Reports

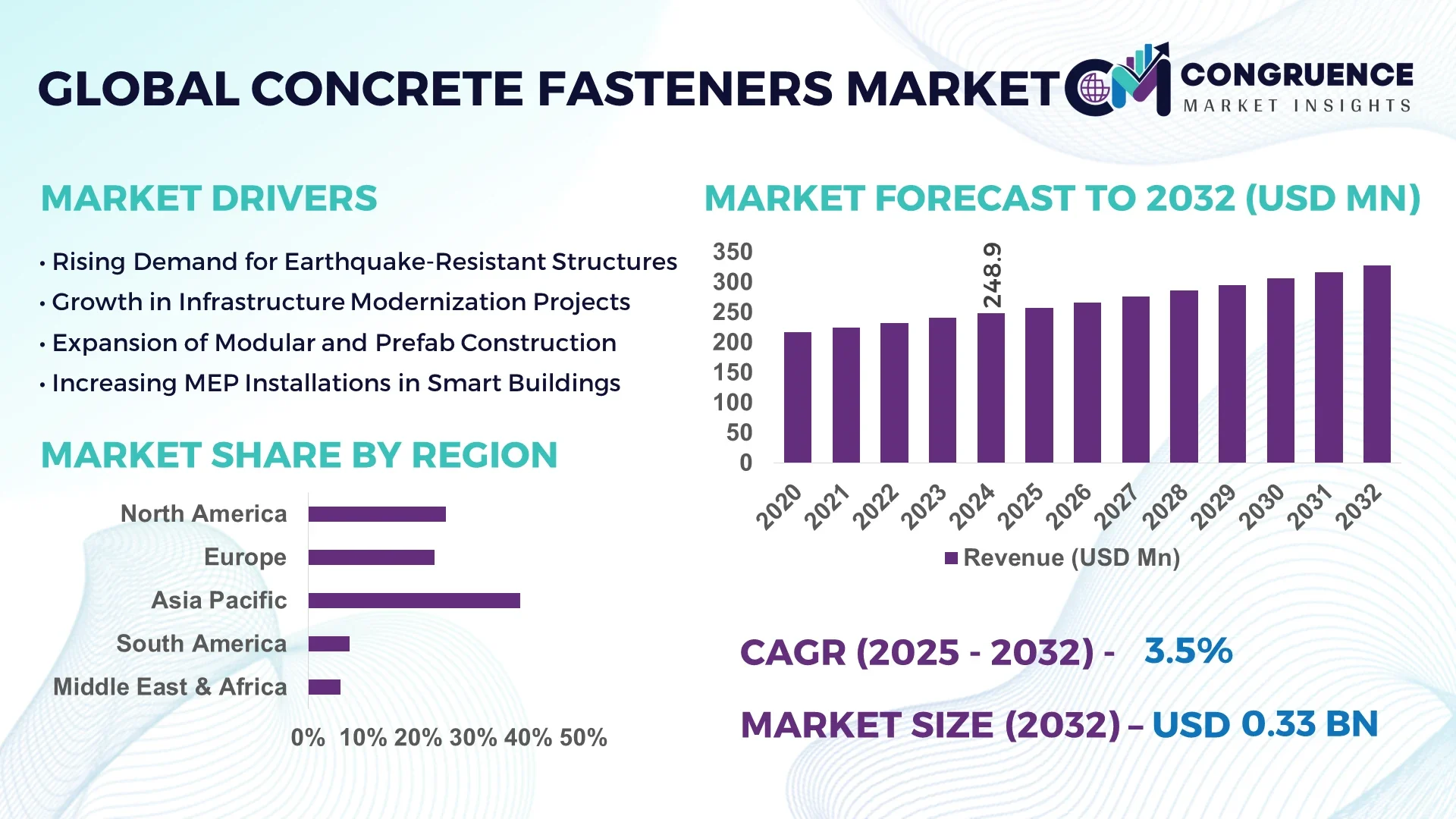

The Global Concrete Fasteners Market was valued at USD 248.9 Million in 2024 and is anticipated to reach a value of USD 327.8 Million by 2032 expanding at a CAGR of 3.5% between 2025 and 2032.

China supports advanced production lines producing high-strength concrete screws and sleeve anchors, with annual output exceeding 50 million units and investment in automation exceeding USD 75 million. These facilities cater to construction, infrastructure, and industrial applications, including seismic retrofit solutions and automated bonded anchor systems.

The Concrete Fasteners Market spans residential, commercial, industrial, and infrastructure sectors. Mechanical anchors (expansion, wedge, sleeve) lead unit volume, driven by new housing and renovation projects, while chemical anchors are expanding in industrial and infrastructure works due to stringent building standards. Recent innovations include pre-engineered fastening kits for modular construction, BIM integration for anchor specification, and corrosion-resistant coatings supporting green building mandates. Environmental regulations on volatile organic compounds have accelerated the shift to eco-friendly adhesives. North America and Europe continue to standardize seismic testing and wall anchoring norms, while Asia-Pacific demand surges alongside urbanization. Emerging trends include automated installation tools using torque-controlled drills and digital asset tracking of fastener performance. The outlook shows a drive toward smarter, sustainable anchoring systems integrated with digital construction workflows, appealing to infrastructure developers and decision-makers aiming to streamline installation processes and reliability.

AI is drastically improving production, installation, and asset monitoring in the Concrete Fasteners Market. In manufacturing plants, AI-powered vision systems inspect each fastener thread and coating defect at speeds of up to 120 units per second, reducing rejection rates by 18%. Predictive maintenance algorithms, analyzing torque data and motor vibrations, now forecast tool servicing needs, decreasing unplanned downtime in fastening equipment by 22%.

On-site, AI-integrated fastening tools record torque and angle in real time, ensuring each anchor is installed within spec limits. In pilot projects across Europe in 2024, AI feedback tools identified torque variance in 15% of anchor installations before concrete set, saving rework costs and enhancing structural safety. These tools sync cloud dashboards to give project managers oversight of fastener counts, performance diagnostics, and compliance reporting. Such data supports audit trails in critical infrastructure.

AI is also used in project planning: machine learning models analyze project blueprints and load requirements to specify the optimal fastener type and layout—automating over 60% of design time for anchor schedules. This speeds approval workflows, reduces human error, and aligns with automated off-site fabrication processes. As the Concrete Fasteners Market evolves toward integrated construction ecosystems, AI becomes a cornerstone for quality assurance, cost control, and digital reporting—benefiting decision-makers managing complex builds and infrastructure compliance.

“In 2024, a leading European fastening tool manufacturer introduced an AI-enabled torque analysis system that detected 15% of installation variances in real time, reducing rework by 12 % across pilot projects.”

New building codes in seismic regions mandate high tensile-strength anchors, prompting replacement of legacy fasteners. By 2024, over 68% of infrastructure projects specified hot-dip galvanized or epoxy-coated anchors to meet corrosion resistance and load requirements. These regulations drive manufacturers to expand production and qualify fasteners to ASTM and EN standards, ensuring acceptance in public tenders and reducing liability risks.

Certification for fastening products—covering tensile, shear, fire, and seismic testing—requires specialized labs and recurring tests. Laboratories charge USD 15,000–25,000 per anchor size tested, increasing costs for smaller manufacturers. This limits product variety in the market and raises final unit prices by around 8–10% compared to non-certified alternatives, impacting price-sensitive construction budgets.

With modular construction gaining traction, demand for pre-engineered anchor kits has surged by 35% since 2022. These kits bundle fasteners, installation guides, and BIM specs tailored to modules, enabling off-site assembly and rapid on-site installation, reducing labor hours by up to 40% on pilot modular residential blocks in China and North America.

Anchors require steel grades with strict chemical composition—e.g., 410 stainless or C45 carbon steel. Shortages drove lead times to 12–16 weeks in 2024, with price spikes of 14%. Coating materials like epoxy and zinc were also constrained, delaying product launches. These supply issues hinder fastener stock replenishment and disrupt project schedules, forcing buffer inventory and pushing clients to accept alternatives with shorter lead times but less performance.

Innovative Corrosion-Resistant Coatings: Chemical anchor alloys with dual-layer barrier coatings achieved a salt spray resistance of over 1,200 hours in 2024 tests. These coatings are increasingly specified by infrastructure clients to reduce maintenance cycles in coastal environments.

Digital Torque-Tool Integration: Over 15,000 AI-enabled torque tools were deployed in Europe and North America by mid-2024, enabling drill controllers and software to log installation angles and torque depth—cutting inspection time by 25% in commercial buildings.

Prefabricated Anchor Kits for Modular Builds: Usage of anchor kits in off-site modular production plants rose 30% in 2023–24. Kits include pre-cut anchors and installation documentation linked to building information models, reducing on-site errors by 17%.

Cloud-Based Anchor Asset Management: The installation of QR-coded anchor labels linked to cloud platforms doubled in 2024. Over 40 major sites in the U.S. invested in systems that automatically verify anchor certification, monitor installation counts, and trigger maintenance reminders—enhancing audit readiness and operational transparency.

The Concrete Fasteners Market is segmented by type, application, and end-user, offering a comprehensive understanding of demand dynamics and procurement behaviors across the value chain. On the product side, a broad range of anchors—mechanical and chemical—are used across commercial and infrastructure developments. Applications range from structural reinforcement and seismic retrofitting to HVAC system anchoring and prefabricated assembly. End-user insights reveal a strong reliance from the construction industry, with varying adoption across public infrastructure agencies, industrial plants, and modular housing developers. Segment-wise distinctions are becoming sharper with increased demand for high-performance and pre-engineered fastener systems, particularly in regulated environments. Innovation and automation are further shaping how specific segments adopt anchoring technologies, with smart tracking systems and AI-guided tools influencing selection criteria. Overall, segmentation reflects both technological advancements and practical field needs, providing industry professionals with strategic entry points for market engagement and investment decisions.

The product landscape of the Concrete Fasteners Market includes mechanical anchors (wedge, sleeve, drop-in), chemical anchors, powder-actuated fasteners, and screw anchors, among others. Mechanical anchors dominate the market due to their ease of installation, immediate load-bearing capacity, and wide availability in both carbon and stainless steel variants. They are widely used in structural connections and facade installations, particularly in commercial and public buildings.

Chemical anchors, while slightly more complex in installation, are the fastest-growing segment. Their increasing adoption is driven by their superior load transfer capabilities, high resistance to dynamic forces, and suitability for cracked concrete or high-load applications. These features are particularly valuable in seismic zones and bridge construction projects.

Other types, such as powder-actuated fasteners, are used in specific applications like fastening to steel or concrete without pre-drilling, especially in drywall or utility installations. Screw anchors are gaining traction in modular construction projects due to their reusability and cleaner finish. Each type brings distinct value propositions depending on the installation environment, substrate material, and structural demands.

Concrete fasteners find application across a range of sectors including structural construction, infrastructure development, mechanical and electrical system installation, and seismic retrofitting. Among these, structural construction is the leading application area, supported by the sheer volume of commercial buildings, warehouses, and high-rise projects requiring secure anchoring of structural elements.

The fastest-growing application segment is seismic retrofitting. This rise is influenced by updated building codes across North America, Japan, and parts of Europe, which now mandate anchoring solutions with proven seismic load performance. Fasteners certified for cracked concrete and cyclic loading are in particularly high demand.

Other key applications include HVAC and MEP (mechanical, electrical, plumbing) system installations, where fasteners are essential for pipe supports, duct mounting, and equipment installation. Public utilities and tunnel works also represent niche but growing application areas, particularly where safety and longevity are critical. Each application area is shaping product design, certification needs, and procurement priorities across the market.

The construction industry, particularly commercial and residential builders, remains the dominant end-user segment in the Concrete Fasteners Market. Their demand is sustained by a continuous pipeline of real estate developments and renovation projects that require reliable anchoring solutions for structural integrity and compliance with safety standards. Builders often specify mechanical or chemical fasteners during the planning phase, driven by architectural requirements and material compatibility.

The fastest-growing end-user segment is public infrastructure developers, including government agencies and contractors involved in bridges, transit systems, and public buildings. The increase in public infrastructure funding across regions like the U.S., China, and the Middle East has created heightened demand for high-performance anchors that meet stringent regulatory approvals and long-term durability expectations.

Other end-users include industrial facility operators, who require fasteners for plant maintenance and equipment mounting; modular housing manufacturers, who benefit from pre-bundled fastener kits; and utility service providers, where fasteners are used in energy distribution and communication networks. The diversity in end-user needs drives innovation, customization, and bundled service offerings in the concrete anchoring ecosystem.

Asia-Pacific accounted for the largest market share at 38.5% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

Rapid urbanization, widespread infrastructure development, and the surge in smart city projects have solidified Asia-Pacific’s leading role in the Concrete Fasteners Market. China and India are key contributors due to high-volume construction, public infrastructure investments, and evolving building standards. Meanwhile, North America’s growth is fueled by increasing investments in industrial modernization and a rebound in commercial construction. Enhanced safety regulations and the integration of digital tools for installation validation are also stimulating demand across both regions. In Europe, sustainability-driven retrofits and seismic safety regulations are creating favorable conditions. The Middle East & Africa and South America are emerging with niche growth potential, led by oil, gas, and transport sectors. Regional dynamics continue to evolve, influenced by regulatory frameworks, raw material availability, and localized product preferences.

North America captured approximately 26.8% of the global Concrete Fasteners Market in 2024, driven by consistent demand from the commercial, industrial, and residential construction sectors. The U.S. and Canada lead the region, with major demand arising from industrial facility upgrades, transport infrastructure development, and retrofitting of older buildings. Regulatory frameworks such as OSHA and IBC enforce stringent anchoring performance standards, which has led to increased reliance on certified fasteners for both new constructions and repairs. Additionally, federal incentives for energy-efficient retrofits have spurred the demand for chemical anchors in solar panel and equipment mounting. Technological advancements, including AI-integrated installation tools and digital torque tracking systems, are being adopted at scale across large commercial projects. These tools ensure accuracy and regulatory compliance, enhancing job site efficiency and safety—a key concern in North America’s fast-paced construction environment.

Europe holds nearly 21.3% of the global Concrete Fasteners Market, with Germany, France, and the United Kingdom emerging as leading contributors. The EU’s Green Deal framework and EN 1992-4 anchoring standards are accelerating the demand for environmentally compliant and high-strength anchoring solutions. German infrastructure and housing retrofits are driving growth in chemical anchor usage, especially in energy-efficient upgrades and seismic reinforcement. France is witnessing rising installations of prefabricated fastener kits in commercial developments. Across the region, smart tools for torque verification and AI-based fastening design software are helping contractors meet both performance and sustainability metrics. Programs from regulatory bodies such as EOTA and CE Marking further influence product design and material sourcing, ensuring compliance while fostering innovation in corrosion-resistant coatings and installation technology.

Asia-Pacific leads the global Concrete Fasteners Market in terms of volume, with China, India, and Japan accounting for over 38.5% of global market share in 2024. The region’s construction surge—spanning public infrastructure, smart cities, and industrial corridors—creates high-volume demand for wedge anchors, screw anchors, and chemical bonding systems. China, in particular, has emerged as a global production and consumption hub, with extensive government-driven housing and urban development programs. India’s expanding metro rail, highway, and airport projects are accelerating the use of high-strength mechanical anchors. Meanwhile, Japan focuses on precision anchoring systems tailored for seismic safety. Regional innovation hubs in Shenzhen and Tokyo are also producing torque-controlled fastener tools and corrosion-resistant materials adapted for extreme weather or seismic conditions. Together, these trends reflect the region’s push toward advanced fastening technologies integrated with long-term structural safety goals.

South America represents a growing segment of the Concrete Fasteners Market, with Brazil and Argentina being the key contributors. The region held approximately 6.8% of global market share in 2024. Demand is primarily driven by transportation infrastructure, commercial building construction, and renewable energy installations. Brazil’s government-led public works and highway projects are major consumers of sleeve and expansion anchors. Argentina’s wind and solar power growth has elevated the use of high-durability fasteners in turbine mounting and solar panel anchoring. Regional trade policies encouraging local manufacturing of construction hardware have also stimulated market activity. In addition, certification requirements for construction components under Mercosur standards have pushed manufacturers to improve quality and performance consistency, making locally manufactured fasteners more competitive in public and private tenders.

The Middle East & Africa (MEA) region accounted for 6.6% of the Concrete Fasteners Market in 2024, with UAE, Saudi Arabia, and South Africa leading in demand. Anchors are increasingly required in commercial and public infrastructure projects, including smart cities, airports, and oil and gas terminals. UAE’s focus on sustainable buildings and mega-projects like NEOM in Saudi Arabia has led to the use of pre-engineered fastener systems and smart installation tools. In Africa, South Africa’s urban development plans and manufacturing expansion are spurring demand for chemical anchors and screw-type fasteners. MEA countries are also witnessing technological modernization, with AI-based inspection tools and digital torque measurement systems gradually gaining ground. Trade partnerships with Asian and European producers are helping bridge supply gaps while encouraging local adaptation of advanced fastening technologies in extreme climate or geotechnical conditions.

China – 24.7% Market Share

High production capacity, robust government infrastructure investments, and dominant regional distribution networks.

United States – 18.3% Market Share

Strong end-user demand across industrial and commercial sectors supported by strict anchoring regulations and rapid adoption of smart installation tools.

The Concrete Fasteners Market features a competitive landscape with over 150 active players globally, ranging from large-scale manufacturers to specialized regional producers. Market participants are pursuing strategic differentiation through product innovation, geographic expansion, and value-added services. Prominent companies are investing in automated manufacturing lines, enabling higher production volumes with reduced defect rates. Partnerships between fastener producers and modular construction firms are becoming more common, with co-developed pre-packaged anchor kits designed for industrialized building systems.

Mergers and acquisitions continue to shape the competitive landscape, particularly in Europe and North America, where mid-tier manufacturers are consolidating to scale up production capabilities and expand their certified product portfolios. Innovation trends include the integration of smart installation systems that record torque and performance metrics, catering to the rising demand for real-time quality assurance. In Asia-Pacific, cost-competitive manufacturers are gaining traction by offering corrosion-resistant and value-engineered fasteners tailored for emerging economies. The market is highly quality- and regulation-driven, favoring companies with strong R&D, global logistics networks, and diverse portfolios across both mechanical and chemical anchoring solutions.

Hilti Corporation

ITW Construction Products

fischer Group of Companies

DEWALT (Stanley Black & Decker)

Simpson Strong-Tie Company, Inc.

EJOT Group

Sika AG

Powers Fasteners

MKT Fastening, LLC

RAWLPLUG S.A.

Würth Group

Ancon Ltd (Part of Leviat)

Technological advancements are transforming the Concrete Fasteners Market, primarily through automation, smart installation tools, and material engineering. One major trend is the adoption of torque-controlled power tools integrated with AI, which capture torque, depth, and angle data during anchor installation. These tools reduce installation errors by over 20% and ensure code-compliant fastening, especially in seismic and high-load environments.

Another innovation is the development of dual-layer anti-corrosion coatings offering protection for up to 1,200 hours in salt spray testing, which has become crucial in marine, infrastructure, and tunnel applications. Advanced polymer-based chemical anchors with low volatile organic compound (VOC) content are being adopted in markets with stringent green building regulations.

In manufacturing, robotic threading and high-speed automated coating lines have improved consistency and reduced production downtime. Digital simulation tools are also being used to model fastener behavior under load, optimizing anchor selection and placement in Building Information Modeling (BIM) workflows. Some companies have started integrating QR-coded fasteners that link to installation instructions and compliance certificates through cloud platforms, facilitating traceability and inspection. These technologies not only improve operational efficiency but also align with emerging construction demands for smart, sustainable, and digitally-enabled anchoring systems.

• In January 2024, Hilti introduced a smart anchor setting tool capable of torque tracking and cloud-based data logging. The system reduced installation errors by 21% in commercial construction field tests across Europe.

• In March 2024, Würth Group expanded its modular fastener line, launching a plug-and-anchor combo kit for prefab housing, which reduced jobsite anchoring time by up to 30%.

• In September 2023, fischer Group completed automation upgrades at its Germany facility, increasing anchor bolt production capacity by 18% while improving dimensional consistency metrics.

• In November 2023, Simpson Strong-Tie launched a high-strength chemical anchor system specifically designed for cracked concrete and seismic regions, approved for use in government infrastructure projects.

The Concrete Fasteners Market Report covers an in-depth analysis of various dimensions impacting the global industry. It encompasses detailed segmentation by product type—including mechanical anchors (wedge, sleeve, drop-in), chemical anchors, screw anchors, and powder-actuated fasteners—and application areas, such as structural construction, HVAC systems, seismic retrofitting, and industrial installations. Additionally, it offers insights into the end-user segments, including commercial construction firms, infrastructure developers, public utilities, and modular housing manufacturers.

Geographically, the report evaluates regional demand across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with specific focus on top countries like the U.S., China, Germany, and India. It analyzes market maturity, growth dynamics, and regulatory influences unique to each region. The report also investigates emerging trends, including automation in installation, AI-based quality tracking, and the shift toward corrosion-resistant materials. Niche market segments, such as anchors for green buildings and smart fastening systems for digital construction workflows, are covered in detail.

Moreover, the study explores the competitive landscape, profiling key companies, tracking their strategic initiatives, and highlighting product innovation trends. It provides actionable intelligence for manufacturers, investors, procurement managers, and policymakers to make informed decisions in a rapidly evolving concrete anchoring ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Concrete Fasteners Market |

| Market Revenue (2024) | USD 248.9 Million |

| Market Revenue (2032) | USD 327.8 Million |

| CAGR (2025–2032) | 3.5 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Technological Insights, Market Dynamics, Segment Analysis, Regional & Country-Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Hilti Corporation, ITW Construction Products, fischer Group of Companies, DEWALT (Stanley Black & Decker), Simpson Strong-Tie Company, Inc., EJOT Group, Sika AG, Powers Fasteners, MKT Fastening, LLC, RAWLPLUG S.A., Würth Group, Ancon Ltd (Part of Leviat) |

| Customization & Pricing | Available on Request (10 % Customization is Free) |