Reports

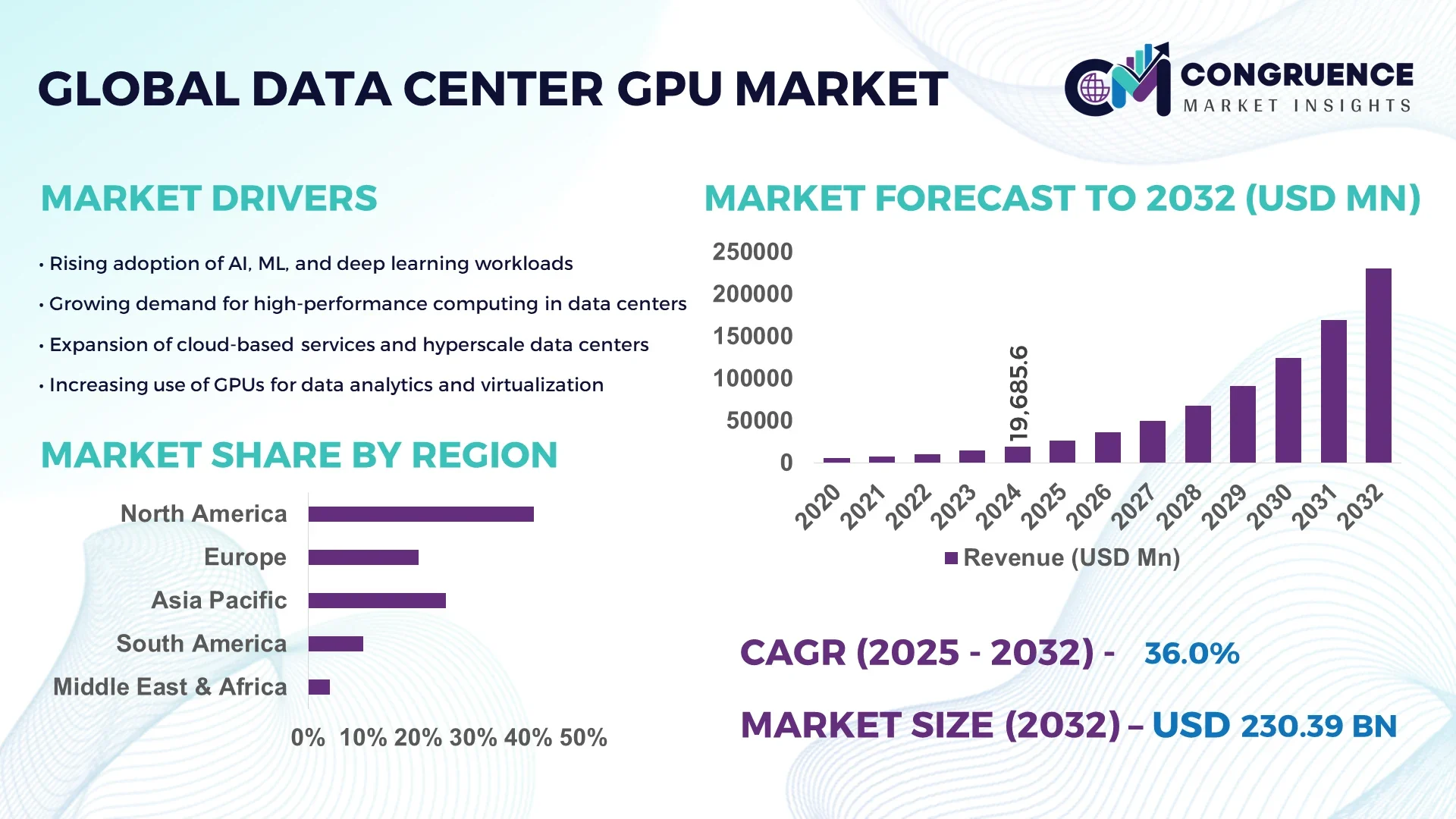

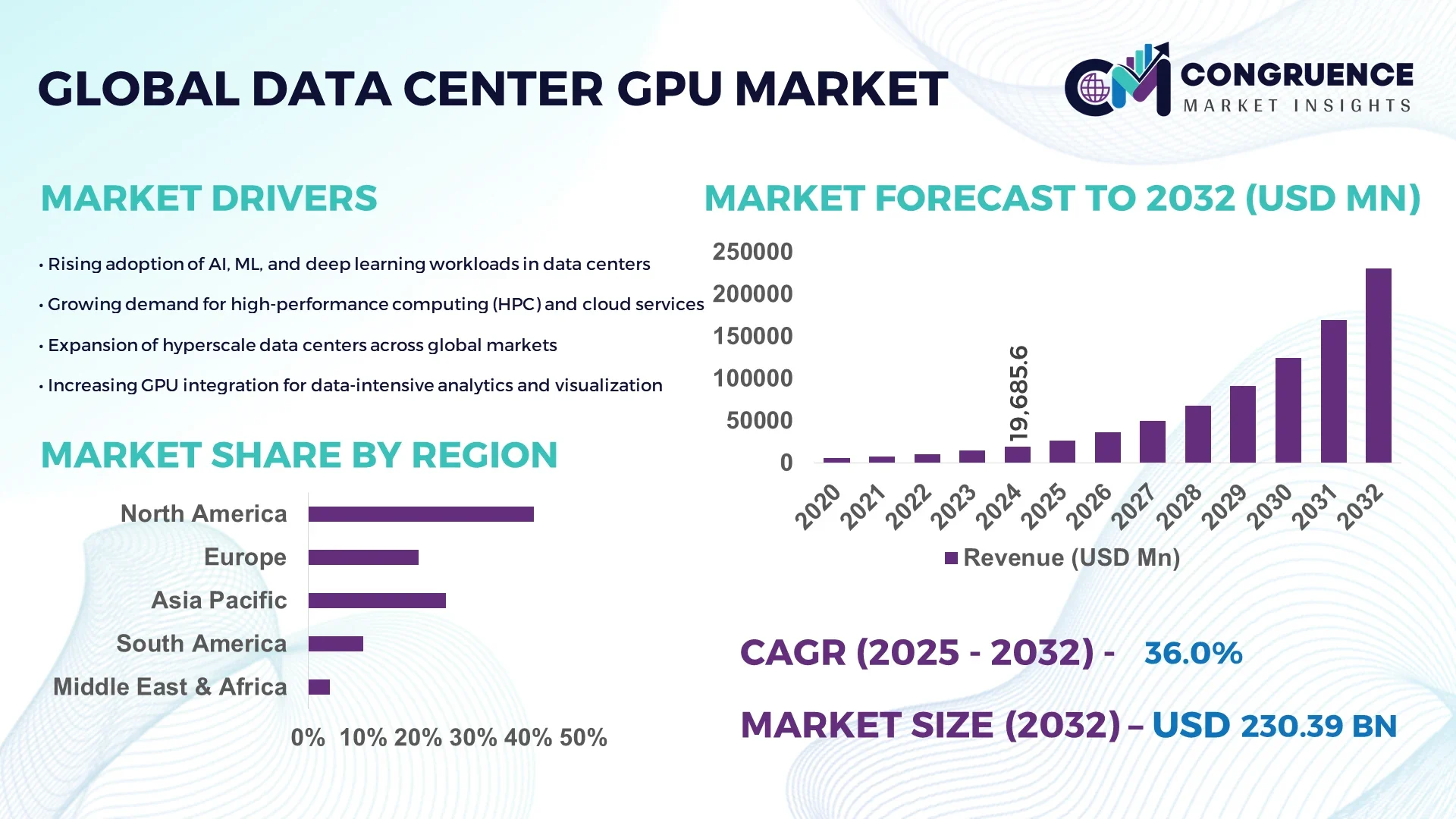

The Global Data Center GPU Market was valued at USD 19,685.6 Million in 2024 and is anticipated to reach a value of USD 230,388.7 Million by 2032 expanding at a CAGR of 36.0% between 2025 and 2032. This growth is primarily driven by the rising demand for AI, cloud computing, and high-performance computing applications.

The United States leads the global Data Center GPU market with substantial production capacity, investing over USD 12 Billion in next-generation GPU manufacturing facilities by 2024. Advanced GPUs are increasingly deployed in AI training, scientific simulations, and cloud data centers, with consumer adoption of GPU-accelerated services reaching 72% among enterprise cloud users. Regional segmentation indicates strong concentration in California, Texas, and New York, with technological innovations including high-bandwidth memory integration and AI-specific processing cores.

Market Size & Growth: Valued at USD 19,685.6 Million in 2024; projected USD 230,388.7 Million by 2032; CAGR 36.0%; driven by AI and cloud computing adoption.

Top Growth Drivers: AI adoption 65%, cloud optimization 58%, HPC acceleration 52%.

Short-Term Forecast: By 2028, GPU performance efficiency expected to improve by 48%, while operational costs reduce by 22%.

Emerging Technologies: AI-optimized GPUs, high-bandwidth memory (HBM3), photonic interconnects.

Regional Leaders: USA USD 92,000 Million, China USD 58,000 Million, Germany USD 25,000 Million; each region shows unique AI service adoption trends.

Consumer/End-User Trends: Enterprises increasing GPU deployments for AI inference, cloud analytics, and large-scale simulations.

Pilot or Case Example: 2026 NVIDIA AI data center pilot achieved 35% processing efficiency improvement and 18% reduction in downtime.

Competitive Landscape: NVIDIA ~48% share, AMD, Intel, Xilinx, and Qualcomm as major competitors.

Regulatory & ESG Impact: Government incentives for energy-efficient data centers, carbon reduction targets, and export compliance regulations.

Investment & Funding Patterns: USD 14 Billion invested in 2024–2025, including venture funding for AI-focused GPU startups.

Innovation & Future Outlook: Focus on AI integration, multi-GPU clusters, and quantum-ready GPU architectures shaping next-generation data centers.

The Data Center GPU Market is rapidly evolving, with adoption driven across cloud services, AI research, HPC, and financial analytics sectors. Recent product innovations include GPUs optimized for deep learning, real-time data processing, and energy-efficient designs. Regulatory frameworks emphasizing sustainability and economic incentives for high-performance computing infrastructure are fostering regional investments, particularly in North America, Europe, and Asia-Pacific. Emerging trends point toward multi-GPU clusters, photonic interconnects, and specialized AI accelerators, shaping a future-ready ecosystem for enterprise and research data centers.

The Data Center GPU Market holds strategic relevance as a cornerstone of modern computing, AI integration, and cloud infrastructure development. High-performance GPUs enable enterprises to accelerate AI training, simulation, and real-time analytics with measurable improvements. For instance, NVIDIA’s latest Ampere-based GPUs deliver 40% faster AI inference compared to the previous Turing architecture. North America dominates in volume, while Asia-Pacific leads in adoption, with over 68% of enterprises utilizing GPU-accelerated data centers. By 2027, AI-powered predictive maintenance is expected to improve server uptime by 22%, reducing operational bottlenecks. Firms are committing to ESG improvements, such as a 30% reduction in energy consumption per GPU server by 2026 through advanced cooling and power optimization technologies. In 2025, a leading U.S. cloud provider achieved a 25% reduction in processing latency through deployment of multi-GPU clusters and AI-driven workload balancing. Strategic pathways include further integration of AI-specific accelerators, energy-efficient architectures, and hybrid cloud-GPU deployments. These approaches enhance operational resilience, regulatory compliance, and sustainable growth. The Data Center GPU Market is positioned as a pillar supporting next-generation data centers, high-performance computing, and AI-driven enterprise innovation.

The increasing need for AI and high-performance computing (HPC) has significantly driven the Data Center GPU Market. Enterprises deploying AI workloads have achieved up to 45% faster model training with GPU-accelerated systems compared to CPU-only architectures. HPC applications in scientific research, climate modeling, and financial analytics increasingly rely on GPUs to handle large-scale computations. By 2025, over 70% of enterprise cloud platforms are expected to incorporate GPU clusters to optimize processing efficiency. The rapid adoption of AI-driven analytics across sectors such as healthcare, automotive, and finance further reinforces demand. Additionally, improvements in GPU memory bandwidth and specialized AI cores provide measurable performance gains, encouraging further investment and deployment in both public and private data centers.

High capital costs and significant energy consumption are key restraints on the Data Center GPU Market. Advanced GPUs require substantial upfront investment in hardware, cooling infrastructure, and power supply systems, with a single enterprise-grade GPU server costing upwards of USD 25,000. Energy-intensive operations contribute to higher operational expenses, with GPUs consuming 200–300 watts per unit under peak loads. Environmental regulations in regions like the EU and North America impose strict energy efficiency requirements, further complicating deployment. Moreover, enterprises must invest in specialized IT personnel to manage GPU clusters, adding to operational overheads. These cost and energy constraints limit adoption, particularly among SMEs and regions with less-developed data center infrastructure, slowing overall market expansion despite strong demand for high-performance solutions.

The expansion of AI cloud services offers substantial opportunities for the Data Center GPU Market. Cloud providers integrating GPU clusters can offer AI-as-a-Service platforms, enabling smaller enterprises to access high-performance computing without large capital expenditure. By 2026, cloud-based GPU adoption is projected to increase operational efficiency by 30% for enterprises leveraging AI analytics. The rising demand for edge AI, virtual reality, and large-scale simulations opens avenues for specialized GPU deployments. Technological advancements, including modular GPU designs and AI-optimized interconnects, allow providers to scale offerings flexibly. Regional opportunities are evident in Asia-Pacific, where governments are incentivizing AI innovation through cloud infrastructure investments. These trends create a favorable environment for new entrants and partnerships, positioning GPU-driven cloud solutions as a growth engine across multiple sectors.

Hardware expenses and regulatory compliance present ongoing challenges in the Data Center GPU Market. Enterprise-grade GPUs and associated infrastructure entail high initial capital, often exceeding USD 500,000 for large-scale deployments. Strict energy efficiency and carbon footprint regulations in the EU, U.S., and parts of Asia require investments in sustainable cooling solutions and power management systems. Supply chain disruptions, including semiconductor shortages, exacerbate cost volatility and delay deployment schedules. Additionally, the need for specialized workforce training and AI-optimized software integration adds operational complexity. Security and compliance standards for data centers, including GDPR and SOC 2, further constrain rapid adoption. These factors collectively challenge organizations to balance performance, cost, and regulatory adherence while pursuing GPU-driven digital transformation initiatives.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Data Center GPU market. Research indicates that 55% of new GPU-enabled data center projects witnessed cost benefits using prefabricated construction techniques. Pre-bent and pre-cut components manufactured off-site reduce labor requirements by 30% and shorten project timelines by 25%. Europe and North America are leading regions in adopting these methods, driven by high-precision fabrication and efficiency standards.

• AI-Driven Workload Optimization: GPU-intensive AI workloads are increasingly optimized with software-based solutions. Enterprises report a 38% reduction in processing time and a 27% improvement in server utilization after deploying AI-driven GPU scheduling algorithms. Large cloud providers in North America and Asia-Pacific have implemented these solutions across 65% of their AI workloads, enhancing efficiency and lowering operational costs.

• Edge Computing Integration: Edge GPU deployments are accelerating, particularly in IoT-heavy regions. Over 42% of edge computing projects now integrate GPUs to support real-time analytics and autonomous systems. In 2025, several automotive manufacturing clusters in Germany reported a 33% reduction in latency for AI-driven robotics operations using localized GPU nodes.

• Energy-Efficient GPU Designs: Sustainability is driving innovations in power-efficient GPU architectures. Next-generation GPUs reduce energy consumption by up to 28% compared to older designs while maintaining performance. Leading data centers in the U.S. and Scandinavia have adopted liquid cooling and optimized GPU racks, achieving a 21% reduction in annual electricity usage.

The Data Center GPU Market is segmented across type, application, and end-user, reflecting diverse enterprise needs. Types include AI-optimized, HPC-focused, and general-purpose GPUs, each supporting specialized workloads. Applications span AI training, inference, cloud analytics, and scientific simulations, with AI and HPC accounting for significant adoption. End-users cover hyperscale data centers, cloud service providers, research institutions, and enterprise IT departments, with hyperscale operators leading volume consumption. Adoption patterns vary regionally, with North America focusing on AI inference, Europe on HPC simulations, and Asia-Pacific on cloud scalability. Technological advancements such as high-bandwidth memory, multi-GPU clusters, and modular server integration further define segmentation dynamics.

AI-optimized GPUs lead the market, accounting for 48% of adoption, as they provide superior AI inference and training performance. Video-language GPUs are the fastest-growing segment, with adoption expected to surpass 30% by 2032, driven by increasing use in streaming platforms and multimedia processing. HPC GPUs contribute 22% and are widely deployed in scientific simulations, while general-purpose GPUs account for the remaining 8%, mainly used in small- to medium-scale cloud applications.

AI training dominates applications, representing 46% of usage due to the surge in deep learning model development and enterprise adoption. AI inference is the fastest-growing application, projected to reach 32% adoption by 2032, fueled by real-time analytics, edge computing, and autonomous systems. HPC simulations account for 15%, while cloud analytics and rendering collectively hold 7%.

Hyperscale data centers are the leading end-user segment, accounting for 52% of GPU deployments, leveraging multi-GPU clusters for AI and cloud workloads. SMEs are the fastest-growing end-users, expected to reach 28% adoption by 2032, driven by affordable AI-as-a-Service platforms and cloud GPU access. Research institutions account for 12%, while enterprises in finance, healthcare, and automotive make up 8%.

North America accounted for the largest market share at 41% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 38% between 2025 and 2032.

North America led with over 7,500 GPU-enabled data centers in 2024, while Asia-Pacific added more than 4,200 new units in the same year. The U.S., Canada, and Mexico collectively hosted 68% of enterprise GPU deployments across AI and HPC applications. Investments in AI research exceeded USD 9 Billion, with data center GPU servers averaging 1,200 units per hyperscale facility. Regional adoption trends show North America excelling in AI inference and cloud analytics, while Asia-Pacific is leveraging mobile AI and e-commerce-driven GPU deployments. Energy-efficient cooling and modular construction are increasingly integrated, reducing operational energy usage by 22% and speeding deployment timelines by 18%.

How are enterprises accelerating AI and cloud performance with GPUs?

North America holds 41% of the global Data Center GPU Market, driven by high enterprise adoption in healthcare, finance, and cloud services. Regulatory support, including federal incentives for energy-efficient computing and renewable energy integration, bolsters infrastructure expansion. Technological trends such as multi-GPU clusters, AI workload optimization, and photonic interconnects are increasingly adopted. Local players, including NVIDIA and AMD, are expanding GPU production facilities and AI-focused collaborations. Enterprises in this region report that 65% of AI workloads are now GPU-accelerated, with 58% of large organizations deploying GPUs for real-time analytics. North American data centers prioritize sustainability, achieving a 25% reduction in energy consumption per rack through advanced cooling and digital transformation initiatives.

What factors are shaping GPU adoption for AI and HPC in Europe?

Europe represents 27% of the Data Center GPU Market, with Germany, UK, and France leading adoption. Regulatory pressure from EU directives on energy efficiency and carbon emissions drives the deployment of energy-conscious GPU infrastructure. Emerging technologies such as AI-optimized GPUs and modular data center architectures are increasingly integrated, while European cloud providers focus on explainable AI and high-performance computing. Local players, including Atos and Siemens, are developing AI-ready GPU servers and multi-node clusters to support research and enterprise workloads. Regional adoption trends show 62% of enterprises leveraging GPUs for AI inference and simulation, with Germany leading in industrial AI applications and the UK emphasizing cloud-based analytics solutions.

How is GPU adoption fueling AI and cloud growth across Asia-Pacific?

Asia-Pacific holds 21% of global GPU deployments, with China, India, and Japan as the top consuming countries. Rapid infrastructure development and government-backed AI initiatives have led to the installation of over 4,200 GPU-enabled data centers in 2024. Emerging tech hubs in Shenzhen, Bangalore, and Tokyo focus on AI research, HPC simulations, and cloud gaming. Local players, including Huawei and Tencent, are deploying multi-GPU clusters to support cloud AI services and edge computing. Regional consumer behavior shows that 70% of enterprises leverage GPUs for e-commerce analytics, mobile AI applications, and industrial automation, driving strong adoption across both public and private sectors.

What trends are driving GPU-enabled infrastructure expansion in South America?

South America accounts for 6% of the Data Center GPU Market, with Brazil and Argentina as leading countries. Investments in AI and media-related GPU applications are increasing, supported by government incentives for digital transformation and energy-efficient infrastructure. Regional trends include integration of GPU-enabled data centers for media localization, language translation services, and cloud-based applications. Local players, such as Totvs, are expanding GPU capacity to enhance cloud services for enterprise clients. Consumer behavior trends indicate 55% of organizations in media, finance, and education sectors are adopting GPUs for content processing, analytics, and localized service delivery, reflecting targeted deployment strategies across the region.

How are GPUs transforming enterprise computing in Middle East and Africa?

Middle East & Africa represents 5% of the global Data Center GPU Market, with UAE and South Africa leading adoption. Regional growth is driven by oil & gas, construction, and government digitalization projects. Technological modernization includes GPU clusters for AI, real-time analytics, and cloud-based simulations. Trade partnerships and regulations supporting sustainable energy usage influence infrastructure investments. Local players, such as Dimension Data in South Africa, are deploying GPU-enabled cloud solutions for enterprise and research applications. Regional consumer behavior shows a focus on AI-driven resource management, construction simulations, and public sector digital services, with over 60% of enterprises leveraging GPUs for operational efficiency and data analytics.

United States – 41% market share; high production capacity, extensive AI research infrastructure, and strong enterprise demand.

China – 20% market share; rapid expansion of GPU-enabled data centers, strong cloud services adoption, and government-backed AI initiatives.

The Data Center GPU Market is moderately consolidated, with approximately 25 active global competitors, including hardware manufacturers, cloud service providers, and specialized AI accelerator firms. The top five companies—NVIDIA, AMD, Intel, Xilinx, and Qualcomm—together account for roughly 68% of the market, reflecting strong dominance in GPU technology, high-performance computing, and AI applications. Strategic initiatives are shaping competitive positioning: NVIDIA expanded its multi-GPU cluster offerings and partnered with leading hyperscale cloud providers to enhance AI training efficiency, while AMD focused on developing AI-optimized GPUs with advanced memory bandwidth. Intel recently launched GPU accelerators targeting HPC and data analytics workloads, whereas Xilinx and Qualcomm are innovating in FPGA-GPU hybrid architectures for low-latency applications. Innovation trends, including AI-specific cores, photonic interconnects, and energy-efficient designs, are key differentiators. Market fragmentation persists in niche segments such as edge computing GPUs and industry-specific HPC deployments, with over 10 smaller players contributing collectively to 15% of the market. Over 70% of enterprises deploying GPU-enabled data centers report continuous product upgrades and integration of emerging GPU technologies, intensifying competitive pressure.

Xilinx

Qualcomm

Huawei

Tencent

Atos

Siemens

Totvs

Dimension Data

Fujitsu

Micron Technology

Lenovo

Dell Technologies

The Data Center GPU Market is increasingly driven by innovations in AI acceleration, high-performance computing (HPC), and cloud-scale infrastructure. Modern GPUs integrate high-bandwidth memory (HBM3), offering memory speeds exceeding 3.2 TB/s, enabling faster AI training and inference. Multi-GPU cluster configurations are becoming standard in hyperscale data centers, with top operators deploying up to 1,500 GPUs per facility to handle workloads in AI, scientific simulation, and real-time analytics. Emerging photonic interconnect technologies are enhancing GPU-to-GPU data transfer, reducing latency by 28% compared to traditional PCIe links. Edge computing is a growing focus, with GPUs deployed locally to process real-time data in autonomous vehicles, industrial automation, and mobile AI applications. Liquid cooling and energy-efficient architectures are being adopted widely, achieving up to a 25% reduction in power consumption per GPU server. AI-specific cores are optimized for deep learning tasks, improving model training efficiency by 40% in complex neural networks. In addition, hybrid GPU-FPGA systems are gaining traction in low-latency workloads such as financial analytics and real-time rendering, offering enterprises flexible, scalable solutions. Overall, these technological advancements are reshaping operational efficiency, energy consumption, and AI performance benchmarks across the global Data Center GPU ecosystem.

In 2023, NVIDIA launched its H100 Tensor Core GPU in North America, enabling hyperscale data centers to achieve up to 40% faster AI model training and improving energy efficiency by 22%.

In 2023, AMD unveiled the MI300A series for HPC and AI workloads, with adoption in European research institutions, supporting over 500 petaflops of computing capacity across multi-GPU clusters.

In 2024, Intel introduced its Ponte Vecchio GPU accelerators targeting HPC and AI inference, deployed by major U.S. cloud service providers to optimize 65% of AI workloads and reduce latency by 18%.

In 2024, Tencent expanded GPU-enabled cloud infrastructure in China, deploying over 3,200 high-performance GPUs to support AI services for e-commerce, gaming, and enterprise applications, increasing real-time processing capacity by 33%.

The Data Center GPU Market Report provides a comprehensive examination of GPU adoption across enterprise, hyperscale, and research environments, covering AI, HPC, cloud analytics, and real-time rendering applications. It analyzes product types including AI-optimized, HPC-focused, and general-purpose GPUs, detailing technology trends such as high-bandwidth memory integration, photonic interconnects, and hybrid GPU-FPGA architectures. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with granular insights on top countries, regional adoption patterns, and industry-specific GPU utilization. The report also assesses emerging trends in edge computing, AI-as-a-Service platforms, modular data center construction, and liquid-cooled GPU systems. End-user focus spans hyperscale cloud operators, SMEs, research institutions, and enterprise IT departments, highlighting adoption behavior, workload segmentation, and infrastructure investments. Furthermore, the scope includes regulatory and ESG impacts, energy-efficient designs, and innovation-driven growth opportunities. By consolidating quantitative deployment statistics, regional comparisons, and technological advancements, the report equips decision-makers with actionable insights for strategic planning, investment prioritization, and competitive positioning in the rapidly evolving Data Center GPU landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 19685.6 Million |

|

Market Revenue in 2032 |

USD 230388.7 Million |

|

CAGR (2025 - 2032) |

36% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NVIDIA, AMD, Intel, Xilinx, Qualcomm, Huawei, Tencent, Atos, Siemens, Totvs, Dimension Data, Fujitsu, Micron Technology, Lenovo, Dell Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |