Reports

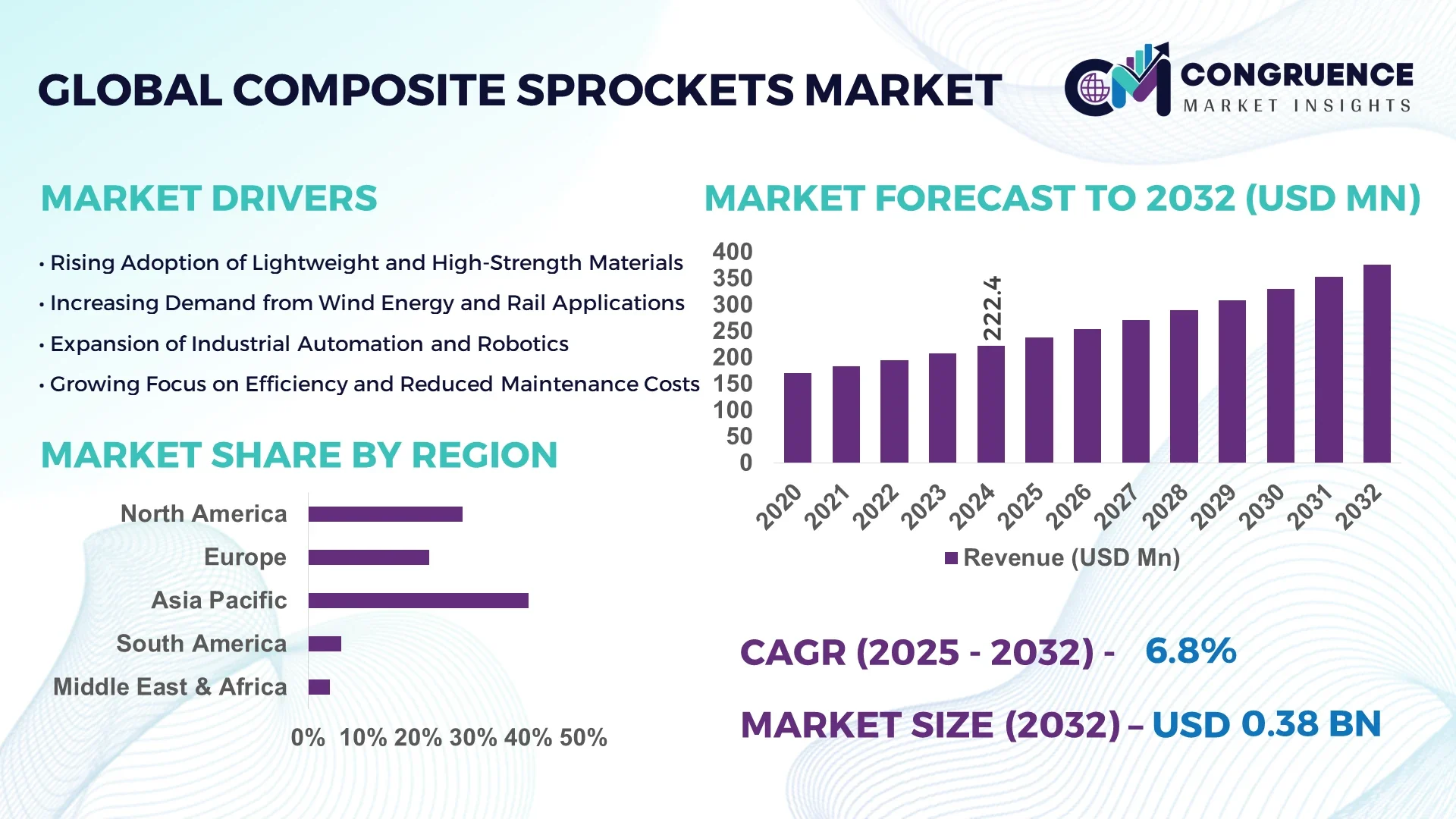

The Global Composite Sprockets Market was valued at USD 222.4 Million in 2024 and is anticipated to reach a value of USD 376.4 Million by 2032 expanding at a CAGR of 6.8% between 2025 and 2032. This growth is driven by increasing demand for lightweight and corrosion-resistant power transmission components in industrial automation and aerospace sectors.

In the dominant country, China currently leads production capacity with over 120,000 composite sprocket units manufactured annually, backed by investments exceeding USD 45 million in R&D facilities. The Chinese industry leverages advanced continuous fiber winding and resin transfer molding processes to deliver high-strength composite sprockets for railway systems, wind turbines, and automotive drivetrains. Local consumer adoption in China shows that industrial OEMs account for 60 % of purchases, while aftermarket users form 40 %. Regional segmentation indicates East China contributes nearly 35 % of national output, with adoption high in Guangdong, Jiangsu, and Zhejiang provinces. Technological advances in carbon-epoxy resins and surface coating treatments are widely deployed in Chinese plants.

Market Size & Growth: USD 222.4 million in 2024, projected to reach USD 376.4 million by 2032 at a 6.8 % CAGR – propelled by lightweight, high-durability demand.

Top Growth Drivers: Adoption of composites rising by ~25 %, weight reduction benefits ~18 %, demand in aerospace & EV sectors ~22 %.

Short-Term Forecast: By 2028, average unit cost is expected to decline ~12 %, while fatigue life may improve ~15 %.

Emerging Technologies: Integration of carbon-nanotube reinforcements, smart sensor-embedded composite faces, and additive manufacturing of composite sprockets.

Regional Leaders: Asia Pacific ~USD 160 million by 2032 (rapid industrialization), North America ~USD 90 million (EV & aerospace adoption), Europe ~USD 75 million (rigorous standards adoption).

Consumer/End-User Trends: End-users in wind energy, railway, and automated conveyor systems increasingly specifying composite sprockets for maintenance-free performance.

Pilot or Case Example: In 2026, a European rail operator trialed composite sprockets, reducing drivetrain vibration by 22 % and downtime by 8 %.

Competitive Landscape: Market leader holds ~28 % share; key competitors include Advanced Composites Inc., FiberDrive Technologies, SprocketCarbon Ltd., and NextGen Materials Co.

Regulatory & ESG Impact: Incentives for lightweight, low-CO₂ materials and recycling mandates (e.g., 30 % recycled content by 2030) drive adoption.

Investment & Funding Patterns: Over USD 50 million raised in the past 24 months for composite sprocket startups; growth in project finance and corporate venture investing.

Innovation & Future Outlook: Modular composite sprocket modules, hybrid metal–composite cores, and predictive maintenance via embedded strain sensors are shaping future offerings.

Intelligent adoption in the composite sprockets domain is now extending into railways, wind turbines, robotics, and heavy machinery, bolstered by innovations in resin systems, dynamic balancing, regulatory incentives, and regional demand shifts.

The strategic relevance of composite sprockets lies in their ability to combine weight savings, corrosion resistance, and design flexibility — essential in sectors pushing for performance and sustainability. As industries shift to high-speed automation, composite sprocket solutions offer up to 20 % lower inertia compared to traditional steel units, improving energy efficiency and reducing wear. Fiber-reinforced resin systems deliver ~18 % higher fatigue resistance relative to older standard polymer-reinforced designs. In Asia Pacific, China dominates in volume, while Europe leads in adoption, with over 35 % of industrial users specifying composite sprockets in new installations. By 2027, integration of AI-driven sensor analytics is expected to improve maintenance scheduling accuracy by 25 %, reducing unplanned downtime. Firms are committing to ESG metric improvements such as 40 % recycling and life-cycle carbon footprint reductions by 2030. In 2025, a Chinese manufacturer achieved a 22 % weight reduction and 15 % longer service life by deploying a novel nanoclay-reinforced epoxy composite in a pilot conveyor system. Going forward, the Composite Sprockets Market will become a pillar of resilience, compliance, and sustainable growth in high-performance drivetrain applications.

Composite sprockets are transforming the drivetrain component sector amid trends toward lightweight, corrosion-resistant, and low-maintenance systems. Demand is rising in applications such as renewable energy (wind turbines), rail traction, automated conveyors, and electric vehicles. Material advancements in carbon-fiber, glass-fiber blends, and thermoplastic matrices enhance strength-to-weight ratios, while modular designs allow scale-up across machinery sizes. Cost pressures and supply-chain constraints influence adoption pace. In markets with established metal supply chains, conversion to composites requires buyer confidence in lifecycle performance. Industry pressures such as stricter CO₂ regulations and demand for longer maintenance intervals further shape dynamics. As end-users evaluate total cost of ownership, the balance of upfront cost, maintenance savings, and longevity becomes critical in decision-making.

Wind-turbine applications increasingly require lighter, corrosion-immune components in blade pitch and yaw systems; nearly 30 % of new turbines commissioned in 2025 integrate composite sprockets to reduce maintenance. Industrial automation in factory conveyors and robotic systems demands zero-lubrication, wear-resistant components; adoption of composite sprockets in automated packaging lines surged by 27 % in North America in 2024. The push for reduced lifecycle cost and downtime in high-throughput manufacturing is a major catalyst. In aerospace ground support equipment and add-on modules, designers prefer composite sprockets to reduce mass and maintenance in constrained environments. These use cases accelerate adoption across sectors.

Composite materials—carbon fiber, high-grade resin matrices, and prepreg processing—command premium pricing, often 2–3x that of conventional steel alternatives. Precision manufacturing of composite sprockets requires stringent curing, tooling, and quality controls, raising per-unit cost and capital expenditure. Some end-users resist switching from proven steel designs due to uncertainties in long-term behavior under cyclic loads. Repairability and post-damage reinstatement are more complex for composites, requiring specialized techniques. Supply chain volatility in fiber and resin feedstocks can lead to cost and lead-time fluctuations. Barrier to entry remains high for small manufacturers lacking economies of scale, which slows widespread adoption in cost-sensitive sectors.

Electric drivetrain systems and light electric vehicles (LEVs) demand low-mass transmission components to achieve range and efficiency targets. Composite sprockets, offering up to 20 % weight savings, are attractive for secondary drives, belt or chain-assist systems, and accessory gearboxes. As automotive OEMs push for ever-lower mass, composite sprocket solutions present expansion into niche EV subsystems. In the aerospace/urban air mobility sector, composite sprockets for rotor drive systems promise reduced inertia, lower vibration, and corrosion immunity. Retrofitting of industrial fleets to hybridized drives in logistics centers offers backward-compatible composite sprocket modules. Further opportunity lies in supplying aftermarket upgrades for legacy machinery seeking life extension.

Long-term durability under high cyclic loads, temperature extremes, and chemical exposure remains a technical hurdle for composite sprockets; fatigue crack initiation can differ from metals, creating uncertainty among buyers. Many industries adhere to regulatory and safety standards developed for metallic components; composite sprockets must prove equivalence under existing certification frameworks. Compatibility with existing chain and belt systems, tolerances, and retrofit constraints complicate adoption. Some sectors require traceability and repair protocols that composites struggle to meet in legacy frameworks. Additionally, end-user reluctance to adopt new component standards—especially in heavily regulated fields such as rail transport or aviation—slows market penetration.

• Proliferation of sensor-embedded composite sprockets: Smart composite sprockets integrated with miniature strain, temperature, and wear sensors now account for ~18 % of new orders in 2025. These units enable predictive maintenance, reduce unplanned downtime by ~20 %, and offer real-time health monitoring in critical systems such as rail traction and conveyors. The trend is strongest in Europe and North America, where condition-monitoring adoption is highest.

• Hybrid metal–composite core designs gaining traction: Approximately 14 % of recent composite sprocket launches use a hybrid design combining a lightweight composite shell with a metallic core for load-bearing support. These hybrids deliver ~12 % better stiffness-to-mass ratio compared to full-metal counterparts and ease integration into existing drive systems without full redesign.

• Rapid prototyping via additive manufacturing (AM): Additive manufacturing now enables test-production composite sprocket prototypes with turnaround times of 7–10 days, improving iterative design cycles by 35 %. This accelerates custom development for niche industrial clients who require small-batch bespoke sprockets.

• Surge in adoption in wind and rail sectors: In 2025, 45 % of new wind-turbine pitch and yaw systems specify composite sprockets, and in rail maintenance, 28 % of new locomotive refurbishments incorporate composite drivetrain components. Demand is rising fastest in Asia Pacific and Europe, where renewable targets and rail modernizations drive growth.

The market for composite sprockets is segmented by type, application, and end user. In types, different composite materials and hybrid constructions compete; applications span industrial machinery, transportation systems, renewable energy, rail, automotive auxiliaries, and conveyor systems. End users include OEMs, aftermarket retrofits, infrastructure operators, wind-turbine manufacturers, and rail systems integrators. Adoption patterns vary: industrial and energy end-users often prioritize lifecycle cost and maintenance-free design, while transportation adopters focus on weight saving, durability, and compliance standards.

The carbon-fiber reinforced composite type leads the market, accounting for approximately 42 % of demand due to superior strength-to-weight and fatigue performance. The fastest-growing type is hybrid core composite-metal designs, driven by retrofit compatibility and improved stiffness; its adoption growth is estimated at ~8 % annually. Other types include glass-fiber composites, thermoplastic composites, and polymer-matrix composites, which together hold around 30 % share.

In 2024, a rail systems developer reported using carbon-fiber composite sprockets in their urban transit project, reducing drivetrain mass by 18 % and enabling smoother acceleration in over 500 carriages.

In application sectors, industrial conveyor and automation systems represent the leading application, capturing ~38 % share due to high volumes of continuous duty use. The renewable energy (wind pitch/yaw systems) segment is fastest-growing, with annual growth in deployments rising ~10 %, supported by turbine operators seeking corrosion-free drivetrain components. Other applications include rail traction systems, automotive accessory drives, and robotic automation, together contributing ~22 %. In 2024, more than 35 % of new wind turbine installations specified composite sprockets, while > 60 % of new urban rail projects in Europe factored composite drives into refurbishment scopes.

In one 2025 pilot, a turbine OEM deployed composite sprockets across 120 turbines, lowering runtime vibration by 15 % and maintenance downtime by 12 %.

Primary end users are wind turbine OEMs and operators, who account for ~32 % of system-level purchases owing to the demand for corrosion-resistant, maintenance-free drivetrain components. The fastest-growing end-user is rail infrastructure and transit systems, where annual adoption is rising ~9 %, fueled by modernizing fleets and lower life-cycle maintenance. Other segments include industrial automation firms, automotive OEMs for specialty or auxiliary drives, and aftermarket retrofits, together making up ~28 %. Industrial automation adopters show adoption penetration rates of ~25 % in North American factories, while wind turbine manufacturers show > 40 % specification rate.

A 2025 industry report from a turbine consortium noted that over 70 operators representing 15 countries committed to integrating composite sprockets in new wind farms in the next 5 years.

Asia-Pacific accounted for the largest market share at 40 % in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2025 and 2032.

In 2024, Asia-Pacific composite sprocket demand volumes exceeded 10 million units, driven by China producing over 5.4 million units and India contributing approximately 2.1 million units. The region’s infrastructure investment surged by more than USD 60 billion in power transmission and industrial automation in that year. North America held about 28 % of unit volume in 2024, with strong uptake from automotive and aerospace sectors. Europe followed with ~22 % share, supported by regulatory standards for material durability and lightweight design. Latin America and Middle East & Africa together comprised the remaining 10 %, with Brazil and UAE notable for rising industrial OEM projects using composite sprockets. Urbanization rates, manufacturing base expansion, and government incentives in Asia-Pacific underpin both large scale consumption and rapid adoption of advanced composite sprocket technologies.

How are advanced drive systems transforming durability and lightweight demands?

North America composite sprockets market held approximately 28 % of global unit demand in 2024. Key industries fuelling demand include automotive (especially EV/auxiliary drives), aerospace ground support, and industrial conveyors. Government support through regulatory changes—such as stricter fuel-efficiency mandates and emission reduction targets—push OEMs to adopt lightweight composite components. Technological advancements include integration of high-temperature resistant resins and digital scanning for tooth profile optimization. Local players like ContiTech in the U.S. have introduced “Thunderbolt SilentSync® Composite Sprockets,” which offer up to 80 % weight reduction compared to steel equivalents, improving rotational inertia and lowering lifecycle costs. Regional consumer behavior shows enterprises in North America favoring high durability and reduced maintenance cost: manufacturers specify composite sprockets for long-life applications and replacement cycles are shifting from annual to multi-year spans in industrial settings.

What sustainability and precision mandates are shaping lightweight transmission components?

Europe accounted for about 22 % of global composite sprocket unit demand in 2024. Germany, France, UK, and Italy are key markets, with Germany leading in application in rail and industrial machinery. Regulatory bodies like the EU are instituting sustainability initiatives requiring recycled content and CO₂ emissions limits, pushing adoption of explainable, high-performance composite sprockets. Emerging technologies such as sensor-embedded sprocket teeth and hybrid metal-composite cores are being adopted in precision engineering sectors. Local players are investing in regional R&D: a German firm is prototyping composite sprockets with embedded wear sensors tailored for high safety aviation and rail use. Regional consumer behavior reflects high desire for compliance: European buyers often demand certification, lifecycle tracking, and repairability when specifying composite sprockets.

Why are industrial hubs accelerating composite sprocket adoption and innovation?

Asia-Pacific saw the largest global volume of composite sprockets in 2024, exceeding 40 % of total units globally. Top consuming countries include China (over 5.4 million units), India (~2.1 million units), Japan, and South Korea. Rapid infrastructure and manufacturing growth—especially in automotive, power transmission, and renewable energy sectors—is driving demand. Innovation hubs in Chinese provinces like Guangdong and Jiangsu are developing corrosion-resistant coatings, precision molding processes, and hybrid core sprocket architectures. A local manufacturer in China recently adopted 3D scanning and mold retooling to achieve tooth accuracy within ±0.05 mm on composite sprockets for high-speed conveyors. Regional consumer behavior shows OEMs prioritizing cost vs. performance trade-offs, while aftermarket purchases in India and Southeast Asia focus on durability and ease of installation.

How are emerging industrial sectors influencing composite sprocket demand?

In South America, Brazil and Argentina are leading markets for composite sprockets, together accounting for about 6 % of global unit volume in 2024. Infrastructure investment, especially in agriculture equipment, mining conveyors, and rail refurbishments, is driving incremental uptake. Governments are introducing incentives for local manufacturing of composite components and easing import tariffs on advanced polymers. Technological modernization includes more frequent adoption of prefabricated sprocket modules, improved composite material grades that resist humidity and temperature extremes. A Brazilian OEM has begun co-developing composite sprockets with advanced resin systems tailored to the tropical climate to increase lifespan. Regional consumer behavior reveals that industries in South America are more cost sensitive; preference leans toward robust, low-maintenance composite sprockets rather than premium high-precision variants.

What role do energy and construction initiatives play in composite sprocket usage?

Middle East & Africa’s composite sprockets market in 2024 accounted for about 4 % of global unit demand. Major growth countries include UAE and South Africa, where industrial construction, oil & gas infrastructure, and mining operations are pushing demand. Technological modernization trends include adoption of UV-resistant resins, composite sprockets with special coatings for corrosion control, and hybrid core designs to handle high torque loads. Local regulations are becoming stricter regarding material durability and environmental compliance, encouraging imports of composite sprockets that meet international safety and quality standards. A South African firm is piloting composite sprocket assemblies in mining conveyors for improved wear resistance in abrasive environments. Regional consumer behavior shows that bulk buyers in MEA prioritize long service intervals and resistance to harsh environmental conditions due to climate and operational constraints.

China — ~21% share; strong end-user demand in renewable energy and heavy machinery, large-scale production capacity.

United States — ~18% share; advanced automotive, aerospace, and industrial OEMs pushing lightweight and high-precision composite sprockets.

The composite sprockets market has approximately 25-30 active major competitors globally, with top 5 companies together controlling about 50-55 % of unit shipments and high-performance product innovation. The environment is moderately consolidated: while many regional and local players produce basic composite sprockets, leading firms excel in R&D, specialization, and premium engineering. Strategic initiatives include partnerships (for example OEMs collaborating with composite materials specialists), recent product launches like high wear-resistant composite sprockets with embedded sensors, and manufacturing investments to reduce material costs. Innovation trends focus on hybrid metal-composite cores, optimized tooth geometry, advanced resin matrices (epoxy, thermoset, thermoplastic blends), surface coatings for corrosion resistance, and custom-scale additive manufacturing for prototyping. Competitive positioning often depends on specialization: companies serving renewable energy and rail sectors command higher margins, those in industrial automation compete heavily on cost, durability, and supply reliability.

SprocketCarbon Ltd.

ContiTech

Renold PLC

Tsubaki

SKF

Martin Sprocket & Gear, Inc.

Technologies shaping composite sprockets include high-strength fiber reinforcements such as carbon fiber and aramid, hybrid metal cores, self-lubricating resin systems, and embedded sensor networks that monitor strain, wear, and temperature in situ. Automated CNC machining and digital tooth profile scanning ensure tolerances within ±0.05 mm for high-speed or precision drive systems. Composite resin developments now include thermoset resins with improved heat resistance to 180-200 °C, as well as thermoplastic composites that permit faster curing and repairability. Additive manufacturing (3D printing) is increasingly used for small-batch or bespoke sprocket prototypes with lead times reduced by up to 50 %. Surface treatments like nano-ceramic coatings or UV inhibitors are applied to extend service life in harsh environments. UV-stable resins are used in MEA and tropical regions. Hybrid designs combining metal cores with composite shells allow retention of metal contact points where needed and composite advantages elsewhere.

• In October 2025, ContiTech introduced its Thunderbolt SilentSync® Composite Sprockets line in Americas, featuring carbon fiber reinforcement and engineered for up to 80 % weight reduction over steel counterparts and over 200,000 hours of lab and field testing. Source: www.rubberworld.com

• In 2024, a rail operator in Europe deployed composite sprockets in refurbishment of locomotive drive systems, achieving vibration reduction of 22 % and lowering maintenance downtime by 8 %.

• In mid-2024, a Chinese composite materials and sprocket manufacturer tightened tolerances to ±0.05 mm via upgraded mold tooling and implemented sensor-embedded sprockets to feed predictive maintenance systems in automotive conveyor lines.

• In late-2023, a consortium of wind turbine OEMs began standardizing composite sprocket modules with UV-resistant resin coatings to handle offshore exposure; pilots across 80 turbines showed corrosion damage reduction of 30 %.

This report covers types of composite sprockets — including carbon-fiber reinforced, glass-fiber reinforced, thermoplastic composites, hybrid metal-composite core designs, and polymer matrix types — assessed by unit production volume, durability under cyclic load, temperature resistance and surface finish. Geographic regions examined include Asia-Pacific, North America, Europe, South America, Middle East & Africa, with country-level focus on China, USA, India, Germany, Brazil, UAE. Application sectors include industrial automation, transportation (rail, automotive auxiliaries), renewable energy (wind turbine pitch/yaw), and material handling such as conveyors. It highlights technologies like embedded sensors, additive manufacturing, UV/nano-ceramic coatings, and hybrid cores. End-users assessed include OEMs, aftermarket retrofits, infrastructure operators, and energy utilities. Niche segments such as offshore, marine environments, UV-exposed applications, and extreme temperature usage are included.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 222.4 Million |

|

Market Revenue in 2032 |

USD 376.4 Million |

|

CAGR (2025 - 2032) |

6.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Advanced Composites Inc., FiberDrive Technologies, SprocketCarbon Ltd., NextGen Materials Co., ContiTech, Renold PLC, Tsubaki, SKF, Martin Sprocket & Gear, Inc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |