Reports

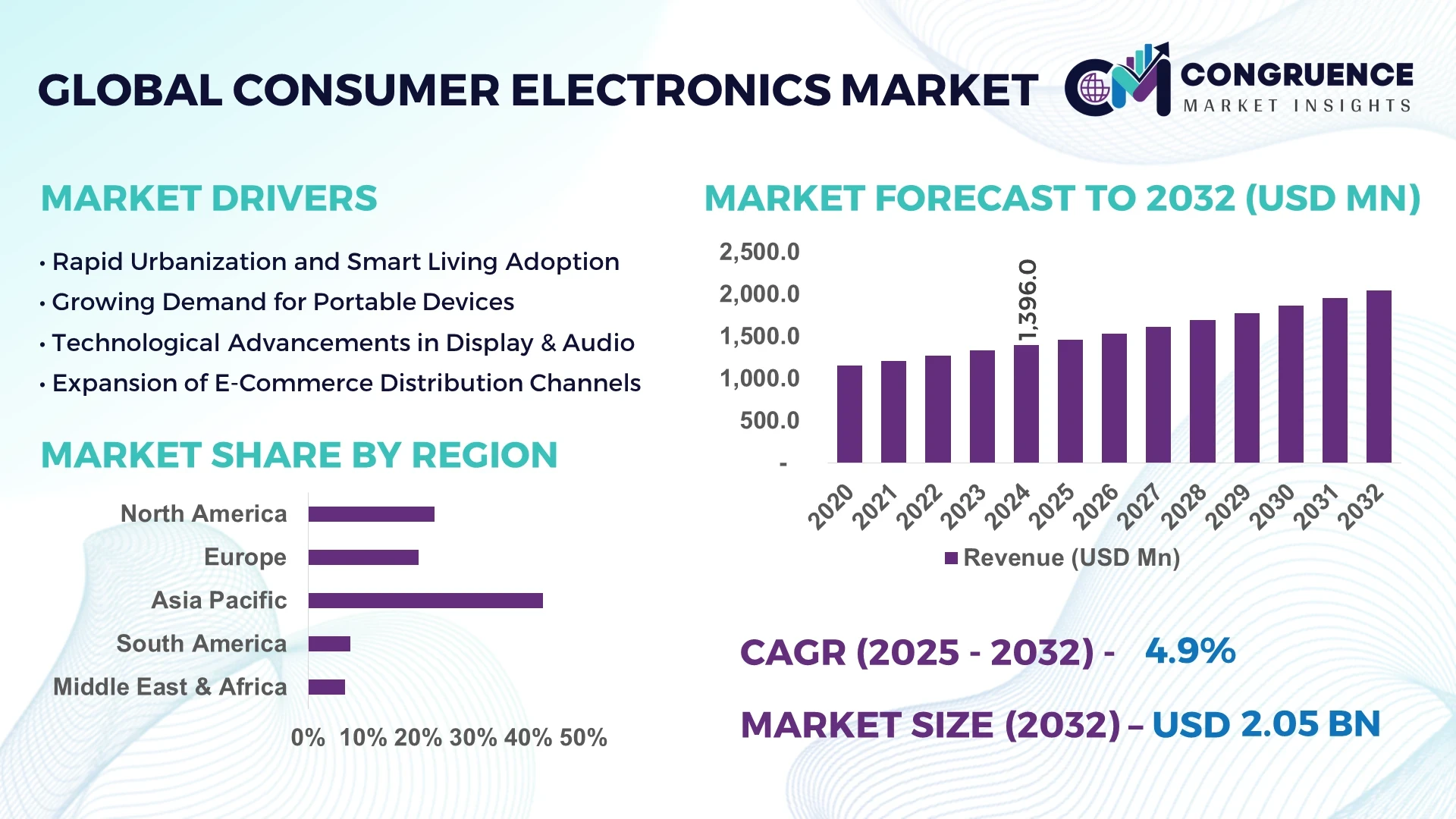

The Global Consumer Electronics Market was valued at USD 1,396 Million in 2024 and is anticipated to reach a value of USD 2,046.86 Million by 2032 expanding at a CAGR of 4.9% between 2025 and 2032.

In 2024, China maintained its dominant position within the Consumer Electronics market, supported by extensive production infrastructure, consistent investment in R&D, diversified electronic manufacturing bases, and robust advancements in microchip integration for both consumer and industrial-grade applications.

The Consumer Electronics Market is evolving rapidly due to shifting consumer preferences, digital lifestyle integration, and innovative product cycles. Segments such as smartphones, smart TVs, wearables, and home automation systems continue to drive major growth, with smartphones contributing significantly to product sales volume globally. Innovations in foldable display technology, OLED advancements, and wireless charging solutions are altering product design dynamics. Additionally, stringent energy efficiency regulations and sustainable production mandates are shaping product development. In developed economies, there is increased demand for connected home ecosystems, while emerging markets are witnessing fast adoption of budget-friendly yet feature-rich electronics. Global supply chains are adapting to incorporate more localized assembly and sourcing practices. Moreover, the transition to 5G and IoT-enabled devices is reshaping user interaction, data processing, and product interoperability. As digital connectivity becomes a cornerstone of modern living, the Consumer Electronics Market is positioned for strong expansion across various geographies and sectors.

Artificial Intelligence (AI) is profoundly reshaping the Consumer Electronics Market by driving intelligent functionality, user personalization, and smarter device integration across multiple product segments. From AI-powered smart speakers that adapt to voice patterns, to televisions that auto-optimize picture quality using machine learning algorithms, AI is redefining how users interact with consumer electronics. Manufacturers are embedding AI processors into devices like smartphones, home appliances, and wearables, enabling real-time decision-making, predictive analytics, and energy-efficient operations.

In the realm of smart home ecosystems, AI facilitates seamless connectivity among devices, enhancing automation through contextual learning. Refrigerators, washing machines, and air conditioners embedded with AI are now capable of predictive maintenance and dynamic performance adjustments. Furthermore, AI-driven recommendation engines on smart TVs improve user satisfaction by tailoring content suggestions to viewing behavior. Robotics, too, is finding traction in home consumer electronics with autonomous vacuum cleaners and personal assistant bots incorporating computer vision and AI for enhanced performance.

AI is also improving operational efficiency across the supply chain, optimizing inventory management, and enabling faster response to market demand changes. In production, AI-driven quality assurance systems are reducing defects and accelerating time-to-market. As personalization becomes central to consumer preferences, the role of AI in enhancing product intelligence and adaptability will be pivotal in shaping the future of the Consumer Electronics Market.

“In 2024, Samsung introduced an AI-powered energy-saving mode across its premium smart TV lineup, which utilizes real-time ambient light data and content type recognition to reduce energy consumption by up to 32% without compromising display quality.”

The widespread adoption of smart and connected technologies has become a key driver in the Consumer Electronics Market. Devices such as smart speakers, connected televisions, AI-based air conditioners, and IoT-integrated refrigerators are increasingly becoming mainstream across both developed and developing economies. According to 2024 shipment statistics, over 900 million smart devices were delivered globally, representing a 14% rise compared to the previous year. This growth is largely supported by the expansion of 5G infrastructure, increased cloud-based services, and improved affordability of IoT-enabled components. Consumers are also embracing seamless digital ecosystems, where smartphones act as central hubs for managing all household devices, entertainment, security systems, and even health monitoring. The demand for interconnected and voice-responsive environments is expected to continue shaping product innovation and purchase behavior.

Despite steady growth, the Consumer Electronics Market is facing substantial pressure due to increasing electronic waste (e-waste) and sustainability challenges. With short product life cycles and rapid technological upgrades, millions of tons of outdated or non-recyclable electronic goods are discarded annually. In 2024, global e-waste generation exceeded 57 million metric tons, a figure projected to grow if circular economy models are not implemented effectively. Many consumer devices are manufactured with limited recyclability, using rare earth materials and non-biodegradable plastics. This has raised regulatory and public concerns over environmental harm and improper disposal. Governments across Europe and parts of Asia have started enforcing stricter guidelines on electronic product recycling, manufacturer responsibility, and eco-friendly designs, making sustainability a central concern for electronics brands.

An emerging opportunity in the Consumer Electronics Market lies in the rapid expansion of wearable technology, particularly health-focused devices. The growing public interest in wellness, fitness, and real-time health tracking has spurred innovation in smartwatches, fitness bands, and biosensor-enabled wearables. In 2024 alone, wearable device shipments reached over 520 million units, with over 60% equipped with health-tracking capabilities such as heart rate monitoring, sleep analytics, and blood oxygen sensing. These devices are now integrating advanced biometric sensors, AI-powered health insights, and compatibility with telehealth platforms. Additionally, demand from aging populations and chronic disease patients is fueling interest in medically-approved consumer wearables. This segment offers manufacturers the chance to diversify product portfolios and tap into the fast-growing intersection of health and personal electronics.

The Consumer Electronics Market faces persistent challenges from geopolitical instability and resulting supply chain disruptions. Trade restrictions, export controls, and rising tariffs between key markets like the U.S. and China have led to increased operational costs and component shortages. In 2024, a global semiconductor shortage caused significant production delays across major product categories, from smartphones to gaming consoles and smart appliances. The over-reliance on specific regions for critical components like microchips and display panels has exposed the vulnerability of global supply chains. Furthermore, regulatory complexities and fluctuating foreign exchange rates have hindered consistent market expansion strategies for global brands. To address this, companies are now reevaluating sourcing practices, diversifying supplier bases, and investing in local assembly to reduce risk exposure and maintain supply continuity.

• Expansion of Foldable and Flexible Display Technology: Foldable devices have transitioned from novelty to mainstream, driven by continuous innovation in OLED technology and hinge durability. In 2024, global shipments of foldable smartphones crossed 30 million units, marking a 42% year-on-year growth. Major electronics brands are diversifying product lines with rollable and bendable displays in laptops and tablets. These devices support multitasking, reduce form factor limitations, and appeal strongly to tech-savvy consumers seeking compact yet multifunctional electronics.

• Accelerated Growth of Smart Home Ecosystems: The demand for integrated smart home systems is intensifying, especially in urban residential sectors. Over 65% of newly launched home appliances in 2024 came equipped with smart assistants or app-based remote controls. Smart TVs, thermostats, lighting systems, and voice-controlled kitchen appliances are increasingly interconnected. This rise is particularly noticeable in North America and East Asia, where high internet penetration and dual-income households are accelerating the need for automation and convenience.

• Rising Popularity of Wearables for Health and Fitness: Wearable technology saw record adoption levels in 2024, with over 520 million devices shipped worldwide. More than 60% of these were equipped with advanced health monitoring features like ECG, SpO2, and sleep pattern tracking. Enhanced accuracy and integration with health platforms are making wearables essential for proactive wellness management. Consumers aged 30–50 represent the fastest-growing user segment, attracted by the convenience of real-time biometric feedback.

• Transition Toward Sustainable and Repairable Electronics: There is a noticeable shift in consumer preference for environmentally responsible electronics. In 2024, over 40% of new consumer electronics models launched in Europe featured modular components for easy repairs and longer product life. Brands are increasingly focusing on eco-friendly packaging, recyclable materials, and offering repair kits. Regulatory bodies in the EU and parts of Asia are pushing for right-to-repair legislation, making sustainability a priority in product development and marketing strategies.

The Consumer Electronics Market is strategically segmented into three core dimensions: type, application, and end-user. These segments offer detailed insights into how products are evolving in response to technological advances and consumer preferences. From smartphones and wearable devices to smart TVs and home appliances, each product category addresses a distinct demand set. On the application front, daily usage, entertainment, communication, and health monitoring have emerged as major focal points. In terms of end-users, households continue to dominate, although rising adoption in commercial and industrial spaces is reshaping distribution dynamics. The segmentation analysis highlights the need for tailored marketing, differentiated product offerings, and innovation pipelines that align with specific user groups and use cases. These structured insights help stakeholders assess where opportunities lie across emerging markets, product categories, and functional domains.

Smartphones remain the leading type in the Consumer Electronics Market, driven by their central role in everyday connectivity, entertainment, and commerce. In 2024, global smartphone shipments surpassed 1.3 billion units, reflecting their widespread penetration across demographics. Premium models with foldable displays, AI-based cameras, and 5G capabilities are particularly popular in urban centers. Wearables are currently the fastest-growing product type, with demand fueled by heightened awareness of personal health and fitness. Smartwatches and fitness bands that monitor vital signs, track sleep, and provide real-time feedback are seeing strong uptake, especially among the 25–45 age group. Their integration with healthcare apps and insurance platforms is further expanding use cases. Other types such as smart TVs, tablets, and audio devices retain consistent demand. Smart TVs are evolving with AI content recommendations and 8K resolution, while wireless audio products like earbuds and smart speakers cater to mobile and remote work lifestyles. Collectively, these types highlight the diversification within the Consumer Electronics Market.

Communication remains the dominant application in the Consumer Electronics Market, propelled by the continued proliferation of smartphones, tablets, and wearables. These devices enable instant messaging, video calls, and real-time notifications, making them indispensable in both personal and professional settings. Enhanced voice recognition and AI-driven translation tools are also supporting growth in this segment. Health monitoring is the fastest-growing application, thanks to rising consumer interest in wellness and the availability of non-invasive biometric tracking. In 2024, over 60% of wearable devices included heart rate, sleep, and oxygen saturation sensors. Their compatibility with digital health records and fitness platforms has expanded their relevance across all age groups. Entertainment and smart home automation follow closely. Streaming-capable smart TVs, AR/VR headsets, and wireless audio devices are transforming how users consume content. Meanwhile, smart appliances and lighting systems with IoT connectivity are streamlining household routines. These diverse applications reflect how the Consumer Electronics Market is interwoven with daily life.

Households represent the leading end-user segment in the Consumer Electronics Market. Modern homes are increasingly integrating smart ecosystems consisting of connected TVs, voice assistants, wearable health devices, and automated appliances. In 2024, nearly 70% of newly launched home appliances featured built-in smart functionalities, reflecting a strong shift toward tech-driven living spaces. The fastest-growing end-user segment is commercial enterprises. Businesses are increasingly adopting consumer-grade electronics such as tablets, VR headsets, smart displays, and collaborative tools for improved productivity, client interaction, and employee wellness programs. Tech-enabled retail experiences and remote working environments are key drivers in this sector. Educational institutions, healthcare providers, and public sector organizations also contribute significantly. Schools are utilizing tablets and smart projectors, while hospitals employ smart monitoring devices for patient tracking. Government agencies are gradually implementing smart kiosks and security electronics. This broad end-user landscape reinforces the pervasive utility of consumer electronics across multiple domains.

Asia-Pacific accounted for the largest market share at 42.6% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

The Asia-Pacific region benefits from high consumer penetration, large-scale production hubs, and rapidly advancing technology ecosystems. Countries like China, Japan, and South Korea are leading the innovation curve in displays, mobile devices, and semiconductors. Meanwhile, regions such as the Middle East are witnessing a surge in consumer electronics adoption due to urbanization, government-backed digital transformation policies, and increasing disposable incomes. In North America and Europe, innovation is driven by sustainability, smart home demand, and early AI integration in devices. Latin American markets are showing steady growth, propelled by mobile phone expansion and improved e-commerce access. Overall, regional dynamics in the Consumer Electronics Market are shaped by local production capacity, economic policy, digital infrastructure, and consumer behavioral trends.

Innovation in Smart Ecosystems Fuels Demand in Modern Households

North America captured approximately 23.4% of the global Consumer Electronics Market in 2024, with strong contributions from the United States and Canada. The region's dominance stems from high-tech adoption, widespread use of smart homes, and an innovation-friendly regulatory environment. Tech giants are heavily investing in AI-powered devices, foldable displays, and home automation systems, creating a dynamic market. The U.S. government continues to support semiconductor manufacturing and AI development, which further stimulates growth in electronics production. Rapid 5G deployment, increased demand for high-end wearables, and digital-first retail channels are also transforming consumer behavior and purchase patterns across the region.

Technological Circularity and Smart Devices Drive Market Expansion

Europe held around 19.6% of the Consumer Electronics Market in 2024, with Germany, the UK, and France as the top-performing countries. The region emphasizes sustainability and eco-friendly production, supported by regulations such as the Right to Repair initiative. The European Commission is also accelerating digital transformation through funding and infrastructure support, encouraging widespread IoT and AI adoption. German companies are known for precision electronics and automotive electronics integration, while France and the UK focus on advanced consumer appliances and wearable tech. Smart cities, smart homes, and circular electronics manufacturing practices are reshaping demand in the European landscape.

Tech-Driven Manufacturing Powerhouses Lead Market Dominance

Asia-Pacific dominated the Consumer Electronics Market in 2024, holding a commanding 42.6% share. China, India, Japan, and South Korea are key consumption and production hubs, with China alone contributing to over 25% of the global volume. The region excels in large-scale manufacturing, supply chain efficiency, and cost-effective production. India’s smartphone market witnessed record shipments in 2024, while Japan and South Korea advanced in display panels and semiconductor innovation. Innovation parks, 5G infrastructure rollouts, and localized assembly units are boosting regional capacity. The ecosystem's agility in adapting to consumer needs makes Asia-Pacific a dominant force in the global market.

Rising Urban Demand and Digital Accessibility Shape Growth

South America contributed 6.8% to the Consumer Electronics Market in 2024, led by Brazil and Argentina. Brazil remains the largest contributor, driven by its expanding middle class, smartphone usage, and the government's digital inclusion initiatives. Argentina is catching up through tax incentives and increasing foreign investment in electronics assembly. Local assembly of smartphones and smart TVs is growing, reducing dependency on imports. Infrastructure upgrades and improved internet penetration are enabling greater access to smart devices across urban and semi-urban regions. Energy-efficient electronics and mobile commerce are key areas of opportunity in this developing but promising market.

Digital Inclusion and Smart Infrastructure Fuel Emerging Market Growth

The Middle East & Africa region accounted for 7.6% of the global Consumer Electronics Market in 2024, with UAE and South Africa emerging as key growth hotspots. Demand is expanding due to smart city initiatives, large-scale infrastructure projects, and growing tech-literate populations. Government-led reforms in digital infrastructure and trade policies are encouraging foreign investment and local innovation. Countries in the Gulf Cooperation Council (GCC) are investing in AI, cloud connectivity, and high-end consumer electronics. South Africa's growing middle-class and telecom infrastructure boost demand for smartphones, wearables, and smart appliances. These factors contribute to the region's rapid market acceleration.

China – 25.3% market share

China leads the Consumer Electronics Market due to its vast production capacity, advanced supply chains, and vertically integrated manufacturing hubs.

United States – 18.9% market share

The U.S. maintains its position through strong end-user demand, innovation in smart home technologies, and sustained investment in AI-based consumer devices.

The Consumer Electronics Market is intensely competitive, with over 150 globally active players ranging from large multinational corporations to specialized domestic brands. The industry is characterized by rapid product innovation, short lifecycle durations, and high R&D intensity. Companies continuously strive to gain a competitive edge through smart device integration, AI-driven technologies, and eco-friendly manufacturing practices. Competitive dynamics are further amplified by aggressive strategies such as strategic mergers, global distribution partnerships, and localized production investments to reduce delivery timelines and import costs.

Major players are investing in IoT-enabled appliances, foldable screen technologies, and wearable electronics, reshaping consumer expectations. Key participants are also focusing on sustainability goals, introducing products with modularity, energy efficiency, and recyclable materials. The premium product segment is witnessing strong competition, particularly in North America and East Asia, where technological innovation and brand differentiation matter most. Meanwhile, mid-tier and budget electronics remain the battleground in emerging markets where price competitiveness is critical. Overall, competitive intensity continues to rise, driven by constant innovation, evolving consumer demand, and technological disruption across the Consumer Electronics Market.

Samsung Electronics Co., Ltd.

Apple Inc.

Sony Corporation

LG Electronics Inc.

Panasonic Corporation

Xiaomi Corporation

HP Inc.

Dell Technologies Inc.

Lenovo Group Ltd.

TCL Technology Group Corporation

ASUSTeK Computer Inc.

Acer Inc.

Huawei Technologies Co., Ltd.

Sharp Corporation

Vivo Communication Technology Co., Ltd.

The Consumer Electronics Market is being rapidly transformed by advancements in smart technologies, miniaturization, and energy efficiency. Key innovations include the integration of Artificial Intelligence (AI) and Machine Learning (ML) into everyday devices such as smartphones, televisions, and wearable electronics. These technologies enhance user experience through predictive personalization, voice recognition, facial recognition, and context-aware computing. For instance, AI-enabled smart TVs now offer real-time content curation and audio optimization based on environmental inputs. 5G connectivity is another game-changing technology fueling growth across multiple product lines. With ultra-low latency and faster speeds, 5G is enabling enhanced mobile gaming, seamless video streaming, and advanced Internet of Things (IoT) ecosystems. Over 1.2 billion consumer electronics devices are estimated to support 5G by the end of 2025, further accelerating digital interconnectivity.

Meanwhile, foldable display technology and microLED panels are redefining form factors and visual experiences. Major brands are already launching dual-screen and flexible smartphones, signaling a shift toward versatile hardware design. In wearables and smart appliances, sensor integration is becoming more advanced, supporting real-time health monitoring and home automation. Additionally, sustainable tech is gaining traction with companies introducing modular designs, recyclable materials, and low-energy consumption circuits to meet environmental standards. These technological developments are shaping the future roadmap of the Consumer Electronics Market and driving a new era of innovation.

• In March 2024, Samsung unveiled its Galaxy Ring, a new health-tracking wearable device with continuous biometric monitoring, including heart rate, sleep cycles, and skin temperature, integrated with AI analytics for personalized wellness recommendations.

• In January 2024, LG Electronics launched the world’s first 98-inch QNED TV equipped with Quantum Dot and NanoCell technologies, offering improved color accuracy and ultra-bright HDR performance tailored for high-end home entertainment markets.

• In August 2023, Sony introduced its next-generation spatial reality display with 4K resolution and real-time eye-tracking for 3D content visualization, aimed at developers in the fields of gaming, design, and education.

• In October 2023, Xiaomi announced the rollout of its HyperOS, a unified operating system across smartphones, tablets, smart TVs, and IoT appliances, aiming to streamline cross-device connectivity and user experience within its ecosystem.

Let me know if you'd like these developments converted into a visual timeline or infographic for business presentations.

The Consumer Electronics Market Report provides an extensive evaluation of the global industry landscape, encompassing an in-depth analysis of key product segments, application areas, and end-user categories. This report outlines developments across mobile devices, televisions, laptops, desktops, gaming consoles, smart wearables, and household appliances, with attention given to both legacy systems and emerging product categories. Particular emphasis is placed on innovations such as AI-powered home assistants, foldable smartphones, and health-monitoring wearables, which are contributing to the market’s evolving structure. The report examines the market across five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—offering granular insights into region-specific consumption trends, technological adoption rates, infrastructure development, and policy frameworks. It highlights leading countries in terms of production, demand, and innovation, including China, the United States, Japan, Germany, and South Korea.

Applications of consumer electronics covered include personal entertainment, healthcare integration, smart home automation, education technology, and mobile communication. The report also identifies shifts toward low-energy, sustainable designs and modular component systems that enable repairability and longer product lifespans. Additionally, the analysis includes a focus on technology-driven market drivers such as 5G connectivity, IoT frameworks, advanced sensor integration, and smart software ecosystems. Niche segments like augmented reality devices and smart rings are also reviewed, reflecting the market's rapid diversification.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1396 Million |

|

Market Revenue in 2032 |

USD 2046.86 Million |

|

CAGR (2025 - 2032) |

4.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End‑User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Specialized Bicycle Components, Trek Bicycle Corporation, Salsa Cycles, Cannondale (part of Dorel Sports but operates independently), Kona Bicycle Co., Giant Manufacturing Co., Surly Bikes, Bombtrack Bicycle Co., Marin Bikes, Norco Bicycles |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |