Reports

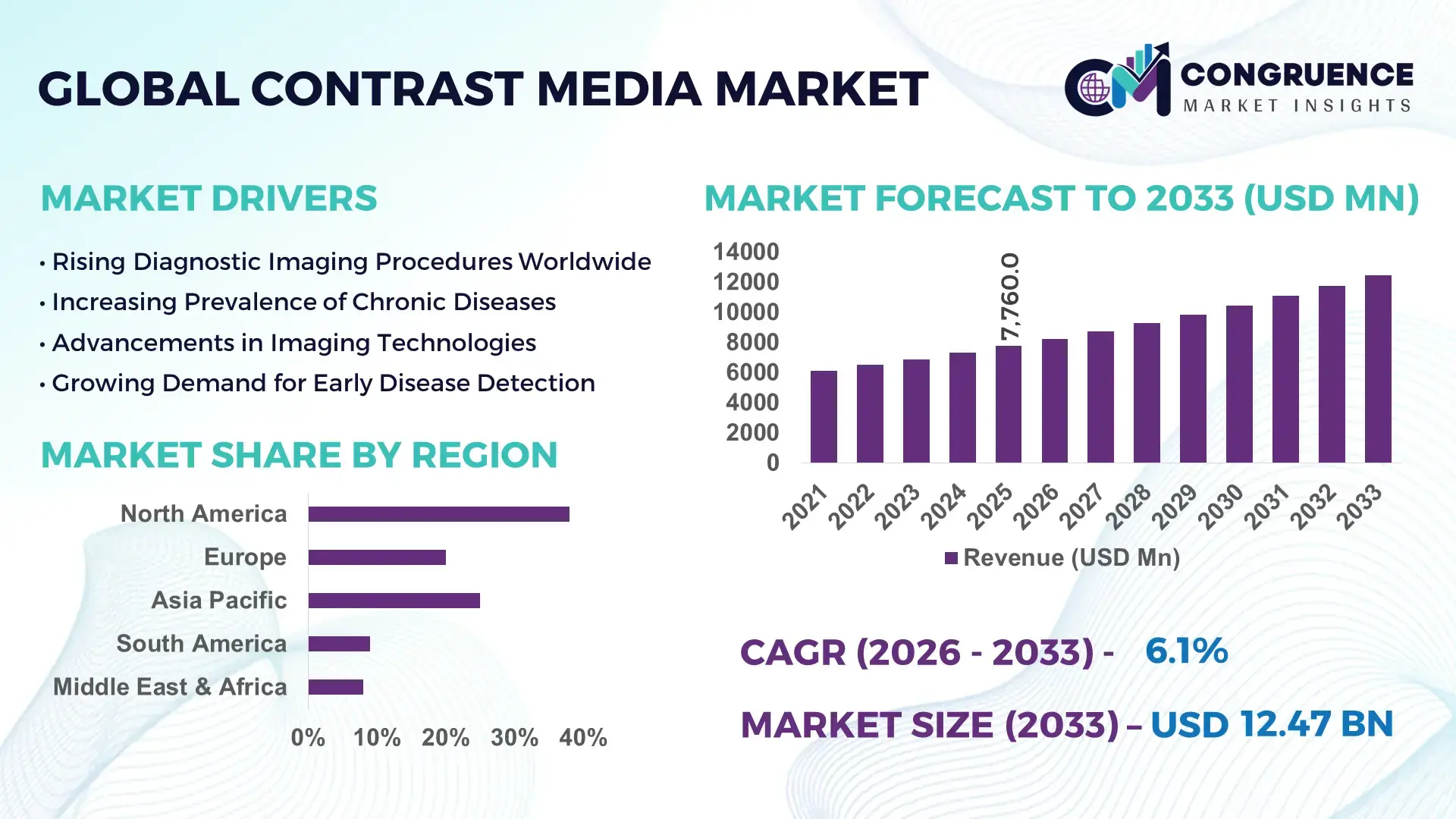

The Global Contrast Media Market was valued at USD 7760 Million in 2025 and is anticipated to reach a value of USD 12471.31 Million by 2033 expanding at a CAGR of 6.11% between 2026 and 2033. The increasing prevalence of chronic diseases and growing demand for diagnostic imaging procedures are key factors accelerating market expansion.

The United States continues to lead the contrast media market with advanced production capacity and significant investments in diagnostic imaging infrastructure. The country accounts for over 40% of global imaging procedures annually, with more than 80 million CT scans performed each year. High adoption of iodinated and gadolinium-based contrast agents is driven by widespread usage in cardiology, oncology, and neurology diagnostics. Investments exceeding USD 2 billion annually in radiology innovation and AI-integrated imaging technologies have further enhanced efficiency and precision. Additionally, over 65% of hospitals in the country utilize automated contrast injection systems, improving safety and dosage accuracy across clinical workflows.

Market Size & Growth: Valued at USD 7760 Million in 2025 and projected to reach USD 12471.31 Million by 2033, expanding at a CAGR of 6.11%, driven by rising diagnostic imaging demand.

Top Growth Drivers: Chronic disease prevalence increased by 35%, imaging procedure volumes up by 28%, and hospital infrastructure expansion contributing 22%.

Short-Term Forecast: By 2028, AI-enabled imaging workflows are expected to improve diagnostic efficiency by 30% and reduce scan time by 18%.

Emerging Technologies: AI-assisted imaging analytics, low-osmolar contrast agents, and microbubble-based ultrasound contrast innovations are gaining rapid traction.

Regional Leaders: North America projected at USD 5200 Million by 2033 with advanced imaging adoption; Europe at USD 3400 Million with regulatory-driven innovation; Asia-Pacific at USD 2900 Million driven by healthcare expansion.

Consumer/End-User Trends: Hospitals account for over 60% usage, with increasing adoption in outpatient imaging centers and specialty diagnostic clinics.

Pilot or Case Example: In 2024, a European healthcare network improved imaging workflow efficiency by 27% using AI-powered contrast optimization tools.

Competitive Landscape: Market leader holds approximately 32% share, followed by major players including multinational pharmaceutical and imaging solution providers.

Regulatory & ESG Impact: Increasing focus on reducing contrast-induced nephropathy risks and improving biodegradability standards across products.

Investment & Funding Patterns: Over USD 1.5 billion invested globally in imaging technologies, with strong venture funding in AI-driven diagnostics.

Innovation & Future Outlook: Integration of precision diagnostics and personalized contrast dosing is shaping next-generation imaging solutions.

The contrast media market is heavily influenced by key industry sectors such as radiology, oncology, cardiology, and neurology, which collectively account for over 70% of total usage. Technological advancements including low-toxicity contrast agents and AI-based imaging protocols are enhancing patient safety and diagnostic accuracy. Regulatory frameworks are increasingly emphasizing patient safety standards and environmental sustainability, pushing manufacturers to develop biodegradable and low-risk formulations. Regionally, Asia-Pacific is witnessing rapid growth due to expanding healthcare infrastructure and rising imaging procedure volumes, while Europe focuses on regulatory compliance and innovation. Emerging trends include personalized contrast dosing, integration with digital imaging platforms, and increased adoption of non-invasive diagnostic procedures, positioning the market for sustained growth.

The strategic relevance of the contrast media market lies in its critical role in enhancing diagnostic accuracy and enabling early disease detection across multiple medical disciplines. With over 75% of advanced imaging procedures requiring contrast agents, the market is increasingly aligned with precision medicine and value-based healthcare delivery. Advanced imaging technologies such as AI-driven contrast optimization deliver 32% improvement in diagnostic accuracy compared to conventional imaging protocols. This measurable enhancement is driving healthcare providers to adopt next-generation contrast solutions that improve clinical outcomes and reduce repeat scans.

From a regional perspective, North America dominates in volume due to high imaging procedure rates, while Asia-Pacific leads in adoption with over 45% of new healthcare facilities integrating advanced imaging technologies. By 2028, AI-integrated contrast media workflows are expected to reduce diagnostic errors by 28% and improve patient throughput by 22%, significantly enhancing operational efficiency in hospitals and imaging centers.

Sustainability and regulatory compliance are also shaping future pathways, with firms committing to reducing contrast agent toxicity by 30% and improving recycling of imaging waste materials by 25% by 2030. In 2024, a leading healthcare provider in Germany achieved a 20% reduction in contrast agent dosage through AI-based imaging protocols, demonstrating measurable efficiency gains and patient safety improvements. The contrast media market is evolving into a cornerstone of modern healthcare systems, supporting resilience through innovation, compliance with stringent regulations, and alignment with sustainable healthcare objectives, ensuring long-term growth and technological advancement.

The increasing demand for advanced diagnostic imaging procedures is a primary driver of the contrast media market. Globally, CT scan volumes have grown by over 30% in the past decade, while MRI usage has increased by approximately 25%, significantly boosting the demand for contrast agents. Chronic diseases such as cancer and cardiovascular conditions account for nearly 60% of imaging procedures requiring contrast enhancement. Hospitals and diagnostic centers are expanding imaging capabilities, with over 50% of new healthcare facilities integrating advanced radiology systems. Furthermore, the growing aging population, expected to reach 1.4 billion people aged 60 and above by 2030, is contributing to higher diagnostic needs. Technological advancements such as automated injectors and AI-based imaging tools are also improving efficiency and encouraging adoption.

Safety concerns associated with contrast agents remain a significant restraint for market growth. Contrast-induced nephropathy affects approximately 2% to 7% of patients undergoing imaging procedures, particularly those with pre-existing kidney conditions. Gadolinium-based contrast agents have also been linked to tissue retention issues, raising regulatory scrutiny and limiting usage in certain patient groups. Healthcare providers are increasingly cautious, with over 40% of hospitals implementing stricter screening protocols before administering contrast agents. Additionally, adverse allergic reactions, though rare, occur in approximately 0.6% of cases, further impacting patient acceptance. These challenges have led to increased demand for safer alternatives and non-contrast imaging techniques, slowing the adoption rate in specific segments of the market.

Technological innovation presents significant growth opportunities in the contrast media market. The development of low-toxicity and biodegradable contrast agents is gaining traction, with over 35% of new product pipelines focused on improving patient safety and environmental sustainability. AI-driven imaging systems are enabling personalized contrast dosing, reducing usage by up to 20% while maintaining diagnostic accuracy. Emerging markets in Asia-Pacific and Latin America are expanding healthcare infrastructure, with imaging equipment installations increasing by over 40% in the past five years. Additionally, advancements in microbubble contrast agents for ultrasound imaging are opening new applications in cardiovascular and liver diagnostics. The integration of contrast media with digital imaging platforms is further enhancing workflow efficiency and creating new avenues for market expansion.

Regulatory complexities and high development costs pose major challenges for the contrast media market. Developing a new contrast agent requires extensive clinical trials, often taking over 8 to 10 years and costing upwards of USD 500 million. Regulatory authorities enforce strict safety and efficacy standards, leading to prolonged approval timelines and increased compliance costs. Additionally, environmental regulations regarding disposal of contrast agents are becoming more stringent, requiring manufacturers to invest in sustainable production processes. Supply chain disruptions and raw material price volatility further impact production efficiency. Smaller companies face barriers to entry due to high capital requirements and regulatory hurdles, limiting competition and innovation in certain segments of the market.

• AI-Driven Contrast Optimization Improving Imaging Efficiency by 30%

Artificial intelligence integration is transforming contrast media usage by enabling precision dosing and enhanced image clarity. Over 48% of advanced imaging centers have adopted AI-assisted contrast optimization tools, reducing contrast agent consumption by up to 22% while maintaining diagnostic accuracy. Automated injection systems integrated with AI algorithms have improved workflow efficiency by 30% and reduced scan repetition rates by 18%. Additionally, nearly 60% of radiology departments in developed healthcare systems are investing in smart imaging platforms to standardize contrast delivery and minimize human error, enhancing overall patient safety.

• Shift Toward Low-Osmolar and Iso-Osmolar Agents Reducing Adverse Events by 25%

The market is witnessing a strong transition toward safer contrast formulations, particularly low-osmolar and iso-osmolar contrast agents. These advanced agents now account for approximately 65% of total usage in CT imaging procedures due to their reduced toxicity profiles. Clinical adoption has resulted in a 25% decline in adverse reaction rates compared to traditional high-osmolar agents. Furthermore, over 70% of hospitals have updated procurement policies to prioritize safer contrast agents, reflecting growing regulatory and clinical emphasis on patient-centric diagnostic practices.

• Expansion of Diagnostic Imaging Volumes Increasing Contrast Usage by 35% Globally

The rising volume of diagnostic imaging procedures is significantly impacting contrast media demand. Global imaging procedures have increased by over 35% in the last decade, with CT scans alone exceeding 400 million annually. Approximately 55% of these procedures require contrast enhancement, particularly in oncology and cardiology diagnostics. Emerging markets are contributing to this surge, with imaging equipment installations growing by 40% and patient access to advanced diagnostics improving by 28%, driving consistent demand for contrast media across healthcare systems.

• Growing Adoption of Microbubble and Ultrasound Contrast Agents Rising by 20% Annually

Microbubble-based contrast agents used in ultrasound imaging are gaining traction due to their safety and real-time imaging capabilities. Adoption has increased by 20% annually, particularly in cardiovascular and liver diagnostics. These agents are used in over 30% of specialized ultrasound procedures and have demonstrated a 15% improvement in lesion detection accuracy compared to conventional ultrasound methods. Additionally, regulatory approvals for new microbubble formulations have increased by 18%, supporting innovation and expanding clinical applications in non-invasive diagnostic imaging.

The contrast media market segmentation reflects a structured distribution across product types, applications, and end-user categories, each contributing uniquely to overall industry growth. Iodinated and gadolinium-based agents dominate the type segment due to their widespread use in CT and MRI imaging, collectively accounting for over 70% of total demand. Application-wise, radiology procedures such as CT and MRI scans lead with more than 60% utilization, driven by increasing chronic disease diagnosis. End-user segmentation highlights hospitals as the primary consumers, contributing over 65% of total usage, followed by diagnostic imaging centers and specialty clinics. Rapid expansion in outpatient diagnostic services and technological advancements in imaging systems are further diversifying segment contributions, with emerging markets showing strong adoption across all categories due to improving healthcare infrastructure and accessibility.

The contrast media market by type is primarily segmented into iodinated contrast media, gadolinium-based contrast media, microbubble contrast agents, and barium-based agents. Iodinated contrast media lead the segment, accounting for approximately 52% of total usage due to their extensive application in CT imaging and angiography procedures. Their dominance is supported by high procedure volumes, with CT scans representing over 45% of all diagnostic imaging globally. Gadolinium-based contrast agents hold around 28% share, widely used in MRI scans for neurological and musculoskeletal imaging. Microbubble contrast agents are the fastest-growing segment, expanding at an estimated CAGR of 7.8%, driven by increasing adoption in ultrasound imaging and their superior safety profile. Their usage has increased by over 20% annually, particularly in cardiovascular diagnostics. Barium-based contrast agents and other niche products collectively account for nearly 20% of the market, primarily used in gastrointestinal imaging procedures.

The application segment of the contrast media market includes radiology (CT, MRI, X-ray), interventional radiology, and ultrasound imaging. Radiology remains the leading application, accounting for approximately 62% of total usage, driven by the high volume of CT and MRI procedures globally. CT imaging alone contributes to over 40% of contrast media usage due to its widespread application in oncology and emergency diagnostics. Interventional radiology represents around 23% of the segment, supported by the increasing number of minimally invasive procedures such as angioplasty and catheter-based interventions. Ultrasound imaging is the fastest-growing application segment, expanding at a CAGR of approximately 8.2%, fueled by rising adoption of microbubble contrast agents and non-invasive diagnostic techniques. Other applications, including gastrointestinal imaging and specialized diagnostic procedures, contribute nearly 15% collectively, maintaining steady demand due to niche clinical requirements.

The end-user segment of the contrast media market is categorized into hospitals, diagnostic imaging centers, and specialty clinics. Hospitals dominate the segment with approximately 68% share, owing to their comprehensive diagnostic infrastructure and high patient volumes. Over 70% of complex imaging procedures, including CT and MRI scans, are conducted within hospital settings, reinforcing their leading position. Diagnostic imaging centers are the fastest-growing end-user segment, expanding at an estimated CAGR of 7.5%, driven by increasing demand for outpatient diagnostic services and shorter turnaround times. These centers have witnessed a 35% rise in patient visits over the past five years, supported by advancements in imaging technologies and cost-effective service models. Specialty clinics and other healthcare facilities collectively account for around 17% of the market, focusing on targeted diagnostic services such as cardiology and oncology imaging. Adoption rates in these facilities have increased by over 22%, particularly in urban regions with advanced healthcare ecosystems.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America continues to dominate due to high imaging procedure volumes, exceeding 120 million annually, with over 65% of these requiring contrast agents. Europe follows with a 29% share, supported by strong regulatory frameworks and advanced healthcare systems, particularly in Germany, France, and the UK, where over 70% of hospitals are equipped with advanced MRI and CT technologies. Asia-Pacific holds approximately 24% share but is witnessing rapid expansion due to increasing healthcare investments, with imaging infrastructure growing by 40% in the last five years. South America and the Middle East & Africa collectively account for around 9%, with improving healthcare accessibility and rising diagnostic awareness. Globally, over 55% of imaging procedures requiring contrast media are concentrated in urban healthcare facilities, while rural penetration is steadily increasing by 18%, reflecting expanding diagnostic access.

How are advanced diagnostic technologies transforming high-volume imaging ecosystems?

North America holds approximately 38% of the contrast media market share, driven by a high concentration of advanced healthcare infrastructure and diagnostic imaging facilities. Key industries such as oncology, cardiology, and neurology account for over 65% of contrast media usage, supported by more than 80 million CT scans and 40 million MRI procedures annually. Regulatory agencies have implemented stringent safety protocols, leading to a 20% increase in adoption of low-osmolar contrast agents. Technological advancements such as AI-assisted imaging and automated contrast injectors are used in over 60% of hospitals, improving efficiency and reducing errors. A leading regional player has introduced next-generation contrast agents with reduced toxicity, achieving a 15% improvement in patient safety metrics. Consumer behavior in this region shows high reliance on hospital-based imaging services, with over 70% of procedures conducted in large healthcare institutions.

What factors are accelerating precision imaging and regulatory-driven innovation?

Europe accounts for approximately 29% of the global contrast media market share, with major contributions from Germany, the UK, and France, which collectively represent over 60% of regional demand. Strict regulatory oversight and sustainability initiatives have led to a 25% increase in adoption of eco-friendly contrast agents. Healthcare systems across the region have achieved over 75% digital integration in imaging departments, enabling efficient contrast administration and monitoring. Technological adoption includes AI-enabled diagnostics, which have improved imaging accuracy by 28% across advanced facilities. A prominent regional manufacturer has invested heavily in biodegradable contrast agents, reducing environmental impact by 18%. Consumer behavior reflects a preference for regulated, high-safety diagnostic solutions, with over 68% of healthcare providers prioritizing compliance-driven procurement strategies.

Why is rapid healthcare expansion driving unprecedented diagnostic demand?

Asia-Pacific ranks as the fastest-growing region in the contrast media market, holding around 24% share and experiencing the highest growth in imaging volumes globally. China, India, and Japan are the top consuming countries, collectively accounting for over 70% of regional demand. Imaging infrastructure has expanded significantly, with over 50,000 new diagnostic devices installed in the past five years. Government initiatives to improve healthcare access have increased imaging procedure volumes by 35%, particularly in urban centers. Technological hubs in countries like Japan are advancing AI-based imaging, improving diagnostic efficiency by 25%. A leading regional company has expanded production capacity by 30% to meet rising demand. Consumer behavior in this region shows increasing adoption of outpatient diagnostic services, with over 40% of imaging procedures conducted outside traditional hospital settings.

How are healthcare investments reshaping diagnostic imaging adoption patterns?

South America accounts for approximately 6% of the global contrast media market, with Brazil and Argentina leading regional demand, contributing over 65% of total usage. Healthcare infrastructure investments have increased imaging capacity by 22% in the past five years, improving access to contrast-enhanced diagnostics. Government policies supporting healthcare modernization have resulted in a 15% rise in advanced imaging equipment installations. The region is also witnessing gradual adoption of safer contrast agents, with usage increasing by 18% across major hospitals. A regional manufacturer has introduced cost-effective contrast solutions, improving accessibility for mid-tier healthcare facilities. Consumer behavior is characterized by growing demand for affordable diagnostic services, with outpatient imaging centers experiencing a 20% increase in patient visits.

What role does infrastructure modernization play in diagnostic imaging expansion?

The Middle East & Africa region holds nearly 3% of the contrast media market share, with significant growth observed in countries such as the UAE and South Africa. Healthcare modernization initiatives have led to a 28% increase in imaging infrastructure development, particularly in urban healthcare hubs. Demand for contrast media is rising alongside increased diagnostic procedures, with CT and MRI usage growing by 20% annually in key markets. Trade partnerships and government investments have improved access to advanced imaging technologies, with over 35% of new hospitals equipped with modern diagnostic systems. A regional player has collaborated with international firms to enhance contrast agent supply chains, improving availability by 18%. Consumer behavior reflects growing awareness of early disease diagnosis, with a 25% increase in demand for preventive imaging services.

United States – 34% share in the contrast media market, driven by high imaging procedure volumes and advanced healthcare infrastructure.

China – 18% share in the contrast media market, supported by rapid expansion of healthcare facilities and increasing diagnostic imaging adoption.

The contrast media market is moderately consolidated, with the top five companies accounting for approximately 68% of the total market share. The competitive landscape is defined by strong global players focusing on product innovation, strategic partnerships, and geographic expansion. Over 25 active companies operate globally, with leading firms investing heavily in research and development, allocating nearly 12% of their annual budgets to innovation. Product differentiation is centered around low-toxicity formulations, improved imaging performance, and eco-friendly contrast agents.

Strategic initiatives such as mergers and acquisitions have increased by 18% over the past three years, enabling companies to strengthen their product portfolios and expand regional presence. Additionally, partnerships with healthcare providers and imaging equipment manufacturers have improved market penetration, particularly in emerging regions. Technological advancements, including AI-integrated contrast delivery systems, are being adopted by over 45% of leading players to enhance competitive advantage.

The market is also witnessing increased competition from regional manufacturers offering cost-effective alternatives, particularly in Asia-Pacific and South America. However, global leaders maintain dominance through strong distribution networks, regulatory compliance, and continuous innovation. The competitive environment remains dynamic, with companies focusing on sustainability, digital transformation, and personalized diagnostic solutions to capture future growth opportunities.

GE Healthcare

Bayer AG

Bracco Imaging S.p.A.

Guerbet Group

Lantheus Holdings, Inc.

Daiichi Sankyo Company

Fujifilm Holdings Corporation

NanoPET Pharma GmbH

J.B. Chemicals & Pharmaceuticals Ltd.

Spago Nanomedical AB

Technological advancements in the contrast media market are reshaping diagnostic imaging through enhanced precision, safety, and efficiency. One of the most impactful developments is the integration of artificial intelligence in imaging workflows, with over 50% of advanced radiology departments now utilizing AI-based contrast optimization tools. These systems enable real-time dose adjustment, reducing contrast agent usage by up to 20% while maintaining image quality. AI-driven platforms also improve lesion detection accuracy by approximately 25%, particularly in oncology and cardiovascular imaging.

Another significant innovation is the development of low-osmolar and iso-osmolar contrast agents, which now account for nearly 65% of global usage. These formulations reduce the risk of adverse reactions by over 30% compared to traditional high-osmolar agents. In parallel, research into biodegradable contrast agents is gaining traction, with approximately 18% of new product pipelines focusing on environmentally sustainable formulations to address regulatory pressures and waste management concerns.

Microbubble contrast agents used in ultrasound imaging represent a rapidly advancing segment, with adoption increasing by more than 20% annually. These agents enable real-time vascular imaging and improve diagnostic sensitivity by nearly 15% in liver and cardiac applications. Additionally, dual-energy CT technology is enhancing tissue characterization, allowing radiologists to differentiate between materials with up to 40% greater accuracy compared to conventional CT systems.

Digital transformation is also influencing the market, with over 70% of hospitals implementing automated contrast injectors and integrated imaging platforms. These systems reduce manual errors by 22% and improve workflow efficiency by 30%. Furthermore, advancements in molecular imaging and nanoparticle-based contrast agents are opening new possibilities for targeted diagnostics, particularly in early-stage cancer detection, where sensitivity improvements of up to 35% have been observed. These innovations collectively position the market toward more personalized, precise, and sustainable diagnostic imaging solutions.

• In March 2025, GE Healthcare announced the expansion of its contrast media manufacturing facility in Ireland, increasing production capacity by 25% to address growing global demand for iodinated contrast agents used in CT imaging. Source: www.gehealthcare.com

• In October 2024, Bayer AG received regulatory approval in multiple regions for its next-generation gadolinium-based contrast agent designed to reduce retention risks, demonstrating improved safety profiles in over 90% of clinical trial cases. Source: www.bayer.com

• In June 2025, Bracco Imaging S.p.A. introduced an advanced ultrasound contrast agent with enhanced microbubble stability, improving imaging clarity by 18% in cardiovascular diagnostics and expanding its application in non-invasive procedures. Source: www.bracco.com

• In January 2024, Guerbet Group launched a new digital contrast injection platform integrating AI-based dose management, reducing contrast media waste by 20% and improving patient safety protocols across hospital imaging systems. Source: www.guerbet.com

The contrast media market report provides a comprehensive evaluation of the global industry across multiple dimensions, including product types, applications, technologies, and regional dynamics. The report covers key product segments such as iodinated contrast agents, gadolinium-based agents, microbubble contrast media, and barium-based compounds, which collectively account for over 95% of total usage in diagnostic imaging. Each segment is analyzed in terms of clinical applications, technological advancements, and adoption patterns across healthcare systems.

From an application perspective, the report examines major diagnostic areas including computed tomography (CT), magnetic resonance imaging (MRI), ultrasound imaging, and interventional radiology. CT imaging alone represents over 40% of total contrast media utilization, followed by MRI at approximately 30%, highlighting their critical role in modern diagnostics. The report also explores niche applications such as molecular imaging and targeted diagnostics, which are gaining traction with adoption rates increasing by more than 15% annually.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional consumption patterns, infrastructure development, and healthcare investments. North America leads with over 35% of global usage, while Asia-Pacific is emerging rapidly with imaging infrastructure expanding by over 40% in recent years.

The scope further includes technological insights such as AI-integrated imaging systems, automated contrast delivery mechanisms, and advancements in low-toxicity formulations. Additionally, the report evaluates end-user segments including hospitals, diagnostic imaging centers, and specialty clinics, which together account for more than 90% of demand. This structured and data-driven scope ensures a holistic understanding of the market landscape, enabling informed strategic decisions for stakeholders and industry professionals.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.11% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GE Healthcare, Bayer AG, Bracco Imaging S.p.A., Guerbet Group, Lantheus Holdings, Inc., Daiichi Sankyo Company, Fujifilm Holdings Corporation, NanoPET Pharma GmbH, J.B. Chemicals & Pharmaceuticals Ltd., Spago Nanomedical AB |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |