Reports

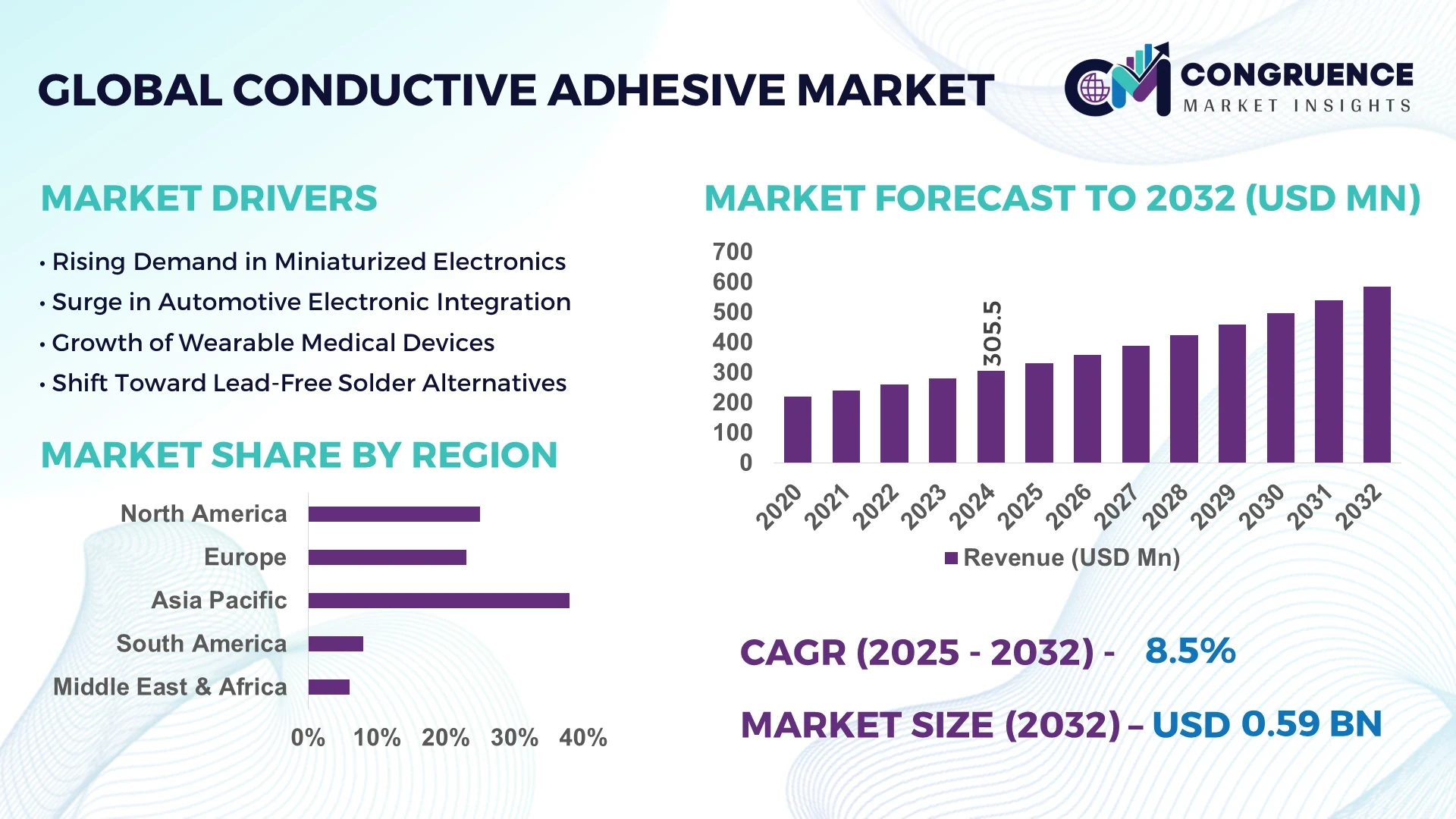

The Global Conductive Adhesive Market was valued at USD 305.45 Million in 2024 and is anticipated to reach a value of USD 585.35 Million by 2032 expanding at a CAGR of 8.47% between 2025 and 2032.

The United States dominates the conductive adhesive marketplace, driven by its advanced electronics manufacturing sector and high demand for miniaturized and flexible electronic devices. The market in this region benefits from significant investments in research and development for innovative conductive materials used in automotive, aerospace, and consumer electronics applications.

The conductive adhesive market is witnessing robust growth due to rising adoption in electronics assembly, renewable energy sectors, and medical devices. In 2024, the demand for silver-based conductive adhesives accounted for over 55% of the total market share, owing to their superior electrical conductivity and reliability. Asia-Pacific is also a major contributor with over 35% of the global market, fueled by growing electronic manufacturing hubs in China, Japan, and South Korea. The increasing use of conductive adhesives in flexible printed circuit boards and wearable electronics is driving technological advancements. Additionally, environmentally friendly conductive adhesives with lower curing temperatures and improved mechanical properties are gaining traction in various industrial applications, enhancing overall market dynamics.

Artificial intelligence (AI) is playing a crucial role in transforming the conductive adhesive market by accelerating product development, quality control, and application optimization. AI-powered predictive analytics and machine learning algorithms enable manufacturers to fine-tune adhesive formulations based on specific electrical and mechanical performance requirements, minimizing trial-and-error cycles and reducing production time. Smart manufacturing systems equipped with AI monitor real-time production parameters such as viscosity, curing time, and temperature to ensure consistent adhesive quality, enhancing yield rates and reducing material wastage.

Moreover, AI-driven image recognition and defect detection technologies help identify microscopic flaws in adhesive layers during electronics assembly, which is critical for high-reliability sectors such as aerospace and automotive electronics. These AI tools increase precision in dispensing conductive adhesives on delicate circuit boards, thereby improving product reliability and longevity. The integration of AI in research also accelerates the discovery of novel conductive materials by analyzing vast datasets of chemical properties and performance metrics, guiding the development of adhesives with enhanced conductivity and environmental resistance. AI-enabled robotics further streamline the manufacturing process by automating the application of conductive adhesives in complex geometries, ensuring uniform thickness and adhesion. This technology reduces human error and increases production throughput, essential for scaling up flexible electronics and wearable device manufacturing. Overall, AI adoption in the conductive adhesive market enhances innovation, quality assurance, and operational efficiency, positioning the industry for rapid growth amid evolving electronic and industrial demands.

“In 2024, a leading adhesive manufacturer integrated AI-powered process control systems to optimize the curing process of silver-based conductive adhesives, resulting in a 20% reduction in production defects and a 15% increase in throughput.”

The increasing global demand for advanced electronic products such as smartphones, tablets, and wearable devices is a key growth driver for the conductive adhesive market. These adhesives provide superior electrical connectivity and mechanical bonding required for miniaturized and flexible circuit assemblies. For example, the global smartphone production reached over 1.3 billion units in 2024, contributing substantially to the demand for high-performance conductive adhesives. Additionally, rising investments in automotive electronics, including electric vehicles and driver-assistance systems, further drive the need for reliable conductive bonding solutions. The electronics industry's shift towards more compact and lightweight designs is directly boosting the demand for conductive adhesives over traditional soldering techniques.

Volatility in the prices of key raw materials such as silver, copper, and carbon, which are essential components of conductive adhesives, acts as a significant restraint on market growth. For instance, silver prices saw fluctuations exceeding 15% in 2024 due to global supply chain disruptions and geopolitical tensions. Such variability increases production costs for adhesive manufacturers and may lead to higher prices for end-users, potentially slowing adoption rates in cost-sensitive segments like consumer electronics and small-scale manufacturers. Moreover, the scarcity of certain raw materials in specific regions affects supply reliability, further complicating manufacturing and pricing strategies within the conductive adhesive market.

The renewable energy sector, particularly solar photovoltaic (PV) and wind energy, presents substantial growth opportunities for conductive adhesives due to their role in efficient electrical connections and environmental resistance. In 2024, solar panel installations worldwide surpassed 150 GW, creating high demand for conductive adhesives capable of withstanding harsh outdoor conditions. Similarly, the growing medical devices market, driven by aging populations and technological advancements in diagnostic and monitoring equipment, requires biocompatible and highly reliable conductive adhesives. These industries’ expanding use of conductive adhesives to replace traditional metal soldering methods opens up new avenues for product innovation and market penetration.

Conductive adhesive manufacturing and application involve complex processes that demand precise control over curing times, temperatures, and adhesive thickness to ensure optimal electrical and mechanical performance. Any inconsistency can lead to defects, impacting product reliability, especially in critical applications such as aerospace and automotive electronics. For example, defective adhesive application can result in circuit failures, necessitating costly rework or recalls. Additionally, maintaining consistent quality standards across large-scale production while incorporating new materials or formulations poses significant operational challenges for manufacturers. These technical difficulties require ongoing investment in advanced equipment and skilled personnel, increasing operational expenditures and entry barriers for new market entrants.

• Expansion of Flexible and Wearable Electronics: The conductive adhesive market is experiencing significant growth due to the rising adoption of flexible and wearable electronic devices. These devices require adhesives that provide excellent electrical conductivity while maintaining flexibility and durability under repeated bending and stretching. In 2024, shipments of wearable electronics surpassed 450 million units globally, fueling demand for advanced conductive adhesives specifically formulated for soft substrates and flexible circuits. This trend is accelerating innovation in low-temperature curing adhesives that preserve component integrity.

• Growth in Electric Vehicle (EV) Electronics: The rapid expansion of the electric vehicle market is driving increased use of conductive adhesives in battery management systems, sensors, and power electronics. Conductive adhesives offer advantages over traditional soldering by enabling lighter, more compact assemblies and enhancing thermal management. By 2024, electric vehicle sales accounted for over 10% of global new car sales, creating substantial demand for high-performance conductive bonding materials that meet stringent automotive standards for durability and conductivity.

• Shift Toward Environmentally Friendly Formulations: Sustainability concerns are prompting manufacturers to develop eco-friendly conductive adhesives with reduced volatile organic compounds (VOCs) and lower curing temperatures. Water-based and bio-based adhesive formulations are gaining popularity in electronics and medical device applications. These greener adhesives not only comply with tightening environmental regulations but also reduce energy consumption during production, contributing to lower carbon footprints in manufacturing processes.

• Integration of Automated Dispensing and Inspection Technologies: Advances in automation are revolutionizing conductive adhesive application processes. Automated dispensing systems with precision control enable consistent adhesive layer thickness and placement, critical for miniaturized electronic components. Additionally, AI-driven inspection tools detect defects such as voids or uneven coverage in real time, ensuring higher yield rates and product reliability. The adoption of such technologies is increasing, especially in high-volume manufacturing hubs in Asia-Pacific and North America.

The conductive adhesive market is segmented by type, application, and end-user, each offering unique insights into industry trends and growth potential. Key types include silver-based, carbon-based, and copper-based conductive adhesives, with silver-based adhesives dominating due to superior conductivity. Application segments span electronics manufacturing, automotive, renewable energy, and medical devices, with electronics manufacturing maintaining the largest share. End-user segments cover individual consumers, automotive manufacturers, electronics OEMs, and healthcare providers, reflecting diverse demand drivers. Understanding these segments helps identify areas of robust growth and innovation within the market.

The conductive adhesive market is primarily divided into silver-based, carbon-based, and copper-based adhesives. Silver-based adhesives lead the market, capturing over 55% of the revenue share in 2024, owing to their excellent electrical conductivity, thermal stability, and reliability in high-performance applications such as automotive electronics and aerospace. Carbon-based adhesives are gaining traction due to their lower cost and good conductivity, representing about 25% of the market share. These are increasingly used in consumer electronics and flexible circuits where cost efficiency is critical. Copper-based conductive adhesives are the fastest growing segment, expanding rapidly due to copper’s affordability and improved oxidation resistance when combined with protective coatings. The demand for copper-based adhesives is rising especially in renewable energy and LED manufacturing, where they offer a cost-effective alternative to silver.

Electronics manufacturing remains the dominant application segment for conductive adhesives, accounting for nearly 60% of market usage in 2024. This is driven by the increasing complexity of circuit designs and miniaturization of devices, which require adhesives that ensure strong electrical connections without the heat damage associated with traditional soldering. Automotive applications follow closely, leveraging conductive adhesives for electric vehicle batteries, sensors, and infotainment systems, contributing over 20% of market consumption. The renewable energy sector is the fastest growing application segment, as conductive adhesives are essential for efficient solar panel interconnections and wind turbine electronics. Medical device manufacturing is also expanding, driven by demand for biocompatible adhesives used in diagnostics and wearable health monitoring devices.

The electronics OEM segment leads the conductive adhesive market, driven by the massive production of consumer electronics such as smartphones, tablets, and laptops. OEMs accounted for approximately 55% of the end-user market share in 2024 due to their focus on high-volume manufacturing and stringent quality requirements. Automotive manufacturers represent a significant and fast-growing segment, increasingly adopting conductive adhesives in electric vehicles and advanced driver-assistance systems to reduce weight and improve thermal management. The healthcare sector is emerging as a promising end-user, utilizing conductive adhesives in medical implants, diagnostic equipment, and wearable devices, which demand high reliability and biocompatibility. Additionally, small- and medium-sized electronics manufacturers are gradually adopting conductive adhesives, seeking cost-effective solutions for assembly and connectivity.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, Latin America is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2025 and 2032.

Asia-Pacific’s dominance is fueled by rapid industrialization, a booming electronics manufacturing sector, and rising adoption of electric vehicles in countries like China, Japan, and South Korea. The region also leads in renewable energy installations, further increasing demand for conductive adhesives. Meanwhile, Latin America’s growth is driven by expanding automotive manufacturing and rising infrastructure investments. North America and Europe hold substantial shares due to advanced electronics industries and stringent environmental regulations encouraging green adhesive technologies.

"Innovations Driving North America’s Conductive Adhesive Market Growth"

North America’s conductive adhesive market is expanding with growing demand in automotive electronics and aerospace industries. In 2024, electric vehicle registrations surpassed 2 million units, boosting the need for conductive adhesives in battery packs and sensor assemblies. The region also leads in healthcare technology, where conductive adhesives are integral in wearable medical devices and diagnostics. U.S. manufacturers are investing heavily in R&D for low-temperature curing adhesives to improve energy efficiency. Canada’s renewable energy projects further stimulate demand for conductive adhesives, especially in solar panel production. The robust electronics OEM base in the U.S. continues to prioritize adhesives that offer reliability and reduced manufacturing complexity.

"Sustainability and Precision Manufacturing Shaping Europe’s Market"

Europe’s conductive adhesive market is characterized by its focus on eco-friendly formulations and precision manufacturing techniques. Countries like Germany and France have integrated strict environmental regulations, pushing manufacturers to develop water-based and low-VOC adhesives. In 2024, Europe accounted for approximately 25% of global conductive adhesive consumption, driven largely by the automotive and electronics sectors. The rise in electric vehicle production—over 1.5 million units registered in 2024—has increased demand for conductive adhesives that meet rigorous safety standards. Additionally, the region’s growing renewable energy capacity, with wind and solar installations rising steadily, creates significant opportunities for adhesive suppliers.

"Rapid Industrialization and Electronics Manufacturing Surge in Asia-Pacific"

Asia-Pacific dominates the conductive adhesive market, fueled by massive electronics manufacturing hubs in China, South Korea, and Japan. In 2024, the region produced more than 60% of the world’s consumer electronics, driving substantial demand for conductive adhesives. The electric vehicle market in China alone surpassed 6 million units in 2024, reinforcing the use of adhesives in battery systems and electronic components. India and Southeast Asia are also emerging as significant markets due to rising industrial automation and solar energy projects. Local manufacturers are focusing on developing cost-effective copper-based adhesives to cater to the price-sensitive markets while maintaining conductivity and durability.

"Emerging Automotive and Electronics Sectors Boost South America"

South America’s conductive adhesive market is witnessing steady growth, driven by expanding automotive production and consumer electronics demand. Brazil leads the region with over 1 million new electric vehicle sales recorded in 2024, catalyzing the use of conductive adhesives in battery management and sensor technology. Argentina and Chile are growing markets for renewable energy installations, further increasing demand for conductive adhesives in solar panel manufacturing. While still developing compared to Asia-Pacific and North America, South America’s increasing infrastructure investments and gradual adoption of smart electronics in households and industries present new growth avenues for adhesive manufacturers.

"Infrastructure Development and Renewable Energy Expansion in Middle East & Africa"

The Middle East & Africa region is gaining momentum in the conductive adhesive market, supported by increasing infrastructure projects and renewable energy deployments. Countries like the UAE and Saudi Arabia are investing heavily in smart city initiatives that incorporate advanced electronics requiring conductive adhesives. Solar energy capacity in the region has grown by over 20% in 2024, creating demand for adhesives with high thermal and electrical conductivity. Africa’s growing mobile device penetration and expanding automotive industry are further encouraging market growth. Manufacturers are focusing on developing conductive adhesives tailored for harsh environmental conditions typical in the region, such as high temperatures and dust exposure.

China (26%): Leading due to its massive electronics manufacturing sector and rapid adoption of electric vehicles driving conductive adhesive demand.

United States (18%): Strong presence in advanced electronics, aerospace, and automotive industries fuels consistent market dominance.

The conductive adhesive market is highly competitive with several key global players investing significantly in R&D to innovate advanced adhesive formulations that meet diverse industrial requirements. Companies are focusing on developing conductive adhesives that offer improved thermal stability, electrical conductivity, and environmental safety. Strategic partnerships and mergers are common to expand product portfolios and geographic reach. The market also witnesses continuous introduction of new products aimed at specialized applications such as flexible electronics, medical devices, and renewable energy. Manufacturers are increasingly adopting sustainable production processes and water-based adhesives to comply with stringent environmental regulations. Competitive pricing, product quality, and customer service are critical factors influencing market positioning. Furthermore, the rise in demand for lightweight and miniaturized electronic devices compels companies to enhance adhesive performance, driving intense competition in the sector.

Henkel AG & Co. KGaA

3M Company

Dow Inc.

H.B. Fuller Company

Master Bond Inc.

Panacol-Elosol GmbH

Permabond LLC

Advanced Adhesive Technologies Ltd.

LORD Corporation

Creative Materials Inc.

The conductive adhesive market is witnessing significant technological advancements that are enhancing product efficiency and expanding application possibilities. Recent innovations focus on improving electrical conductivity, thermal management, and environmental safety. One of the leading technological trends is the development of silver and carbon-based conductive adhesives, which provide superior conductivity while reducing reliance on expensive metals. Nano-silver particles and graphene are increasingly integrated into adhesive formulations to boost performance at lower filler concentrations, resulting in lighter and more flexible electronic assemblies. Additionally, advancements in curing technologies, such as UV-curable and heat-curable adhesives, enable faster processing times and better control over adhesive properties. These innovations help manufacturers meet the growing demand for high-precision electronics in sectors like aerospace, automotive, and consumer electronics. Water-based conductive adhesives are gaining traction due to their eco-friendly nature, reducing volatile organic compound (VOC) emissions during manufacturing.

The integration of conductive adhesives in flexible and wearable electronics is another key technology trend. Adhesives that maintain conductivity under mechanical stress and bending are critical for the growth of these markets. Moreover, improvements in thermal interface materials embedded with conductive adhesives are enhancing heat dissipation in compact devices, supporting the miniaturization trend. Overall, technology-driven enhancements in raw materials, curing processes, and functional properties are shaping the future of the conductive adhesive market by enabling more reliable, cost-effective, and sustainable solutions across various industries.

In September 2024, Panacol introduced Elecolit 3648, a one-component electrically conductive adhesive designed for flexible perovskite and organic photovoltaic modules. This adhesive offers excellent adhesion to various plastics and cures at low temperatures, addressing the growing need for flexible, durable adhesives in temperature-sensitive solar technologies.

In May 2024, Azelis launched ARALDITE GY 40100, an advanced electrically conductive epoxy resin incorporating 2 wt% MIRALON conductive filler. This innovative formulation enhances adhesive properties, providing improved conductivity and processing ease without the use of airborne nanomaterials.

In October 2024, Creative Materials Inc. unveiled two advanced one-component, electrically conductive die-attach adhesives: 110-19(SD) and 129-50LS-2. These products are designed to replace outdated polyimide adhesives, offering superior durability and enhanced bond strength, catering to the evolving needs of the semiconductor industry.

In June 2023, Polytec PT partnered with Bostik to launch a new range of thermal conductive adhesives (TCAs) aimed at efficient thermal management in cell-to-pack battery configurations used in e-mobility applications. This collaboration addresses the increasing demand for advanced materials in electric vehicle battery systems.

The scope of the Conductive Adhesive Market report encompasses a detailed analysis of product types, applications, and end-user industries worldwide. It covers key segments such as silver-based, carbon-based, and other metal-based conductive adhesives, highlighting their performance characteristics, electrical conductivity, and thermal management capabilities. The report further explores the use of conductive adhesives in critical applications including electronics assembly, automotive manufacturing, renewable energy systems, and medical devices, reflecting the growing adoption across diverse sectors.

Additionally, the report examines regional market dynamics, focusing on major markets like North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing insights into market size, growth drivers, and competitive landscape within these regions. It also identifies emerging trends such as flexible electronics and wearable devices, which are significantly influencing the demand for advanced conductive adhesives with enhanced flexibility and reliability.

Furthermore, the report evaluates technological advancements in adhesive formulations, curing methods, and application techniques that improve adhesion strength, electrical performance, and environmental sustainability. Key factors such as regulatory frameworks, raw material availability, and environmental impact assessments are also analyzed to provide a comprehensive understanding of the market's future trajectory. This extensive scope enables stakeholders, including manufacturers, suppliers, and investors, to make informed decisions and strategize effectively in the evolving conductive adhesive landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 305.45 Million |

|

Market Revenue in 2032 |

USD 585.35 Million |

|

CAGR (2025 - 2032) |

8.47% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Henkel AG & Co. KGaA, 3M Company, Dow Inc., H.B. Fuller Company, Master Bond Inc., Panacol-Elosol GmbH, Permabond LLC, Advanced Adhesive Technologies Ltd., LORD Corporation, Creative Materials Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |