Reports

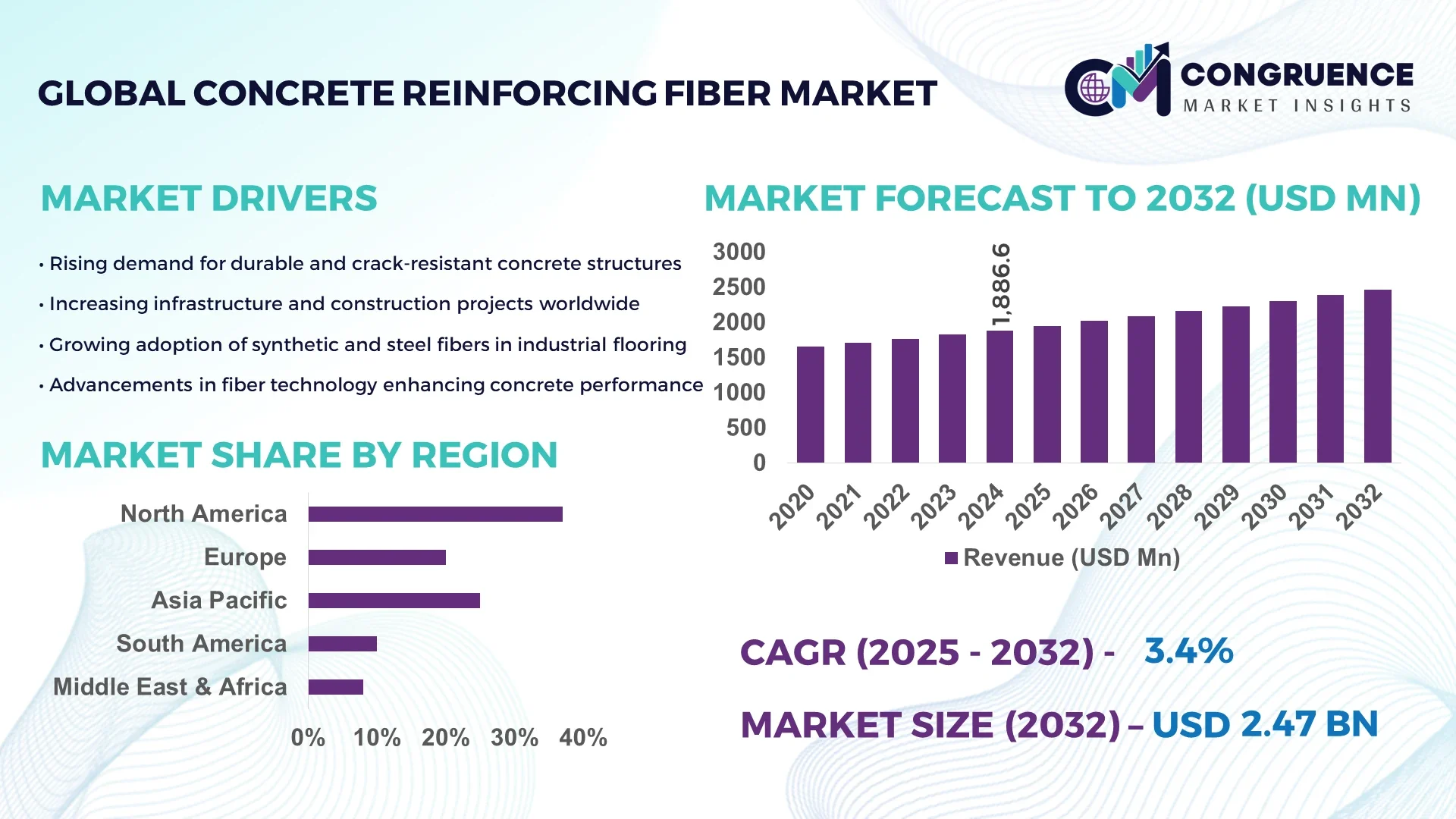

The Global Concrete Reinforcing Fiber Market was valued at USD 1886.63 Million in 2024 and is anticipated to reach a value of USD 2465.2 Million by 2032 expanding at a CAGR of 3.4% between 2025 and 2032. The growth is driven by increasing infrastructure investments and the rising need for durable and sustainable concrete solutions in both commercial and industrial projects.

The United States dominates the global concrete reinforcing fiber market, supported by advanced manufacturing facilities, extensive R&D investment, and robust adoption in transportation, defense, and civil construction projects. The country has over 250 operational fiber-reinforced concrete production facilities, with annual capacity exceeding 1.5 million metric tons. U.S. construction projects increasingly specify macro-synthetic and steel fibers, with an adoption rate of nearly 62% in large-scale highway and bridge applications by 2024, driven by ongoing infrastructure renewal and technological integration such as automated fiber dispersion systems.

• Market Size & Growth: Valued at USD 1886.63 million in 2024, projected to reach USD 2465.2 million by 2032, expanding at a CAGR of 3.4%, driven by the growing demand for high-performance concrete materials across urban infrastructure projects.

• Top Growth Drivers: 48% adoption of fiber-reinforced concrete in urban construction, 37% efficiency improvement in crack control, and 29% enhancement in load-bearing performance.

• Short-Term Forecast: By 2028, average concrete lifecycle cost reduction expected to reach 18% due to improved fiber-matrix compatibility and automated fiber dosing technologies.

• Emerging Technologies: Advancements in basalt and carbon fiber integration, nanofiber reinforcement, and automated dispersion systems are enhancing structural uniformity and performance reliability.

• Regional Leaders: North America, Europe, and Asia-Pacific expected to collectively reach USD 1.8 billion by 2032, with Asia-Pacific showing rapid adoption in smart city and infrastructure projects.

• Consumer/End-User Trends: Growing utilization across residential, industrial, and transportation sectors, with high adoption among contractors seeking longer service life and minimal maintenance costs.

• Pilot or Case Example: In 2024, a U.S. highway restoration project using macro-synthetic fibers demonstrated a 25% reduction in surface cracking and 15% faster project completion.

• Competitive Landscape: BASF SE holds approximately 14% market share, followed by Sika AG, Owens Corning, Bekaert SA, and Nycon Corporation leading through innovation and regional capacity expansion.

• Regulatory & ESG Impact: Sustainability mandates and green construction regulations in the EU and North America are accelerating fiber-based reinforcement usage over traditional rebar solutions.

• Investment & Funding Patterns: Over USD 420 million invested globally since 2023 in advanced fiber production lines and automated blending systems for infrastructure-grade concrete.

• Innovation & Future Outlook: Future growth driven by bio-based fiber research, hybrid reinforcement systems, and integration with 3D concrete printing technologies for next-generation construction solutions.

The Concrete Reinforcing Fiber market is witnessing increasing traction across transportation, defense, and industrial sectors, with key innovations in macro-synthetic fiber manufacturing and enhanced durability composites. Recent product launches emphasize high thermal stability and corrosion resistance. Environmental and regulatory frameworks promoting low-carbon construction materials are reshaping procurement standards globally. Rapid adoption in Asia-Pacific and the Middle East, coupled with digitized quality control systems and predictive maintenance technologies, is expected to strengthen the market outlook through 2032.

The strategic relevance of the Concrete Reinforcing Fiber Market lies in its ability to redefine modern infrastructure performance standards by improving durability, sustainability, and lifecycle efficiency. As urbanization accelerates and smart city initiatives expand globally, the adoption of advanced fiber-reinforced materials is transforming concrete applications in bridges, tunnels, and high-rise structures. Carbon fiber-reinforced composites deliver a 42% improvement in tensile strength compared to conventional steel mesh, enabling lighter yet more resilient concrete structures. North America dominates in volume, while Europe leads in adoption with 58% of enterprises integrating fiber-enhanced concrete systems into public infrastructure projects.

By 2028, AI-enabled process optimization and automated fiber blending are expected to cut production wastage by 23% and improve concrete homogeneity by 17%. Firms are committing to ESG-driven goals such as a 35% reduction in carbon emissions and 25% recycling of fiber-reinforced waste by 2030 to meet green construction mandates. In 2024, Japan achieved a 21% improvement in construction time through robotic placement of macro-synthetic fibers in commercial foundations, demonstrating measurable efficiency gains. Looking forward, the Concrete Reinforcing Fiber Market is positioned as a cornerstone of resilient infrastructure, environmental compliance, and sustainable construction innovation across both developed and emerging economies.

The surge in global infrastructure modernization projects is a primary driver for the Concrete Reinforcing Fiber Market. Governments worldwide are prioritizing durable and sustainable materials for highways, airports, and bridges. In 2024, over 68% of new public construction projects in Asia-Pacific adopted fiber-reinforced concrete for its enhanced crack control and load distribution benefits. Technological advances in macro-synthetic and basalt fiber integration have improved tensile performance by nearly 35%, reducing maintenance costs and extending asset lifespan. As construction firms aim to achieve 20–30% longer structure durability, fiber reinforcement is emerging as a preferred material across public infrastructure, industrial flooring, and defense construction applications.

One of the major restraints impacting the Concrete Reinforcing Fiber Market is the volatility of raw material costs, especially for steel, polypropylene, and carbon fibers. The lack of global standardization in fiber quality, length, and dispersion also creates inconsistencies in performance and complicates large-scale adoption. Between 2023 and 2024, steel fiber prices fluctuated by nearly 18%, directly affecting production budgets for manufacturers and contractors. Smaller regional suppliers face challenges meeting international quality benchmarks, leading to project delays and higher operational costs. Additionally, limited interoperability between fiber types in concrete formulations restricts flexibility for end-users seeking tailored reinforcement solutions.

The transition toward sustainable and smart construction presents significant opportunities for the Concrete Reinforcing Fiber Market. Green infrastructure policies and smart city programs are driving the need for eco-efficient and low-maintenance materials. Between 2025 and 2030, the adoption of recycled polymer-based fibers is projected to increase by 40%, reducing environmental impact and promoting circular economy models. Integration of IoT-based quality monitoring systems in concrete mixing and fiber dispersion processes is also enhancing reliability and productivity. Emerging economies, particularly in Asia-Pacific and the Middle East, are allocating large-scale funding toward transport and energy infrastructure that increasingly favors fiber-reinforced composites for extended structural performance.

Despite its advantages, the Concrete Reinforcing Fiber Market faces challenges related to technical complexity and installation costs. Proper fiber dosage, orientation, and distribution are crucial for achieving uniform mechanical properties, often requiring advanced mixing systems and trained personnel. The initial investment for automated fiber blending units can range between USD 150,000 and USD 300,000, making it less accessible to smaller contractors. In 2024, installation inefficiencies led to an estimated 12% rise in project rework rates across developing regions. Moreover, limited awareness among builders about long-term performance benefits restricts the broader adoption of fiber-reinforced concrete, slowing market penetration in cost-sensitive sectors.

• Rise in Modular and Prefabricated Construction: The growing adoption of modular and prefabricated building methods is transforming the demand profile in the Concrete Reinforcing Fiber market. Approximately 55% of newly launched infrastructure projects in 2024 achieved measurable cost efficiencies through off-site prefabrication using fiber-reinforced concrete panels. Automated pre-bending and cutting systems have reduced labor dependency by nearly 28% and project timelines by up to 20%. This trend is particularly strong in Europe and North America, where high-precision fiber blending machines are being installed to meet construction quality and speed benchmarks.

• Expansion of Sustainable Fiber Solutions: The shift toward sustainable and recyclable fiber materials is gaining traction, with over 35% of manufacturers investing in bio-based or recycled polymer fiber formulations. Recycled polypropylene fibers now constitute nearly 18% of total fiber output, supporting low-carbon building strategies. In 2025, large-scale infrastructure projects in Asia-Pacific are projected to increase green fiber adoption by 30% compared to 2023. This evolution is reinforcing compliance with ESG commitments targeting up to 40% material recyclability by 2030.

• Integration of Automation and AI-Based Mixing Systems: Automation and AI-driven dosing technologies are enhancing concrete uniformity and performance in fiber-reinforced applications. Over 60% of major producers have incorporated AI-based fiber distribution control systems, achieving up to 15% improvement in tensile strength consistency and a 25% reduction in production wastage. These advancements enable real-time monitoring and predictive maintenance, minimizing errors and optimizing production cycles.

• Growing Use in Transportation and Infrastructure Projects: Demand for Concrete Reinforcing Fiber in transportation infrastructure is rising sharply, with more than 48% of new highway and bridge projects utilizing fiber-enhanced concrete in 2024. Macro-synthetic and steel fibers are improving fatigue resistance by 22% and extending structure lifespan by up to 15 years. The Asia-Pacific region is witnessing accelerated adoption, driven by government-backed programs aimed at replacing traditional steel mesh reinforcement in major rail, port, and urban mobility developments.

The Concrete Reinforcing Fiber Market is segmented by type, application, and end-user, reflecting a diverse adoption pattern across construction and infrastructure domains. Steel fibers remain the dominant type due to their superior tensile strength and load-bearing capability, accounting for the majority of structural applications. Macro-synthetic fibers are expanding rapidly, driven by their corrosion resistance and compatibility with precast concrete solutions. In terms of applications, industrial flooring and transportation infrastructure lead global adoption, collectively exceeding half of total utilization. End-user analysis shows construction and infrastructure developers representing the largest share, while industrial and defense sectors demonstrate growing preference for high-performance fiber composites in heavy-duty concrete reinforcement.

Steel fibers currently account for 47% of total adoption in the Concrete Reinforcing Fiber Market, maintaining dominance due to their strength and proven performance in high-load applications like bridges, pavements, and industrial floors. Synthetic fibers, primarily polypropylene and macro-synthetic variants, follow with 32% market share, offering lightweight, corrosion-resistant alternatives ideal for water-retaining structures and coastal constructions. Glass fibers contribute approximately 12% share, catering to decorative and architectural concrete products, while basalt and natural fibers collectively represent the remaining 9%, serving niche eco-friendly applications.

Among all, macro-synthetic fibers are the fastest-growing type, projected to expand at a 4.8% CAGR through 2032. Their increasing use is driven by low maintenance, enhanced crack resistance, and compliance with green construction mandates. The growing preference for blended hybrid systems—combining steel and synthetic fibers—further strengthens market adaptability across climates and project requirements.

Industrial flooring remains the leading application segment in the Concrete Reinforcing Fiber Market, accounting for 41% of global adoption due to the material’s high fatigue resistance and crack control performance. Transportation infrastructure—including highways, tunnels, and bridges—holds a 33% share, driven by ongoing public works programs emphasizing long-term durability and minimal repair frequency. Precast concrete applications follow with 16%, while residential and commercial constructions collectively comprise the remaining 10%.

The transportation segment is the fastest-growing application area, expanding at a 5.1% CAGR, propelled by global infrastructure modernization and government investment in sustainable mobility. Fiber-reinforced concrete provides up to 25% improved fatigue resistance compared to conventionally reinforced concrete, reducing maintenance cycles significantly. Industrial flooring adoption continues to benefit from automation and robotics-based fiber dispersion systems that improve precision and consistency.

Construction and infrastructure developers represent the leading end-user category, accounting for 53% of total market participation, driven by widespread integration of fiber reinforcement in highways, commercial buildings, and public utilities. Industrial manufacturers follow with 27%, utilizing fiber-reinforced concrete for flooring, heavy machinery foundations, and high-load structures. Defense and energy sectors contribute around 12%, adopting advanced fiber systems for bunkers, storage facilities, and wind turbine foundations. The remaining 8% includes water management and mining applications where enhanced crack resistance is critical.

The defense and energy sector is currently the fastest-growing end-user group, projected to expand at a 5.4% CAGR due to rising adoption in blast-resistant and corrosion-prone structures. Increasing investment in renewable infrastructure—particularly offshore wind platforms—is accelerating demand for high-durability fiber composites. Meanwhile, private construction contractors are leveraging automation and 3D concrete printing technologies to enhance project efficiency and cost control.

North America accounted for the largest market share at 37% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.8% between 2025 and 2032.

Europe followed closely with 28% share, driven by sustainability mandates and infrastructure modernization. South America and the Middle East & Africa collectively represented around 14% of global consumption, reflecting growing adoption in energy and transportation sectors. In 2024, global consumption volumes surpassed 1.3 million metric tons, with the United States, China, and Germany being the top producing regions. While North America leads in technological adoption and standardization, Asia-Pacific’s rising demand from smart infrastructure projects and urban housing developments positions it as a major future growth hub for concrete reinforcing fiber utilization.

North America held a 37% share of the global Concrete Reinforcing Fiber Market in 2024, supported by strong demand from industrial, defense, and transportation sectors. The U.S. and Canada have integrated high-strength steel and synthetic fibers across more than 60% of major highway renovation projects. Federal infrastructure funding programs and state-level green construction incentives are encouraging wider use of fiber-based materials to extend service life and minimize maintenance costs. Local manufacturers such as Nycon Corporation are investing in automated fiber blending technologies, improving consistency by 18% across production batches. Consumer behavior in the region favors performance reliability, with enterprises in heavy infrastructure and logistics adopting fiber-reinforced concrete at higher rates compared to residential users.

Europe captured 28% of the global Concrete Reinforcing Fiber Market in 2024, with Germany, the UK, and France leading adoption. Strict EU directives on reducing CO₂ emissions and increasing recyclability have prompted the use of synthetic and basalt fibers in both public and private projects. The European Construction Products Regulation and Green Deal commitments continue to promote sustainable material adoption, targeting a 40% reduction in embodied carbon by 2030. Technological advancements such as fiber-integrated precast systems are gaining traction, especially in Western Europe’s smart city developments. Consumer behavior reflects growing awareness of sustainability, with 52% of enterprises prioritizing eco-compliant concrete reinforcement materials. Bekaert SA remains a notable regional player, expanding its high-tensile steel fiber line to meet regional quality standards and infrastructure demand.

Asia-Pacific accounted for 29% of total market volume in 2024, positioning it as the fastest-growing regional market. China, India, and Japan dominate consumption, collectively contributing over 70% of regional demand. Rapid urbanization, smart city infrastructure, and transportation corridor expansions are key factors stimulating fiber integration in concrete structures. Local players in China are scaling polymer fiber production capacity by over 25% annually to meet construction and manufacturing sector demand. Technological hubs in South Korea and Japan are deploying robotic concrete placement systems and AI-driven material testing frameworks. Consumer preferences across Asia-Pacific emphasize cost efficiency and high output rates, with rising acceptance of hybrid macro-synthetic fibers for industrial flooring and bridge decks.

South America represented approximately 8% of the global Concrete Reinforcing Fiber Market in 2024, led by Brazil and Argentina. Government-backed infrastructure investments and rising private-sector participation in renewable energy projects are creating strong demand for durable, corrosion-resistant materials. Brazil’s highway and port development programs have integrated fiber-reinforced concrete across 35% of new construction since 2023. Regional players are focusing on cost-effective polypropylene fiber formulations tailored for tropical climates, improving concrete resilience by 22% against humidity-related degradation. Consumer trends favor adaptable, low-maintenance materials, particularly in commercial and logistics construction. National trade policies supporting domestic production of construction fibers continue to strengthen the local supply chain across the region.

The Middle East & Africa accounted for around 6% of the global Concrete Reinforcing Fiber Market in 2024, with the UAE, Saudi Arabia, and South Africa driving demand. Mega infrastructure projects such as NEOM and urban expansion in Dubai are incorporating macro-synthetic and steel fiber systems to enhance structural performance and reduce construction time by 20%. Local government initiatives supporting energy-efficient building codes are stimulating material innovation and regional fiber manufacturing capacity growth. Firms like Emirates Concrete Innovations are investing in basalt and polymer fiber lines tailored for desert climate conditions. Consumer behavior reflects strong institutional demand, especially within the oil, gas, and industrial construction sectors, where lifecycle sustainability is increasingly prioritized.

• United States – 23% Market Share: Dominates due to advanced manufacturing infrastructure, large-scale public construction investments, and early adoption of fiber-blending automation.

• China – 19% Market Share: Leads in production capacity and demand from industrial and transportation megaprojects supported by ongoing infrastructure expansion initiatives.

The global Concrete Reinforcing Fiber market demonstrates a moderately consolidated structure, with the top five companies collectively accounting for approximately 52% of the total market share in 2024. Around 60 active players are currently competing across key regions, including multinational building material producers and regional fiber innovators. Strategic moves such as mergers, product line expansions, and cross-border collaborations are reshaping competitive positioning. Nearly 40% of major participants have introduced hybrid fiber compositions—integrating steel and synthetic materials—to enhance concrete strength and reduce microcracking. Furthermore, advancements in corrosion-resistant and high-tensile fibers have extended infrastructure durability by up to 25%, aligning with green construction trends. Digital transformation initiatives, including smart production lines and AI-based quality control, are improving production consistency across global facilities. The competitive environment remains driven by sustainability, product differentiation, and customized performance solutions catering to high-demand sectors such as transportation and energy infrastructure.

Owens Corning

GCP Applied Technologies Inc.

ABC Polymer Industries, LLC

Nycon Corporation

Euclid Chemical Company

Propex Operating Company, LLC

Forta Corporation

Elkem ASA

CHRYSO Group

Hunan Sunshine Steel Fiber Co., Ltd.

Hunan Xianghui Metal Fiber Co., Ltd.

Fibrin SA

Technological innovation in the Concrete Reinforcing Fiber market is centered around enhancing material performance, manufacturing efficiency, and environmental sustainability. Advanced fiber processing technologies such as automated extrusion, plasma surface treatment, and high-tensile polymer modification are improving fiber-matrix bonding by nearly 35%, significantly increasing crack resistance and structural durability. Nanofiber reinforcement, utilizing fibers below 100 nanometers in diameter, is gaining traction, particularly in high-strength concrete applications where enhanced flexural strength of up to 40 MPa is achieved.

Digitalization is reshaping production workflows, with approximately 45% of leading manufacturers adopting Industry 4.0 automation systems that ensure consistent fiber length, uniform dispersion, and reduced production waste by 18%. AI-driven quality control platforms are being implemented across fiber manufacturing units to detect micro-defects in real time, enhancing overall product reliability and compliance with construction standards.

Sustainability-focused technologies are also driving innovation. Around 28% of new product launches in 2024 incorporated recycled polymers or waste steel fibers, reducing carbon emissions per ton of output by up to 22%. 3D printing applications using fiber-reinforced concrete are expanding in infrastructure and modular construction, offering 20% faster build times and improved structural uniformity. Collectively, these technological advancements are reinforcing the market’s transition toward performance-driven, eco-efficient, and digitally optimized production ecosystems.

In April 2024, Sika AG opened a state-of-the-art synthetic macro-fiber production hub in Lima, Peru to support infrastructure and mining construction in Latin America, enabling on-site fiber production close to demand zones and reducing delivery lead-times.

In October 2024, Sika reported nine-month sales growth of 9.1 % in CHF (corresponding to 8.1 % organic growth) with Americas region showing 12.2 % rise in local currency, reflecting stronger uptake of fiber-enhanced concrete solutions in transportation and industrial segments.

In 2023, Bekaert SA announced expansion of steel-fiber production capacity in China with a new facility capable of producing 40,000 tons annually, aligning with rising demand for high-load industrial flooring and infrastructure reinforcement in Asia.

Also in 2024, Sika’s product brand Fibermesh launched an upgraded fiber-reinforced concrete portfolio from its Chattanooga, Tennessee facility (129,000 sq ft), enabling enhanced shotcrete and slab applications with improved energy-absorption and crack-control performance in U.S. construction projects.

The report on the Concrete Reinforcing Fiber Market covers a comprehensive analysis of the product types (steel fibers, macro-synthetic fibers, glass fibers, basalt and natural fiber composites) and segments them by maturity, performance characteristics, and niche applications. It examines applications such as industrial flooring, transportation infrastructure (highways, bridges, tunnels), precast concrete components, shotcrete, and residential/commercial construction, providing detailed insight into performance requirements and material selection criteria. End-user categories are addressed, including construction and infrastructure developers, industrial manufacturers, defense and energy sectors, and water & mining projects, with emphasis on adoption rates and usage behaviour. Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional consumption patterns, manufacturing hubs and emerging demand corridors. Technology focus areas include fiber manufacturing innovations (automated extrusion, nanofiber reinforcement, hybrid fiber systems), digital process adoption (AI-based quality-control, Industry 4.0 production lines) and sustainability metrics (recycled fiber content, carbon reduction strategies). The study further addresses regulatory and environmental drivers, infrastructure funding trends, and the competitive landscape—providing actionable insights for decision-makers evaluating product portfolios, manufacturing investment, regional market entry strategies and innovation partnerships. Emerging segments such as 3D-printed concrete with fiber reinforcement and smart sensor-embedded fiber systems are also explored within the report’s scope.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 1886.63 Million |

Market Revenue in 2032 | USD 2465.2 Million |

CAGR (2025 - 2032) | 3.4% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | BASF SE, Sika AG, Bekaert SA, Owens Corning, GCP Applied Technologies Inc., ABC Polymer Industries, LLC, Nycon Corporation, Euclid Chemical Company, Propex Operating Company, LLC, Forta Corporation, Elkem ASA, CHRYSO Group, Hunan Sunshine Steel Fiber Co., Ltd., Hunan Xianghui Metal Fiber Co., Ltd., Fibrin SA |

Customization & Pricing | Available on Request (10% Customization is Free) |