Reports

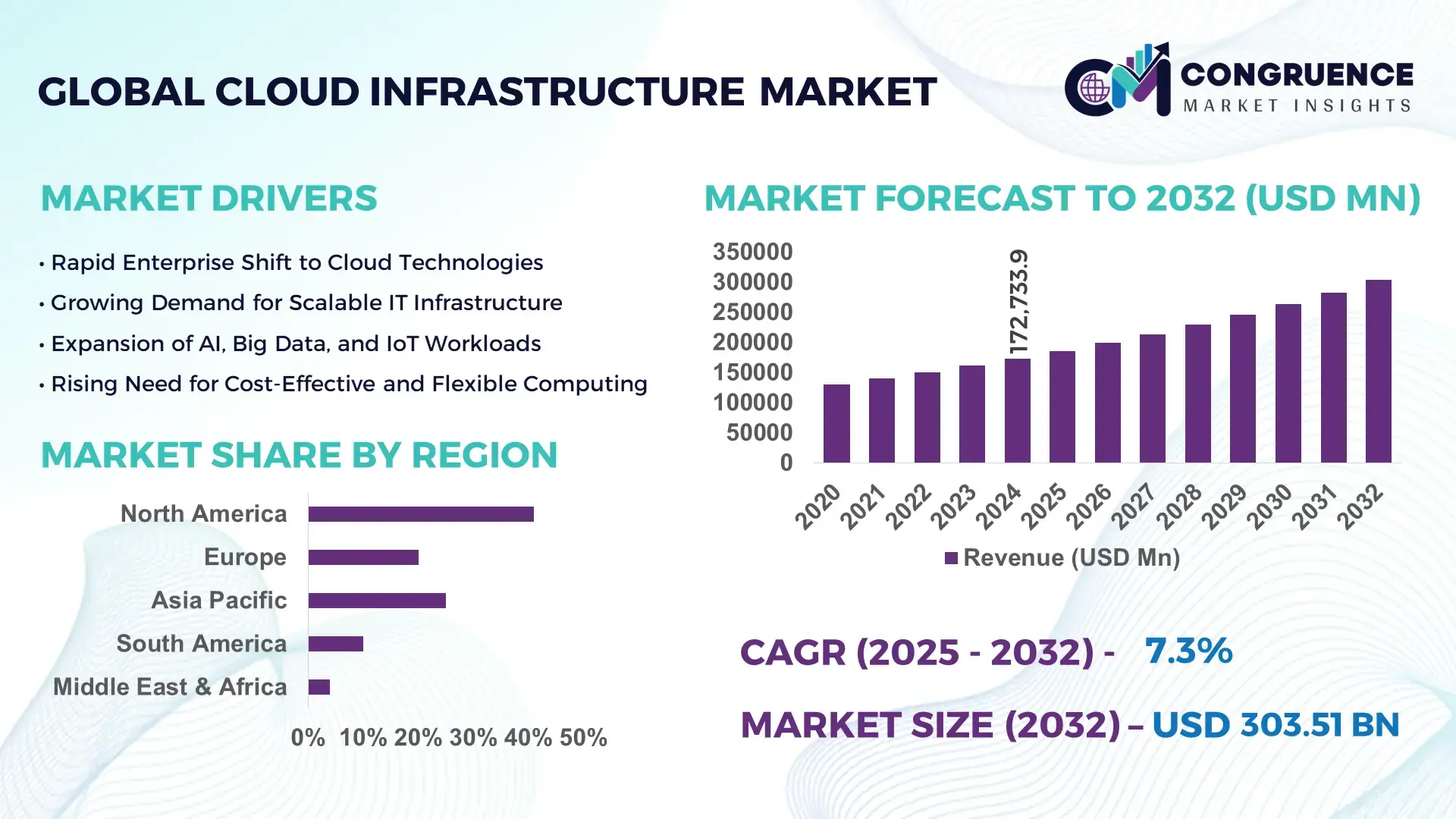

The Global Cloud Infrastructure Market was valued at USD 172733.88 Million in 2024 and is anticipated to reach a value of USD 303511.62 Million by 2032 expanding at a CAGR of 7.3% between 2025 and 2032. This growth is driven by increasing enterprise demand for scalable storage and computing resources and rising adoption of cloud-native technologies.

The United States continues to lead global cloud infrastructure capacity with massive investments in data‑center expansion and hyperscale deployments. In 2024 U.S. data‑center capacity exceeded 21,000 MW, driven by major hyperscale builds and enterprise cloud migrations, and investment in high‑performance computing, networking infrastructure, and renewable‑powered data centers has accelerated. Enterprises across IT, finance, healthcare, and retail in the U.S. are heavily adopting hybrid and multi‑cloud architectures, with compute‑and‑storage services being rapidly provisioned to support digital transformation, AI workloads, and large‑scale enterprise applications — reflecting advanced production capacity, robust investment levels and technological readiness.

Market Size & Growth: Global cloud infrastructure reached ~USD 172,734 Million in 2024 and is forecast to reach ~USD 303,512 Million by 2032 at a CAGR of 7.3%, propelled by surging demand for elastic compute and storage capacity.

Top Growth Drivers: rising hybrid cloud adoption (≈ 55%), surge in enterprise digital workloads (≈ 48%), increasing demand for scalable storage & compute (≈ 42%).

Short-Term Forecast (by 2028): cost reduction up to ~25% for enterprises migrating to cloud infrastructure; performance and provisioning speed improvements up to ~30%.

Emerging Technologies: integration of AI‑optimized infrastructure and high‑density GPU clusters; growth in edge computing and distributed cloud deployments; adoption of energy‑efficient and sustainable data center designs.

Regional Leaders by 2032: North America ~USD 135 Billion (sustained hyperscale growth), Asia‑Pacific ~USD 85 Billion (rapid digital adoption & cloud migration), Europe ~USD 60 Billion (hybrid cloud and regulatory‑driven upgrades).

Consumer/End-User Trends: major uptake in IT & telecom, BFSI, healthcare and retail sectors — driving hybrid cloud adoption, demand for low-latency access, and large-scale storage usage.

Pilot or Case Example: in 2026 several enterprises report up to 30% reduction in infrastructure downtime and 22% efficiency gains after migrating legacy systems to cloud‑based infrastructure.

Competitive Landscape: Market leader (approx. share ~40%) — major hyperscaler-based data‑center operators; other key competitors include large global cloud providers and regional data‑center firms vying for enterprise and regulated‑industry contracts.

Regulatory & ESG Impact: rising emphasis on data‑localization laws, data sovereignty regulations, and incentives for sustainable energy usage in data centers; environmental compliance promoting green‑powered infrastructure.

Investment & Funding Patterns: recent global investments exceeding tens of billions of USD, with growing participation from institutional investors, project financing for hyperscale builds, and rising venture funding for edge and AI‑ready infrastructures.

Innovation & Future Outlook: advancements in AI‑ready cloud infrastructure, expansion of multi‑cloud and hybrid‑cloud models, growth of edge data centers, and increasing integration with emerging technologies like 5G, IoT, and real‑time data analytics.

The cloud infrastructure market is witnessing transformation across major industry sectors including IT & telecommunications, healthcare, BFSI, retail, and manufacturing. Enterprises increasingly leverage hybrid and multi‑cloud deployments to support agile operations and elasticity. Recent innovations — such as AI‑ready GPU clusters, edge computing, and sustainable data‑center designs — are reshaping infrastructure priorities. Regulatory factors including data localization requirements and ESG mandates are encouraging adoption of environmentally‑compliant cloud deployments. Regional consumption patterns are shifting: developed markets maintain stable hyperscale growth, while emerging regions in Asia‑Pacific and parts of Europe see rapid adoption driven by digitalization and cloud migration. The trend toward distributed cloud architectures, edge computing, and integration with AI/IoT promises to accelerate infrastructure demands — positioning the market for robust growth and technological evolution through 2032 and beyond.

The strategic importance of Cloud Infrastructure lies in its ability to deliver agile, scalable, and cost efficient IT backbone capable of supporting modern digital transformation, big data analytics, AI workloads, and global operations. For many enterprises, shifting from on premises data centers to cloud infrastructure yields measurable improvements. Virtualization and resource sharing can lead to up to 70-80% server utilization compared to typical 15-20% usage in traditional setups, dramatically reducing idle capacity and optimizing compute resources. AI optimized infrastructure delivers 30-40% improvement in energy efficiency compared to older standard data centers thanks to advanced cooling, workload scheduling, and energy aware resource allocation. Global volumes remain dominated by North America, while Asia Pacific leads in adoption rates, with over 45% of enterprises provisioning new workloads in cloud environments in recent years.

By 2027, edge computing and distributed cloud adoption is expected to improve latency and data throughput performance by up to 25%, enabling real time processing for IoT and AI applications in manufacturing, retail, and telecom. Firms are committing to ESG driven energy efficiency improvements, targeting a 40% reduction in carbon emissions from IT operations by 2030 through use of renewable powered data centers and virtualized infrastructure. In 2025, a leading global enterprise migrating 60% of on premises workloads to cloud infrastructure reported a 35% reduction in IT related emissions and a 22% reduction in operational energy consumption after leveraging cloud native virtualization and workload consolidation. This micro scenario underscores tangible environmental and cost benefits achievable through strategic cloud transition.

Looking ahead, the Cloud Infrastructure Market is positioned as a key pillar for resilience, compliance, sustainable growth and digital agility, offering firms a robust platform to scale operations globally, meet regulatory and ESG requirements, and stay competitive in a rapidly evolving technological landscape.

The proliferation of AI, IoT, big data analytics and large scale digital workflows has significantly expanded enterprise demand for scalable compute and storage resources. As companies deploy machine learning models, real time analytics, and data intensive applications, legacy on premises infrastructure often fails to deliver required performance or elasticity. The ability of cloud infrastructure to rapidly provision high performance compute, storage and networking, combining public cloud, private cloud, and hybrid models, enables firms to scale dynamically without heavy capital investment. Businesses report substantial improvements in resource utilization, operational efficiency, and agility when workloads shift to cloud platforms.

Data privacy, compliance, and security concerns remain a major obstacle for organizations migrating sensitive workloads to cloud infrastructure. Many enterprises, especially in finance, healthcare and government sectors, must abide by strict data sovereignty and privacy regulations. The risk of cyberattacks and data breaches further complicates adoption, with some organizations hesitant to move critical data off premises. Additionally, there is a persistent shortage of skilled cloud professionals able to architect, manage and secure complex cloud environments, including hybrid and multi cloud deployments. This skills gap limits opportunities for smaller enterprises and constrains adoption in markets lacking technical talent.

As environmental awareness and regulatory emphasis on ESG (Environmental, Social, Governance) criteria grow, demand for sustainable, energy-efficient data centers is rising. Cloud providers that invest in renewable energy, efficient cooling, virtualization, and workload optimization are positioned to attract enterprises seeking lower carbon footprints and compliance with environmental regulation. Migration to cloud infrastructure can yield up to 80-90% reduction in IT energy consumption compared to traditional on premises servers through higher utilization and advanced infrastructure design. Furthermore, distributed cloud and edge computing architectures open opportunities in latency-sensitive sectors such as telecom, manufacturing, and IoT. Enterprises expanding digital services in emerging markets can leverage cloud infrastructure to deploy edge data centers, support real time analytics, and reach new customers with minimized latency, creating new revenue streams and enhancing global competitiveness.

Initial investment costs, particularly for migration from legacy systems, remain substantial. Smaller or mid-sized firms may lack budget or resources to transition smoothly. Integration with existing IT environments can be complex, especially in organisations with legacy hardware and heterogeneous systems. Vendor lock in, proprietary tooling, and data portability issues complicate migration between providers. Once workloads are tied to a specific cloud platform, switching carries high costs and technical hurdles. This reduces flexibility for businesses and can dampen willingness to adopt extensive cloud infrastructure deployment, especially in multicloud or hybrid strategies.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Cloud Infrastructure market. Recent data indicates that 55% of new data center projects achieved cost savings through modular and prefabricated practices. Pre-bent and cut elements are fabricated off-site using automated machinery, reducing labor requirements by up to 40% and accelerating project timelines by 30%. High-precision prefabricated components are particularly in demand in Europe and North America, where efficiency and rapid deployment are critical to meet enterprise cloud expansion needs.

• Expansion of Edge Data Centers: Edge computing is driving construction of smaller, distributed data centers closer to end users. Over 48% of cloud providers are planning edge facility rollouts in urban and suburban areas to reduce latency by up to 25%. The Asia-Pacific region is leading in volume, while North America shows the highest adoption rate with 42% of enterprises integrating edge nodes into their cloud strategies. This trend enables real-time data processing for IoT, autonomous vehicles, and AI workloads, enhancing network performance and service reliability.

• Integration of AI and Automation in Operations: Cloud operators are increasingly adopting AI-driven automation to improve operational efficiency. AI-based workload management systems have reduced energy consumption by up to 35% and improved server utilization by 28% in large-scale deployments. Predictive maintenance using machine learning algorithms has cut unplanned downtime by 22%, providing measurable improvements in performance and resource allocation. Enterprises in North America and Europe are leading this integration, with over 40% of hyperscale data centers implementing AI-enabled management tools.

• Adoption of Green and Sustainable Practices: Environmental sustainability is becoming a key trend in cloud infrastructure development. Approximately 60% of newly commissioned data centers now utilize renewable energy sources, while energy-efficient cooling and virtualization strategies have lowered power usage effectiveness (PUE) by 18% on average. Firms are committing to ESG improvements, with targeted reductions in carbon emissions of up to 45% by 2030. This shift is especially evident in Europe and North America, where regulatory and consumer pressure drives investments in green cloud infrastructure projects.

The Cloud Infrastructure market is segmented across several dimensions, including type of infrastructure deployment, application scenarios, and end‑user industries. These segmentation layers provide clarity on how different infrastructure models, workloads, and sectors contribute to overall demand and adoption patterns. By analyzing types such as public cloud, private cloud, hybrid or colocation services, as well as applications like enterprise IT workloads, high‑performance computing, edge applications, and storage/back‑up services, analysts and decision‑makers gain insight into investment priorities, growth potential, and infrastructure utilization. End‑user segmentation—covering sectors like IT/telecom, finance, healthcare, manufacturing, and retail—helps characterize consumption behavior, regulatory sensitivity, compliance needs, and regional adoption dynamics. This segmentation framework offers a structured view of the Cloud Infrastructure market, guiding strategic planning and investment decisions across diverse enterprise and industry landscapes.

Public cloud infrastructure currently leads segmentation with approximately 48 % share of global Cloud Infrastructure capacity. This dominance stems from the ease of scaling resources, on-demand provisioning, and broad availability across multiple geographic regions. Private cloud accounts for around 30 % share, favored by organizations requiring strict control, data‑sovereignty, and customization for compliance‑sensitive environments. Hybrid cloud or colocation services contribute the remaining 22 %, offering a blend of flexibility and control that suits enterprises with mixed workload profiles.

Hybrid or colocation deployment is the fastest-growing segment, with usage increasing by roughly 8–10 % annually as enterprises seek to combine benefits of public and private clouds while maintaining regulatory compliance and optimizing latency and cost. Other niche types—such as community clouds or specialized enterprise-hosted private clouds—constitute a small but significant portion (roughly 5–7 % collectively) and serve industries like government, healthcare, and financial services that demand heightened security and compliance controls.

Enterprise IT workloads remain the leading application area for Cloud Infrastructure, constituting about 52 % of total infrastructure usage. These workloads include standard business applications, ERP systems, collaboration tools, and back‑office operations where elasticity, remote access, and disaster recovery are critical. High‑performance computing (HPC) and big data analytics account for around 23 %, driven by growing data volumes, AI/ML processing needs, and analytics‑driven decision systems. Edge computing and latency‑sensitive applications—such as IoT data ingestion, real‑time analytics, and content delivery—are rapidly gaining ground, projected to represent about 15 % of application usage as more enterprises adopt distributed architectures. Storage and backup services make up the remaining 10 %, valued for scalable, reliable archival and redundancy.

Edge computing applications are the fastest-growing area, with infrastructure deployments for edge nodes rising by an estimated 12–15 % per year, encouraged by demand in IoT, autonomous systems, content streaming, and low-latency services. Other applications like backup/storage and specialized disaster recovery solutions remain stable but represent a smaller share collectively (~10–12 %) and serve sectors needing data protection, compliance, or long-term archival capabilities.

Within end‑user segmentation, IT and telecommunications companies lead consumption of Cloud Infrastructure, accounting for roughly 35 % of overall market usage. These firms typically demand large-scale compute and storage resources, handling workloads like networking, hosting, SaaS delivery, and telecom backend operations. The finance and banking sector follows with approximately 22 %, driven by needs for secure data storage, compliance, disaster recovery, and scalable transaction processing. Healthcare and life‑sciences industries contribute about 18 %, leveraging cloud infrastructure for data‑intensive research, electronic health records (EHR), and secure remote access. Manufacturing and industrial enterprises represent roughly 15 %, increasingly using cloud infrastructure for IoT, automation, supply‑chain analytics, and real-time monitoring. Retail, e‑commerce, and services sectors make up the remaining ~10 %, relying on cloud for customer‑facing platforms, inventory management, and digital‑commerce operations.

Manufacturing and industrial users are the fastest-growing end‑user segment, with cloud infrastructure adoption rising by approximately 9–11 % annually as companies digitize operations, adopt IoT and real-time monitoring, and migrate legacy systems to scalable cloud environments. Other sectors—such as retail, services, and education—constitute the residual ~10–15 % combined and primarily adopt cloud infrastructure for scalable web presence, content delivery, remote work support, and seasonal demand handling.

North America accounted for the largest market share at 42% in 2024 however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of 13% between 2025 and 2032.

North America continues to dominate through a mature ecosystem of hyperscale data centers and high enterprise adoption across diverse sectors. In contrast Asia‑Pacific’s rapid digital transformation, expanding data‑center investments, and growing enterprise demand point to a strong upward trajectory in infrastructure expansion.

Is the Established Engine Fueling Global Cloud Expansion?

North America commands roughly 40–42% of global cloud infrastructure capacity, reflecting a dense network of data centers, widespread enterprise adoption, and high digital maturity. Key demand drivers include IT & telecom, finance, healthcare, and large‑scale enterprise digital transformation projects. Regulatory frameworks and government support for data security, privacy, and infrastructure modernization further boost demand. Technological advances such as AI/ML workloads, 5G deployment, and multi‑cloud architectures are accelerating migrations to cloud infrastructure. Local players and global hyperscalers continue scaling operations, driven by deep pockets and strong enterprise consumption. Enterprises in this region show high adoption especially in healthcare and finance sectors, where compliance and performance are critical.

Is the Compliance‑Driven, Sovereignty‑Focused Cloud Leader Across Regulators and Enterprises?

Europe holds about 26–28% of cloud infrastructure market share, with large contributions from countries such as Germany, the UK, France, and the Netherlands. The region’s regulatory environment and strong emphasis on data privacy and sovereignty drive hybrid and private cloud adoption, especially among regulated industries and public‑sector institutions. Sustainability initiatives and green‑cloud mandates are influencing infrastructure upgrades and energy‑efficient data‑center designs. Adoption of emerging technologies such as hybrid-cloud orchestration, secure cloud enclaves, and compliance‑ready cloud services is rising. Local European providers and sovereign‑cloud initiatives are increasingly relevant, although global hyperscalers continue to play a significant role. Enterprises in Europe often prioritize explainable cloud infrastructure, compliance assurance, and regulatory alignment.

Is the Digital Acceleration Hub Transforming Cloud Demand Across Emerging Economies?

Asia-Pacific represents roughly 22–34% of the global cloud infrastructure market volume and is recognized as the fastest-growing region by infrastructure buildouts and enterprise cloud migrations. Major consuming countries include China, India, Japan, and South‑Korea, driven by booming e‑commerce, fintech, government digitalization, and mobile‑AI applications. Countries are rapidly expanding data‑center capacity and deploying cloud infrastructure to support telecom, manufacturing, public services, and retail sectors. Regional tech hubs are emerging, combining infrastructure investments with advanced innovations in cloud‑native services and edge computing. Local providers and regional data‑center players are scaling capacity to meet growing demand, especially for cloud‑first enterprises. In Asia‑Pacific, growth is driven by demand for scalable, flexible, and cost‑effective cloud infrastructure to support rapid digital transformation and consumer‑facing services.

Is the Emerging Market Leveraging Cloud to Fuel Media, Retail, and Local Enterprise Growth?

Key countries such as Brazil and Argentina are gradually increasing adoption of cloud infrastructure, though overall share remains modest compared to leading regions. Demand is particularly strong in media, e‑commerce, retail, and localization services where cloud enables scalable content delivery and enterprise flexibility. Infrastructure and energy-sector modernization, along with favorable government incentives or trade policies in select countries, support cloud uptake. Local players and regional providers are beginning to establish data‑center capacity to meet enterprise and SME demand. End‑user behavior leans toward media, localization, and language‑sensitive offerings, making cloud infrastructure attractive for regional content and service providers.

Is the Regional Cloud Growth Powered by Government Initiatives and Sector Modernization?

Middle East & Africa show growing demand driven by sectors such as oil & gas, government digitization, telecom modernization, and enterprise expansion. Major growth countries include the UAE and South Africa, where cloud infrastructure investment is increasing. Technological modernization, including adoption of 5G, distributed cloud, and digital public services, supports infrastructure deployments. Government cloud‑first policies and trade partnerships help stimulate demand. Enterprises and public‑sector institutions are increasingly adopting cloud infrastructure for scalability, compliance, and cost efficiency. Regional consumer behavior shows a mix of enterprise-level adoption and emerging SME cloud engagements.

United States: ~ 40–42% share of global market — dominance driven by high production capacity, extensive data‑center network, and strong enterprise cloud demand.

China: ~ 25–30% share within Asia‑Pacific (making it among top global contributors) — leadership supported by massive infrastructure investments, rapid enterprise cloud adoption, and government‑backed digital initiatives.

The global cloud infrastructure market is moderately consolidated, with a small number of dominant providers capturing a substantial portion of total capacity, while a larger set of smaller and regional players compete for niche and specialized segments. As of 2025, roughly 8–10 significant competitors are active at a global scale, and the top 5 providers together hold approximately 65–70% of total infrastructure capacity or market share, creating a “Big Three + a few niche players” landscape.

The frontrunners maintain strong market positioning through aggressive strategic initiatives — including expansion of new data‑center regions, acquisition of complementary technology firms, partnerships with enterprise clients, and continuous innovation in service offerings. For example, major providers are launching advanced AI‑optimized infrastructure, enhanced hybrid‑cloud and multi‑cloud solutions, and integrated edge‑cloud services to capture demand from AI workloads, real‑time analytics, and remote‑work-driven enterprise needs. This pushes competition beyond simple compute or storage offerings toward full-stack infrastructure services and managed cloud ecosystems. Smaller and emerging cloud providers are carving niches by focusing on specialized services — such as high‑performance computing (HPC), GPU‑powered AI inference, data‑sovereignty compliance, region‑specific data center deployment, or cost‑optimized bare-metal offerings. This dynamic has increased competitive pressure, especially in regional markets and industries with strict regulatory or performance requirements.

Innovation trends — including AI‑ready GPU clusters, edge‑computing infrastructure rollouts, green/sustainable data‑center designs, and hybrid or distributed cloud architectures — are reshaping competition. Providers are investing in energy‑efficient cooling, automation, and sustainable power sources to gain advantage through lower operating costs and ESG credentials. Strategic alliances and mergers among providers and with technology partners continue to influence competitive positioning. Overall, the Cloud Infrastructure market remains competitive but concentrated: while a handful of large providers dominate, a diverse set of smaller and regional players, combined with rapid innovation and emerging enterprise needs, ensure ongoing disruption and opportunity.

Amazon Web Services (AWS)

Microsoft Azure

Google Cloud Platform (GCP)

Alibaba Cloud

Oracle Cloud Infrastructure (OCI)

IBM Cloud

Tencent Cloud

Huawei Cloud

The Cloud Infrastructure market is undergoing rapid transformation driven by both current and emerging technologies. AI and machine learning integration is now central to data-center optimization, with predictive analytics and automated resource allocation reducing energy consumption by up to 35% and improving server utilization by nearly 30% in large-scale deployments. Virtualization and containerization remain fundamental, with over 65% of enterprise workloads running on containerized platforms to enable rapid scaling, simplified management, and seamless migration between on-premises and cloud environments. Edge computing is increasingly critical, particularly in latency-sensitive applications such as IoT, autonomous vehicles, and real-time analytics. Approximately 48% of newly commissioned cloud nodes are deployed at the edge to enhance performance, lower latency by up to 25%, and support distributed workloads. Multi-cloud and hybrid cloud architectures are now standard practice for enterprises, enabling flexibility, redundancy, and regulatory compliance across global operations.

Emerging technologies, including serverless computing and AI-optimized GPUs, are reshaping infrastructure design. AI-optimized hardware clusters, installed in over 20% of hyperscale data centers, support high-performance workloads while reducing operational inefficiencies. Green technologies such as renewable-powered data centers, liquid cooling, and advanced heat-exchange systems are being adopted in over 60% of new cloud facilities, meeting ESG targets and reducing power usage effectiveness (PUE) by 15–18%. In addition, software-defined networking (SDN) and advanced security frameworks are now critical, with over 40% of cloud deployments leveraging automated threat detection, network segmentation, and compliance monitoring. Blockchain-based data integrity solutions are also being piloted, particularly in finance and healthcare, ensuring secure, traceable, and tamper-proof data operations. Collectively, these technological innovations are driving performance, efficiency, sustainability, and competitiveness in the global Cloud Infrastructure market.

In December 2023, Amazon Web Services (AWS) launched its second infrastructure region in Canada — the Canada West (Calgary) Region featuring three availability zones — expanding its global footprint and increasing options for resilience and local data residency. (Amazon Web Services, Inc.)

In December 2024, Google Cloud inaugurated its 41st cloud region located in Querétaro, Mexico, marking its third region in Latin America and enabling lower-latency access and local data‑residency compliance for enterprises and public-sector clients in Mexico. (Google Cloud)

By Q3 2024, global infrastructure‑as‑a‑service spending surged 21% year‑on‑year, with the top three providers — AWS, Microsoft Azure, and Google Cloud — together accounting for 64% of total spending, reflecting strong uptake driven by AI workloads and rising enterprise demand. (canalys.com)

In 2024, enterprise adoption of generative AI and GPU‑as‑a‑service offerings contributed significantly to market growth: Q4 enterprise spending on cloud infrastructure services rose by roughly 22% compared with Q4 2023, indicating accelerating demand for AI‑ready cloud capacity across industries. (Tech Monitor)

The Cloud Infrastructure Market Report covers a comprehensive range of segments including infrastructure deployment types (public cloud, private cloud, hybrid/colocation), service models (IaaS, PaaS, bare‑metal, GPU/AI‑optimized infrastructure), and delivery modes (centralized data centers, edge‑distributed nodes, hybrid‑cloud orchestration). It examines application domains such as enterprise IT workloads, high‑performance computing, big data analytics, real‑time IoT/edge applications, storage and backup services, and AI/ML workloads. The geographic scope spans all major regions — North America, Europe, Asia‑Pacific, Latin America, and Middle East & Africa — with regional consumption patterns and regulatory influences evaluated. Industry verticals covered include IT & telecom, finance, healthcare, manufacturing, retail, and public sector — each analyzed for infrastructure needs, compliance constraints, and growth drivers.

In addition, the report considers technological dimensions: virtualization and containerization, serverless computing, AI‑optimized hardware clusters, edge computing, energy‑efficient data centers, and sustainable infrastructure practices. Niche and emerging segments are included, such as GPU‑as‑a‑service platforms for AI workloads, distributed edge data‑center deployments close to end‑users, and hybrid‑multi‑cloud orchestration for regulated industries needing compliance and data‑locality controls.

The analysis encompasses both demand‑side factors — enterprise cloud migration, AI adoption, regulatory and ESG requirements — and supply‑side dynamics — capacity expansion, data‑center infrastructure investments, regional data‑center launches, and technological innovation. This breadth provides decision‑makers with insights into market segmentation, regional strategies, technological readiness, industry‑specific adoption, and forward‑looking infrastructure needs.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 172733.88 Million |

|

Market Revenue in 2032 |

USD 303511.62 Million |

|

CAGR (2025 - 2032) |

7.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), Alibaba Cloud, Oracle Cloud Infrastructure (OCI), IBM Cloud, Tencent Cloud, Huawei Cloud |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |