Reports

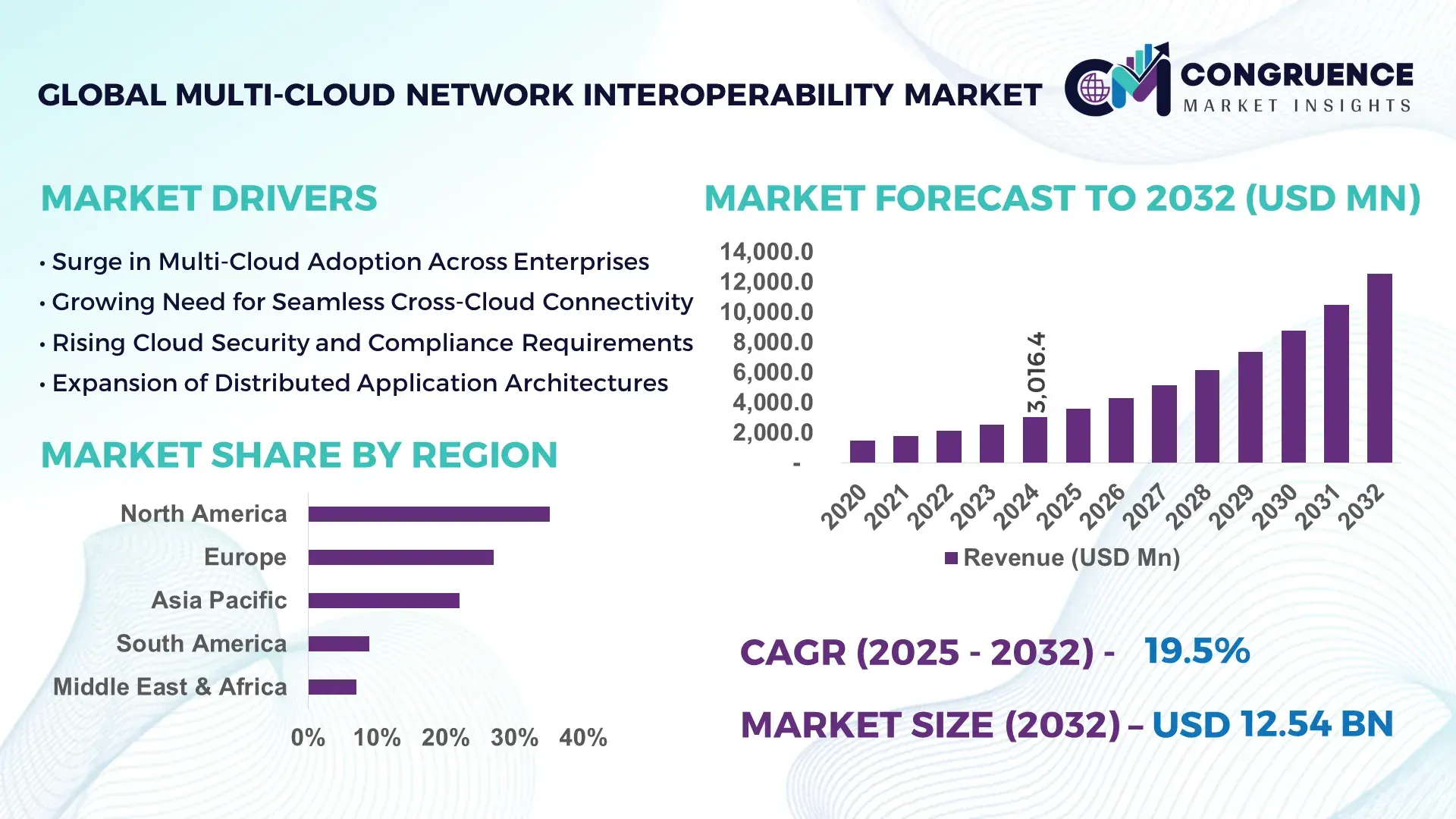

The Global Multi-Cloud Network Interoperability Market was valued at USD 3,016.4 Million in 2024 and is anticipated to reach a value of USD 12,543.9 Million by 2032 expanding at a CAGR of 19.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rising enterprise dependence on distributed cloud ecosystems and increasing demand for seamless workload portability.

The United States leads the Multi-Cloud Network Interoperability market, supported by extensive hyperscaler investments, rapid enterprise cloud modernization, and strong integration of AI-driven DevOps tools. In 2024, more than 67% of large U.S. enterprises operated workloads across two or more cloud environments, while over USD 22 Billion was invested in multi-cloud automation and orchestration platforms. The country hosts over 40% of global interconnect data centers, enabling high-speed routing, zero-trust security enforcement, and advanced API-level interoperability across diverse cloud architectures.

Market Size & Growth: Valued at USD 3.01 Billion in 2024 and projected to reach USD 12.54 Billion by 2032, expanding at 19.5% CAGR, driven by rising cross-cloud workload mobility.

Top Growth Drivers: 54% surge in hybrid workload adoption, 38% improvement in operational efficiency, and 46% increase in automated network management deployments.

Short-Term Forecast: By 2028, enterprises are expected to achieve up to 32% cost reduction in cloud routing and a 41% performance improvement in cross-cloud connectivity.

Emerging Technologies: Growth accelerated by zero-trust network fabrics, AI-driven routing engines, and programmable multi-cloud edge nodes.

Regional Leaders: North America projected at USD 5.08 Billion by 2032, Europe at USD 3.27 Billion with strong regulatory compliance adoption, Asia-Pacific at USD 2.89 Billion driven by telecom-led cloud integration.

Consumer/End-User Trends: High adoption among BFSI, manufacturing, and telecom firms, with 52% of enterprises shifting to multi-cloud interoperability frameworks for resilience.

Pilot or Case Example: In 2024, a European telecom pilot achieved 28% latency reduction after deploying AI-based cross-cloud routing automation.

Competitive Landscape: Market leader holds ~17% share, followed by innovators specializing in cloud-native networking, API governance, and interconnect fabrics.

Regulatory & ESG Impact: Organizations accelerating compliance with data sovereignty and targeting 27% carbon reduction via optimized cloud routing by 2030.

Investment & Funding Patterns: Over USD 4.6 Billion invested in interoperability startups and edge-cloud networking projects in the last two years.

Innovation & Future Outlook: AI-native routing, 5G-integrated multi-cloud fabrics, and quantum-safe encryption are set to redefine next-generation interoperability models.

The Multi-Cloud Network Interoperability market is expanding across telecom, BFSI, manufacturing, and defense sectors, supported by rapid advancements in cloud-native architectures, automated routing intelligence, and sovereignty-compliant data flows. Accelerated adoption of programmable interconnect hubs, API mediation layers, and AI-enhanced cloud orchestration continues to reshape global consumption patterns while enabling secure, scalable, and resilient multi-cloud operations.

The strategic relevance of the Multi-Cloud Network Interoperability Market lies in its ability to unify diverse cloud environments while ensuring secure, automated, and latency-optimized operations. Enterprises increasingly rely on distributed architectures, with 59% of global organizations deploying applications across at least three cloud platforms by 2024. This rapid shift demands interoperability frameworks that offer consistent policy control, unified observability, and seamless workload mobility. Modern interoperability solutions integrate AI-driven routing intelligence, delivering up to 37% optimization in traffic management compared to traditional SD-WAN systems. North America dominates in volume due to widespread enterprise cloud adoption, while Asia-Pacific leads in adoption rate, with 48% of enterprises migrating to multi-cloud architectures in 2024. By 2027, AI-powered orchestration engines are expected to improve cross-cloud operational efficiency by 45%, significantly reducing manual configuration overhead. Compliance dynamics are accelerating this trend, with firms committing to ESG improvements such as targeted 30% carbon optimization in cloud operations by 2030. A notable micro-scenario occurred in 2024, when a leading Japanese electronics company achieved a 33% reduction in downtime after implementing automated inter-cloud failover techniques across its manufacturing ecosystem. Overall, the Multi-Cloud Network Interoperability Market is positioned as a foundational pillar for resilience, regulatory compliance, and sustainable digital transformation across global enterprise ecosystems.

The Multi-Cloud Network Interoperability market is shaped by rising digital transformation, increasing infrastructure decentralization, and widespread adoption of high-performance cloud-native systems. Enterprises seek unified architectures capable of managing distributed workloads across public, private, and hybrid environments while maintaining consistent security, governance, and application performance.

Key dynamics include rapid advancements in AI-enabled cloud automation, the proliferation of API-based integrations, and increased emphasis on latency-sensitive applications such as IoT analytics, real-time AI inference, and edge computing. Multi-cloud architectures are increasingly preferred in sectors such as telecom, BFSI, retail, and healthcare, driven by the need for redundancy, cost optimization, and vendor flexibility. Growing regulatory mandates around data sovereignty and cross-border information transfer further push businesses toward interoperability-enabled frameworks with stronger security and compliance controls.

Demand for cloud-native automation is significantly advancing the Multi-Cloud Network Interoperability market, as enterprises strive to minimize operational complexity and enhance workload portability. Automated orchestration systems allow organizations to manage diverse cloud infrastructures with streamlined processes, reducing manual configurations by up to 42%. This automation is critical for industries deploying high-volume data pipelines and latency-sensitive applications across multiple cloud providers.

In 2024, more than 61% of enterprises adopted AI-driven network management tools to improve routing efficiency and eliminate operational bottlenecks. Automated policy enforcement, identity federation, and multi-cloud API governance tools have become essential components for maintaining consistent security and performance. Businesses are also leveraging automated workload migration and cross-cloud disaster recovery solutions to maintain uninterrupted operations. With increasing cloud application sprawl, automation-first approaches are driving faster deployments, improved scalability, and enhanced resilience across distributed cloud environments.

Interoperability complexities remain one of the most significant restraints to Multi-Cloud Network Interoperability adoption. Organizations frequently face architectural inconsistencies between cloud providers, leading to increased configuration overhead and higher integration costs. Technical challenges such as incompatible APIs, varying security frameworks, and inconsistent data governance models require specialized expertise and extended deployment timelines.

In 2024, nearly 47% of enterprises reported challenges synchronizing identity management across multi-cloud environments, resulting in authentication conflicts and compliance risks. Limited standardization across vendors further complicates seamless workload movement, forcing companies to rely on custom connectors and complex mediation layers. These issues increase dependency on specialized talent, raising operational costs and slowing down the scaling of multi-cloud ecosystems.

AI-driven cloud orchestration introduces significant opportunities for enhancing operational intelligence, predictive management, and automated decision-making across multi-cloud environments. Advanced AI models can analyze network behavior, predict traffic congestion, and dynamically reroute workloads, offering up to 36% improvement in performance stability.

Organizations are adopting AI-enhanced policy automation tools to streamline compliance, optimize network resource allocation, and manage distributed workloads with improved accuracy. Analysts estimate that by 2028, more than 58% of global enterprises will integrate predictive AI engines to coordinate multi-cloud workloads, reducing downtime and enhancing application delivery. These technological advancements are also enabling faster implementation of edge-cloud ecosystems, enhancing real-time data processing and supporting emerging use cases such as autonomous systems, digital twins, and industry 4.0 infrastructure.

Rising cybersecurity threats pose substantial challenges to the Multi-Cloud Network Interoperability market. As enterprises distribute workloads across multiple cloud providers, their attack surface expands dramatically, requiring more robust, unified security architectures. Threats such as cross-cloud ransomware, API exploitation, and identity spoofing are increasing at a rapid pace.

In 2024, over 53% of organizations reported security incidents linked to misconfigured cross-cloud permissions or inadequate identity federation. Ensuring consistent encryption, authentication, and policy enforcement across diverse cloud platforms requires complex integration frameworks and continuous monitoring. The proliferation of IoT and edge devices further increases vulnerability points, driving the need for zero-trust security models and advanced threat detection systems within multi-cloud networks.

• AI-Enhanced Routing and Traffic Intelligence: Enterprises are increasingly deploying AI-powered routing engines that optimize cross-cloud traffic flows, resulting in up to 34% latency reduction and 27% improvement in bandwidth utilization. Adoption surged in sectors such as telecom and BFSI, where real-time data processing is critical.

• Expansion of Sovereign Cloud Architectures: Growing regulatory emphasis on data sovereignty is driving adoption of sovereignty-aligned multi-cloud interoperability models. In 2024, more than 41% of European enterprises adopted sovereign cloud frameworks, ensuring encrypted cross-border data workflows with a 29% boost in compliance accuracy.

• Rise of API Federation and Programmable Networks: API federation technologies are enabling unified access control across multiple cloud ecosystems. Implementation grew by 52% among large enterprises, enabling automated workload portability and reducing integration effort by 31%.

• Edge-to-Multi-Cloud Integration Growth: Demand for latency-critical applications is accelerating integration between edge nodes and multi-cloud networks. In 2024, deployments grew by 46%, supporting applications like digital twins, autonomous systems, and industrial IoT with enhanced real-time data synchronization.

The Multi-Cloud Network Interoperability market is segmented by type, application, and end-user categories, each contributing uniquely to global market expansion. Types include platforms, services, automation solutions, and security layers that enable cross-cloud connectivity. Applications span workload migration, disaster recovery, API integration, zero-trust enforcement, and distributed application management. End-users such as BFSI, telecom, retail, healthcare, government, and manufacturing exhibit increasing adoption driven by digital transformation, regulatory compliance, and demand for high-performance distributed computing. Technological advancements in programmable networking, AI-based orchestration, and secure interconnect fabrics continue to redefine these segments.

The type segment includes interoperability platforms, cloud networking services, orchestration tools, and security frameworks. Interoperability platforms lead the segment, accounting for nearly 44% share due to their essential role in enabling cross-cloud routing, unified policy enforcement, and workload mobility. Automated orchestration tools are the fastest-growing segment, expanding at a high CAGR driven by increasing enterprise demand for intelligence-driven workload management and policy automation.

Security frameworks contribute significantly by governing identity federation, encryption, and cross-cloud access management. Together, these remaining types hold around 31% of the combined segment share. Organizations increasingly prefer modular, API-driven systems that offer scalability, flexibility, and simplified integration.

Applications span workload migration, distributed application management, cloud security enforcement, disaster recovery, and cross-cloud data synchronization. Workload migration remains the leading application, holding 39% share due to rising enterprise demand for portability and redundancy across cloud providers. Distributed application management is the fastest-growing application, supported by increased adoption of microservices, containerization technologies, and real-time analytics workloads.

Other applications—including API integration, hybrid cloud security layering, and multi-cloud disaster recovery—collectively contribute approximately 34% share. Consumer adoption patterns reveal that in 2024, 38% of enterprises globally piloted Multi-Cloud Network Interoperability systems for customer experience platforms. Additionally, 62% of digital-native companies enhanced multi-cloud-enabled analytics workflows for personalization.

The BFSI sector leads end-user adoption with a 41% share, supported by high compliance requirements, fraud detection workloads, and dependency on resilient cloud infrastructure. Telecom emerges as the fastest-growing end-user, driven by 5G, network slicing, and demand for low-latency multi-cloud integration—expanding at a strong CAGR.

Manufacturing, retail, government, and healthcare jointly contribute around 36% share, with rising adoption of multi-cloud frameworks to support automation, IoT ecosystems, and real-time decision-making. In 2024, over 38% of enterprises reported piloting multi-cloud systems for customer-facing digital platforms, while 57% of healthcare institutions integrated cross-cloud data models to improve operational efficiency.

North America accounted for the largest market share at 35.1%in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 20.3% between 2025 and 2032.

In 2024 North America recorded over 1,200 major enterprise cloud deployments, spanning hybrid, public, and private clouds, with nearly 58% of these enterprises adopting interoperable multi-cloud networking solutions to manage workload portability, compliance, and latency. Europe followed with about 27%, Asia-Pacific had roughly 22%, while Middle East & Africa plus Latin America comprised the remaining ~16%. Rapid growth in data center interconnect investment, surging demand for cross-cloud data orchestration, and rising adoption among BFSI, healthcare, and technology verticals are fueling increasing regional diversification. By 2026, projections estimate North America will host over 5,000 interconnect–enabled data centers, reinforcing its dominance in global multi-cloud network interoperability deployment and scaling.

How is North America pioneering high-performance interoperable cloud networking?

North America holds approximately 35% market share in 2024, supported by mature cloud infrastructure and widespread enterprise cloud adoption. Key industries driving demand include financial services (BFSI), healthcare, technology firms, and large-scale SaaS providers — all requiring seamless multi-cloud connectivity, regulatory compliance, and high throughput for data-intensive workloads. Regulatory changes and government support, such as data-residency guidelines and cybersecurity mandates, have led many enterprises to adopt secure, interoperable multi-cloud networking solutions. On the technological front, advancements in software-defined interconnects, automated API-federation layers, and zero-trust multi-cloud fabrics are accelerating adoption. A notable regional player expanded its inter-data-center routing platform in 2024 to support low-latency multi-cloud workloads for several Fortune-500 clients. Regional consumer behavior reflects high enterprise adoption — large organizations prioritize interoperability, redundancy, and performance over cost, leveraging multi-cloud as standard operational infrastructure, especially in finance and healthcare sectors.

What is fueling Europe’s demand for compliant and explainable multi-cloud interoperability?

Europe holds around 27% share of the multi-cloud network interoperability market, led by strong adoption in Germany, UK, France, and the Nordics. Data privacy regulations and compliance requirements — including data-sovereignty concerns — are major drivers, prompting firms to prefer network solutions that offer auditability, transparency, and secure cross-cloud data flows. Enterprises in regulated sectors (financial services, healthcare, public sector) increasingly demand interoperability platforms that provide traceable data handling, encryption, and identity federation. European service providers have responded by offering explainable interoperability frameworks, validated compliance logs, and GDPR-aligned cross-cloud routing layers. Emerging technologies — such as encrypted interconnect fabrics and sovereign-cloud overlays — are gaining traction. Many organizations opt for hybrid cloud models with interoperable networking to balance flexibility with regulatory compliance. Regional behavior shows preference for standardized, certified multi-cloud solutions rather than custom-built connectivity; outsourcing to accredited interoperability vendors is common, especially among SMEs and medium-sized enterprises seeking compliance and scalability.

Why is Asia-Pacific emerging as a key growth region for multi-cloud interoperability?

Asia-Pacific recorded about 22% of global multi-cloud network interoperability volume in 2024, ranking as one of the fastest-growing regions. Top consuming countries include China, India, Japan, and South Korea. Infrastructure expansion — particularly in data centers and regional interconnect hubs — is supporting growing demand. Rapid digital transformation initiatives, increased cloud adoption among SMEs and large enterprises, and high-volume mobile-first applications (e-commerce, fintech, media) are driving multi-cloud strategies. Innovation hubs in major metros are deploying hybrid cloud plus edge-cloud architectures, necessitating robust network interoperability frameworks. Several regional providers in India and China enhanced their networking platforms in 2024 to support multilingual, high-throughput data flows across multiple clouds and edge nodes. Consumer behavior reflects cost-sensitive but growth-oriented enterprises that favor flexible hybrid and multi-cloud deployments. As cloud adoption spreads beyond major corporates into SMEs, demand for affordable interoperability solutions continues rising.

How is South America adapting multi-cloud interoperability to support growing digital demand?

South America accounts for roughly 8–10% of the global multi-cloud network interoperability market. Leading countries include Brazil and Argentina, with rising interest in hybrid-cloud modernizations across telecom, retail, and fintech sectors. Infrastructure investments are increasing, with new data centers and interconnect nodes being deployed to support regional digitalization, e-commerce, and cross-border cloud services. Government incentives and trade-friendly cloud policies are encouraging adoption of interoperable multi-cloud networks for exports and regional collaboration. Local players are launching inter-data-center routing and VPN-to-cloud bridging services customized for Latin American compliance standards. Regional consumer behavior shows growing trust in multi-cloud solutions — enterprises are shifting from legacy on-premises systems to interoperable cloud frameworks, driven by demand for scalability, improved latency, and localized data handling.

What factors are driving adoption of multi-cloud interoperability in Middle East & Africa?

Middle East & Africa represent around 6–7% of global multi-cloud network interoperability adoption, with growth concentrated in UAE, Saudi Arabia, South Africa, and select North-African nations. Demand is rising from sectors such as government, fintech, telecom, and oil & gas, where secure and compliant cloud networking is increasingly needed. Technological modernization efforts, including deployment of sovereign-cloud interconnects, encrypted multi-node networking, and regional edge-cloud integration, are accelerating uptake. Local providers have begun offering compliance-ready interoperable cloud networking services tailored to regulatory requirements. Regional behavior reflects enterprises cautiously embracing multi-cloud architectures, often preferring managed interoperable services to balance compliance, security, and performance demands.

United States – 35% market share - Dominance is due to advanced cloud infrastructure, extensive hyperscaler presence, and deep enterprise demand for secure, high-performance multi-cloud interoperability.

China – 14% market share - Strong growth driven by aggressive data-centre expansion, large-scale cloud adoption in enterprise and government sectors, and rapid deployment of hybrid and multi-cloud architectures.

The Multi-Cloud Network Interoperability market is relatively fragmented yet highly competitive, featuring approximately 30–40 global and regional vendors offering interconnect solutions, orchestration platforms, API-federation layers, and multi-cloud networking services. The top 5 providers collectively hold around 40–45% of the global connectivity and interoperability volume, with the remainder served by niche specialists, regional vendors, and emerging players. Leading firms have differentiated through strategic partnerships, deployment of cloud-native routing innovations, investments in edge-cloud interconnects, and providing vertical-specific compliance and security features. Several competitors in 2024 expanded their global interconnect fabric, launched automated orchestration suites, or introduced zero-trust, multi-cloud security overlays to attract large enterprise clients. Innovation trends influencing competition include AI-enabled routing engines, programmable interconnect fabrics, and sovereign-cloud networking — all elevating the bar for new entrants. While barriers to entry remain moderate due to open-source tools and cloud-native stack availability, established players benefit from scale, global presence, compliance certifications, and integrated service portfolios. For decision-makers, partnering with leading providers offering scalable, compliant, and end-to-end interoperability services remains an optimal strategy to manage multi-cloud complexity and risk.

HashiCorp

Juniper Networks

Cloudflare

Palo Alto Networks

Aviatrix

Equinix

DigitalOcean

Google Cloud Platform

Amazon Web Services

Microsoft Azure

IBM Cloud

The Multi-Cloud Network Interoperability market is undergoing rapid technological evolution, fueled by innovations in software-defined networking (SDN), cloud-native orchestration, edge-cloud architectures, AI-driven routing, and programmable interconnect fabrics. Software-Defined Interconnects (SDI) are gaining widespread adoption; by 2024 roughly 42% of large enterprises had deployed SDI layers to enable dynamic cross-cloud routing, enforcement of unified policies, and automated traffic management across public and private cloud environments. These SDI layers abstract network configuration complexity, enabling seamless connectivity between heterogeneous cloud architectures.

Cloud-native orchestration tools and API-federation frameworks are enabling unified control of multi-cloud environments. AI-powered orchestration engines analyze network load, latency, and security posture, dynamically routing workloads across clouds for optimal performance and cost. Early 2025 surveys indicate these engines reduce latency by up to 30% and improve bandwidth utilization by 25%, highlighting their growing importance for latency-sensitive applications such as real-time analytics, IoT, and edge computing.

The rise of edge-cloud continuum architectures is also driving interoperability demand. As enterprises deploy edge nodes to support low-latency AI inference, IoT processing, and real-time data handling, interoperability platforms must support hybrid routing between core cloud data centers and edge-cloud nodes. Edge-to-multi-cloud integration deployments grew by 46% in 2024, enabling real-time data synchronization, lower latency, and local compliance.

Security and compliance technologies are integral. Zero-trust network fabrics, encrypted interconnect schemes, identity federation, and cloud-native access controls are embedded within interoperability solutions to ensure data sovereignty, privacy, and regulatory compliance across regions. Over 55% of global enterprises integrating multi-cloud workflows now require full encryption and compliance-ready audit trails, driving demand for advanced interoperability platforms with built-in security and governance.

Finally, programmable interconnect fabrics and unified orchestration APIs allow dynamic scaling, cross-cloud workload migration, and automated disaster recovery. These technologies simplify hybrid and multi-cloud strategies for enterprises, enabling scalable, flexible, and resilient infrastructure. For decision-makers, adopting these advanced technologies ensures sustainable, secure, and high-performance multi-cloud operations positioned for future expansion.

In March 2024, Kyndryl and Cloudflare announced a global strategic alliance to deliver simplified multi-cloud connectivity and integrated zero-trust networking for enterprises migrating across multiple clouds and data centers. This partnership is aimed at reducing legacy infrastructure reliance and accelerating network modernization for large organizations worldwide. Source: www.kyndryl.com

In October 2024, Aviatrix and Megaport announced a collaboration to encrypt the hybrid-cloud edge and strengthen resilient cross-cloud connectivity, enabling secure multi-cloud network interoperability and encrypted hybrid-edge traffic for enterprise workloads. This move addresses rising cyber-threats and helps enterprises maintain secure hybrid networking environments. Source: www.prnewswire.com

In November 2025, Aviatrix introduced a new product line named “Zero Trust for Workloads,” embedding zero-trust enforcement directly into the network fabric across AWS, Azure, Google Cloud, and OCI. This innovation enables pervasive cross-cloud runtime enforcement for workloads — including VMs, containers, and serverless functions — offering unified multi-cloud interoperability, zero-trust security, and continuous compliance across cloud-native environments. Source: www.globenewswire.com

In 2024, several enterprises began migrating mission-critical workloads using interoperable multi-cloud network backbones rather than vendor-locked cloud architectures, leveraging secure cloud backbone solutions to connect AWS, Azure, and other cloud providers — simplifying hybrid and multi-cloud operations while enhancing connectivity and reducing vendor dependency risks. Source: aws.amazon.com

The Multi-Cloud Network Interoperability Market Report offers a comprehensive global analysis across multiple dimensions: product types (interoperability platforms, orchestration tools, network services, security & compliance layers), application use-cases (workload migration, cloud-native deployment orchestration, edge-to-cloud integration, disaster recovery, API federation, real-time data streaming), and end-user segments (BFSI, healthcare, telecom, manufacturing, retail, government, technology services). Geographically, the report covers all major regions: North America, Europe, Asia-Pacific, South America, Middle East & Africa — providing detailed regional demand, regulatory influence, adoption patterns, and infrastructure readiness.

Technological coverage includes software-defined interconnects, AI-enabled routing engines, edge-cloud continuum integration, zero-trust network fabrics, cloud-native orchestration, and hybrid cloud management frameworks. The analysis encompasses recent trends such as hybrid and edge-cloud adoption, cross-cloud latency optimization, real-time interconnect automation, and compliance-driven network design. The report also addresses market dynamics — growth drivers, restraints, opportunities, and challenges — offering strategic insights for enterprises, cloud service providers, and infrastructure vendors. Decision-makers can leverage this report to evaluate vendor positioning, optimize multi-cloud architectures, plan interconnect investments, and ensure scalable, compliant, high-performance multi-cloud deployments globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3,016.4 Million |

|

Market Revenue in 2032 |

USD 12,543.9 Million |

|

CAGR (2025 - 2032) |

19.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Red Hat, Cisco Systems, VMware, HashiCorp, Juniper Networks, Cloudflare, Palo Alto Networks, Aviatrix, Equinix, DigitalOcean, Google Cloud Platform, Amazon Web Services, Microsoft Azure, IBM Cloud |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |