Reports

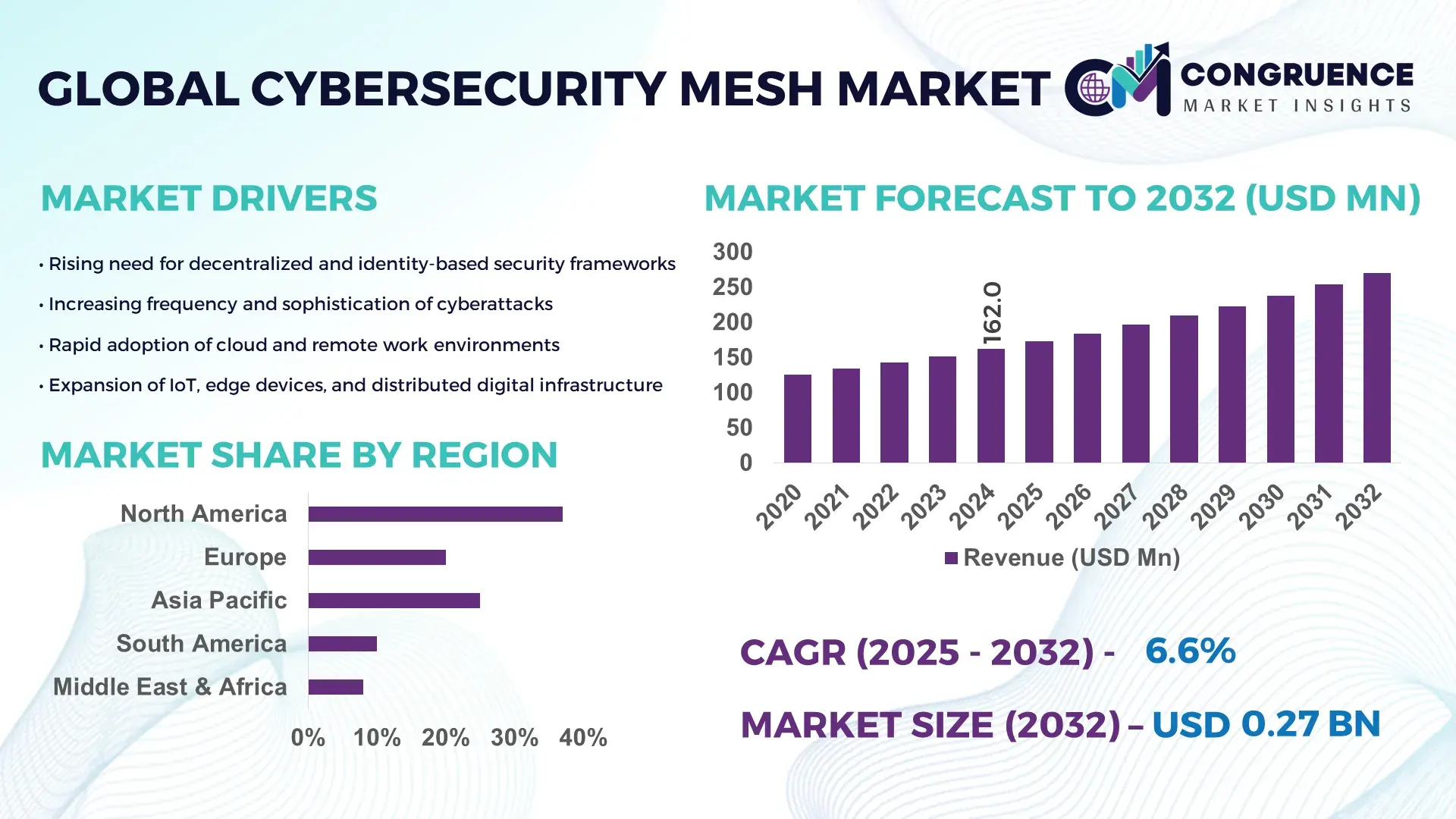

The Global Cybersecurity Mesh Market was valued at USD 162.03 Million in 2024 and is anticipated to reach a value of USD 270.18 Million by 2032 expanding at a CAGR of 6.6% between 2025 and 2032. Growth is fueled by rising enterprise investments in distributed security frameworks to mitigate risks associated with remote and hybrid IT environments.

The United States plays a pivotal role in the Cybersecurity Mesh Market, driven by high deployment of zero-trust security architectures across government, defense, banking, cloud service providers, and large enterprises. More than 58% of Fortune 500 organizations have already integrated cybersecurity mesh frameworks into their digital transformation roadmaps, supported by federal investments exceeding USD 4.9 billion in advanced cyber infrastructure in 2023. The country also hosts over 300 AI-driven cybersecurity solution vendors and records a 32% annual rise in consumption of decentralized authentication tools across cloud and edge computing applications.

• Market Size & Growth: Valued at USD 162.03 Million in 2024, projected to reach USD 270.18 Million by 2032 at a CAGR of 6.6%, driven by rapid adoption of distributed security architecture across cloud and IoT ecosystems.

• Top Growth Drivers: 41% rise in zero-trust adoption, 36% improvement in breach detection efficiency, 28% increase in secure identity management deployments.

• Short-Term Forecast: By 2028, enterprises are expected to achieve up to 33% average reduction in cybersecurity operational costs through automated mesh-based frameworks.

• Emerging Technologies: AI-powered threat intelligence, decentralized digital identity (DID), and blockchain-enabled authentication.

• Regional Leaders: North America projected at USD 113.2 Million by 2032 with high-scale enterprise cloud adoption; Europe expected at USD 72.8 Million driven by GDPR-aligned cybersecurity upgrades; Asia-Pacific projected at USD 64.5 Million with fast adoption across BFSI and telecom.

• Consumer/End-User Trends: BFSI, healthcare, and government sectors lead adoption due to expanding hybrid networks and rising demand for secure access controls.

• Pilot or Case Example: In 2024, a multinational telecom pilot using cybersecurity mesh achieved 47% reduction in system downtime during cyber incidents.

• Competitive Landscape: Market led by Palo Alto Networks with approx. 14% share, followed by IBM, Fortinet, Cisco, Check Point, and Zscaler.

• Regulatory & ESG Impact: Compliance frameworks such as GDPR, HIPAA, and NIS2 mandate decentralized security controls, increasing long-term adoption.

• Investment & Funding Patterns: Over USD 2.1 Billion invested globally in 2023–2024 for AI-enabled mesh cybersecurity platforms and identity access technologies.

• Innovation & Future Outlook: Integration of predictive analytics, self-learning cyber engines, and cross-platform mesh interoperability expected to shape next-generation security infrastructures.

The Cybersecurity Mesh Market is gaining traction across high-risk sectors including BFSI, healthcare, energy, telecommunications, and government, with each contributing strongly to global cybersecurity spending. Innovations such as autonomous breach containment, adaptive identity management, and quantum-resilient encryption are accelerating product development cycles. Regulatory and risk-compliance pressures are fostering faster deployment across Europe and North America, while Asia-Pacific demonstrates the strongest growth momentum due to digital banking and smart-infrastructure investments. Increasing reliance on distributed cloud networks, 5G rollout, and IoT-linked vulnerabilities continues to establish cybersecurity mesh as a core enterprise security layer, with forward-looking adoption expected to combine AI analytics, automated threat response, and security-driven business continuity planning.

The strategic relevance of the Cybersecurity Mesh Market lies in its ability to decentralize protection architectures and deliver security directly to distributed digital assets, users, and applications. Organizations are replacing siloed security tools with unified identity, policy, and access frameworks to reduce breach risk and downtime across cloud, edge, and hybrid infrastructures. Advanced mesh environments support 46% faster threat containment and 38% higher authentication accuracy due to centralized analytics and policy orchestration. AI-driven access monitoring delivers 52% improvement compared to legacy perimeter-based security standards, enabling real-time anomaly detection and automated response at scale. North America dominates in volume, while Europe leads in adoption with 61% of enterprises integrating zero-trust security layers. By 2027, AI-centric mesh security automation is expected to cut manual incident handling time by up to 42%, delivering measurable cost and productivity outcomes. Firms are committing to ESG-aligned cybersecurity operational responsibility, including 28% reduction in energy usage from data center security workloads by 2028. In 2024, a leading Asia-Pacific telecom group achieved a 56% drop in credential misuse incidents through an autonomous identity mesh initiative. Looking forward, the Cybersecurity Mesh Market is positioned to become a foundational layer of digital resilience, regulatory compliance, and sustainable enterprise security growth across global industries.

The Cybersecurity Mesh Market is benefiting significantly from the accelerating shift toward decentralized security models across hybrid and multi-cloud ecosystems. As 73% of global enterprises now operate workloads across multiple cloud platforms, the need for unified identity and policy enforcement has intensified. Cybersecurity mesh enables consistent authentication and authorization across distributed assets, reducing breach response time by up to 45% and lowering unauthorized access attempts by 39%. Highly regulated industries such as BFSI and healthcare are leading deployment, as mesh-based controls allow secure integration of third-party partners, IoT endpoints, and legacy systems without weakening security posture. Enterprises adopting cybersecurity mesh are reporting a 32% improvement in security operations efficiency and a 27% reduction in security tool redundancy through platform consolidation. These measurable operational gains continue to push organizations toward large-scale modernization strategies built on decentralized security frameworks.

The Cybersecurity Mesh Market faces constraints due to the complexity involved in integrating mesh security into existing enterprise environments and the shortage of skilled cybersecurity professionals with expertise in zero-trust and distributed identity frameworks. Global surveys indicate that 68% of organizations struggle to merge legacy security systems with mesh-compatible architectures, often delaying deployment timelines. The deployment process also requires advanced knowledge of AI-driven risk analytics, identity federations, and cross-platform policy automation—skills that remain scarce in the global talent pool. Additionally, 54% of businesses cite high customization requirements and interoperability challenges as primary barriers when migrating from traditional perimeter-based security models. These constraints lead to extended implementation cycles, increased dependence on third-party integration partners, and rising operational complexity, collectively moderating rapid adoption of mesh-based security ecosystems.

The growth of AI-enabled autonomous cybersecurity systems unlocks major opportunities for the Cybersecurity Mesh Market by enabling self-learning and predictive threat response across distributed infrastructures. As organizations accelerate investments in automated security governance, demand for intelligent mesh platforms capable of proactively detecting, correlating, and mitigating threats is expanding. Adoption of autonomous cyber engines increased by 44% globally in 2023–2024, reflecting rising confidence in AI governance across mission-critical environments. Sectors including telecom, BFSI, and energy are increasingly prioritizing identity-driven automation to protect IoT and real-time data networks. Mesh ecosystems equipped with machine learning can reduce mean time to detect (MTTD) by 49% and mean time to respond (MTTR) by 46%, significantly improving operational resilience. These performance gains position AI-enabled cybersecurity mesh as a priority investment area for both mid-sized enterprises and large corporations.

The Cybersecurity Mesh Market faces sustained challenges due to rapidly evolving cyberattack techniques and increasingly stringent compliance requirements across industries and regions. Advanced threats such as deepfake phishing, multi-vector ransomware, and AI-generated malware demand highly adaptive security mechanisms, pushing enterprises to continuously upgrade their mesh frameworks. However, 63% of companies report difficulties in maintaining compliance across jurisdictions such as GDPR, HIPAA, NIS2, and sector-specific security mandates when distributed systems span multiple geographies. Rising audit and reporting obligations add further operational burden, especially for industries managing confidential and regulated data. Additionally, 48% of enterprises cite escalating costs associated with continuous threat intelligence, identity automation, and security analytics updates as a mounting challenge. The need to evolve cybersecurity mesh infrastructures in lockstep with threat sophistication and compliance complexity remains a key factor imposing operational and financial pressure on adopters.

• Rapid Expansion of Zero-Trust Identity Integration Across Distributed Networks: The market is witnessing accelerated adoption of zero-trust identity architectures, with 64% of enterprises integrating decentralized identity verification into cloud and edge environments in 2024. Cybersecurity mesh deployments now support up to 51% faster user authentication and a 43% reduction in unauthorized access attempts across hybrid networks. Adoption of continuous identity monitoring tools has increased by 39% across the BFSI and government sectors as remote and multi-device access becomes standard for enterprise operations.

• AI-Driven Autonomous Threat Detection and Response Increasing Operational Efficiency: AI-enabled mesh frameworks are becoming a core investment priority, with 58% of organizations deploying automated threat intelligence modules to replace manual incident management. This shift enables 49% faster breach containment and 46% improvement in anomaly prediction accuracy. Enterprises incorporating AI in mesh security report a 37% drop in false alerts and a 28% improvement in cyber-resilience scores due to better prioritization of real-time risks and adaptive runtime policies.

• Interoperability and API-Based Security Consolidation Across Multi-Cloud Ecosystems: A growing portion of enterprises — currently 62% — are transitioning from isolated security tools toward unified mesh platforms that consolidate controls across AWS, Azure, Google Cloud, and private databases. This interoperability-driven consolidation delivers measurable outcomes, including a 34% reduction in security management overhead and a 41% improvement in policy enforcement consistency. API-driven mesh deployments support seamless third-party integration, strengthening vendor-agnostic cybersecurity strategies across global industries.

• Increasing Adoption of Distributed Security Analytics for Real-Time Risk Intelligence: Security analytics embedded within cybersecurity mesh deployments are reshaping cyber governance models, with 47% of organizations now utilizing distributed telemetry to monitor endpoints, applications, and identities simultaneously. These analytics engines deliver a 52% boost in risk scoring accuracy and a 44% reduction in dwell time for emerging threats. Industrial, telecom, and energy sectors report up to 36% faster mitigation of operational disruption through real-time threat visualization, policy automation, and cross-platform incident correlation.

The Cybersecurity Mesh Market segmentation reflects evolving enterprise security priorities across diverse deployment environments. By type, solutions range from identity and policy orchestration tools to threat analytics engines and interconnectivity layers designed to unify multi-cloud environments. Applications span across network security, identity and access management, cloud workload protection, and secure operational technology environments. End-user adoption is concentrated in highly regulated industries such as BFSI and healthcare, while telecom, government, manufacturing, and energy are expanding mesh implementations to safeguard distributed data ecosystems. Adoption patterns indicate a shift toward integrated, automation-centric security strategies, with 56% of enterprises prioritizing interoperability across cloud and edge environments and 48% emphasizing intelligent access governance as a primary deployment driver.

Identity and access management (IAM)–centric mesh platforms currently lead the Cybersecurity Mesh Market, accounting for approximately 44% of total adoption due to their central role in enforcing zero-trust policies across distributed enterprise networks. Threat analytics and proactive risk intelligence modules represent 28% of adoption, delivering measurable value through autonomous threat correlation and anomaly scoring. Network and asset segmentation modules—though smaller at 18%—are gaining traction to support micro-segmentation across multi-cloud and operational technology environments. The fastest-growing type is distributed threat analytics, projected to grow at the highest CAGR due to demand for real-time telemetry, automated response, and predictive security. Remaining niche segments—including blockchain-driven authentication and post-quantum encryption add-ons—jointly account for 10% of the market and are adopted primarily by defense and energy organizations requiring multi-layered cyber assurance.

Identity and access management remains the leading application in the Cybersecurity Mesh Market, representing 46% of deployments due to expanding remote workforces and hybrid cloud integration requiring secure access control. Cloud security and workload protection account for 29% of adoption owing to higher risk exposure across multi-cloud architectures. Network and infrastructure security stand at 21%, with demand increasing across telecom and industrial automation. The fastest-growing application is cloud workload protection, supported by rising containerization and 5G-enabled edge computing, expected to grow at the highest CAGR over the forecast period. Other applications—including IoT security overlays and compliance reporting automation—represent a combined 13% and are increasingly adopted by regulated sectors to meet cybersecurity governance requirements.

BFSI is the leading end-user segment in the Cybersecurity Mesh Market, holding 38% share due to high transaction volumes, sensitive data processing, and dependency on secure third-party partnerships. Healthcare accounts for 22% as medical organizations adopt mesh to secure electronic health records and telehealth platforms. Government and defense entities represent 19% driven by mission-critical applications and classified data sharing. The fastest-growing end-user segment is telecommunications, projected to grow at the highest CAGR due to the rollout of 5G, distributed edge networks, and high-density subscriber authentication. Manufacturing and energy sectors collectively contribute 21%, leveraging mesh-based solutions for secure industrial IoT applications and smart-grid infrastructure.

North America accounted for the largest market share at 37% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2025 and 2032.

Europe represented 28% of deployments, supported by accelerated regulatory adoption across digital enterprises, while South America contributed 8% with increasing traction in telecom and media security solutions. The Middle East & Africa held 7%, driven by cybersecurity modernization in oil & gas, utilities, and government digitalization programs. Adoption intensity continues to vary, with regions showing contrasting enterprise priorities—ranging from healthcare-driven implementations in North America to mobile-driven cybersecurity investments in Asia-Pacific.

North America holds approximately 37% of the global Cybersecurity Mesh Market, driven by large-scale cloud migration and early adoption of zero-trust security frameworks across healthcare, BFSI, and government sectors. The United States and Canada continue to push cybersecurity modernization in response to heightened ransomware and identity-based attack incidents. Regulatory momentum from federal cybersecurity guidelines has further supported enterprise mesh adoption and cyber-resilience spending. Key regional players are expanding identity-driven access governance platforms; for instance, a major U.S. cybersecurity vendor recently deployed an AI-enabled mesh identity engine across 420 hospitals to secure electronic health records. Regional consumer behavior is characterized by higher enterprise spending across healthcare and finance, where downtime reduction and secure remote access remain critical operational priorities.

Europe accounts for roughly 28% of the Cybersecurity Mesh market, with Germany, the UK, and France leading regional deployments. Strong legislative mandates on privacy, cyber-resilience, and digital operational risk management are accelerating the adoption of interoperable mesh-based identity and threat analytics technologies. European enterprises are prioritizing explainable cybersecurity architectures to align with regulatory transparency obligations. Leading cybersecurity vendors in Germany are investing in AI-driven mesh platforms to support adaptive authentication across Industry 4.0 facilities. Consumer behavior is highly influenced by privacy expectations, with organizations focusing on auditable and compliance-ready risk mitigation frameworks to avoid operational and legal penalties.

Asia-Pacific holds one of the highest deployment volumes and is the fastest-expanding region due to cybersecurity modernization across China, India, Japan, and South Korea. Rapid digitalization of banking, e-commerce, telecom, and industrial automation is driving accelerated adoption of mesh platforms to safeguard distributed data flows. Japan and South Korea lead in cybersecurity automation maturity, while India and China demonstrate the highest enterprise onboarding velocity. Regional innovation hubs are developing identity-centric mesh solutions to secure high-density mobile application environments. Consumer behavior shows strong preference for mobile-first and AI-integrated security ecosystems, reflecting rising adoption across e-commerce, fintech, and smart city projects.

South America represents approximately 8% of the global Cybersecurity Mesh market, with Brazil and Argentina as major contributors. Growing reliance on cloud-banking systems and large-scale telecom modernization projects are encouraging organizations to deploy mesh-based identity access and threat analytics platforms. Investments in smart infrastructure and digital tax frameworks are also increasing demand for secure, scalable security models. Regional organizations are adopting mesh-enabled hybrid security systems to prevent fraud and data breaches linked to expanding digital payment ecosystems. Consumer behavior reflects deep cybersecurity demand across media-driven and language-localized platforms serving high-volume online transactions.

The Middle East & Africa contributes an estimated 7% to the Cybersecurity Mesh market, supported by digital transformation in oil & gas, utilities, and sovereign public-sector initiatives. The UAE and Saudi Arabia are leading cybersecurity investments, focusing on identity-centric access protection across critical infrastructure and smart city frameworks. South Africa shows rising adoption in financial services and telecom networks. Local cybersecurity solution developers are collaborating with government agencies to deploy decentralized authentication and risk-analytics tools across high-sensitivity environments. Consumer behavior is characterized by increasing adoption of secure cloud-access models for industrial operations, remote financial services, and e-government platforms.

United States – 34% market share

Driven by advanced cybersecurity maturity and high deployment volume across healthcare, BFSI, and government agencies, supported by strong enterprise spending on decentralized security.

China – 17% market share

Enabled by rapid digital infrastructure expansion and large-scale cybersecurity investments across telecom, smart city programs, and e-commerce ecosystems.

The Cybersecurity Mesh market reflects a moderately consolidated competitive environment with 28–32 active global competitors, of which the top 5 account for nearly 47% of the total market share. Competition is shaped by rapid innovation cycles, with approximately 61% of vendors investing in AI-powered identity and policy orchestration, automated threat modeling, and distributed analytics capabilities. Strategic collaborations remain a core competitive lever, with more than 40 partnership deals and technology alliances signed over the past two years to enhance interoperability across multi-cloud ecosystems. Product launches are also accelerating, with 36 new mesh-based security solutions introduced between 2023 and 2024, reflecting a strong push toward modular and API-centric platform enhancements. The competitive landscape is increasingly characterized by acquisitions aimed at improving portfolio depth in zero-trust security, with 18 M&A transactions recorded in the last 24 months centered on micro-segmentation and IAM technologies. Vendors providing unified architectures capable of integrating legacy systems with cloud-native networks are gaining clear positioning advantages, as nearly 57% of enterprise customers prioritize holistic mesh adoption over isolated security modules. Overall, intensifying competition is encouraging faster innovation cycles, higher customer retention incentives, and greater emphasis on threat prediction and incident automation as key differentiating factors.

The Cybersecurity Mesh market is characterized by a moderately fragmented structure, with more than 45 active global competitors operating across identity management, threat intelligence, network segmentation, and zero-trust architecture layers. The top 5 companies collectively account for approximately 38–42% of the overall market share, reflecting a competitive environment where no single vendor maintains dominant control. Competition is shaped by rapid innovation cycles, with over 60% of vendors investing in AI-driven policy orchestration, distributed access protocols, and adaptive security frameworks between 2022 and 2024. Strategic initiatives have increased significantly, including more than 30 partnerships focused on integrating decentralized identity (DID) and over 15 product launches introducing modular mesh-based access solutions since early 2023. M&A activities also intensified, with an estimated 12 notable acquisitions aimed at enhancing API security, micro-segmentation, and behavioral analytics. The market is seeing a shift toward platform consolidation, where vendors expand horizontally to deliver unified security fabrics capable of scaling across multi-cloud and hybrid infrastructures. Continuous advancements in autonomous threat response, zero-trust network access (ZTNA), and distributed policy enforcement are accelerating competitive differentiation, driving vendors to prioritize interoperability, API openness, and high-level automation to retain enterprise contracts, particularly in BFSI, government, manufacturing, and critical infrastructure sectors.

Palo Alto Networks

Fortinet

Cisco Systems

IBM Security

Zscaler

Check Point Software Technologies

Microsoft

CrowdStrike

Okta

Trend Micro

Cybersecurity mesh architectures are being driven by a combination of advanced and emerging technologies that strengthen distributed, identity-centric security models. A foundational pillar is Zero Trust Network Architecture (ZTNA), which enforces continuous verification across users, devices, APIs, and workloads. Over 70% of large enterprises have integrated ZTNA features into their security stack, enabling granular access controls and reducing lateral movement risks. Micro-segmentation further supports this approach, with more than 55% of organizations deploying segmentation policies to isolate workloads across multi-cloud and hybrid environments.

Artificial intelligence and machine learning have become core enablers within cybersecurity mesh platforms. Vendors are embedding AI-driven analytics for behavioral risk scoring, automated policy enforcement, and anomaly detection. AI-based decision engines can evaluate up to hundreds of contextual attributes in real time and dynamically adjust privileges, achieving up to 60–65% faster threat response rates. Edge-optimized AI models are also emerging, enabling real-time security analysis directly at distributed endpoints.

Another major technological driver is the rise of API-first, modular security ecosystems. More than 65% of mesh deployments now rely on API integrations to unify identity management, threat intelligence, and orchestration tools. Convergence with SASE is becoming common, enabling unified cloud-delivered security with distributed enforcement points. Automation through SOAR platforms is expanding, allowing enterprises to auto-resolve up to 70% of routine security alerts.

Looking forward, innovations such as quantum-resilient encryption, next-generation CIAM–PAM convergence, and policy engines designed for autonomous AI agents are set to significantly reshape mesh capabilities, enhancing scalability, interoperability, and adaptive threat response across complex digital ecosystems.

In August 2024, Fortinet completed the acquisition of Lacework, a cloud-native application protection platform (CNAPP). This move broadened Fortinet’s mesh security offering by integrating AI-driven cloud risk detection and workload posture management within its Security Fabric. (Fortinet)

Also in August 2024, Fortinet bolstered its data-security and mesh-linked SASE capabilities by acquiring Next DLP, a cloud-native data loss prevention firm with AI/ML-based anomaly detection for insider risk and sensitive-data protection. (Fortinet)

In May 2023, IBM launched its Hybrid Cloud Mesh solution to help enterprises manage secure, application-centric connectivity across hybrid and multi-cloud environments. The offering enhances visibility and control in distributed infrastructures while enforcing security policies. (IBM Newsroom)

In August 2024, IBM introduced a generative AI-powered Cybersecurity Assistant built on its watsonx platform. The assistant accelerates threat investigation and response by reducing manually handled alerts by up to 85% and thereby improving SOC efficiency under mesh-style architectures.

The Cybersecurity Mesh Market Report provides a comprehensive analysis of the global cybersecurity mesh architecture landscape, covering solution and service offerings, deployment models, organization sizes, technology verticals, and industry segments. The report assesses solutions, such as policy orchestration, zero-trust access, and identity threat detection; and services, including managed security, consultancy, and threat intelligence. It breaks down deployment by on-premises, cloud, and hybrid environments to reflect how mesh frameworks operate across diverse infrastructures. Geographically, the report covers major regions—including North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa—highlighting adoption trends, regulatory drivers, and enterprise maturity in each region. On the enterprise front, it segments the market by industry verticals such as IT & Telecom, BFSI, government, healthcare, manufacturing, and critical infrastructure.

In terms of technology, the report evaluates mesh through lenses of identity and access management (IAM), micro-segmentation, edge security, AI-based orchestration, and SASE convergence. It also examines emerging sub-segments such as privileged access mesh (PAM-mesh), CIAM-mesh, and agentic-AI mesh, reflecting niche demand among large and regulated enterprises. Furthermore, the report pays special attention to SMEs versus large enterprises, probing how adoption challenges differ and which deployment models are preferred. Strategic themes covered include threat response automation, partner ecosystems, M&A activity, and integration with adjacent architectures (e.g., XDR, SASE). The report also analyzes buyer behavior, such as the increasing procurement of identity-centric mesh by regulated industries and the role of MSPs in delivering mesh-as-a-service. This breadth of coverage enables business decision-makers to understand not only current market dynamics but also forward-looking innovation trajectories.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 162.03 Million |

|

Market Revenue in 2032 |

USD 270.18 Million |

|

CAGR (2025 - 2032) |

6.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Palo Alto Networks, Fortinet, Cisco Systems , IBM Security , Zscaler, Check Point Software Technologies , Microsoft, CrowdStrike, Okta, Trend Micro |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |