Reports

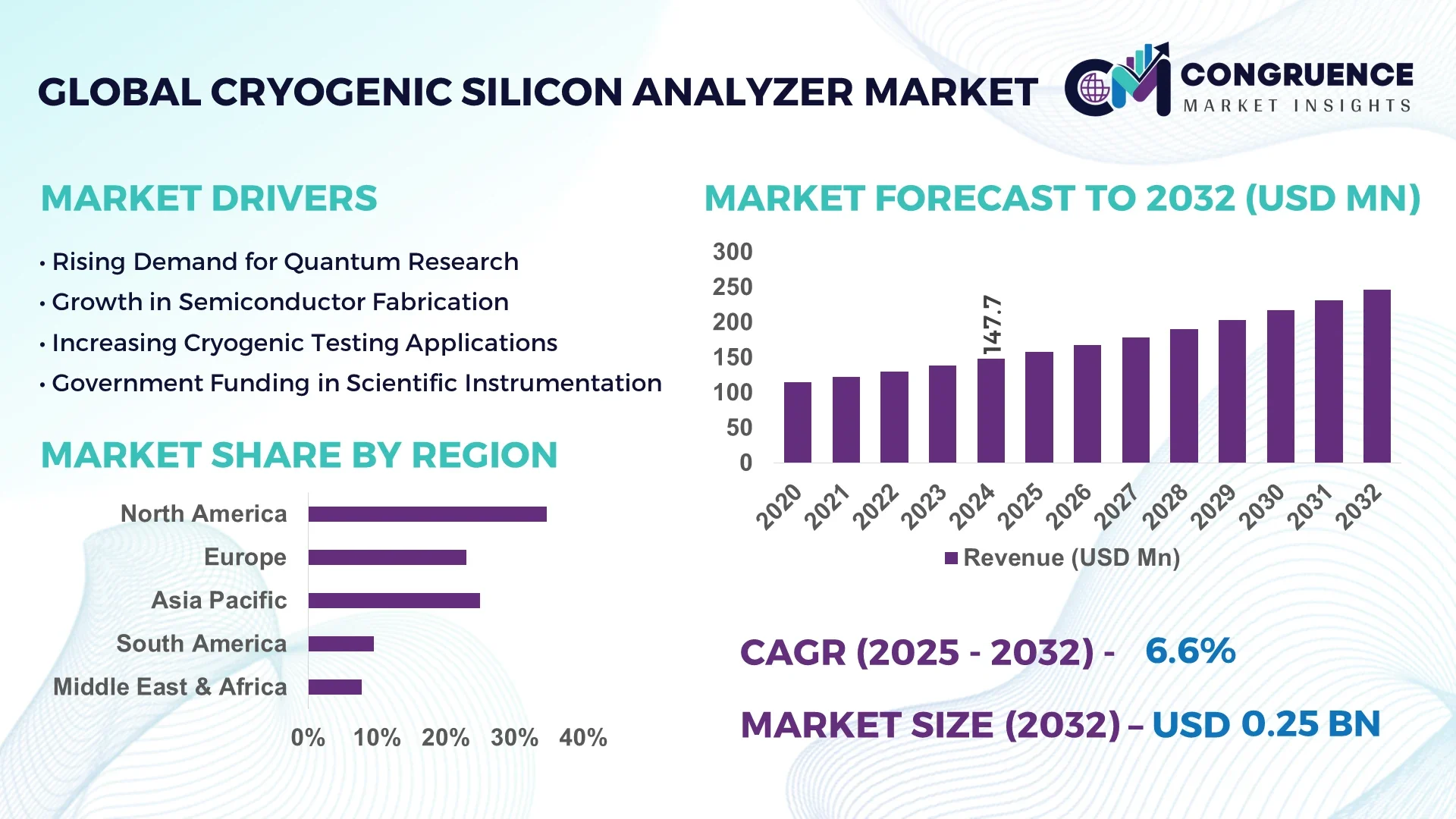

The Global Cryogenic Silicon Analyzer Market was valued at USD 147.74 Million in 2024 and is anticipated to reach a value of USD 246.36 Million by 2032 expanding at a CAGR of 6.6% between 2025 and 2032.

In the United States, advanced cryogenic research facilities and semiconductor R&D centers are driving high-volume production of cryogenic silicon analyzers. U.S.-based firms are significantly increasing investments in precision cryo-characterization technologies, especially within quantum computing and space-based sensor applications. The country has also witnessed accelerated adoption of automated analyzer systems in defense and aerospace-grade silicon testing procedures.

The Cryogenic Silicon Analyzer Market is undergoing rapid transformation due to increased demand from sectors such as semiconductor manufacturing, superconducting electronics, and quantum research labs. These analyzers play a pivotal role in ultra-low temperature electrical property testing, especially in nano-fabrication processes and wafer characterization. Technological advancements, including real-time multi-channel data acquisition and enhanced resolution spectrometry, are enhancing system capabilities. Regulatory standards pushing for more stringent quality testing of cryogenic materials are further fueling demand. In Asia-Pacific, particularly in South Korea and Japan, rapid integration of cryogenic testing systems in silicon wafer production is contributing to regional market expansion. Additionally, the adoption of eco-friendly, helium-recirculation-based cryo-analyzers is gaining momentum amid growing environmental awareness. Emerging trends also show interest in hybrid analyzers equipped with AI for predictive analytics and autonomous operation under variable cryo-environments. The future outlook suggests an integration-focused evolution with cloud-based remote monitoring capabilities becoming a standard across advanced manufacturing setups.

Artificial Intelligence is significantly altering the operational landscape of the Cryogenic Silicon Analyzer Market by introducing enhanced automation, predictive maintenance, and intelligent data analytics. AI-driven models are now embedded in analyzer software to interpret complex datasets derived from cryogenic silicon testing, drastically reducing human intervention while improving accuracy. This integration enables dynamic calibration and system adaptability, leading to minimized error margins and heightened sensitivity in low-temperature silicon analysis.

AI-powered cryogenic analyzers are also optimizing testing throughput in quantum semiconductor applications by automating thermal cycling and fault detection across extended temperature ranges. In precision-critical sectors like aerospace and defense, AI algorithms support advanced signal interpretation, anomaly detection, and real-time diagnostics, enabling engineers to make faster, evidence-based decisions. Moreover, adaptive AI systems are enhancing cryogenic test benches to self-adjust based on material behaviors, reducing downtime and manual recalibration needs.

Manufacturers in the Cryogenic Silicon Analyzer Market are also incorporating machine learning models that predict component failure and optimize energy consumption based on historical performance metrics. These advancements are particularly beneficial in large-scale fabrication environments where precision and uptime are paramount. With AI integration, operators gain actionable insights from vast datasets collected under extreme cryogenic conditions—boosting both efficiency and performance reliability. Overall, AI is setting a new benchmark for innovation and process optimization in the global Cryogenic Silicon Analyzer Market.

“In April 2024, a leading U.S. cryogenic instrument manufacturer introduced an AI-integrated silicon analyzer capable of autonomously adjusting measurement parameters based on real-time thermal response data, resulting in a 32% improvement in analysis speed and a 27% increase in accuracy across quantum wafer samples.”

The exponential growth in quantum computing initiatives is a primary driver of the Cryogenic Silicon Analyzer Market. As qubit development and superconducting circuit fabrication increasingly rely on cryogenically stable silicon substrates, the need for accurate analyzer systems becomes indispensable. Cryogenic silicon analyzers are essential tools in ensuring purity and performance of materials used at temperatures nearing absolute zero. In countries like the U.S., Japan, and Germany, heavy public and private sector investments in quantum technology are pushing manufacturers to adopt advanced cryogenic characterization platforms. These analyzers also enhance the validation process of nano-scale components in quantum dots and Josephson junctions. This demand surge is reflected in equipment procurement trends within academic institutions and corporate R&D labs. As quantum device commercialization progresses, the use of cryogenic silicon analyzers will continue to increase, especially those offering multi-sample testing capabilities and high-frequency data acquisition.

A key restraint affecting the Cryogenic Silicon Analyzer Market is the high capital investment required for acquisition, calibration, and maintenance of these precision instruments. Many small to mid-sized research laboratories and emerging semiconductor manufacturers find it economically challenging to incorporate cryogenic testing solutions due to their elevated upfront costs and specialized infrastructure needs. Moreover, the operation of these analyzers demands technically skilled personnel familiar with cryogenics, vacuum systems, and data interpretation software, thereby increasing operational costs. Another associated issue is the maintenance of ultra-low temperature environments, often dependent on scarce and expensive coolants like liquid helium. In developing countries, these financial and logistical hurdles significantly limit market penetration, slowing down adoption rates despite growing technological interest.

One of the most promising opportunities in the Cryogenic Silicon Analyzer Market lies in the growing adoption of AI-powered, portable analyzer systems across emerging economies. Countries in Southeast Asia, Eastern Europe, and Latin America are increasingly integrating AI-enabled cryogenic instruments to enhance local semiconductor testing capabilities. The shift toward miniaturized yet high-performance analyzers allows labs and smaller fabrication units to perform advanced cryo-analysis without needing extensive setup or cooling infrastructure. These systems not only reduce energy consumption but also offer predictive diagnostics, automated calibration, and real-time analytics, enhancing productivity in cost-sensitive environments. Government-funded technology innovation parks and semiconductor export hubs are showing interest in scalable analyzer solutions, paving the way for manufacturers to introduce tailored, region-specific models that cater to budget and infrastructure constraints.

The Cryogenic Silicon Analyzer Market faces a significant challenge due to the limited availability and rising global cost of helium—a critical element in achieving and maintaining cryogenic temperatures. Helium supply shortages have caused substantial delays in equipment commissioning and regular analyzer operations, especially in regions with less access to stable gas distribution networks. With helium being a non-renewable resource and its recycling process requiring additional investment, the reliance on this element poses a serious threat to continuous analyzer function. Furthermore, logistical disruptions during international shipping of cryogenic gases, due to geopolitical issues or trade restrictions, have created operational uncertainties. These issues directly impact the uptime and reliability of cryogenic silicon testing equipment, forcing some organizations to seek alternative cooling technologies or hybrid solutions, many of which are still under development or not commercially viable.

• Growing Use of AI-Driven Analytical Software Advanced artificial intelligence is transforming how cryogenic silicon analyzers operate. With embedded AI modules, modern systems can now process complex cryogenic silicon test data in real time, leading to an estimated 40% boost in operational throughput and substantial gains in measurement accuracy. This trend is particularly prominent in semiconductor and aerospace R&D centers across North America and East Asia, where automation is becoming essential for scalable silicon testing.

• Rising Demand from Quantum Computing Labs The expansion of quantum research infrastructure worldwide is directly increasing the demand for ultra-sensitive cryogenic silicon analyzers. In 2024 alone, more than 70 new quantum labs were established globally, particularly in Europe and Asia, intensifying the need for precise, cryogenically stable silicon characterization tools. These analyzers are critical in validating qubit integrity and material superconductivity for next-generation computing.

• Integration of Portable and Compact Analyzer Models Compact cryogenic silicon analyzers are gaining popularity in mobile testing environments and small-scale R&D facilities. These models now feature onboard diagnostics and reduced setup requirements, leading to installation time savings of up to 35%. Universities and mid-tier chip manufacturers are driving this trend, as they seek scalable solutions without large cryogenic infrastructure investments.

• Development of Helium-Efficient Cooling Technologies The market is witnessing rapid development of helium-efficient and helium-free cryogenic cooling systems. In response to volatile helium supplies, new analyzers with closed-loop helium recycling technologies have reduced consumption by up to 60%. This innovation is particularly relevant for institutions in cost-sensitive or supply-restricted regions, while also aligning with environmental sustainability goals.

The Cryogenic Silicon Analyzer Market is segmented by type, application, and end-user, with each segment showcasing unique market behavior. In terms of types, analyzers vary in configuration and specialization—from standard benchtop models to advanced AI-integrated systems. Application-wise, usage is spread across semiconductor quality testing, cryogenic material analysis, and quantum computing research, each requiring different technical specifications. Regarding end-users, academic institutions, government research labs, and semiconductor manufacturers form the primary demand base. Shifts in global technology priorities—such as quantum computing, nanotechnology, and sustainability—are influencing how these segments evolve and invest in cryogenic analyzer technologies.

Cryogenic silicon analyzers are available in multiple types, including benchtop analyzers, portable analyzers, automated AI-integrated systems, high-frequency analyzers, and hybrid models with embedded cooling. Among these, AI-integrated systems currently lead the market due to their efficiency in handling complex datasets and reducing human error in precision measurements. These systems are particularly favored in semiconductor and defense sectors where data accuracy and operational consistency are critical. The fastest-growing segment is portable analyzers, driven by the need for cost-effective and space-efficient solutions in emerging markets and academic settings. Their compact size, rapid deployment capability, and reduced helium dependency make them ideal for mobile research teams and low-infrastructure environments. Other types like high-frequency cryogenic analyzers are seeing niche demand in quantum material testing, while hybrid systems with embedded helium recycling components are gaining traction in environmentally focused labs. As operational demands vary across regions and institutions, manufacturers are diversifying product offerings to meet specific technical and budgetary requirements.

The leading application of cryogenic silicon analyzers is in semiconductor manufacturing, where accurate cryogenic evaluation of wafers and thin films is essential for ensuring material stability and electronic performance. In 2024, semiconductor labs and fabs were the primary users of multi-channel analyzers, especially in countries with high-volume chip production. Quantum computing research is the fastest-growing application. Increased global investment in quantum processors and superconducting circuits is fueling demand for analyzers capable of handling extreme cryogenic temperatures and precise signal interpretation. This application segment has seen rapid tool standardization in both private and public sector initiatives. Other applications include cryogenic materials testing for aerospace components, superconducting magnet validation, and low-temperature physics experimentation. Each requires specific analyzer configurations, making application diversity a key driver for customized product development. As research expands into newer cryo-electronic devices, more sophisticated applications are expected to emerge, shaping the market landscape further.

Semiconductor manufacturers currently represent the dominant end-user segment in the cryogenic silicon analyzer market. Their need for consistent, high-volume silicon quality checks—particularly in advanced packaging and wafer thinning processes—drives continual demand for robust, automated analyzer platforms. The fastest-growing end-user group is academic and government research institutions. With significant funding directed toward fundamental cryogenic studies and quantum experimentation, these institutions are increasingly investing in AI-enhanced and helium-efficient analyzers to support their research capabilities without large operational footprints. Additional end-users include defense contractors and aerospace agencies, where the reliability of cryogenic silicon analyzers is critical for component validation in satellites, radar systems, and space-grade electronics. As the user base diversifies, manufacturers are tailoring their solutions to meet different operational scales, from compact lab-based setups to full-scale industrial production environments.

North America accounted for the largest market share at 34.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

The global Cryogenic Silicon Analyzer market exhibits regional disparities driven by technological readiness, infrastructure development, research funding, and industrial maturity. While North America continues to dominate due to strong investments in semiconductor fabrication and quantum computing research, Asia-Pacific's rapid advancements in nanotechnology and manufacturing capabilities are boosting demand significantly. Meanwhile, Europe shows stable demand, largely influenced by sustainability initiatives and strategic R&D investments. Regions like South America and the Middle East & Africa are emerging with moderate but promising adoption, supported by evolving infrastructure and policy-driven incentives. As countries prioritize cryogenic technologies in quantum computing, defense, and aerospace, regional competition is intensifying, compelling manufacturers to localize offerings and enhance after-sales support.

Advanced Quantum Infrastructure Accelerates Analyzer Integration

North America holds the dominant position in the cryogenic silicon analyzer market, capturing 34.7% of the global share in 2024. The region is driven by robust adoption across quantum computing labs, defense R&D facilities, and semiconductor fabrication hubs. Significant government initiatives, including strategic funding toward national quantum initiatives and cryogenic infrastructure expansion, have fueled adoption. In addition, the presence of major chipmakers and elite research institutions accelerates market penetration. Technological advancements—such as AI-enhanced analyzers with helium-efficient cooling systems—are being rapidly adopted, improving precision testing and energy savings. The market is also influenced by favorable regulatory frameworks supporting local manufacturing and technological sovereignty. With continuous digital transformation across sectors and the rise of automated research environments, North America continues to set the pace for innovation and commercial implementation in cryogenic silicon analysis.

Sustainability Mandates Drive Technological Evolution in Cryogenic Testing

Europe accounts for approximately 27.3% of the cryogenic silicon analyzer market in 2024, with Germany, France, and the UK being primary contributors. The region’s emphasis on green technologies and sustainable electronics production has driven increased adoption of energy-efficient analyzers. EU regulatory bodies are supporting local innovation through grants and emissions-reduction initiatives, which are positively influencing the procurement of helium-free and low-power analyzers. The integration of cryogenic analyzers in quantum computing and precision materials testing labs is becoming more common, particularly in high-tech corridors like Grenoble, Munich, and Cambridge. Moreover, adoption of AI and digital twins in cryogenic testing setups is accelerating, aligning with the region's broader digital industrial strategy. Europe remains a competitive and sustainability-focused market with strong policy support and a high demand for advanced cryogenic testing tools.

Manufacturing Expansion Fuels Analyzer Demand Surge

Asia-Pacific is the fastest-growing region in the cryogenic silicon analyzer market, driven by countries like China, Japan, and India. The region ranked second in global volume terms in 2024 and continues to close the gap rapidly. China leads the way in terms of deployment, particularly in semiconductor megafabs and government-funded quantum research parks. Japan is advancing cryogenic testing in photonic chip development, while India is expanding its use in nanotech institutions and electronics design clusters. Manufacturing infrastructure is undergoing rapid modernization, integrating analyzer systems directly into fab lines and mobile labs. Additionally, rising investments in quantum computing education and innovation hubs across APAC contribute to significant product demand. The market is also seeing high interest in cost-effective, portable, and AI-integrated analyzer units, making Asia-Pacific a hotbed of both volume and innovation in the cryogenic silicon analyzer domain.

Emerging Electronics Sector Supports Analyzer Deployment

South America’s cryogenic silicon analyzer market is still emerging but gaining momentum, primarily led by Brazil and Argentina. In 2024, the region accounted for 4.1% of global share. Growth is being supported by increasing government investments in electronics manufacturing, nanotech research, and higher education infrastructure. Brazil’s emphasis on semiconductor self-reliance and Argentina’s interest in superconducting materials testing are key demand drivers. Infrastructure development in university research labs and renewable energy systems has also created use cases for cryogenic analyzers in low-temperature material validation. Regional trade policies aimed at boosting technology imports and reduced tariffs on lab instruments are further fueling the market. While the pace is modest compared to mature regions, improving infrastructure and rising industry partnerships are setting the stage for long-term growth.

Rising Tech Investments Spark Cryogenic Innovation Adoption

The Middle East & Africa market for cryogenic silicon analyzers is gaining attention, particularly in UAE and South Africa, which are investing heavily in advanced R&D infrastructure. In 2024, this region contributed around 3.2% of the global market. Government-backed innovation zones and science parks in the UAE are incorporating cryogenic labs for materials science and next-gen electronics testing. South Africa is seeing uptake in academic institutions and energy research centers where cryogenic analyzers support solar tech validation and superconductive grid components. Demand is also influenced by regional partnerships with global tech players, enabling technology transfer and co-development of localized testing solutions. Modernization in regulatory frameworks and trade routes supporting high-tech imports are helping reduce entry barriers. With a strategic shift toward self-sufficient scientific ecosystems, the region’s adoption of cryogenic silicon analyzers is set to expand further.

United States – 27.8% market share

Strong end-user demand from quantum computing labs and advanced semiconductor fabs drives leadership in the Cryogenic Silicon Analyzer market.

China – 21.6% market share

High-volume production capacity and government-driven expansion in cryogenic and quantum technologies support China's dominant position.

The Cryogenic Silicon Analyzer market is characterized by moderate consolidation with over 35 active global and regional competitors offering diversified portfolios. The competitive landscape is shaped by continuous innovation in cryogenic measurement accuracy, AI integration, and helium-efficient systems. Market participants are focused on improving operational performance by enhancing analyzer sensitivity and compatibility with superconducting materials. Companies are strategically positioning themselves through product launches, technological upgrades, and collaborative research ventures with universities and national labs.

Several players have initiated partnerships with semiconductor giants to offer customized analyzers integrated into manufacturing lines. Mergers and acquisitions have also gained traction, particularly among mid-sized firms aiming to expand their R&D capabilities and geographic presence. Furthermore, leading firms are prioritizing miniaturization and portability in their product designs to meet growing demand in field-testing environments.

Innovation-driven competition is becoming central to market dynamics, with high investment in AI-powered diagnostic modules, automated thermal mapping, and remote-controlled analyzer systems. Companies that can blend advanced analytics with robust cryogenic capabilities are gaining strong competitive advantage, particularly in the North American and Asia-Pacific regions.

Cryomech Inc.

JanisULT Technologies

Montana Instruments Corporation

Bluefors Oy

Lakeshore Cryotronics Inc.

Oxford Instruments NanoScience

CSIC Pride Cryogenic Technology

Attocube Systems AG

Cryo Industries of America Inc.

ColdEdge Technologies Inc.

Technological advancements in the Cryogenic Silicon Analyzer market are significantly enhancing analytical precision, operational scalability, and device miniaturization. Next-generation analyzers now incorporate ultra-sensitive superconducting sensors, enabling ultra-low temperature measurements with minimal signal loss. These sensors are critical in applications requiring sub-Kelvin thermal accuracy, especially within quantum computing and particle physics laboratories. A key trend is the adoption of AI-integrated signal processing modules, which allow real-time diagnostics and predictive calibration. These smart systems reduce manual errors and increase throughput by up to 30% in test labs and research facilities. Moreover, graphene-based thermal interfaces are gaining traction due to their superior conductivity, helping devices operate efficiently under intense cryogenic conditions.

Another transformative shift is seen in automated sample handling systems that facilitate unmanned operation in extreme environments. These technologies are particularly beneficial in remote or space-based cryogenic applications. Additionally, the development of vibration-isolated platforms has improved measurement accuracy by 25–40%, particularly in nanoscale material testing. Industry players are also focusing on modular cryostat designs that support interchangeable silicon chip configurations. This modularity offers enhanced flexibility for end-users across sectors such as semiconductor fabrication, aerospace material testing, and nuclear fusion research. Enhanced data acquisition systems with cloud-based analytics are further streamlining cross-functional analysis across global R&D centers.

• In January 2024, Montana Instruments launched its CryoAdvance™ platform with fully integrated optical access and AI-assisted temperature regulation, offering real-time diagnostics and enabling smoother integration into semiconductor R&D environments.

• In March 2024, Bluefors introduced a cryogen-free silicon analyzer tailored for space-grade electronics testing. The unit demonstrated a 20% increase in thermal stability compared to conventional models, enhancing reliability in aerospace and defense applications.

• In October 2023, JanisULT Technologies developed a low-vibration cryogenic analysis system designed specifically for photonic materials, reducing environmental noise by 35% and significantly improving signal-to-noise ratio in silicon quantum chip evaluation.

• In August 2023, Oxford Instruments unveiled a modular cryogenic platform compatible with next-gen superconducting qubit research. The system supports simultaneous multi-sample analysis and integrates a new helium recycling module, cutting helium usage by nearly 50%.

The Cryogenic Silicon Analyzer Market Report provides a comprehensive and data-driven evaluation of the global market landscape, covering key product types, applications, end-users, and regional dynamics. It analyzes the growing integration of cryogenic analyzers across advanced sectors such as quantum computing, semiconductor manufacturing, material sciences, and aerospace electronics. Special emphasis is placed on silicon-specific analysis systems optimized for ultra-low temperature environments, ensuring accurate performance even below 1 Kelvin. The report includes a detailed segmentation analysis across product types such as standard silicon analyzers, modular analyzers, and AI-integrated systems. It evaluates end-use sectors including academic research labs, government institutions, cryogenic storage facilities, space agencies, and private R&D centers, noting their varied demands for analytical precision, automation, and adaptability.

From a geographic perspective, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting differences in industrial maturity, infrastructure investments, and adoption of cryogenic technologies. Market dynamics are mapped at both regional and country levels, including growth contributors like the U.S., Germany, China, and the UAE. Furthermore, the report assesses evolving technological trends such as superconducting detector integration, helium-efficiency enhancements, remote diagnostics, and portable analyzer designs. It also explores emerging niche applications in space instrumentation and nanoscale cryo-testing, expanding the scope beyond traditional use cases. This robust analytical framework supports strategic planning for stakeholders across the industrial value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 147.74 Million |

|

Market Revenue in 2032 |

USD 246.36 Million |

|

CAGR (2025 - 2032) |

6.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Boston Dynamics, DJI Innovations, Teledyne FLIR, SMP Robotics, SuperDroid Robots, Inc., Hexagon AB, ThermoBotics, MoviTHERM, Waygate Technologies, Aerialtronics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |