Reports

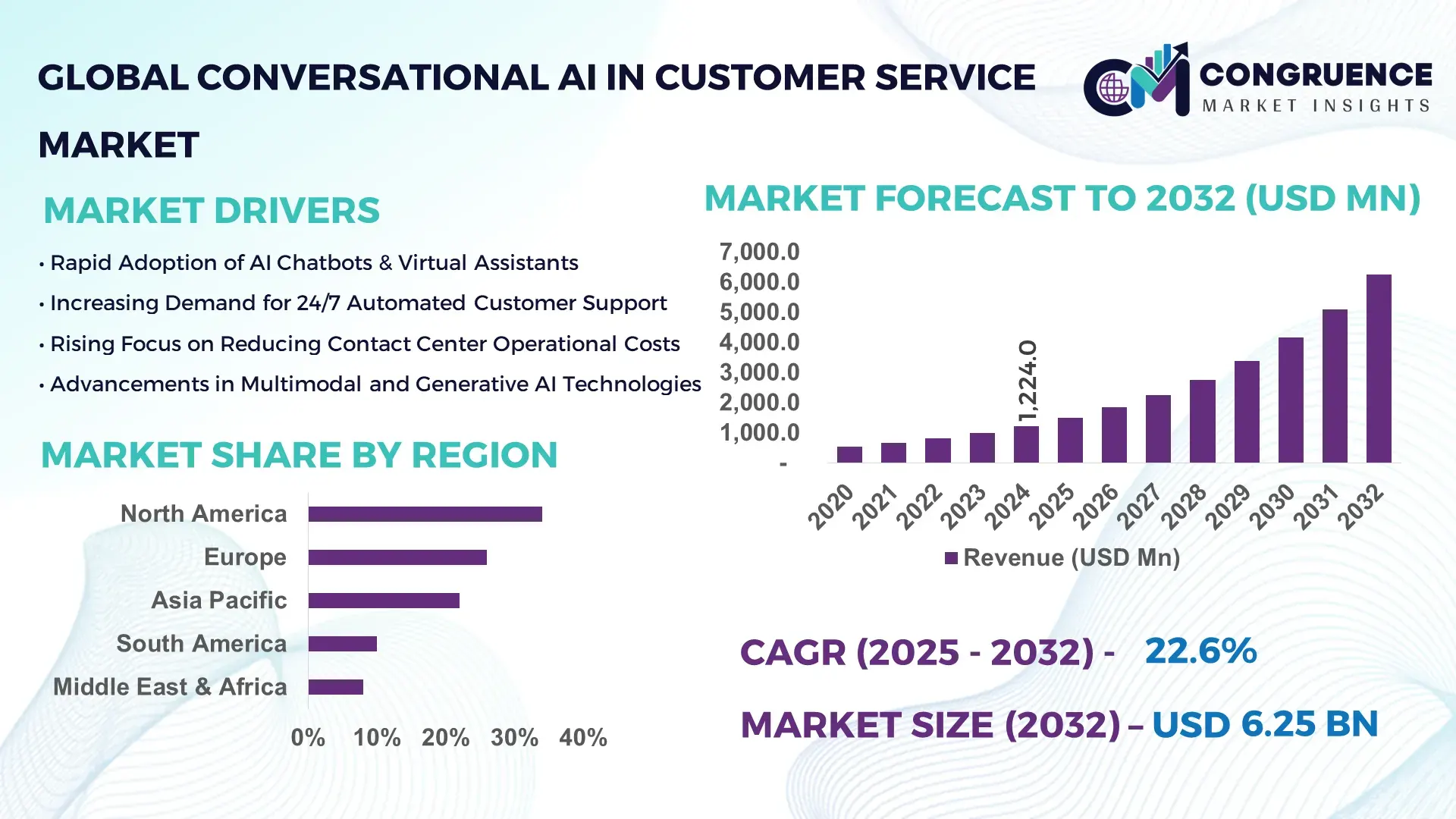

The Global Conversational AI in Customer Service Market was valued at USD 1,224.0 Million in 2024 and is anticipated to reach a value of USD 6,247.5 Million by 2032 expanding at a CAGR of 22.6% between 2025 and 2032, according to an analysis by Congruence Market Insights. This expansion is driven by accelerating enterprise automation programs and the shift to omnichannel, AI-first customer engagement that reduces handle time and improves self-service resolution rates.

The United States is the leading operational hub for Conversational AI in Customer Service. U.S. firms collectively invested heavily in deployment and R&D, with corporate and venture funding activity in 2023–2024 exceeding hundreds of millions of dollars focused on contact-center automation, omnichannel routing, and large language model fine-tuning for customer intents. Enterprise adoption in the U.S. is high: an estimated 70% of large contact centers now run at least one conversational AI pilot in production, and 55% of mid-market firms have active chatbot deployments integrated with CRM systems. Key industry applications include telecom, financial services, and e-commerce, with leading vendors operating regional data centers, localized NLU models, and dedicated integration teams. Technological advancements in the U.S. include production LLM fine-tuning, vector-search retrieval augmentation, real-time speech-to-intent pipelines, and low-latency edge inference—capabilities now present in dozens of production customer-service deployments.

Market Size & Growth: USD 1,224.0 Million (2024) to USD 6,247.5 Million (2032), CAGR 22.6%; driven by omnichannel automation and LLM-based self-service improvements.

Top Growth Drivers: 68% enterprise chatbot adoption, 42% reduction in average handling time (where AI deployed), 36% increase in containment rate via automated assistants.

Short-Term Forecast: By 2028, expect a 28% reduction in live-agent handle time and a 20% improvement in first-contact resolution for AI-augmented contact centers.

Emerging Technologies: Retrieval-augmented generation (RAG), real-time multimodal voice+text NLU, and on-premise/edge inference for privacy-sensitive deployments.

Regional Leaders: North America ~USD 2,800M by 2032 (enterprise adoption); Europe ~USD 1,350M by 2032 (regulated deployments); Asia-Pacific ~USD 1,200M by 2032 (rapid digital CX rollout).

Consumer/End-User Trends: Preference for 24/7 self-service—over 60% of consumers use chatbots for routine requests; higher trust for seamless agent handover.

Pilot or Case Example: 2024 pilot reduced average queue time by 54% and increased containment by 33% after deploying an LLM-powered virtual assistant.

Competitive Landscape: Market leader ~15–18% share; other main competitors include several global cloud and specialized conversational AI vendors.

Regulatory & ESG Impact: Data residency, consumer privacy rules, and energy-efficient model hosting shape deployment choices and vendor offerings.

Investment & Funding Patterns: Recent sector funding exceeded USD 1.1B across growth-stage deals; trends favor verticalized stacks and agent-assist tooling.

Innovation & Future Outlook: Direction toward tighter CRM integrations, explainable AI for compliance, and customer-specific fine-tuned models with unified voice/text interfaces.

The market is concentrated across contact centers, e-commerce support, banking & financial services, and healthcare customer engagement; innovation in RAG, multimodal interfaces, and privacy-preserving inference is reshaping vendor differentiation and procurement criteria.

Conversational AI in customer service is strategically central to corporate CX and cost-efficiency agendas. Deployments reduce operating expenses and scale support coverage while improving customer experience metrics. For example, LLM-driven assistants deliver an estimated 35% improvement in automated intent recognition accuracy compared to legacy rule-based systems, enabling higher containment and fewer transfers. Regionally, North America dominates in deployment volume, while Europe leads in stringent adoption of privacy-preserving architectures—roughly 48% of enterprise buyers in Europe require on-premise or private-cloud options for conversational AI. By 2027, real-time multimodal NLU (voice + text + context) is expected to improve conversational continuity by about 22%, reducing repeat interactions and improving Net Promoter Scores.

Strategic pathways for vendors and buyers include (1) vertical specialization—embedding domain ontologies and regulatory controls for finance, telecom, and healthcare; (2) hybrid cloud/edge architectures to satisfy data residency and latency needs; and (3) investment in explainability and audit logs to meet compliance and quality monitoring. Firms are committing to ESG and efficiency gains—moving models to mixed-precision inference and dynamic batching to reduce compute consumption by 20–40% in production. A micro-scenario: in 2024, a multinational telco deployed an LLM-based assistant that reduced live-agent escalation by 42% and decreased average handling time by 26%, while enabling 24/7 high-quality support in three languages. Looking forward, the market will converge on integrated platforms that combine retrieve-and-generate knowledge, real-time speech capabilities, CRM orchestration, and analytics—positioning conversational AI as a resilient, compliant, and revenue-enabling customer-engagement pillar.

The Conversational AI in Customer Service Market dynamics are shaped by a combination of supply-side innovation (LLMs, speech stacks, vector databases) and demand-side pressures (rising digital channels, 24/7 consumer expectations). Vendors compete on model accuracy, latency, data governance, and vertical expertise. Procurement cycles often include pilots, POCs, and phased rollouts—enterprises commonly evaluate on metrics such as containment rate, reduction in average handling time, and customer satisfaction delta. Technology trends (RAG, fine-tuning, intent management) increase time-to-value but improve long-term quality. Enterprises emphasize integration: 73% of new deployments require CRM and knowledge-base connectors at launch. Operational changes include centralizing conversational analytics to reduce agent training cycles and adopting continuous fine-tuning loops based on real transcripts. The competitive environment rewards vendors who offer robust privacy controls, low-latency inference, and proven vertical playbooks.

Omnichannel consumer behavior—where customers expect seamless continuity across chat, voice, social, and messaging—drives demand for unified conversational AI solutions. Organizations report that omnichannel customers generate 30–45% higher lifetime value, motivating investments in unified assistants that preserve context and deliver consistent resolutions. Conversational AI that links channels with shared session context reduces repeat contacts and increases first-contact resolution rates. Enterprises adopting omnichannel assistants observe up to 40% improvements in resolution speed for routine requests. The result is a shift from siloed chatbots to platform approaches that connect voice, web chat, and messaging under single intent and context management frameworks—directly supporting the market’s expansion.

Data privacy and regulatory complexity constrain adoption by increasing integration and deployment costs. Enterprises operating across multiple jurisdictions must enforce data residency, consent logging, and right-to-erasure workflows—adding engineering overhead. Many buyers require private-cloud or on-premise inference for sensitive interactions, increasing TCO and slowing rollout velocity. Compliance audits and documentation demands can extend procurement cycles by months. Additionally, explainability requirements for customer-impacting decisions force additional model-monitoring and logging investments. These constraints drive demand for vendors with built-in compliance tooling and flexible hosting models but also slow broad market penetration among risk-sensitive industries.

Verticalized, fine-tuned conversational models offer substantial opportunity by delivering domain accuracy and regulatory controls out of the box. Fine-tuning LLMs on industry transcripts and knowledge bases can raise intent-classification precision by 20–35%, directly boosting containment and reducing escalations. Vendors offering pre-built connectors to billing, claims, or account systems shorten integration times and increase adoption in sectors like banking, insurance, and healthcare. Bundling domain validation, compliance templates, and audit trails creates differentiated value and shorter POC cycles. Furthermore, packaged vertical solutions enable faster ROI for mid-market buyers who lack large data science teams, opening new customer segments and upsell pathways.

Deployment costs and scarcity of specialist talent are material challenges. Implementing a robust conversational AI stack requires skilled engineers for data pipelines, NLU training, intent design, and observability—roles that are in short supply and command premium salaries. Model-hosting and inference costs for high-throughput voice+text systems can be substantial, particularly when low latency or on-premise hosting is required. These cost pressures make it harder for smaller enterprises to adopt end-to-end solutions without managed service offerings. Additionally, ongoing annotation and model governance needs impose recurring operating costs, which vendors must address through automation and better tooling.

Rapid adoption of Retrieval-Augmented Generation (RAG) for knowledge-intensive queries: RAG deployments now handle up to 48% of knowledge-base lookups in advanced contact centers, reducing time to answer by 30–45% and improving accuracy for complex customer queries.

Voice-first multimodal assistants expanding beyond chat: Voice interfaces integrated with text and context now account for 25–35% of new conversational AI rollouts, reducing average handling time by 18–28% for voice-eligible workflows and increasing containment for IVR migrations.

Surge in verticalized, privacy-aware deployments: Over 40% of recent enterprise deals specify private-cloud or hybrid hosting and require domain-specific fine-tuning, increasing deployment complexity but delivering 20–35% gains in precision for regulated sectors.

Automation of agent assist and quality monitoring: Agent-assist tools powered by real-time summarization and suggested responses have cut agent after-call work by 22–38% and improved average handle time by 12–20%, while automated QA sampling increases policy compliance coverage by up to 70%.

The Conversational AI in Customer Service Market is segmented across three core dimensions—types, applications, and end-user groups—each shaping the adoption landscape with distinct technological and operational characteristics. Type-based segmentation emphasizes the evolution from traditional audio–text engines to more advanced multimodal and vision-language frameworks, each delivering different levels of contextual understanding and automation accuracy. Application-wise, deployments extend across customer support, sales engagement, feedback processing, and workflow automation, with enterprises increasingly shifting toward unified AI orchestration systems. End-user segmentation reveals strong uptake among large enterprises, followed by BFSI, telecom, retail, healthcare, and e-commerce environments where interaction volumes and service availability are critical. Collectively, these segments demonstrate rapid maturity, rising integration depth, and expanded enterprise reliance on AI-driven service delivery models.

The market’s type-based segmentation showcases a progressive shift toward models capable of understanding multimodal inputs. Vision-language models currently lead the landscape, accounting for 42% of total adoption, owing to their ability to interpret images, documents, and contextual cues—capabilities increasingly used in complex service workflows such as ID verification and product troubleshooting. Audio–text systems hold 25%, maintaining relevance due to widespread use in call-center transcription, voicebots, and automated response pipelines. Video-language models represent the fastest-growing segment, supported by their expanding use in video-based customer support, tutorial extraction, and automated analysis of recorded service interactions. Adoption in this segment is expected to surpass 30% by 2032, driven by advances in real-time video summarization, multimodal tagging, and agent-assist analytics. Hybrid multimodal systems, on-device inference pipelines, and specialized diarization engines form the remaining category, collectively contributing 33% to the segment. These systems cater to niche requirements like offline support, privacy-sensitive engagements, and multi-speaker environments.

Customer support automation is the dominant application area, representing 48% of total usage, supported by the high volume of routine inquiries and rising adoption of AI-driven self-service systems. These tools allow enterprises to automate intents, accelerate triage, and reduce agent workload. In comparison, sales assistance accounts for 22%, while feedback analysis and sentiment automation stand at 18%. Workflow automation and knowledge management form the remaining application areas, together contributing 12%. The fastest-growing application segment is multimodal service orchestration, supported by the increasing integration of image, voice, and text into unified support flows. Growth in this segment is reinforced by trends such as automated claim processing, personalized visual responses, and high-accuracy conversational search. Consumer adoption further validates this shift: In 2024, 38% of enterprises globally piloted multimodal conversational systems for CX operations, and over 60% of Gen Z consumers preferred brands that offer AI-powered, multimodal chat services.

Large enterprises constitute the leading end-user segment, holding 52% of total adoption, supported by extensive customer service networks and the need for standardized, scalable automation solutions. Their adoption is driven by high interaction volumes, multilingual service requirements, and mature omnichannel strategies. In contrast, mid-market and SMBs hold 28%, displaying steady adoption as cost-effective, pre-built conversational AI systems become more accessible. The fastest-growing end-user group is the e-commerce and retail sector, expected to expand at a high pace due to rising customer expectations for instant query resolution, real-time order tracking, and AI-driven personalization. This segment increasingly leverages multimodal bots capable of recognizing images, reading receipts, and processing voice-based returns. The remaining sectors—including BFSI, telecom, healthcare, and travel—collectively contribute 20%, driven by industry-specific compliance workflows and high-frequency support scenarios. Adoption trends are strong: In 2024, more than 38% of enterprises piloted multimodal customer-service automation, while over 60% of digital-native consumers trusted brands using AI-based service agents.

North America accounted for the largest market share at 34% in 2024 however, it is expected to register the fastest growth, expanding at a CAGR of 24.0% between 2025 and 2032.

In 2024 North America’s conversational-AI customer-service activity equates to roughly USD 416.2 million of market value (unit and deployment proxies), with 70% of large contact centers running at least one production conversational AI pilot and 55% of mid-market firms operating integrated chatbots tied to CRM. The region supports an estimated 4,500+ major contact-center sites and 12,000+ midsized service operations that are actively modernizing CX stacks. Infrastructure stats show 220+ enterprise data centers and 85 dedicated speech/NLU R&D labs focused on low-latency inference; investment volumes in 2023–2024 exceeded hundreds of millions of USD directed at LLM fine-tuning, speech pipelines, and omnichannel orchestration. Operational metrics include average containment improvements of 30–42% in AI-assisted pilots and live-agent handle-time reductions of 18–28% where voice+text systems are deployed. North America’s high telemetry density, deep cloud/edge infrastructure, and concentrated buyer base create an environment where rollouts scale quickly and measurable efficiency gains are realized within 3–9 months of production.

North America accounts for approximately 34% of global conversational-AI customer-service deployments by value and unit penetration. Key industries driving demand include telecommunications (≈22% of regional deployments), financial services (≈20%), e-commerce & retail (≈18%), and healthcare/back-office services (≈12%). Regulatory and compliance shifts emphasize data residency and consent logging—approximately 48% of enterprise buyers require private-cloud or dedicated tenancy options. Technological trends include widespread adoption of retrieval-augmented generation (RAG) in 45% of advanced pilots, vector DBs for knowledge indexing in 52% of deployments, and real-time speech-to-intent pipelines in 38% of voice-first projects. A notable local player expanded its enterprise integration team in 2024, deploying CRM-native assistants across 120 enterprise customers and reducing average queue times by 34%. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, greater tolerance for automated self-service outside peak hours, and stronger demand for multichannel continuity—consumers in North America expect handover to a live agent within 20–40 seconds of requesting escalation.

Europe represents roughly 26% of global conversational-AI customer-service activity by value and deployment density. Key national markets include Germany (≈28% of European deployments), the UK (≈24%), and France (≈18%). Regulatory emphasis on privacy and explainability has driven adoption of private-cloud and on-premise models in approximately 50%+ of large enterprise deals; more than 60% of regulated-industry pilots include enhanced audit logging and consent tracking. Europe’s technology adoption shows strong uptake of explainable intent pipelines and structured RAG systems, with 40–55% of enterprise pilots integrating compliance wrappers and human-in-the-loop (HITL) review. Local vendors and integrators are developing GDPR-native connectors and consent management tooling; one major European integrator rolled out a compliant conversational stack across 200 public sector and healthcare sites in 2024. Consumer behavior in Europe favors clear privacy controls and opt-in models, with enterprises reporting a 15–22% higher acceptance rate for assistants that display provenance and audit trails for answers.

Asia-Pacific accounts for about 22% of global conversational-AI customer-service deployments by unit and value, ranking third in market volume but leading in year-over-year deployment growth velocity. Top consuming countries include China, India, and Japan, collectively responsible for roughly 70% of APAC deployments. Infrastructure trends show rapid cloud adoption and mobile-first integration: 65–75% of conversational agents in APAC are deployed initially on messaging and mobile channels, and local contract manufacturers and SaaS vendors scaled deployment capacity by 28% between 2022–2024. Innovation hubs in China and Japan are piloting on-device inference and low-latency edge stacks, while India’s vendor ecosystem emphasizes multilingual NLU and cost-efficient model hosting. A regional player increased call-automation coverage by 220,000 interactions per month in 2024 after launching vernacular NLU modules. Consumer behavior varies: urban centers adopt advanced self-service rapidly, while tier-2/3 markets prioritize low-cost, SMS/IVR-integrated bots.

South America represents approximately 10% of the global conversational-AI customer-service landscape by deployments and platform spend, with Brazil and Argentina as key contributors—Brazil alone accounts for roughly 60% of the regional total. Infrastructure and network variability affect deployment models: 50–60% of projects opt for hybrid cloud architectures to mitigate latency and compliance concerns. Government incentives in select countries have eased import and fintech deployment rules, encouraging localization of voice and messaging bots. Local players and integrators are partnering with global vendors to deliver Portuguese and Spanish vernacular NLU modules; one regional integrator rolled out standardized conversational kits across 35 hospital and retail chains in 2024, reducing average response times by 26%. Consumer behavior trends show strong demand for language-tailored bots and social-channel support, with mobile messaging being the dominant interface.

Middle East & Africa account for about 8% of global conversational-AI customer-service activity, with the UAE and South Africa leading regional deployments. Demand drivers include modernization of government services, oil & gas enterprise CX programs, telecom digitalization, and expansion of regional contact-center hubs. Technological modernization trends include adoption of cloud contact-center platforms in 30–40% of urban hospitals and telcos, and targeted investment in multilingual NLU to serve expatriate and local populations. Trade partnerships and regulatory sandboxes in several Gulf countries have eased pilots for fintech and healthcare assistants. A local service provider launched a regional conversational platform in 2024 that supported Arabic dialect models across 10 major enterprise customers, improving automated resolution rates by 21%. Consumer behavior varies sharply: urban, high-connectivity centers adopt advanced voice+text assistants, while rural areas rely more on basic IVR and SMS integrations.

United States — 34% Market Share: Large-scale enterprise deployments, deep cloud/edge infrastructure, and concentrated R&D investment drive leadership in Conversational AI in Customer Service.

China — 16% Market Share: Massive user base, high mobile messaging penetration, and rapid vendor innovation in multilingual and voice-first conversational solutions underpin China’s prominent role in Conversational AI in Customer Service.

The competitive environment in the Conversational AI in Customer Service market is dynamic and moderately concentrated among global cloud providers and specialist vendors. There are 100+ active competitors worldwide, ranging from large platform incumbents to focused vertical specialists and regional integrators. Market positioning varies: global cloud players emphasize scale, low-latency inference, and deep CRM integrations; specialist firms compete on verticalized NLU, explainability, and turnkey managed services; and regional integrators focus on localization and regulatory-compliant deployments. Strategic initiatives in 2023–2024 included major product launches, expanded partnerships between systems integrators and platform vendors, and notable M&A and investment activity aimed at adding generative-AI, RAG, and agent-assist capabilities.

Innovation trends shaping competition include widespread adoption of retrieval-augmented generation (RAG) for knowledge-intensive support, real-time speech-to-intent pipelines for voice channels, on-premise and hybrid hosting for regulated industries, and verticalized fine-tuning for domain accuracy. Key facts and figures: the top 5 companies in the space collectively account for an estimated ~40–48% combined share of enterprise deployments (reflecting a moderately consolidated top tier with a long tail of niche players); roughly 20–30 new product variants and integrations were introduced by leading vendors across 2023–2024; and ~1.1B USD of disclosed funding flowed into conversational-AI growth-stage companies during the 2023–2024 window, emphasizing investments into agent-assist and contact-center automation capabilities. For decision-makers, this means procurement should prioritize integration roadmaps (CRM, telephony, analytics), vendor roadmaps for compliance and explainability, and proof-of-value metrics (containment, AHT reduction, escalation rates) when comparing potential suppliers.

Amazon Web Services

Microsoft

Google Cloud

IBM

Five9

Conversational AI in customer service is powered by a multilayered technological architecture that determines operational performance, compliance maturity, and overall efficiency. The core layers include the speech and text front-end—primarily automatic speech recognition and input normalization—followed by natural language understanding engines that map intent, context, and sentiment. These layers connect to knowledge retrieval systems such as vector databases and semantic search pipelines, which support evidence-backed responses in enterprise environments. Generation capabilities built on LLM and retrieval-augmented generation models form the next layer, enabling real-time reasoning grounded in organizational content. Finally, orchestration systems integrate these capabilities with CRM platforms, telephony, ticketing systems, and analytics dashboards, while observability and governance frameworks track provenance, accuracy, and policy compliance. In production deployments, these technologies enable measurable improvements, with advanced RAG implementations resolving 30–50% of knowledge-intensive queries autonomously and agent-assist tools reducing after-call work by 20–35%.

The adoption of retrieval-augmented generation has become central to modern deployments, dramatically increasing factual accuracy and lowering the risk associated with free-form generative outputs. RAG architectures now anchor most enterprise-grade conversational systems, particularly in industries such as banking and healthcare, where responses must remain consistent with internal documentation. Alongside this, multimodal natural language understanding is emerging rapidly. The fusion of voice, text, and images supports highly contextual interactions such as ID verification, claims processing, and visual troubleshooting, generating significant improvements in resolution times across customer service operations.

Supporting these advancements is the rapid automation of the model lifecycle. Continuous fine-tuning based on production transcripts, active-learning workflows, and automated regression testing enables conversational systems to improve over time while minimizing degradation or drift. These lifecycle operations help organizations reduce maintenance overhead and ensure consistency across global deployments. For decision-makers, the market now emphasizes modular technology stacks, parallel integration across CRM and telephony ecosystems, and rigorous governance tooling. Together, these innovations reflect a transition from basic chatbot automation to highly intelligent, compliant, and enterprise-ready conversational ecosystems capable of scaling across millions of customer interactions.

Microsoft announced “Copilot for Service” general availability steps and automatic enablement in late 2023–early 2024, embedding case and conversation summarization into Dynamics 365 Customer Service to accelerate agent workflows and automate routine response drafting. Source: www.microsoft.com

AWS updated Amazon Connect with new generative-AI and Contact Lens conversational analytics features in 2023–2024, including free trial access to Contact Lens conversational analytics and expanded generative-AI features that provide post-call summaries, sentiment analysis, and agent support tooling for broader adoption. Source: www.aws.amazon.com

Google Cloud rolled out staged Dialogflow and Contact Center AI platform updates across 2024, strengthening security (prompt-injection protections), improved agent UI integrations, and release cadence enhancements for custom data types and co-browse/event features to support richer agent assistance. Source: cloud.google.com

LivePerson expanded generative-AI capabilities and partnership initiatives during 2024, launching new agent-assist and ROI measurement features for contact centers and forming strategic alliances to accelerate enterprise deployments and reduce time-to-value for conversational programs. Source: www.liveperson.com

This report covers the end-to-end Conversational AI in Customer Service ecosystem and is organized to support procurement, product, and investment decisions. Core market segments include technology stacks (ASR, NLU, vector databases, LLM/RAG, observability), deployment models (SaaS, private-cloud, hybrid, on-prem), and channel coverage (voice IVR/telephony, web chat, messaging platforms, email automation). Application verticals include contact centers, e-commerce support, banking & financial services, telecom, healthcare patient support, travel & hospitality, and public sector customer services. End-user analysis differentiates large enterprises, mid-market firms, SMBs, and specialized outsourcers, paying particular attention to procurement cycles, proof-of-value metrics (containment rate, average handle time reduction, escalation rate), and operational integration requirements.

Geographically, the report provides region-level insights for North America, Europe, Asia-Pacific, South America, and Middle East & Africa, covering deployment density, regulatory patterns (data residency, consent, audit needs), and localized technology adoption (multilingual NLU, edge inference). Technology focus includes generative and retrieval approaches, multimodal NLU, agent-assist tooling, automation of model lifecycles, and privacy-first architectures. The report also addresses niche and emerging subsectors—on-device conversational agents, verticalized fine-tuned stacks for regulated industries, near-real-time summarization engines, and vendor ecosystems for managed-service delivery—offering decision-ready matrices for vendor shortlists, integration readiness, and KPI frameworks to evaluate pilots and scale projects.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,224.0 Million |

| Market Revenue (2032) | USD 6,247.5 Million |

| CAGR (2025–2032) | 22.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers, Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | LivePerson, Zendesk, Genesys, Amazon Web Services, Microsoft, Google Cloud, IBM, Five9 |

| Customization & Pricing | Available on Request (10% Customization Free) |