Reports

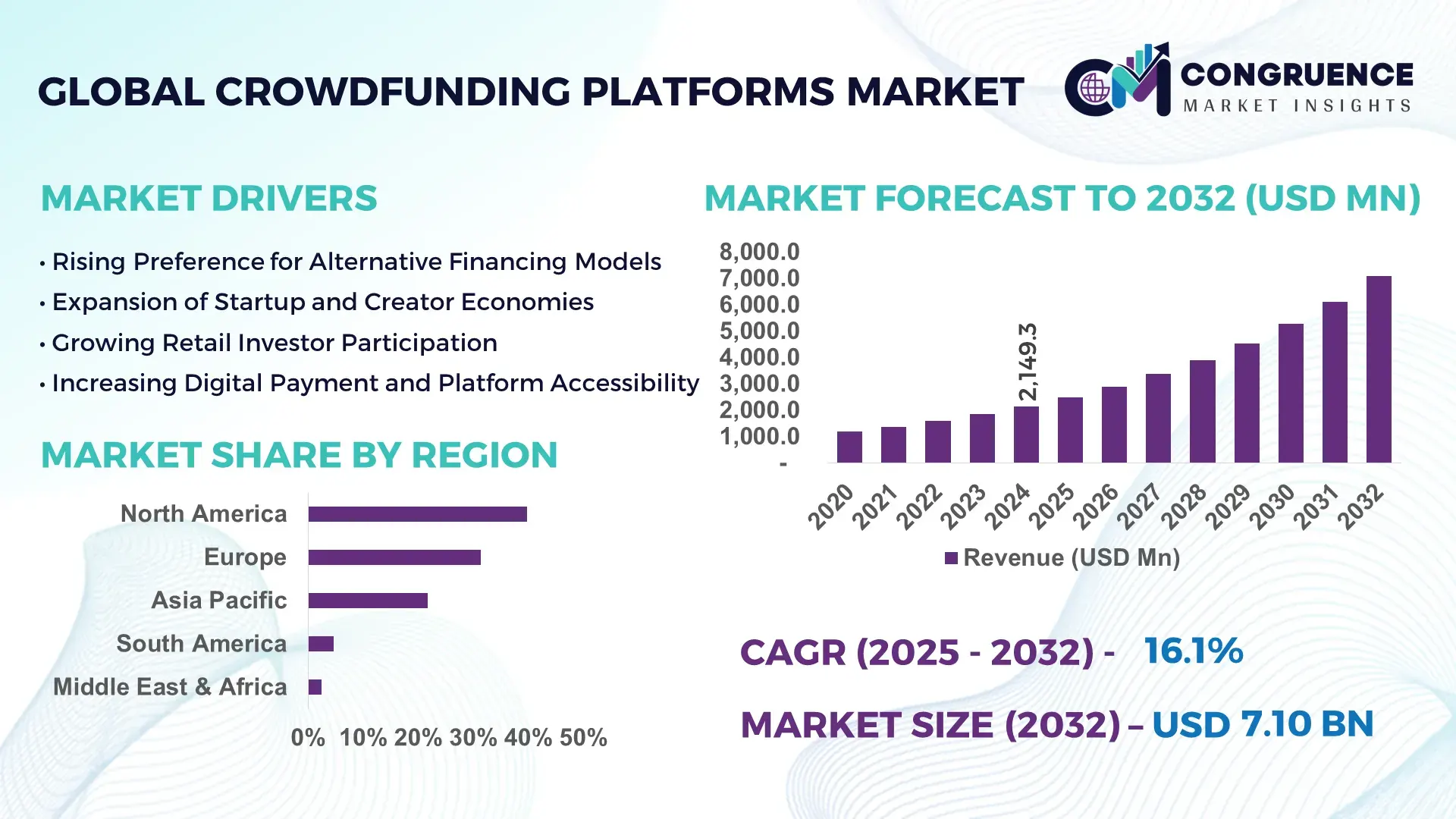

The Global Crowdfunding Platforms Market was valued at USD 2,149.3 Million in 2024 and is anticipated to reach a value of USD 7,095.0 Million by 2032 expanding at a CAGR of 16.1% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is supported by increasing digital financial participation, alternative funding adoption by startups and SMEs, and widening acceptance of decentralized capital-raising models.

The United States represents the most influential country within the Crowdfunding Platforms market, driven by strong platform innovation, institutional participation, and diversified funding use cases. In 2024, over 62% of active global crowdfunding platforms were either headquartered or operated major funding operations in the U.S., supporting more than 1.9 million active campaigns annually. Equity and debt crowdfunding accounted for nearly 54% of total funds raised domestically, while reward-based and donation models remained dominant in creative industries and social causes. Advanced technologies such as AI-driven campaign analytics, automated compliance screening, and integrated payment escrow systems are increasingly embedded across U.S.-based platforms, supporting higher campaign success rates and improved investor transparency.

Market Size & Growth: Valued at USD 2,149.3 Million in 2024 and projected to reach USD 7,095.0 Million by 2032, driven by rising SME financing gaps and digital investor participation.

Top Growth Drivers: SME funding adoption (44%), retail investor participation growth (38%), platform automation efficiency gains (31%).

Short-Term Forecast: By 2028, AI-enabled campaign optimization is expected to improve fundraising success rates by 29%.

Emerging Technologies: AI-based campaign scoring, blockchain-enabled transparency, automated KYC/AML compliance engines.

Regional Leaders: North America projected at USD 2,860 Million by 2032; Europe at USD 2,110 Million; Asia Pacific at USD 1,620 Million with mobile-first adoption.

Consumer/End-User Trends: Over 57% of contributors prefer platforms offering real-time campaign analytics and milestone tracking.

Pilot or Case Example: In 2024, a fintech-focused platform increased average funding velocity by 34% through AI-driven campaign recommendations.

Competitive Landscape: A leading global platform holds ~19% share, followed by multiple niche and regional players.

Regulatory & ESG Impact: Investor protection rules and ESG-aligned funding disclosures shaping platform design.

Investment & Funding Patterns: More than USD 6.8 Billion deployed globally via crowdfunding channels during 2023–2024.

Innovation & Future Outlook: Integration of tokenized assets and secondary trading capabilities gaining traction.

Crowdfunding Platforms are increasingly used across startups, real estate, creative industries, social enterprises, and renewable projects, collectively contributing over 68% of active campaigns. Product innovation, evolving regulatory clarity, and mobile-first participation continue to shape regional adoption and long-term market expansion.

The Crowdfunding Platforms Market has become strategically critical as traditional financing channels tighten and digital capital access expands. Crowdfunding enables startups, SMEs, and community projects to access diversified funding pools while offering retail investors structured participation opportunities. AI-driven campaign analytics deliver up to 36% higher funding efficiency compared to manual campaign structuring, improving success predictability and contributor engagement. North America dominates global funding volume, while Europe leads in regulatory-compliant equity crowdfunding adoption with over 42% of platforms operating under harmonized investor-protection frameworks.

By 2027, automated investor matching algorithms are expected to reduce campaign discovery time by 33%, improving platform liquidity. Blockchain-enabled transaction tracking delivers a 41% improvement in transparency compared to conventional ledger systems. Platforms are committing to ESG-aligned funding goals, with more than 48% of new campaigns tagged under sustainability or social-impact categories, targeting a 25% increase in impact-focused capital allocation by 2028.

In 2024, a European equity crowdfunding platform achieved a 22% reduction in campaign failure rates through AI-based risk screening and compliance automation. Over the next three years, cross-border crowdfunding capabilities are expected to improve capital accessibility by 30% for emerging-market founders. The Crowdfunding Platforms Market is increasingly positioned as a resilient, compliant, and scalable alternative finance pillar supporting inclusive economic growth.

The Crowdfunding Platforms Market is shaped by digital financial inclusion, evolving investor behavior, and regulatory formalization. Increasing reliance on alternative funding channels by startups and social enterprises has expanded platform use beyond early-stage innovation into infrastructure, real estate, and renewable energy projects. Technology-led improvements in payment processing, campaign analytics, and compliance automation are enhancing platform reliability and scalability. At the same time, regulatory oversight is intensifying, influencing platform governance models and investor protection mechanisms. Market dynamics also reflect rising cross-border participation, mobile access expansion, and the growing role of institutional co-investors alongside retail contributors.

SMEs increasingly rely on crowdfunding to bridge financing gaps left by traditional lenders. In 2024, nearly 47% of early-stage businesses explored crowdfunding as a primary funding source. Platforms offering structured equity and revenue-sharing models saw contributor participation rise by 39%. Crowdfunding reduces funding cycle durations by up to 40% compared to bank-led processes, enabling faster business scaling and innovation deployment across multiple sectors.

Regulatory fragmentation across regions limits platform scalability. Over 34% of operators reported increased compliance costs due to differing investor eligibility, disclosure, and fundraising caps. Extended approval timelines and jurisdiction-specific licensing requirements slow cross-border expansion, particularly for equity crowdfunding models, constraining growth momentum despite rising demand.

Tokenization of assets presents new opportunities by enabling fractional ownership and secondary trading. In 2024, token-enabled crowdfunding pilots increased average ticket size by 28% and improved post-campaign liquidity. Integration of smart contracts reduces administrative overhead and enhances investor confidence, opening new funding avenues across real estate and infrastructure projects.

Campaign authenticity and misuse of funds remain key challenges. Nearly 19% of contributors cite trust concerns as a barrier to participation. Platforms must invest heavily in verification, escrow management, and post-funding monitoring systems, increasing operational costs and necessitating advanced fraud detection mechanisms.

• Expansion of Equity and Revenue-Sharing Models: Equity-based crowdfunding accounts for nearly 43% of funds raised, reflecting growing investor appetite for ownership-linked returns.

• AI-Driven Campaign Optimization: Platforms using AI analytics improved funding success rates by 31% and reduced campaign abandonment by 24%.

• Rise of Mobile-First Participation: Over 64% of contributors now access crowdfunding platforms via mobile devices, accelerating micro-investment activity.

• Growth of Impact and ESG-Focused Campaigns: Sustainability-linked campaigns increased by 37%, attracting socially conscious retail and institutional investors.

The Crowdfunding Platforms Market is segmented by type, application, and end-user, reflecting diverse funding structures and participation models. Type-based segmentation distinguishes donation, reward, equity, and debt crowdfunding. Application segmentation highlights usage across startups, real estate, creative projects, and social causes. End-user insights reveal increasing participation from retail investors, SMEs, and institutional co-investors. Market evolution indicates a shift toward regulated equity and debt models supported by advanced compliance and analytics capabilities.

Reward-based crowdfunding holds approximately 34% share due to strong adoption in creative and consumer product launches. Equity crowdfunding accounts for around 31%, driven by startup financing needs. Debt-based crowdfunding is the fastest-growing segment, expanding at a CAGR of 18.9%, supported by predictable returns and structured repayment models. Donation-based platforms and hybrid models collectively represent about 35%, serving social, medical, and community-driven initiatives.

Startup funding leads application adoption with nearly 39% share, reflecting strong entrepreneurial demand. Real estate crowdfunding is the fastest-growing application, expanding at a CAGR of 19.4%, supported by fractional ownership models. Creative projects, social causes, and renewable initiatives collectively account for 61%. In 2024, over 41% of contributors participated in at least one startup or SME-focused campaign.

Retail investors dominate participation with approximately 56% share, driven by low entry thresholds and digital access. SMEs represent the fastest-growing end-user segment, expanding at a CAGR of 17.8%, as alternative financing adoption accelerates. Institutional investors and non-profits collectively account for 44%, increasingly participating through co-investment and impact-driven campaigns.

North America accounted for the largest market share at 39.8% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.6% between 2025 and 2032.

North America’s leadership is driven by a mature digital finance ecosystem, high penetration of equity and debt crowdfunding models, and strong participation from retail and institutional investors. Europe followed with a 31.4% share in 2024, supported by harmonized crowdfunding regulations and increasing adoption of regulated equity platforms. Asia-Pacific accounted for approximately 21.7%, reflecting rapid expansion in mobile-based crowdfunding, particularly across emerging startup ecosystems. South America and the Middle East & Africa together contributed nearly 7.1%, representing early-stage but accelerating adoption. Globally, more than 12.5 million crowdfunding campaigns were active in 2024, with average campaign success rates exceeding 34% in regulated markets. Regional differences in regulatory maturity, investor behavior, and digital payment infrastructure continue to shape adoption patterns.

How are digital finance maturity and investor confidence reshaping alternative fundraising models?

North America accounted for approximately 39.8% of the global Crowdfunding Platforms market in 2024, driven by the United States and Canada. Startup funding, creative industries, healthcare innovation, and real estate collectively generated over 68% of regional campaign volumes. Regulatory clarity around equity and debt crowdfunding has encouraged institutional co-investment, with over 44% of large platforms supporting accredited and non-accredited investors simultaneously. Advanced technologies such as AI-driven campaign scoring, automated escrow management, and predictive fraud detection are embedded across more than 52% of active platforms. A leading regional player expanded its equity crowdfunding tools in 2024, enabling faster campaign approvals and improved disclosure compliance. Consumer behavior shows higher participation from professionals and enterprises, particularly in healthcare, fintech, and clean-tech fundraising, with average contribution sizes exceeding USD 420 per investor.

Why is regulatory harmonization accelerating structured crowdfunding adoption?

Europe represented nearly 31.4% of the global Crowdfunding Platforms market in 2024, with Germany, the UK, and France contributing more than 63% of regional activity. Regulatory alignment under pan-European crowdfunding frameworks has strengthened investor protection and boosted confidence in equity-based platforms. Sustainability-linked and social-impact campaigns accounted for over 36% of total European campaigns. Adoption of emerging technologies such as automated compliance checks, blockchain-based transaction records, and AI-powered investor matching increased by 29% year-over-year. A prominent European platform expanded cross-border equity crowdfunding capabilities, supporting campaigns across multiple EU countries. Regional consumer behavior reflects strong demand for explainable platforms, transparent risk disclosures, and fixed investment limits, driven by regulatory oversight and investor education initiatives.

What is driving the surge of mobile-first crowdfunding ecosystems across emerging economies?

Asia-Pacific accounted for approximately 21.7% of global Crowdfunding Platforms activity in 2024 and ranked as the fastest-growing region by campaign volume. China, India, and Japan together generated nearly 71% of regional campaigns, supported by smartphone penetration exceeding 74% and rapid growth in startup ecosystems. Mobile-first platforms dominate, with over 67% of contributors accessing campaigns via apps. Infrastructure development in digital payments and instant settlement systems has reduced funding cycle times by nearly 32%. A regional platform expanded SME-focused crowdfunding services in India, supporting thousands of early-stage ventures. Consumer behavior is highly transaction-driven, with frequent micro-investments and strong participation in e-commerce, social innovation, and creator-led campaigns.

How are financial inclusion goals shaping alternative funding adoption?

South America accounted for around 4.6% of the global Crowdfunding Platforms market in 2024, led by Brazil and Argentina, which together represented over 64% of regional activity. Crowdfunding adoption is closely tied to SME financing, renewable energy projects, and creative industries. Government-backed digital finance initiatives and relaxed fundraising caps have supported platform growth. More than 38% of contributors in the region are first-time investors, highlighting the role of crowdfunding in financial inclusion. A regional platform expanded localized language interfaces and installment-based contributions to improve accessibility. Consumer behavior emphasizes community-backed campaigns and localized storytelling, particularly in media, arts, and social development projects.

Why are digital transformation and youth demographics fueling platform adoption?

The Middle East & Africa region accounted for approximately 2.5% of global Crowdfunding Platforms activity in 2024, with the UAE and South Africa emerging as key growth markets. Rising digital banking adoption and regulatory sandboxes have enabled controlled expansion of equity and donation-based crowdfunding. Technology modernization, including secure payment gateways and AI-driven identity verification, has improved platform reliability. A local platform in the Gulf region expanded Sharia-compliant crowdfunding offerings to attract new contributors. Consumer behavior is influenced by youth participation and diaspora funding, with higher engagement in social causes, small business funding, and technology startups.

United States – ~34.2% market share; driven by advanced platform innovation, strong investor participation, and diversified crowdfunding models.

United Kingdom – ~11.6% market share; supported by mature equity crowdfunding regulations and high startup funding activity.

The Crowdfunding Platforms market is moderately fragmented, with over 120 active global and regional platforms operating across donation, reward, equity, and debt models. The top five platforms collectively account for approximately 47% of total global activity, reflecting strong brand recognition and user trust. Competitive positioning is influenced by platform transparency, regulatory compliance, campaign success rates, and technology sophistication. Strategic initiatives include partnerships with payment processors, integration of AI-based campaign analytics, and expansion into cross-border fundraising. In 2024, more than 35 strategic collaborations were announced to enhance investor onboarding and fraud prevention. Innovation trends focus on secondary market access, tokenized assets, and real-time reporting dashboards. Smaller players compete through niche focus areas such as social impact, creative industries, or regional SME funding.

Seedrs

Crowdcube

Fundable

CircleUp

Patreon

Mightycause

Republic

Wefunder

StartEngine

Givebutter

Kiva

Technology plays a central role in the evolution of the Crowdfunding Platforms market, enhancing trust, efficiency, and scalability. AI-driven campaign analytics evaluate thousands of behavioral and financial data points to predict funding success, improving campaign optimization by over 30%. Automated KYC and AML systems reduce onboarding times by nearly 45%, enabling faster campaign launches. Blockchain technology is increasingly used for immutable transaction records and smart contract–based fund releases, improving transparency and accountability. Advanced payment gateways support multi-currency and micro-transaction processing, expanding cross-border participation. Data visualization dashboards provide real-time insights into campaign performance, contributor demographics, and funding velocity. Cybersecurity enhancements, including biometric authentication and encrypted escrow accounts, protect investor funds. Emerging technologies such as tokenized equity, secondary trading modules, and API-based integrations with financial institutions are expected to reshape platform capabilities and investor engagement models.

• In April 2024, Kickstarter enhanced its platform with AI-powered campaign recommendation tools, improving project discovery and increasing average pledge conversion rates. Source: www.kickstarter.com

• In September 2023, Indiegogo expanded its equity crowdfunding services to support additional international markets, streamlining compliance and investor onboarding. Source: www.indiegogo.com

• In June 2024, GoFundMe introduced advanced fraud detection algorithms that reduced suspicious campaign activity and improved donor trust metrics. Source: www.gofundme.com

• In November 2023, Crowdcube launched enhanced investor analytics dashboards, enabling startups to track engagement and funding momentum in real time. Source: www.crowdcube.com

The Crowdfunding Platforms Market Report delivers a comprehensive assessment of digital fundraising ecosystems across global regions and industry verticals. The scope covers major crowdfunding models, including donation-based, reward-based, equity-based, and debt-based platforms. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level insights for leading markets. The report evaluates applications across startups, SMEs, real estate, creative industries, social causes, healthcare innovation, and renewable energy projects. Technology coverage includes AI-driven analytics, blockchain-enabled transparency, automated compliance tools, secure payment infrastructure, and mobile-first platform architectures. Competitive analysis reviews global leaders and regional specialists, highlighting platform capabilities, innovation strategies, and operational scale. The scope also incorporates regulatory frameworks, investor behavior trends, cross-border fundraising dynamics, and emerging niches such as tokenized crowdfunding and impact investing.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2,149.3 Million |

|

Market Revenue in 2032 |

USD 7,095.0 Million |

|

CAGR (2025 - 2032) |

16.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Kickstarter, Indiegogo, GoFundMe, Seedrs, Crowdcube, Fundable, CircleUp, Patreon, Mightycause, Republic, Wefunder, StartEngine, Givebutter, Kiva |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |