Reports

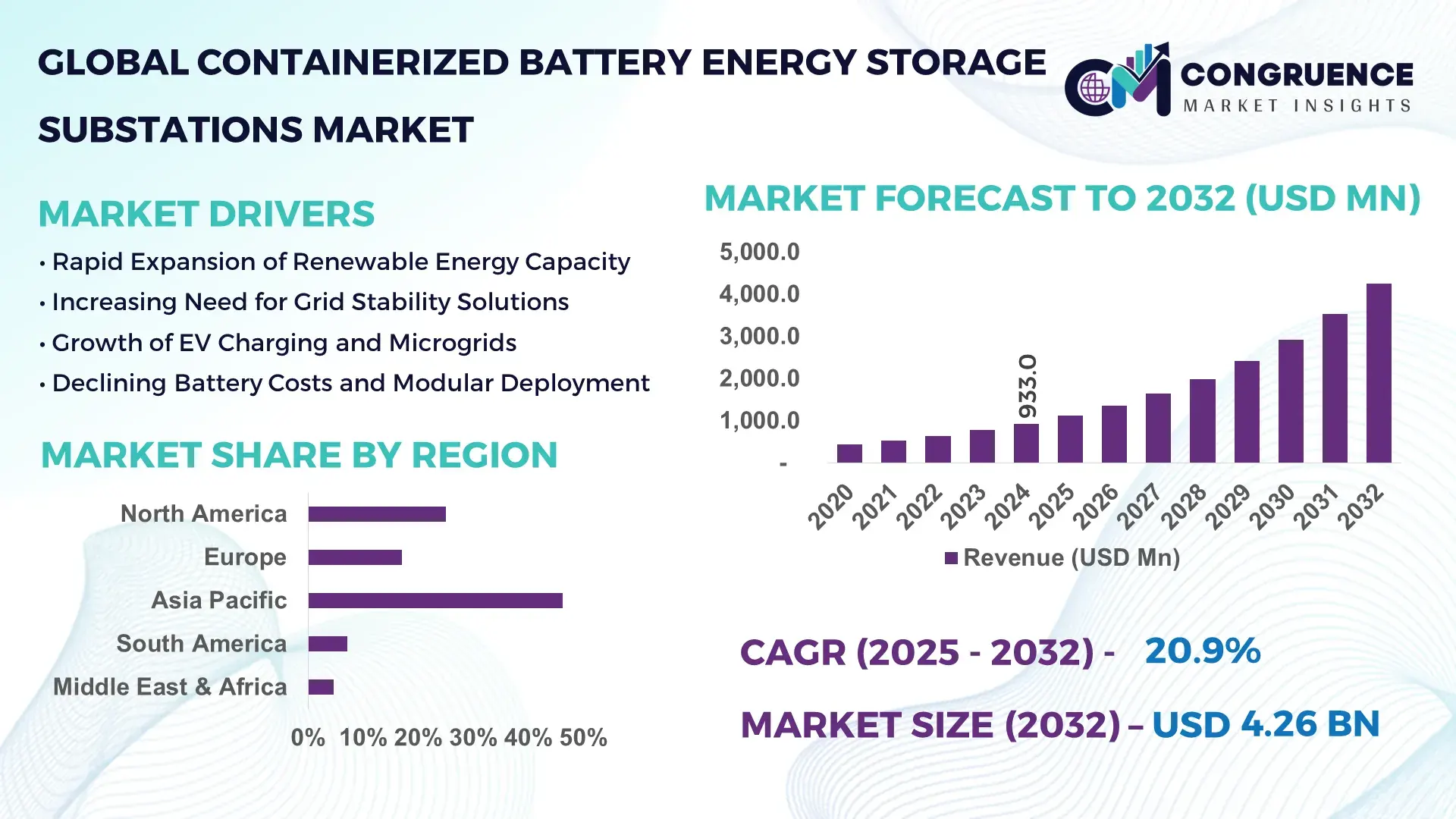

The Global Containerized Battery Energy Storage Substations Market was valued at USD 933.0 Million in 2024 and is anticipated to reach a value of USD 4,258.8 Million by 2032 expanding at a CAGR of 20.9% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily supported by the rapid integration of renewable energy assets with grid-scale storage solutions to enhance grid stability and peak-load management.

China dominates the global Containerized Battery Energy Storage Substations Market through large-scale manufacturing capacity, accelerated infrastructure investment, and deployment across utility-scale and industrial applications. The country accounts for over 60% of global lithium-ion battery production capacity, exceeding 2,000 GWh annually, which directly supports domestic containerized substation deployment. In 2024, China commissioned more than 45 GW of grid-connected energy storage projects, with containerized substations widely used in renewable parks, EV charging hubs, and industrial microgrids. State-owned utilities and private developers invested over USD 35 billion in energy storage-linked grid infrastructure, while advanced battery management systems and high-voltage containerized designs enabled operational efficiencies exceeding 92% system availability.

Market Size & Growth: Valued at USD 933.0 Million in 2024, projected to reach USD 4,258.8 Million by 2032, expanding at a CAGR of 20.9%, driven by grid-scale renewable integration and peak-demand balancing needs.

Top Growth Drivers: Renewable energy integration (48%), grid reliability improvement initiatives (32%), and industrial energy optimization adoption (27%).

Short-Term Forecast: By 2028, standardized container designs are expected to reduce deployment timelines by 35% while lowering installation costs by 22%.

Emerging Technologies: AI-enabled battery management systems, liquid-cooled container architectures, and high-voltage DC containerized substations.

Regional Leaders: Asia Pacific (USD 1,980 Million by 2032, utility-scale renewables), North America (USD 1,120 Million, data center and EV infrastructure), Europe (USD 860 Million, grid modernization).

Consumer/End-User Trends: Utilities account for nearly 52% adoption, followed by industrial users at 28% and commercial microgrids at 20%.

Pilot or Case Example: In 2023, a 200 MWh containerized storage substation project in Australia improved grid response times by 41%.

Competitive Landscape: CATL leads with ~21% share, followed by BYD, Tesla Energy, Siemens Energy, and Hitachi Energy.

Regulatory & ESG Impact: Net-zero grid mandates and storage incentives support 30–40% faster project approvals in key markets.

Investment & Funding Patterns: Over USD 52 billion invested globally in containerized storage-linked grid assets since 2022.

Innovation & Future Outlook: Hybrid battery–supercapacitor systems and AI-driven predictive maintenance will shape next-generation deployments.

The Containerized Battery Energy Storage Substations Market is increasingly influenced by utilities (52%), renewable developers (31%), and industrial users (17%), with lithium-ion systems dominating installations. Recent innovations include liquid-cooled containers improving thermal efficiency by 18%, while grid codes and decarbonization mandates accelerate adoption in Asia Pacific and Europe. Rising electrification and distributed energy resources position the market for sustained expansion.

The Containerized Battery Energy Storage Substations Market holds strategic relevance as power systems transition toward decentralized, renewable-driven architectures. These substations enable rapid deployment of grid-scale storage, supporting frequency regulation, peak shaving, and energy arbitrage across utility, industrial, and commercial networks. Advanced lithium-ion containerized substations now deliver up to 30% higher energy density compared to conventional stationary battery rooms, enabling compact installations in space-constrained environments.

From a technology standpoint, AI-enabled battery management systems deliver 22% improvement in predictive fault detection compared to legacy rule-based monitoring standards. Asia Pacific dominates in deployment volume, while North America leads in adoption intensity, with nearly 38% of utilities integrating containerized storage into grid resilience programs. By 2027, AI-driven optimization is expected to cut operational downtime by 28% through real-time performance analytics and automated load balancing.

Compliance and ESG considerations further strengthen strategic relevance. Utilities are committing to lifecycle sustainability metrics, including 45% battery material recycling by 2030, aligning with circular economy mandates. In 2024, Germany achieved a 19% reduction in grid congestion costs through AI-coordinated containerized storage deployments across transmission substations. Looking forward, the Containerized Battery Energy Storage Substations Market will serve as a cornerstone of grid resilience, regulatory compliance, and long-term sustainable energy growth.

The Containerized Battery Energy Storage Substations Market dynamics are shaped by accelerating renewable penetration, grid modernization initiatives, and rising demand for flexible energy infrastructure. Utilities increasingly deploy containerized substations to support intermittent solar and wind assets, enabling rapid scalability and standardized installation. Industrial users adopt these systems to stabilize power quality and reduce dependence on diesel backup generation. Technological progress in battery chemistry, thermal management, and digital monitoring enhances system reliability and safety. However, supply chain concentration and evolving grid interconnection standards continue to influence procurement strategies and deployment timelines.

The rapid expansion of renewable energy capacity is a primary driver of the Containerized Battery Energy Storage Substations Market. In 2024, renewables contributed over 30% of global electricity generation, increasing grid volatility due to intermittent output. Containerized substations provide fast-response storage solutions capable of stabilizing frequency within milliseconds. Grid operators deploying storage-backed substations recorded up to 40% reduction in curtailment losses and 25% improvement in load balancing efficiency. Utility-scale solar and wind parks increasingly mandate co-located containerized storage to meet grid code compliance and enhance dispatch flexibility.

Despite operational advantages, high upfront costs restrain broader adoption of containerized battery energy storage substations. Advanced battery modules, fire suppression systems, and grid-grade power electronics elevate capital requirements by 30–45% compared to traditional substations. Additionally, compliance with evolving safety and interconnection standards increases engineering and certification costs. Smaller utilities and industrial users often delay adoption due to limited access to long-term financing and uncertainty around battery lifecycle replacement expenses.

Grid digitalization presents significant opportunities for the Containerized Battery Energy Storage Substations Market. The integration of AI, IoT sensors, and cloud-based energy management platforms enables real-time monitoring and predictive maintenance, reducing failure risks by up to 35%. Emerging smart grid programs across Asia Pacific and Europe prioritize digitally enabled substations capable of autonomous dispatch and self-diagnostics. These advancements open opportunities for premium solutions tailored to utilities pursuing fully automated grid operations.

Regulatory fragmentation and safety compliance pose persistent challenges. Fire safety standards, grid interconnection rules, and environmental permitting vary widely across regions, complicating standardized product deployment. In 2024, over 20% of planned projects faced commissioning delays due to evolving battery safety codes. Manufacturers must continuously redesign container architectures to meet regional compliance, increasing engineering complexity and time-to-market pressures.

Modular and Prefabricated Deployment Acceleration: Modular containerized substations now represent nearly 55% of new installations, reducing on-site construction time by 40% and lowering labor requirements by 32%. Utilities benefit from faster grid connection and predictable commissioning schedules.

Advanced Thermal and Fire Safety Systems: Liquid cooling and multi-layer fire suppression adoption increased by 46% in 2024, improving battery lifespan by 18% and reducing thermal runaway incidents by over 50%. These enhancements are becoming mandatory for high-density deployments.

AI-Driven Energy Management Integration: Over 37% of newly deployed containerized substations integrate AI-based control software, improving charge–discharge efficiency by 21% and enabling autonomous grid response during peak demand events.

Expansion into Industrial and EV Infrastructure: Industrial facilities and EV fast-charging hubs account for 29% of new deployments, with containerized substations improving power availability by 34% and reducing reliance on diesel backup systems by 41%.

The Containerized Battery Energy Storage Substations Market is segmented by type, application, and end-user, reflecting diverse deployment requirements across grid infrastructure, industrial energy systems, and emerging distributed energy models. By type, segmentation is influenced by battery chemistry, voltage configuration, and cooling architecture, each aligned with specific performance, safety, and lifecycle expectations. Application-based segmentation highlights the dominant role of utility-scale grid support, alongside rapidly growing use in renewable integration and electric mobility infrastructure. End-user segmentation further underscores how utilities, industrial operators, and commercial energy consumers adopt containerized substations differently based on load criticality, regulatory obligations, and energy optimization goals. Across segments, standardization, modularity, and digital integration remain common decision criteria, while adoption intensity varies by operational scale, grid complexity, and decarbonization targets.

The market by type is primarily categorized into lithium-ion battery-based containerized substations, flow battery-based containerized substations, and hybrid or alternative chemistry systems. Lithium-ion containerized battery energy storage substations represent the leading type, accounting for approximately 68% of total installations. Their dominance is supported by high energy density, fast response times below 100 milliseconds, and mature supply chains that enable standardized container designs for utility and industrial use. Flow battery-based containerized substations account for nearly 18%, favored in long-duration storage applications exceeding 6 hours due to extended cycle life and reduced degradation. However, adoption in hybrid and advanced chemistry containerized systems—including sodium-ion and lithium iron phosphate configurations—is rising fastest, expanding at an estimated 24% CAGR, driven by improved safety profiles and lower critical mineral dependency. These emerging systems currently contribute a combined 14% share but are gaining traction in regions prioritizing grid resilience and lifecycle sustainability.

By application, grid stabilization and utility-scale energy storage is the leading segment, accounting for approximately 49% of total deployment. Containerized battery energy storage substations are extensively used for frequency regulation, peak shaving, and reserve capacity in transmission and distribution networks. Renewable energy integration follows with 27% adoption, as solar and wind projects increasingly deploy co-located containerized substations to mitigate intermittency and reduce curtailment. However, electric vehicle charging infrastructure and industrial microgrids represent the fastest-growing application area, expanding at an estimated 26% CAGR, supported by rapid electrification and the need for high-power, fast-response energy buffering. Other applications—including data centers, commercial buildings, and remote off-grid systems—collectively account for the remaining 24%. From an adoption perspective, in 2024, over 41% of utilities globally reported piloting containerized battery energy storage substations for grid flexibility programs, while nearly 36% of industrial energy users integrated storage-backed substations to improve power quality and reduce downtime.

End-user segmentation highlights utilities as the leading adopters, representing approximately 52% of total demand. Utilities prioritize containerized battery energy storage substations for grid resilience, deferred infrastructure upgrades, and compliance with renewable integration mandates. Industrial and manufacturing users account for around 29%, leveraging these systems to stabilize mission-critical operations, reduce voltage fluctuations, and support behind-the-meter energy optimization. However, commercial and infrastructure operators—including data centers, transport authorities, and large commercial campuses—form the fastest-growing end-user group, expanding at an estimated 23% CAGR, driven by digital infrastructure expansion and electrified transport systems. These and other smaller end-users collectively contribute the remaining 19%. In terms of adoption trends, more than 34% of global industrial enterprises reported deploying or testing containerized battery energy storage substations to enhance power reliability, while nearly 28% of data center operators integrated on-site containerized substations to support load balancing and backup power strategies.

Asia-Pacific accounted for the largest market share at 46.2% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 22.4% between 2025 and 2032.

Asia-Pacific’s leadership is supported by high deployment volumes exceeding 45 GW of grid-connected energy storage systems, extensive battery manufacturing capacity above 2,000 GWh, and large-scale renewable integration projects. North America’s accelerated growth outlook reflects rising grid congestion events, more than 38% increase in utility-scale storage interconnection requests, and rapid expansion of EV fast-charging and data center infrastructure. Europe held approximately 28.5% market share, driven by grid modernization and energy security initiatives, while South America and the Middle East & Africa collectively contributed nearly 12%, supported by emerging renewable investments, mining electrification, and industrial microgrid deployment. Regional variations in policy frameworks, grid stability requirements, and energy transition maturity continue to shape demand patterns globally.

North America accounted for approximately 31.4% of the global Containerized Battery Energy Storage Substations Market in 2024, supported by high deployment intensity across the United States and Canada. Utilities, data centers, EV charging networks, and critical infrastructure operators are the primary demand drivers, with utilities alone representing over 44% of regional installations. Federal and state-level grid resilience programs, investment tax credits, and capacity market incentives have accelerated project approvals. Technological advancements include AI-enabled energy management platforms and liquid-cooled containerized substations, improving system uptime by over 20%. A leading regional energy solutions provider expanded standardized 20-foot and 40-foot containerized substations to support multi-MWh installations for grid balancing. Consumer behavior shows higher enterprise adoption in energy-intensive sectors, with more than 40% of large enterprises integrating on-site storage to mitigate outage risks.

Europe represented around 28.5% of the global market in 2024, with Germany, the United Kingdom, and France collectively accounting for over 62% of regional demand. Strong regulatory oversight, grid decarbonization targets, and energy security strategies are driving adoption. National transmission operators increasingly deploy containerized substations for frequency regulation and cross-border power balancing. Emerging technologies such as digital substations, advanced fire suppression systems, and recyclable battery modules are gaining traction. A major European grid equipment manufacturer introduced modular containerized substations designed for rapid deployment at renewable parks. Regional consumer behavior reflects regulatory pressure, with utilities prioritizing compliant, low-risk storage systems aligned with environmental and safety standards.

Asia-Pacific ranked first globally by deployment volume, accounting for approximately 46.2% of total installations in 2024. China, India, and Japan are the top consuming countries, together representing more than 75% of regional demand. Infrastructure expansion, domestic battery manufacturing, and large renewable capacity additions exceeding 300 GW annually underpin growth. Manufacturing trends include vertically integrated battery-to-substation production and localized power electronics supply chains. Regional innovation hubs focus on high-voltage containerized substations and AI-based battery optimization. A major regional manufacturer scaled standardized containerized substations for solar-plus-storage projects exceeding 500 MWh capacity. Consumer behavior shows adoption driven by rapid urbanization, industrial electrification, and distributed energy systems.

South America held approximately 7.1% of the global market in 2024, led by Brazil and Argentina. The region’s demand is closely tied to renewable energy integration, particularly solar and wind, which account for over 65% of new power capacity additions. Grid constraints and long transmission distances increase the need for localized containerized storage substations. Government incentives supporting renewable-plus-storage projects and reduced import duties on energy equipment have improved adoption. A regional energy developer deployed containerized substations to stabilize wind farms exceeding 300 MW capacity. Consumer behavior reflects utility-driven demand, with increasing interest from mining and industrial operators seeking reliable off-grid power solutions.

The Middle East & Africa region accounted for nearly 4.8% of global demand in 2024, with the UAE, Saudi Arabia, and South Africa as key growth countries. Demand is driven by energy diversification strategies, large-scale solar projects, and power reliability requirements in oil & gas, construction, and mining sectors. Technological modernization includes hybrid battery-diesel containerized substations and high-temperature-resistant designs. Regulatory frameworks increasingly support energy storage integration within national grid plans. A regional utility deployed containerized substations at desert solar facilities to improve peak load response by over 30%. Consumer behavior varies, with industrial users prioritizing resilience and utilities focusing on renewable integration.

China – 34.8% Market Share: High battery production capacity, large-scale renewable integration, and extensive grid infrastructure investments drive dominance in the Containerized Battery Energy Storage Substations Market.

United States – 22.6% Market Share: Strong utility-scale storage deployment, supportive grid resilience programs, and rapid expansion of EV and data center infrastructure underpin leadership in the Containerized Battery Energy Storage Substations Market.

The Containerized Battery Energy Storage Substations Market exhibits a moderately consolidated competitive structure, characterized by the presence of large multinational energy technology providers alongside specialized battery and power electronics manufacturers. More than 45 active global and regional competitors operate in this market, competing on system efficiency, safety compliance, scalability, and digital integration capabilities. The top five companies collectively account for approximately 52–55% of total deployments, indicating strong concentration at the upper tier while leaving room for regional and niche innovators.

Competitive positioning is strongly influenced by vertical integration across battery manufacturing, power conversion systems, and digital energy management platforms. Leading players focus on standardized 20-foot and 40-foot containerized designs, high-voltage architectures above 1,500 V, and advanced thermal and fire suppression systems to differentiate offerings. Strategic initiatives include long-term supply agreements with utilities, partnerships with renewable developers, and localized manufacturing expansion to reduce delivery timelines by 20–30%. Product innovation remains intense, with over 60% of major players introducing upgraded containerized substation platforms featuring AI-enabled monitoring, predictive maintenance, and remote commissioning. Mergers, technology licensing, and joint ventures—particularly between battery manufacturers and grid equipment suppliers—continue to shape competitive dynamics and accelerate global market penetration.

Siemens Energy

Hitachi Energy

ABB

Schneider Electric

Eaton

Sungrow Power Supply

Fluence Energy

Technology evolution is central to value creation in the Containerized Battery Energy Storage Substations Market. Modern systems increasingly adopt high-voltage DC architectures exceeding 1,500 V, enabling up to 8–12% reduction in conversion losses compared to legacy configurations. Battery chemistry advancements, particularly lithium iron phosphate and sodium-ion variants, improve safety margins while supporting cycle life beyond 7,000–8,000 cycles under grid-duty conditions.

Thermal management has become a key innovation area. Liquid cooling systems now support energy densities above 280 Wh/kg, improving footprint efficiency by nearly 20%. Integrated multi-layer fire suppression, gas detection, and compartmentalized container designs significantly enhance compliance with evolving safety standards. Digitalization is another defining trend, with AI-driven battery management systems delivering 20–25% improvement in fault prediction accuracy and enabling real-time optimization across distributed substations.

Power electronics are also advancing, as silicon carbide-based inverters increase switching efficiency and reduce system losses by up to 30%. Additionally, plug-and-play modular substations allow parallel scaling beyond 500 MWh capacity with minimal on-site engineering. These technologies collectively improve reliability, lifecycle performance, and operational transparency, making containerized battery energy storage substations a cornerstone of next-generation grid infrastructure.

In May 2025, Contemporary Amperex Technology Co., Limited (CATL) launched the TENER Stack, the world’s first 9 MWh ultra-large capacity energy storage system, designed for high-density and transportable containerized storage applications to meet rising demand from utilities, industrial users, and data centers. Source: www.prnewswire.com

In September 2024, Honeywell commissioned a 1.4 MWh microgrid battery energy storage system (BESS) in India’s Lakshadweep Islands, integrating advanced energy management and microgrid control capabilities to decarbonize the remote archipelago’s grid and support renewable energy distribution. Source: www.honeywell.com

On May 28, 2024, Vilion’s EnerCube containerized battery energy storage system successfully completed Factory Acceptance Testing (FAT) and is set for shipment to a new customer. The EnerCube uses a standard 20HQ container design with flexible modular cabinet configuration, enabling on-site PV self-consumption, peak-load shifting, and on-grid operation for peak-to-valley price arbitrage. Source: www.szvilion.com

The Containerized Battery Energy Storage Substations Market Report provides comprehensive coverage of the global market landscape, encompassing technology types, applications, end-user industries, and regional deployment patterns. The scope includes analysis of battery-based containerized substations across multiple chemistries, voltage classes, cooling technologies, and digital control architectures. It evaluates applications ranging from grid stabilization and renewable integration to industrial microgrids, EV charging infrastructure, and critical commercial facilities.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional variations in infrastructure maturity, regulatory frameworks, and deployment intensity. The study further addresses industry participation across utilities, industrial operators, commercial infrastructure providers, and emerging distributed energy users. Technology coverage extends to AI-enabled battery management systems, advanced fire safety solutions, high-efficiency power electronics, and modular construction methodologies.

Additionally, the report examines competitive structure, innovation pathways, and evolving standards influencing system design and procurement decisions. By integrating quantitative deployment metrics with qualitative strategic insights, the report offers decision-makers a structured understanding of current capabilities, emerging opportunities, and long-term positioning within the Containerized Battery Energy Storage Substations Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 933.0 Million |

| Market Revenue (2032) | USD 4,258.8 Million |

| CAGR (2025–2032) | 20.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | CATL; BYD Energy Storage; Tesla Energy; Siemens Energy; Hitachi Energy; ABB; Honeywell; Schneider Electric; Eaton; Sungrow Power Supply; Vilion; Fluence Energy |

| Customization & Pricing | Available on Request (10% Customization Free) |