Reports

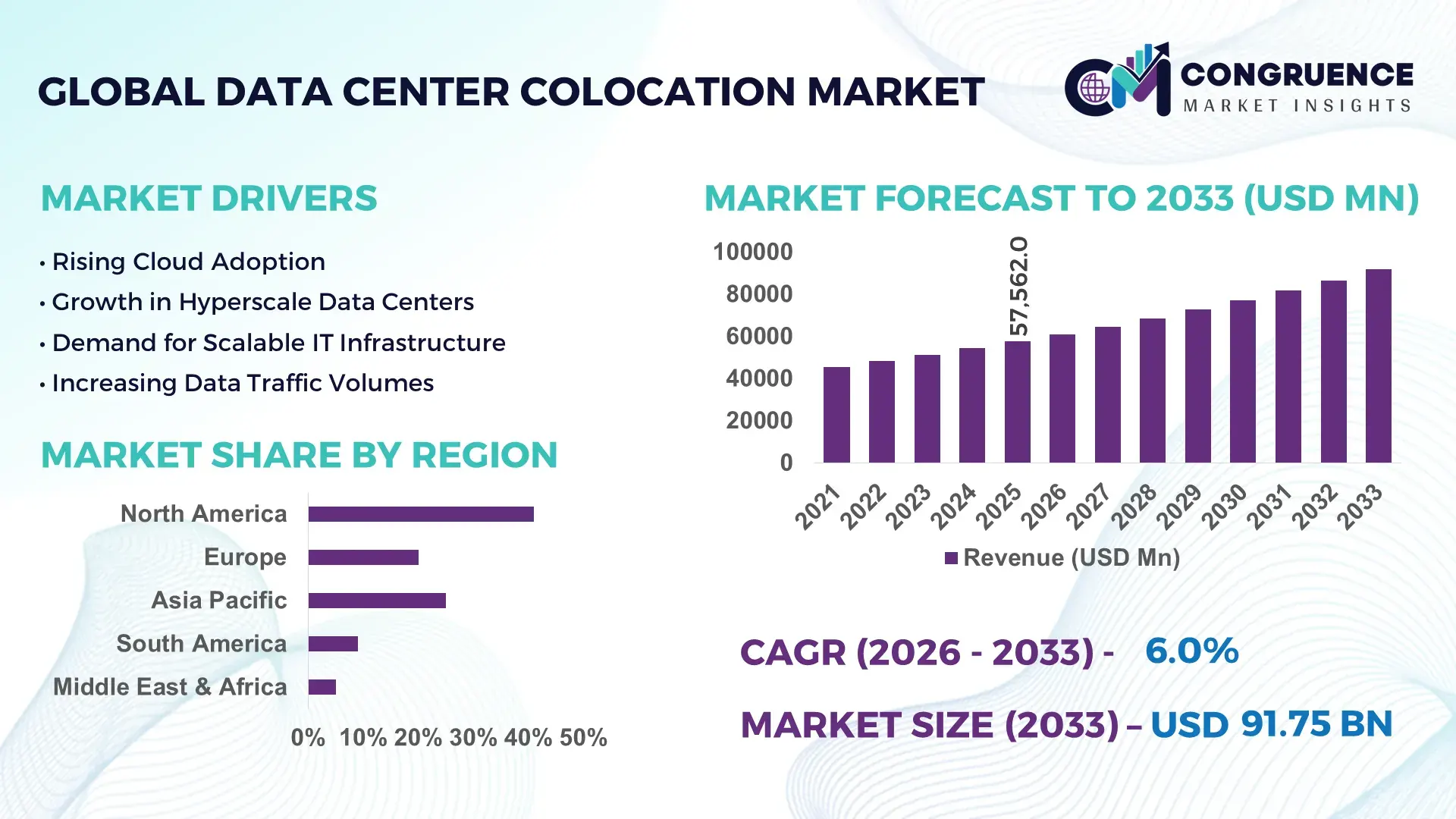

The Global Data Center Colocation Market was valued at USD 57562.02 Million in 2025 and is anticipated to reach a value of USD 91745.12 Million by 2033 expanding at a CAGR of 6% between 2026 and 2033. Growth is primarily supported by rising enterprise demand for scalable, cost-efficient IT infrastructure and accelerated cloud and edge computing adoption.

The United States represents the dominant country in the global data center colocation landscape, supported by extensive hyperscale-ready capacity, deep capital investment, and advanced infrastructure ecosystems. As of 2025, the U.S. hosts over 5,300 operational data centers, with colocation facilities accounting for more than 55% of new capacity additions annually. Annual investments exceeding USD 18 billion are directed toward multi-tenant and interconnection-focused facilities. Key applications span cloud services, financial trading platforms, content delivery networks, healthcare data hosting, and government workloads. Technological advancements include widespread deployment of liquid cooling, AI-optimized racks exceeding 30 kW per cabinet, and renewable-powered campuses, with over 45% of new U.S. colocation capacity tied to long-term clean energy power purchase agreements.

Market Size & Growth: Valued at USD 57562.02 Million in 2025, projected to reach USD 91745.12 Million by 2033 at a CAGR of 6%, driven by enterprise migration from on-premise data centers to flexible colocation models.

Top Growth Drivers: Hybrid cloud adoption at 68%, operational cost optimization of 32%, and energy efficiency improvements of 27%.

Short-Term Forecast: By 2028, average colocation operating costs are expected to decline by 14% through energy optimization and automation.

Emerging Technologies: AI-ready data halls, liquid and immersion cooling systems, software-defined interconnection platforms.

Regional Leaders: North America projected at USD 38200 Million by 2033 with hyperscale interconnection growth; Europe at USD 26700 Million driven by sovereign data requirements; Asia Pacific at USD 21400 Million led by cloud-native enterprise adoption.

Consumer/End-User Trends: BFSI, cloud service providers, and digital media firms increasingly prefer multi-site colocation for latency reduction and disaster recovery.

Pilot or Case Example: In 2024, a large-scale colocation campus expansion achieved a 22% reduction in downtime through AI-based predictive maintenance.

Competitive Landscape: Equinix holds approximately 18% share, followed by Digital Realty, NTT Global Data Centers, CyrusOne, and ST Telemedia Global Data Centres.

Regulatory & ESG Impact: Stricter energy efficiency norms and carbon reporting mandates are accelerating adoption of green colocation facilities.

Investment & Funding Patterns: Over USD 42 billion invested globally during 2023–2025, with strong momentum in REIT-backed and green-financed projects.

Innovation & Future Outlook: Integration of edge colocation, high-density AI workloads, and renewable-powered campuses is shaping next-generation deployments.

The Data Center Colocation Market serves critical industry sectors including cloud service providers contributing approximately 38% of demand, BFSI at nearly 21%, digital content and media at 17%, and healthcare and government workloads collectively exceeding 14%. Recent innovations such as modular prefabricated data halls, AI-driven energy management platforms, and high-density rack configurations are improving scalability and efficiency. Regulatory pressure around data sovereignty, energy consumption, and emissions is reshaping facility design and location strategies, while economic drivers include enterprise cost containment and rapid digitalization. Regionally, North America leads consumption, followed by Europe’s compliance-driven growth and Asia Pacific’s rapid capacity expansion. Emerging trends point toward edge colocation, carbon-neutral campuses, and AI-centric infrastructure as key growth avenues through the next decade.

The Data Center Colocation Market holds strong strategic relevance as enterprises increasingly prioritize operational resilience, regulatory compliance, and infrastructure flexibility amid accelerating digital transformation. Colocation enables organizations to balance cost control with high-performance computing needs while retaining control over critical workloads. Advanced technologies are redefining competitive benchmarks; for instance, liquid cooling delivers nearly 30% improvement in energy efficiency compared to traditional air-cooling standards, directly improving power usage effectiveness and rack density. Regionally, North America dominates in volume due to large-scale hyperscale campuses, while Asia Pacific leads in adoption with approximately 64% of enterprises actively expanding colocation footprints to support cloud-native and AI workloads.

Short-term strategic pathways emphasize automation and intelligence. By 2028, AI-driven infrastructure management is expected to improve uptime and predictive maintenance efficiency by 25%, reducing unplanned outages and optimizing asset utilization. Sustainability and compliance are becoming embedded in strategic planning, with firms committing to ESG improvements such as 40% carbon emission reduction and over 50% renewable energy sourcing by 2030. A micro-scenario illustrates this shift: in 2024, a leading U.S.-based colocation provider achieved a 22% reduction in energy consumption intensity through AI-powered cooling optimization and real-time energy analytics. Looking forward, the Data Center Colocation Market is positioned as a foundational pillar supporting enterprise resilience, regulatory alignment, and sustainable digital growth across global economies.

The accelerating shift toward hybrid and multi-cloud architectures is a primary driver of the Data Center Colocation Market. Over 70% of large enterprises now operate hybrid IT environments, requiring neutral, carrier-dense facilities to interconnect private infrastructure with multiple cloud platforms. Colocation enables enterprises to reduce capital expenditure on owned facilities while improving scalability and disaster recovery readiness. High-density racks exceeding 25–30 kW are increasingly deployed to support AI and analytics workloads, driving demand for advanced colocation capabilities. Additionally, financial services, healthcare, and digital media sectors rely on colocation to meet latency-sensitive application requirements and regulatory compliance, reinforcing sustained demand across industries.

Power availability and energy pricing represent significant restraints for the Data Center Colocation Market. In several mature markets, grid congestion and long utility connection timelines delay new facility deployments. Energy costs have risen by more than 20% in certain regions over recent years, directly impacting operating expenses for colocation providers and tenants. High-density AI workloads further intensify power demand, often exceeding local infrastructure capacity. These constraints can limit expansion in prime metropolitan areas and force operators to seek secondary locations, increasing network complexity and potentially affecting latency-sensitive applications.

The rapid expansion of edge computing presents substantial opportunities for the Data Center Colocation Market. Applications such as autonomous systems, smart cities, and real-time video analytics require processing closer to end users, driving demand for smaller, distributed colocation facilities. Enterprises are increasingly deploying workloads across multiple edge sites to achieve latency reductions of up to 40%. This shift opens opportunities in tier-2 and tier-3 cities, where land and power availability are comparatively favorable. Colocation providers that integrate edge infrastructure with centralized hyperscale campuses can offer unified, scalable platforms supporting next-generation digital services.

Regulatory complexity and sustainability mandates pose ongoing challenges for the Data Center Colocation Market. Data protection laws, cross-border data transfer restrictions, and industry-specific compliance requirements increase operational and administrative burdens. Simultaneously, governments and enterprises demand measurable reductions in water usage, carbon emissions, and electronic waste. Meeting these standards requires significant investment in renewable energy sourcing, advanced cooling technologies, and reporting systems. Smaller operators may struggle to absorb these costs, while inconsistent regulations across regions complicate global expansion strategies, affecting speed to market and long-term planning.

Rise in Modular and Prefabricated Construction Accelerating Deployment Timelines

Modular and prefabricated construction methods are increasingly shaping capacity expansion strategies in the Data Center Colocation market. Around 55% of newly announced colocation projects report measurable cost benefits from modular builds, with deployment timelines shortened by nearly 30% compared to traditional construction. Factory-built power and cooling modules enable standardized quality control and reduce on-site labor requirements by over 25%. Adoption is particularly strong in Europe and North America, where rapid capacity delivery and skilled labor constraints are driving demand for pre-engineered data hall components.

Growing Shift Toward High-Density and AI-Optimized Colocation Facilities

Colocation facilities are rapidly transitioning toward high-density configurations to support AI, machine learning, and advanced analytics workloads. More than 48% of new colocation deployments now support rack densities above 25 kW, compared to less than 20% five years ago. Liquid and hybrid cooling solutions are being integrated to manage thermal loads, improving energy efficiency by approximately 20%. This trend is reshaping facility design, with greater emphasis on reinforced power distribution, advanced airflow management, and scalable cooling architectures.

Increasing Emphasis on Sustainability and Renewable Energy Integration

Sustainability has become a central trend in the Data Center Colocation market, with over 60% of operators committing to renewable energy sourcing for new facilities. Many colocation campuses now achieve power usage effectiveness levels below 1.4, representing efficiency improvements of nearly 18% compared to older sites. Water-efficient cooling technologies have reduced water consumption by up to 25% in water-stressed regions. These initiatives are driven by enterprise ESG requirements and regulatory pressure for transparent environmental performance.

Expansion of Interconnection-Rich and Edge-Oriented Colocation Models

Demand for low-latency connectivity is driving the expansion of interconnection-dense and edge-focused colocation facilities. Approximately 42% of enterprises deploying latency-sensitive applications now utilize multiple colocation sites within a single region to reduce network latency by 35%. Edge colocation nodes located closer to population centers support use cases such as content delivery, IoT analytics, and real-time financial trading. This trend is increasing the strategic value of colocation providers offering dense carrier ecosystems and geographically distributed infrastructure.

The Data Center Colocation Market is segmented based on type, application, and end-user, each reflecting distinct infrastructure requirements, workload characteristics, and adoption drivers. By type, retail, wholesale, and hybrid colocation models address varying scalability and control needs, with enterprise preferences shifting toward flexible, interconnection-rich environments. Application-based segmentation highlights strong demand from cloud enablement, disaster recovery, and high-performance computing, driven by digital transformation and data-intensive operations. End-user insights reveal concentrated adoption among cloud service providers, BFSI institutions, and digital content platforms, while healthcare, government, and manufacturing show accelerating uptake due to compliance and latency requirements. These segments collectively illustrate how operational scale, regulatory intensity, and workload density shape purchasing decisions across the Data Center Colocation Market.

Retail colocation currently represents the leading type, accounting for approximately 46% of total adoption, supported by strong demand from small and mid-sized enterprises seeking scalable space, power, and interconnection without long-term capacity commitments. Wholesale colocation follows with nearly 34% share, favored by hyperscale cloud providers and large enterprises deploying multi-megawatt capacity blocks to support AI and cloud-native workloads. Hybrid colocation models, combining retail flexibility with wholesale scale, account for around 20% and are gaining relevance for enterprises balancing cost optimization with growth flexibility. Wholesale colocation is the fastest-growing type, expanding at an estimated 7.8% CAGR, driven by hyperscale expansion, high-density rack deployments exceeding 30 kW, and long-term capacity contracts. The remaining niche formats, including managed and custom-built colocation solutions, collectively contribute under 15%, serving specialized compliance-driven or latency-sensitive use cases.

Cloud enablement and hybrid IT connectivity dominate application usage, contributing nearly 41% of total demand, as enterprises rely on colocation to interconnect private infrastructure with multiple public cloud platforms. Disaster recovery and business continuity applications follow with about 23%, reflecting increased focus on operational resilience and multi-site redundancy. High-performance computing and AI workloads account for roughly 19%, supported by rising adoption of GPU-dense environments and advanced cooling systems. Edge computing and content delivery applications collectively contribute around 17%, serving latency-sensitive services. High-performance computing is the fastest-growing application, expanding at an estimated 9.2% CAGR, fueled by AI training, real-time analytics, and simulation workloads requiring high power density and low-latency interconnection.

Cloud service providers represent the largest end-user segment, accounting for approximately 38% of adoption, driven by demand for scalable, carrier-neutral facilities supporting multi-cloud ecosystems. BFSI institutions follow with nearly 24%, relying on colocation for secure, compliant, and low-latency transaction processing. Digital content and media companies contribute about 18%, leveraging colocation to support streaming, content delivery, and real-time analytics. Healthcare, government, manufacturing, and telecom end-users collectively account for around 20%, with healthcare and government showing the fastest expansion. Healthcare is the fastest-growing end-user segment, advancing at an estimated 8.6% CAGR, driven by electronic health records, imaging data growth, and strict data protection requirements.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

North America benefits from more than 5,300 operational data centers, extensive hyperscale capacity, and high enterprise workload concentration. Europe followed with nearly 27% share, driven by compliance-focused infrastructure demand and sustainability mandates. Asia-Pacific captured approximately 23% share, supported by cloud adoption, mobile-first economies, and expanding digital services. South America and the Middle East & Africa collectively accounted for around 9%, reflecting developing-stage infrastructure expansion. Globally, power capacity additions exceeded 7.2 GW in 2025, with Asia-Pacific contributing over 38% of new developments. Data localization requirements, renewable energy integration above 60% in new facilities, and edge deployments across more than 120 metropolitan areas continue to shape regional demand in the Data Center Colocation Market.

How is enterprise-scale digital infrastructure shaping demand intensity across advanced economies?

North America represents approximately 41% of the global Data Center Colocation Market, supported by large-scale enterprise and hyperscale demand. BFSI, healthcare, cloud services, and digital media collectively account for more than 65% of regional workloads. Regulatory developments related to data protection, cybersecurity compliance, and clean energy incentives are influencing facility expansion and modernization. Technological advancements include AI-driven infrastructure management, liquid cooling adoption in nearly 45% of new deployments, and dense interconnection ecosystems enabling latency below 10 milliseconds in major metros. Regional operators continue to expand multi-megawatt campuses and edge colocation nodes. Consumer behavior shows higher enterprise adoption in healthcare and finance, where uptime requirements exceed 99.99% and compliance-driven workloads dominate.

Why is compliance-centric infrastructure redefining deployment strategies across mature digital economies?

Europe accounts for nearly 27% of the Data Center Colocation Market, led by Germany, the UK, France, and the Netherlands. Regulatory frameworks related to data sovereignty, carbon disclosure, and energy efficiency strongly influence deployment strategies. More than 70% of newly developed facilities are designed to meet strict sustainability and reporting thresholds. Adoption of advanced cooling systems and waste heat reuse has improved energy efficiency by around 20% compared to legacy facilities. Local providers are expanding renewable-powered campuses and regional interconnection hubs to support multinational enterprises. Consumer behavior reflects regulatory pressure, increasing demand for transparent, auditable, and environmentally efficient colocation solutions across public sector and regulated industries.

How are digital-first economies accelerating infrastructure scale and density requirements?

Asia-Pacific holds around 23% market share and contributes over 38% of global new capacity additions. China, India, Japan, Singapore, and Australia are the primary consuming countries, driven by cloud services, e-commerce platforms, and mobile applications. Infrastructure trends emphasize high-density deployments, with rack power frequently exceeding 25 kW in urban hubs. Regional innovation centers supporting AI, fintech, and smart manufacturing are increasing demand for low-latency colocation. Local operators are expanding hyperscale-ready campuses exceeding 50 MW per site. Consumer behavior is heavily influenced by e-commerce growth and mobile AI applications, with digital platforms representing more than 45% of regional demand.

What role does regional digital inclusion play in shaping infrastructure demand?

South America accounts for approximately 6% of the global Data Center Colocation Market, with Brazil and Argentina as the primary contributors. Market development is supported by expanding fiber networks, access to renewable energy, and emerging data localization requirements. Over 60% of new facilities are positioned near major urban centers to support fintech platforms, media streaming, and localized cloud services. Government incentives and trade policies promoting digital infrastructure investment are attracting regional and international operators. Modular facility deployment has reduced build timelines by nearly 25%. Consumer behavior shows demand closely linked to media consumption and language-localized digital services.

How are diversification strategies and digital modernization influencing infrastructure build-outs?

The Middle East & Africa represents roughly 3% of global market activity, with demand driven by oil and gas digitalization, smart city initiatives, and financial services modernization. The UAE, Saudi Arabia, and South Africa account for more than 70% of regional capacity. Governments are encouraging development through free zones, cloud-first policies, and investment incentives. Technological modernization includes energy-efficient cooling systems suited for high-temperature environments, improving operational efficiency by nearly 18%. Regional providers are expanding carrier-neutral hubs to support cloud platforms and content delivery. Consumer behavior reflects growing demand from government entities and large enterprises focused on digital sovereignty.

United States – 36% market share

High hyperscale capacity, strong enterprise demand, and advanced interconnection ecosystems support leadership in the Data Center Colocation Market.

China – 14% market share

Large-scale digital platforms, expanding cloud infrastructure, and government-backed development programs drive Data Center Colocation Market demand.

The Data Center Colocation Market is highly competitive and moderately consolidated, with over 1,200 active operators globally spanning hyperscale, enterprise-focused, and regional colocation providers. The top five companies collectively account for approximately 55% of the global market, reflecting strong market positioning by leading players such as Equinix, Digital Realty, and NTT Global Data Centers. Competitive strategies are increasingly focused on interconnection-rich campus expansion, green and renewable-powered facilities, edge colocation rollouts, and multi-cloud integration. Strategic partnerships between cloud service providers and colocation operators are driving enhanced service offerings and reduced latency for enterprise clients. In 2025, over 120 new multi-tenant colocation campuses were commissioned worldwide, reflecting both organic expansion and targeted acquisitions. Innovation trends such as AI-driven predictive maintenance, high-density rack configurations exceeding 30 kW, and modular prefabricated builds are reshaping competitive differentiation. Regional variations in regulatory compliance, ESG mandates, and latency-sensitive demand are influencing market dynamics, with North America and Asia-Pacific leading in volume, while Europe focuses on sustainability and compliance-driven infrastructure. Smaller and regional players are pursuing niche differentiation through specialized services, local interconnection ecosystems, and green energy adoption, contributing to market diversity and competitive intensity.

NTT Global Data Centers

CyrusOne

ST Telemedia Global Data Centres

CoreSite

QTS Realty Trust

Iron Mountain

Interxion

Global Switch

Flexential

Switch

Vantage Data Centers

The Data Center Colocation Market is being reshaped by a range of current and emerging technologies that are enhancing operational efficiency, scalability, and sustainability. AI-driven infrastructure management is increasingly deployed, with over 40% of new colocation facilities incorporating predictive analytics for power, cooling, and workload optimization. These systems reduce downtime by up to 22% and improve energy utilization across high-density racks exceeding 30 kW per cabinet. Liquid and immersion cooling technologies are gaining traction, accounting for approximately 28% of newly commissioned high-density deployments, enabling facilities to manage thermal loads more effectively and reduce water consumption by nearly 25% compared to conventional air cooling.

Edge computing and interconnection-rich platforms are another transformative technology, enabling latency reductions of up to 35% for critical applications in financial services, content delivery, and AI-driven analytics. Over 120 new edge colocation nodes were established globally in 2025 to support distributed workloads and cloud-native applications. Modular and prefabricated construction methods are also being widely adopted, with 55% of new projects leveraging prebuilt power and cooling modules to shorten deployment timelines by 30% and reduce labor requirements by over 25%.

In addition, renewable energy integration and microgrid technologies are advancing rapidly, with more than 60% of new colocation facilities sourcing power from clean energy and implementing energy storage solutions to maintain uptime. High-density interconnection fabrics, software-defined networking, and automated monitoring platforms are further enhancing operational agility and service reliability. These technological advancements collectively position the Data Center Colocation Market as a highly adaptive, energy-efficient, and future-ready infrastructure solution for enterprise, cloud, and hyperscale applications.

• In August 2025, Equinix was named a Leader in the IDC MarketScape: Worldwide Datacenter Colocation Services 2025 Vendor Assessment for its AI-ready infrastructure, extensive interconnection portfolio spanning more than 220 cloud on-ramps, and a global footprint across 76 metros in 36 countries. (Equinix Newsroom)

• In February 2025, Equinix inaugurated the PA13x colocation data center in Meudon, France, designed to support high‑density and AI workloads, integrating heat recovery systems and photovoltaic panels to enhance environmental performance and meet rising European enterprise demand.

• In June 2025, CyrusOne unveiled its 90 MW sixth UK campus in Buckinghamshire, equipped with on‑site solar panels covering 64% of office power, reinforcing regional sustainable capacity expansion and supporting enterprise and hyperscale customer requirements. (TechStock²)

• In 2024 and early 2025, several major strategic shifts occurred across the colocation industry: Digital Realty expanded its PlatformDIGITAL footprint in Japan with a new AI‑ready data hall, NTT acquired land for major multi‑site campuses in Phoenix and Hillsboro, and Equinix completed the acquisition of three carrier‑neutral data centers in Manila, boosting regional interconnection capacity.

The Data Center Colocation Market Report provides a comprehensive view of market segmentation, geographic coverage, technology trends, application domains, and sectoral demand patterns shaping global and regional landscapes. The report delineates type segmentation including retail, wholesale, and hybrid colocation models, analyzing adoption patterns by enterprise size and workload requirements, and highlights infrastructure variants such as high‑density AI‑ready halls and edge colocation nodes. Geographic regions covered encompass North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with insights on regional deployment volumes, infrastructure capacity, regulatory impacts, power availability, and interconnection density across major metropolitan hubs. Application analysis in the report spans cloud enablement, disaster recovery, high‑performance computing, content delivery, and edge services, providing data on application usage percentages and workload distribution across industries.

Technology coverage addresses current and emerging innovations including advanced cooling solutions—liquid and immersion cooling—AI‑driven management systems, modular prefabricated construction, software‑defined networking, and sustainability technologies such as renewable energy integration and energy storage systems. The report also examines competitive dynamics, profiling leading operators, expansion strategies, partnerships, acquisitions, and innovation initiatives influencing market positioning. End‑user and industry insights include adoption behaviors across cloud service providers, BFSI institutions, digital media, healthcare, government, manufacturing, and telecom sectors, with metrics on segment contributions and usage patterns. Additionally, niche and emerging segments such as edge colocation, AI‑optimized infrastructure, and flexible consumption models are addressed, offering decision‑makers a detailed market reference to inform strategy, investment, and infrastructure planning.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 6% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Equinix, Digital Realty, NTT Global Data Centers, CyrusOne, ST Telemedia Global Data Centres, CoreSite, QTS Realty Trust, Iron Mountain, Interxion, Global Switch, Flexential, Switch, Vantage Data Centers |

Customization & Pricing | Available on Request (10% Customization is Free) |