by nearly 70% of major vendors, reinforcing the market’s trajectory toward unified, intelligent, and automation-centric data ecosystems.

In February 2023, Talend launched a major update to its Data Fabric platform, introducing over 1,000 new connectors—including SAP S/4HANA and modern cloud databases—and smart services that allow users to pause/resume tasks and reduce compute time via automated timeouts. (Qlik)

During 2023, Talend discontinued its open-source Talend Open Studio, effective January 31, 2024, signaling a shift to its enterprise-grade Studio and commercial data integration offerings. (thedatasciencedossier.com)

In November 2023, IBM announced the deprecation of metadata integration brokers and bridges in InfoSphere Information Server, effective April 2025, while recommending clients migrate to its lineage solution powered by Manta to obtain richer, automated data mapping and governance. (IBM TechXchange)

In Fall 2024, Informatica released a major enhancement to its Intelligent Data Management Cloud (IDMC), adding GenAI-driven integration, enhanced SQL ELT for Databricks Delta Lake and Google BigQuery, and more granular metadata governance and privacy controls. (Informatica)

The Data Mapping Software Market Report provides a comprehensive analysis of global market segmentation, covering multiple types (rule-based, AI-driven, low-code mapping), and detailing their use across key application domains such as data integration, data governance, cloud migration, and API lifecycle management. The report examines end-user sectors—such as BFSI, healthcare, telecom, retail, manufacturing, and government—and evaluates how different verticals deploy mapping solutions to meet industry-specific data lineage and regulatory requirements.

Geographically, the study spans major regions (North America, Europe, Asia-Pacific, South America, Middle East & Africa), highlighting regional consumption patterns, local innovation hubs, and adoption behaviors. On the technology front, the report investigates current and emerging capabilities, including machine-learning schema detection, metadata-driven lineage, real-time event-stream mapping, knowledge-graph mapping, and AI-enabled automation. It also explores cloud-native deployment models, containerized mapping services, low-code/no-code interfaces, and the integration of mapping tools with data catalogues and data fabric infrastructures.

Additionally, the report covers market dynamics such as competitive intensity among more than 45 vendors, strategic initiatives like product launches and partnerships, and innovation trends in data intelligence. Niche segments, such as regulation-driven mapping in highly regulated industries and real-time mapping for event-driven architectures, are also addressed. The detailed scope helps decision-makers understand technological, regional, and industry-level levers driving demand and provides insight into the future trajectory and investment opportunities within the data mapping domain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 372.94 Million |

|

Market Revenue in 2032 |

USD 695.42 Million |

|

CAGR (2025 - 2032) |

8.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Talend, IBM, Microsoft, MuleSoft, Precisely, Tibco Software, Denodo, CloverDX, Adeptia, Informatica, SnapLogic, Boomi |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |