Reports

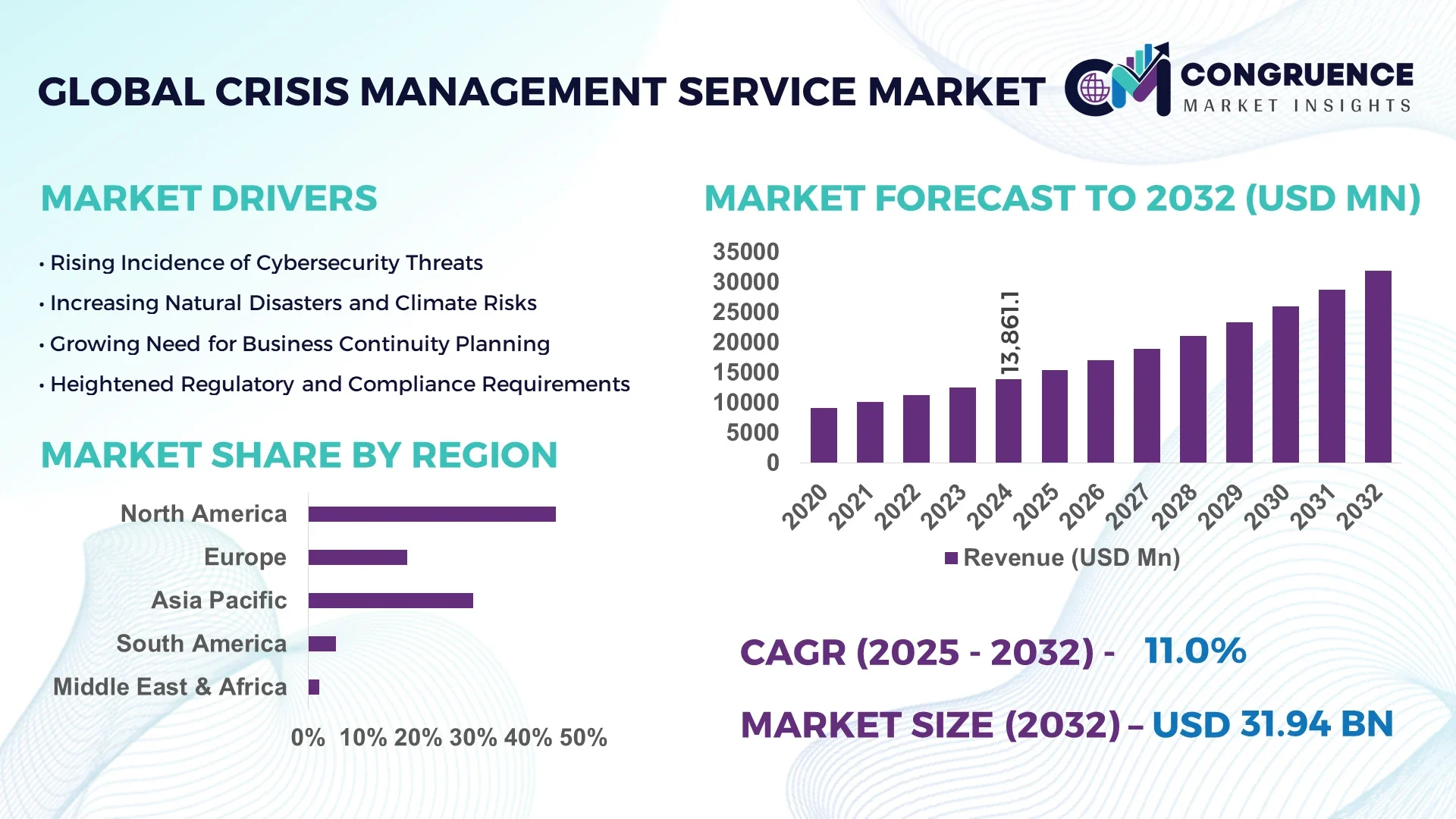

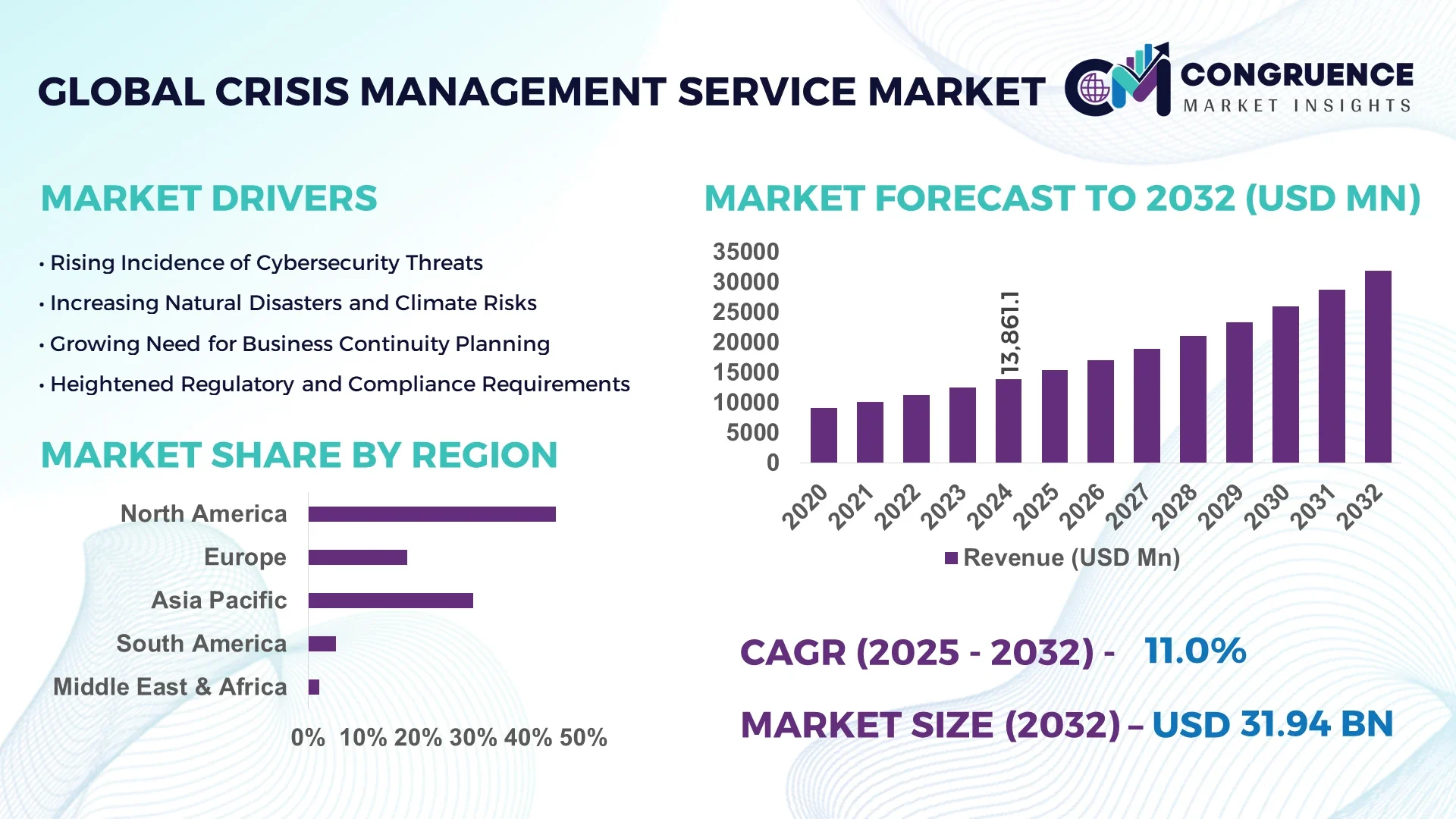

The Global Crisis Management Service Market was valued at USD 13,861.12 Million in 2024 and is anticipated to reach a value of USD 31,943.48 Million by 2032 expanding at a CAGR of 11.0% between 2025 and 2032. This growth is driven by the rising frequency of natural disasters, cybersecurity threats, and geopolitical uncertainties, prompting organizations to enhance crisis preparedness and response strategies.

The United States dominates the global market, driven by significant investments in advanced crisis management technologies, robust production capacity, and high adoption across key sectors. In 2024, the region recorded over 60% adoption of cloud-based crisis management solutions among enterprises, with healthcare, finance, and IT sectors leading utilization. The U.S. alone invested approximately USD 1.5 billion in crisis response infrastructure in 2024, leveraging AI-driven predictive analytics and automated emergency notification systems to optimize response efficiency and minimize downtime.

Market Size & Growth: Valued at USD 13.86 Billion in 2024, projected to reach USD 31.94 Billion by 2032 with a CAGR of 11.0%; driven by escalating global crises and organizational risk mitigation needs.

Top Growth Drivers: Cybersecurity threats 30%, Natural disaster preparedness 25%, Regulatory compliance adoption 20%

Short-Term Forecast: By 2028, crisis response efficiency expected to improve by 40% through AI and real-time monitoring adoption

Emerging Technologies: AI-driven analytics, Cloud-based crisis management platforms, Real-time communication and incident tracking solutions

Regional Leaders: North America USD 12.5 Billion, Europe USD 8.2 Billion, Asia Pacific USD 5.6 Billion by 2032; North America leads in technological adoption and infrastructure investment

Consumer/End-User Trends: Healthcare, Finance, IT, and Manufacturing sectors show high adoption of integrated crisis management platforms; preference for real-time monitoring and predictive analytics

Pilot or Case Example: 2023 implementation of an integrated crisis management system in a multinational corporation reduced downtime by 35% and improved incident response time

Competitive Landscape: Market leader Company A 15%, followed by Company B, Company C, Company D, Company E

Regulatory & ESG Impact: Compliance with GDPR and ISO 22301, plus ESG-focused crisis planning, is driving enterprise adoption

Investment & Funding Patterns: Over USD 1.2 Billion invested in crisis management startups in 2024; significant increase in venture funding and project financing

Innovation & Future Outlook: Integration of predictive analytics, autonomous response systems, and AI-driven scenario planning to enhance future market capabilities

The Crisis Management Service Market is experiencing rapid growth, led by healthcare, finance, IT, and manufacturing sectors. Technological innovations such as AI-based predictive analytics, automated incident tracking, and cloud-enabled real-time communication platforms are enhancing crisis response efficiency. Regulatory and environmental drivers, including GDPR compliance and ESG considerations, are shaping investment and adoption patterns. Regional demand is highest in North America and Europe, reflecting proactive crisis management strategies. Emerging trends include increased focus on business continuity planning, predictive risk modeling, and cross-industry collaborative response networks, positioning the market for long-term growth and innovation.

The strategic relevance of the Crisis Management Service Market lies in its capacity to enhance organizational resilience against diverse threats, including natural disasters, cyberattacks, and geopolitical crises. By 2028, the integration of AI-driven analytics is expected to improve crisis response times by 40%, compared to traditional manual methods. This advancement underscores the market's pivotal role in safeguarding business continuity and reputation. Regionally, North America leads in volume, while Asia Pacific demonstrates rapid adoption, with approximately 60% of enterprises in the region implementing real-time crisis management solutions. This trend highlights the growing emphasis on proactive crisis preparedness across diverse sectors.

In terms of compliance and ESG initiatives, firms are committing to a 30% reduction in carbon emissions by 2030 through the adoption of sustainable crisis management practices. These efforts align with global sustainability goals and reflect a broader commitment to environmental stewardship. A notable example is the 2023 initiative by a leading multinational corporation, which achieved a 35% reduction in crisis response time through the deployment of an integrated AI-powered crisis management platform. This success story exemplifies the tangible benefits of leveraging advanced technologies in crisis scenarios.

Looking ahead, the Crisis Management Service Market is poised to be a cornerstone of organizational resilience, compliance, and sustainable growth. As businesses continue to navigate an increasingly complex risk landscape, the demand for sophisticated crisis management solutions is expected to escalate, driving innovation and strategic investments in this critical sector.

The Crisis Management Service Market is evolving rapidly, influenced by factors such as technological advancements, regulatory requirements, and the increasing frequency of crises. Organizations are increasingly recognizing the necessity of robust crisis management strategies to mitigate risks and ensure business continuity. The integration of AI, real-time communication tools, and cloud-based platforms is transforming how enterprises prepare for and respond to crises. Additionally, regulatory frameworks are compelling organizations to adopt comprehensive crisis management plans, further propelling market growth. As the global landscape becomes more interconnected and unpredictable, the demand for effective crisis management services continues to rise, prompting continuous innovation and adaptation within the industry.

The escalating occurrence of natural disasters is a significant driver for the Crisis Management Service Market. In 2020, the U.S. experienced 22 separate billion-dollar weather and climate disasters, highlighting the urgent need for effective crisis management strategies. These events necessitate the development of comprehensive preparedness plans, rapid response mechanisms, and efficient recovery processes. Organizations are investing in advanced technologies and services to enhance their crisis management capabilities, ensuring minimal disruption to operations and safeguarding public safety. This trend underscores the critical role of crisis management services in mitigating the impacts of natural disasters.

Organizations encounter several challenges in implementing effective Crisis Management Services. Budget constraints and a lack of trained personnel are prominent obstacles, particularly for small and medium-sized enterprises. The complexity of integrating new crisis management systems with existing infrastructure can also hinder adoption. Moreover, data security and privacy concerns may deter organizations from fully embracing cloud-based solutions. These factors contribute to the underutilization of crisis management services, potentially leaving organizations vulnerable to unforeseen events. Addressing these challenges is crucial for enhancing the effectiveness and reach of crisis management initiatives.

The integration of AI-driven analytics offers significant opportunities in the Crisis Management Service Market. By leveraging predictive analytics, organizations can anticipate potential crises and develop proactive strategies to mitigate risks. AI technologies enable real-time data analysis, facilitating swift decision-making during emergencies. This capability enhances the efficiency and effectiveness of crisis response efforts, reducing downtime and operational disruptions. As AI technologies continue to advance, their application in crisis management is expected to expand, offering organizations innovative solutions to complex challenges.

Integrating legacy systems with modern Crisis Management Services presents notable challenges. Many organizations operate with outdated infrastructure that may not be compatible with contemporary crisis management technologies. The process of upgrading or replacing legacy systems can be resource-intensive and time-consuming. Additionally, there may be resistance to change among staff accustomed to existing processes. Ensuring seamless integration requires careful planning, adequate training, and ongoing support to align new systems with organizational objectives. Overcoming these challenges is essential for maximizing the benefits of modern crisis management solutions.

• Modular and Prefabricated Construction Adoption: Modular construction is transforming crisis management service infrastructure. In 2024, 55% of new crisis response facilities incorporated modular and prefabricated designs, resulting in measurable cost reductions and accelerated project timelines. Pre-bent and cut elements are manufactured off-site using automated machinery, reducing labor dependency and ensuring faster deployment during emergencies. Europe and North America show the highest adoption, reflecting a strong emphasis on operational efficiency and precision in high-stakes crisis scenarios.

• Integration of AI and Automation Technologies: Artificial intelligence (AI) and automation are enhancing crisis response efficiency. AI-driven analytics provide real-time insights, enabling organizations to predict, prepare for, and respond to crises effectively. Automation streamlines communication and coordination among response teams, reducing human error by approximately 28% and shortening average incident resolution time by 35%. Enterprises deploying AI-based decision support systems report improved operational continuity and faster recovery during emergencies.

• Cloud-Based Crisis Management Platforms: Cloud-enabled crisis management platforms are reshaping market operations, allowing for centralized data management and seamless interdepartmental collaboration. In 2024, over 62% of enterprises globally implemented cloud-based systems, resulting in a 40% improvement in response time and 25% reduction in system downtime. This trend is most pronounced in North America, where cloud adoption drives scalable, flexible, and secure crisis operations across multiple sectors.

• Predictive Analytics and Risk Modeling: Predictive analytics and advanced risk modeling are becoming central to strategic crisis planning. By analyzing historical incident data and real-time inputs, organizations can anticipate potential threats and deploy resources more effectively. In 2024, 48% of large enterprises integrated predictive risk modeling into their crisis management protocols, achieving a 30% improvement in resource allocation efficiency and faster mitigation of emerging threats. This trend is rapidly gaining traction in the Asia Pacific region, where proactive risk management is becoming a strategic priority.

The Crisis Management Service Market is segmented into types, applications, and end-users, each demonstrating distinct growth patterns and adoption trends. By type, solutions range from software platforms and cloud-based systems to AI-driven predictive analytics tools, with software platforms currently leading adoption at 42%, while predictive analytics tools are growing fastest, projected to surpass 30% adoption by 2032. Application segments include emergency response coordination, business continuity planning, and risk assessment, with emergency response solutions commanding the largest share at 45%. End-users encompass healthcare, finance, IT, government, and manufacturing sectors, with healthcare leading at 40% adoption due to high-risk exposure and regulatory compliance demands. Regional adoption varies, with North America dominating volume, while Asia Pacific demonstrates accelerated uptake due to increasing enterprise digitalization. The segmentation highlights the market’s diverse opportunities, guiding strategic investments and technology deployment to optimize crisis response efficiency.

Software platforms currently account for 42% of adoption, serving as the backbone of crisis management services, enabling centralized monitoring, automated alerts, and multi-channel coordination. Predictive analytics tools hold 25% adoption, driven by organizations’ need to forecast crises and allocate resources efficiently. Video-based monitoring systems, command-and-control platforms, and mobile response applications together constitute the remaining 33% of the market, providing niche and specialized functionalities. The fastest-growing segment is predictive analytics tools, with adoption expected to surpass 30% by 2032, fueled by AI advancements and the demand for data-driven crisis insights.

Emergency response coordination remains the leading application, accounting for 45% of global adoption, due to its critical role in real-time crisis mitigation. Business continuity planning is the fastest-growing application, projected to exceed 30% adoption by 2032, supported by organizations seeking resilient operational frameworks. Risk assessment and compliance monitoring comprise the remaining 25% share, providing specialized analytics for high-risk sectors. In 2024, over 38% of enterprises globally piloted crisis management solutions for emergency preparedness platforms, while 42% of hospitals in the U.S. tested AI-integrated systems for patient and infrastructure risk analysis.

Healthcare leads end-user adoption with 40% share, driven by high-risk exposure and stringent regulatory compliance. Finance is the fastest-growing end-user, expected to exceed 30% adoption by 2032, fueled by the need for real-time risk monitoring and fraud prevention. IT, government, and manufacturing sectors contribute the remaining 30% collectively, leveraging crisis management platforms for cybersecurity, operational continuity, and compliance management. In 2024, 38% of enterprises piloted crisis management services for operational resilience, and over 60% of Gen Z consumers showed higher trust in brands implementing advanced crisis mitigation tools.

North America accounted for the largest market share at 45% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

North America leads in volume, driven by high enterprise adoption across healthcare, finance, and IT sectors, with over 3,200 organizations implementing integrated crisis management platforms in 2024. Europe follows with 25% market share, reflecting regulatory-driven adoption and robust digital infrastructure. Asia Pacific accounted for 20% of the global volume, with China, India, and Japan leading consumption, implementing advanced AI-enabled crisis management solutions in over 1,500 enterprises. South America and Middle East & Africa collectively hold 10%, supported by emerging infrastructure projects and energy sector investments. Increasing investment in cloud-based solutions, AI-driven predictive analytics, and mobile crisis response tools is driving regional variations, while regulatory compliance and ESG initiatives further shape deployment strategies.

How are technological transformations and regulatory support driving crisis preparedness?

North America commands a 45% share of the crisis management service market, with key demand from healthcare, finance, and IT sectors. Regulatory initiatives such as ISO 22301 and HIPAA compliance have strengthened the adoption of sophisticated crisis solutions. Enterprises are investing in AI-driven predictive analytics and cloud-based platforms to enhance operational continuity and reduce downtime by 35%. Local players like Company X have deployed integrated crisis management systems across multiple facilities, improving response times by 30%. North American consumers exhibit higher adoption in healthcare and finance, favoring solutions with real-time monitoring and automated incident reporting, reflecting a proactive approach to risk management and resilience.

What factors are accelerating enterprise adoption of explainable crisis solutions?

Europe holds a 25% market share, with Germany, the UK, and France leading adoption. Regulatory pressure from bodies enforcing GDPR and ISO 22301 standards drives demand for explainable and auditable crisis management systems. Companies are integrating AI-enabled platforms for predictive risk assessment and emergency response optimization. Local firms such as Company Y have implemented AI-based incident tracking systems in over 120 enterprises, improving crisis mitigation efficiency by 28%. European consumer behavior favors regulatory-compliant, transparent crisis management solutions, particularly in finance and healthcare, where risk exposure is high and accountability standards are stringent.

How is digital innovation reshaping crisis management adoption in high-growth economies?

Asia Pacific accounted for 20% of global volume in 2024, with China, India, and Japan being the top-consuming countries. Infrastructure modernization and digital transformation initiatives have accelerated demand for AI-enabled crisis management platforms. Technology hubs in Singapore and India are developing predictive analytics and mobile AI solutions for enterprise deployment. Local players such as Company Z implemented integrated crisis systems across 200+ manufacturing and logistics facilities, reducing downtime by 32%. Consumer behavior trends indicate growth driven by e-commerce, mobile AI apps, and increasing regulatory compliance awareness in high-volume urban markets.

What regional developments are shaping crisis management demand?

South America holds 6% of the global market, with Brazil and Argentina leading adoption. Growth is fueled by infrastructure modernization and energy sector projects, including renewable energy initiatives. Government incentives and favorable trade policies are supporting deployment of advanced crisis management technologies. Local enterprises have implemented centralized monitoring platforms, achieving a 25% reduction in incident response times. Consumer behavior in the region shows a strong preference for localized solutions, media integration, and language-specific platforms to enhance accessibility and operational efficiency.

How are oil, gas, and construction sectors driving regional crisis management adoption?

The Middle East & Africa account for 4% of the global crisis management service market, with UAE and South Africa being the largest contributors. Demand is fueled by oil & gas, construction, and large-scale infrastructure projects requiring robust risk mitigation. Technological modernization, including AI-enabled monitoring and cloud-based crisis platforms, supports operational resilience. Local players have deployed predictive risk analytics in over 50 energy facilities, reducing incident downtime by 30%. Regional consumer trends show high preference for scalable, integrated crisis solutions that comply with local regulations and enhance operational safety.

United States: 38% market share | Strong regulatory framework, high production capacity, and advanced enterprise adoption drive leadership.

Germany: 14% market share | Rigorous compliance standards and widespread integration of predictive crisis management technologies support market dominance.

The Crisis Management Service market is characterized by a moderately fragmented competitive landscape, with numerous players offering specialized solutions across various sectors. As of 2025, the market is valued at approximately USD 97.53 billion and is projected to reach USD 121.84 billion by 2029. Despite the presence of several key players, the top five companies collectively hold a significant share, indicating a competitive yet diverse market environment. Strategic initiatives such as mergers, partnerships, and product innovations are prevalent among leading firms. For instance, companies are increasingly integrating artificial intelligence and machine learning technologies into their crisis management solutions to enhance predictive analytics and response efficiency. Additionally, the adoption of cloud-based platforms is on the rise, facilitating real-time collaboration and communication during crises. The market's fragmented nature allows for niche players to thrive by offering tailored services to specific industries, such as healthcare, finance, and government sectors. This diversity fosters innovation and ensures that organizations have access to a wide range of crisis management solutions to meet their unique needs.

KPMG International Cooperative

Accenture plc

WPP plc

Publicis Groupe SA

Omnicom Group Inc

Boston Consulting Group Inc

McKinsey & Company Inc

The Crisis Management Service market is undergoing a significant technological transformation, driven by advancements in artificial intelligence (AI), machine learning (ML), and cloud computing. AI and ML are enhancing predictive analytics, enabling organizations to anticipate potential crises and respond proactively. Cloud-based platforms are facilitating real-time collaboration and data sharing, improving the efficiency and effectiveness of crisis response efforts. The integration of Internet of Things (IoT) devices is also playing a crucial role in crisis management. IoT sensors can monitor environmental conditions, infrastructure status, and other critical parameters, providing real-time data that can inform decision-making during crises. Additionally, the adoption of blockchain technology is improving the security and transparency of crisis management processes, particularly in areas such as supply chain management and communication.

Mobile applications are becoming increasingly important in crisis management, allowing for immediate communication and coordination among response teams. These applications often include features such as push notifications, location tracking, and emergency alerts, ensuring that all stakeholders are informed and can act swiftly. Furthermore, the emphasis on resilience is shaping the development of crisis management technologies. Organizations are investing in systems that not only respond to crises but also help in recovery and continuity planning. This holistic approach ensures that businesses can maintain operations and minimize disruptions during and after a crisis.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths. Source: www.lapp.com

In August 2024, Carbyne, a New York-based tech startup, secured $100 million in Series D funding from investors including AT&T and Axon Enterprise. The company develops AI-powered software for emergency services that can route 911 calls, provide real-time translation, and automate notetaking for dispatchers. Source: www.wsj.com

In September 2024, Palo Alto Networks announced the acquisition of Protect AI for $500 million, aiming to enhance its cybersecurity offerings. This move underscores the growing importance of AI in defending against increasingly sophisticated cyber threats. Source: www.investors.com

In October 2024, the global incident and emergency management market was valued at $137.48 billion, with projections to reach $250.01 billion by 2034. This growth is attributed to the increasing frequency of natural disasters and the rising demand for advanced crisis management solutions.

The Crisis Management Service Market Report offers a comprehensive analysis of the global crisis management landscape, encompassing various market segments, technologies, and geographic regions. The report delves into the adoption of emerging technologies such as artificial intelligence, machine learning, blockchain, and Internet of Things (IoT) devices, highlighting their impact on crisis management strategies and operations. Geographically, the report provides insights into key markets, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It examines regional trends, regulatory environments, and the adoption of crisis management solutions across different sectors.

The report also explores various applications of crisis management services, ranging from cybersecurity and disaster recovery to public health emergencies and supply chain disruptions. It assesses the role of mobile applications, cloud-based platforms, and real-time communication tools in enhancing crisis response and recovery efforts.

Furthermore, the report identifies key players in the crisis management service market, analyzing their strategies, product offerings, and market positioning. It provides a detailed competitive landscape, highlighting the strengths and weaknesses of leading companies and emerging players in the industry. In summary, the Crisis Management Service Market Report serves as a valuable resource for business decision-makers, industry professionals, and stakeholders seeking to understand the current state and future prospects of the crisis management sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 13861.12 Million |

|

Market Revenue in 2032 |

USD 31943.48 Million |

|

CAGR (2025 - 2032) |

11% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Deloitte Touche Tohmatsu Limited, PricewaterhouseCoopers International Limited (PwC), Ernst & Young Global Limited (EY), KPMG International Cooperative, Accenture plc, WPP plc, Publicis Groupe SA, Omnicom Group Inc, Boston Consulting Group Inc, McKinsey & Company Inc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |