Reports

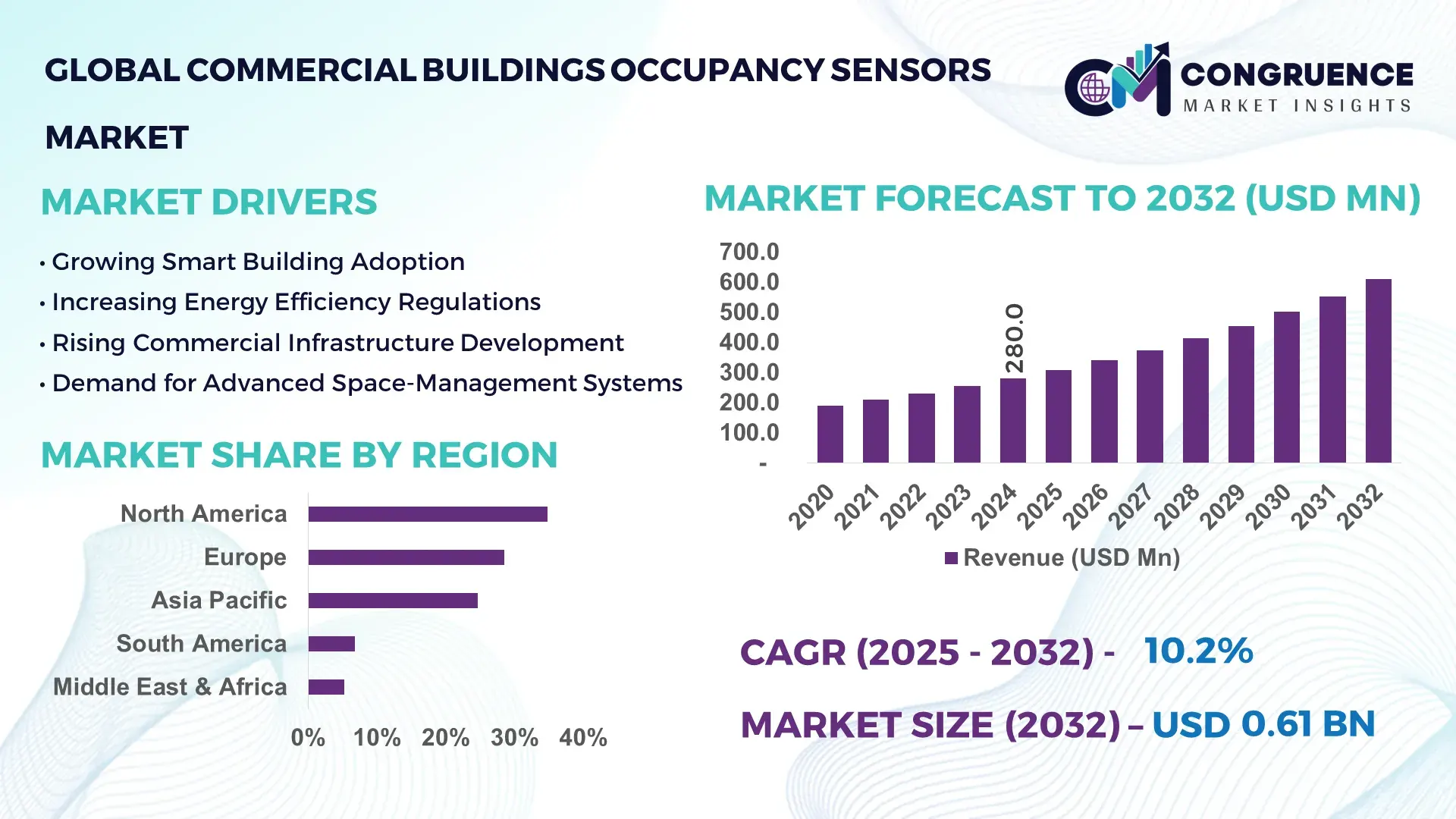

The Global Commercial Buildings Occupancy Sensors Market was valued at USD 280.0 Million in 2024 and is anticipated to reach USD 609.0 Million by 2032, expanding at a CAGR of 10.2% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is primarily driven by expanding smart-building deployments and rising demand for energy-optimized commercial infrastructure.

The United States maintains a leading position supported by large-scale investments in smart commercial infrastructure, advanced IoT integration capabilities, and continuous upgrades in building automation systems. The country hosts more than 5.9 million commercial buildings, with over 900 million smart IoT devices deployed across enterprise facilities. With sustained federal energy-efficiency programs and over USD 27 billion committed to building modernization initiatives, the U.S. demonstrates strong technological leadership, enabling sophisticated sensor manufacturing, AI-enabled building controls, and high adoption across corporate, retail, and institutional facilities.

Market Size & Growth: Market valued at USD 280.0 Million in 2024, projected to reach USD 609.0 Million by 2032 at a CAGR of 10.2%; driven by rising integration of intelligent control systems in commercial spaces.

Top Growth Drivers: Smart-building adoption up 38%, lighting-energy optimization improving by 27%, and IoT-enabled automation rising by 33%.

Short-Term Forecast: By 2028, automation-driven facilities expected to achieve a 22% reduction in operational inefficiencies.

Emerging Technologies: AI-powered adaptive sensing, LiDAR-enhanced occupancy mapping, and wireless mesh sensors improving building analytics.

Regional Leaders: North America expected to reach USD 215 Million by 2032; Europe projected at USD 175 Million; Asia Pacific at USD 135 Million—each driven by expanding digital infrastructure.

Consumer/End-User Trends: Retail chains, corporate offices, and institutional complexes accelerating adoption due to efficiency and comfort requirements.

Pilot or Case Example: In 2027, a U.S. commercial retrofit pilot achieved 31% energy savings through AI-enabled occupancy analytics.

Competitive Landscape: Leading vendor holds approximately 14% share, followed by 5–6 major competitors offering IoT-integrated sensing solutions.

Regulatory & ESG Impact: Energy codes and green-building mandates accelerating adoption, supported by sustainability commitments targeting 25% efficiency gains by 2030.

Investment & Funding Patterns: Over USD 1.2 Billion recently invested in smart-building automation platforms and sensor-integration projects.

Innovation & Future Outlook: Future growth influenced by AI-enabled automation, cloud-integrated occupancy prediction, and scalable wireless sensing architectures shaping next-gen commercial ecosystems.

Unique information: Commercial building adoption is expanding across sectors such as corporate offices, retail, hospitality, and healthcare, each contributing significantly to sensor deployment volumes. Recent product innovations incorporate multi-sensing modules, thermal imaging, and advanced wireless protocols. Regulatory incentives for building efficiency and shifting energy economics drive installation rates, while Asia Pacific and Europe lead in next-generation retrofit demand. Market evolution continues toward integrated analytics and automation-driven facility optimization.

The Commercial Buildings Occupancy Sensors Market plays a critical role in the modernization of intelligent commercial infrastructure, enabling efficiency, automation, and real-time building utilization insights. Organizations increasingly recognize the strategic value of occupancy-driven automation as commercial buildings account for more than 30% of global electricity consumption, making sensing technologies essential for operational optimization. Advanced AI-integrated sensors deliver precision detection and adaptive lighting, HVAC modulation, and space-optimization analytics. Comparative benchmarks show that AI-driven adaptive sensing delivers 45% improvement compared to legacy passive infrared systems in commercial environments.

Regional variations are becoming more pronounced as North America dominates in volume, while Europe leads adoption with 62% of enterprises integrating intelligent sensing into building-management systems. By 2028, predictive AI-based building-management tools are expected to improve facility operational efficiency by 28%, reshaping workplace planning and resource allocation. ESG alignment further strengthens the market’s strategic relevance, with firms committing to 20–30% carbon-reduction gains by 2030 through energy-efficient technologies.

Measurable outcomes highlight the market’s acceleration; for example, in 2026, a major real estate group in Japan achieved a 37% reduction in lighting energy consumption through an AI-enabled occupancy-automation initiative. The pathway forward includes deeper integration with cloud analytics, space-utilization dashboards, and digital-twin platforms supporting predictive control. As commercial infrastructure evolves toward net-zero and intelligent automation, the Commercial Buildings Occupancy Sensors Market stands as a foundational pillar for resilience, compliance, and sustainable growth.

The Commercial Buildings Occupancy Sensors Market is shaped by rising demand for smart-building automation, increased emphasis on energy efficiency, and integration of IoT-based facility-management platforms. Organizations are adopting occupancy-driven intelligence to improve space utilization, reduce energy wastage, and enhance operational efficiency in commercial structures. Technology convergence involving AI, wireless connectivity, and cloud-based data analytics is reshaping design and deployment. Growing retrofit activity, workplace modernization, and sustainability regulations continue to influence market direction, while advancements in multi-sensing capabilities and building-level automation accelerate adoption across diverse commercial environments.

Advanced smart-building automation is significantly transforming operational efficiency in commercial facilities, driving the adoption of occupancy sensors. Modern buildings depend on real-time data to automate lighting, HVAC control, and space utilization, resulting in measurable resource optimization. Studies indicate that smart automation can reduce energy consumption in commercial buildings by 20–35% through occupancy-responsive controls. The integration of AI and machine-learning algorithms allows sensors to adapt to variable occupancy patterns, improving accuracy and minimizing false triggers. Additionally, wireless technologies enable flexible installation in retrofit and new-build projects. With expanding adoption of cloud-based management platforms and digital workspace planning tools, occupancy sensors have become a fundamental technology supporting modern building ecosystems.

Integration complexities create notable challenges for widespread deployment, especially in older commercial facilities with outdated electrical systems, inconsistent building-management platforms, or limited wireless support. Commercial buildings often feature heterogeneous infrastructure, requiring custom interfaces and additional hardware to ensure compatibility between sensors, HVAC units, and centralized controls. Calibration difficulties may reduce accuracy, with improper installation resulting in up to 18% detection inefficiency. Additionally, privacy concerns associated with advanced imaging or multi-modal sensors may slow adoption where regulatory compliance is strict. The need for skilled technicians and higher installation time contributes to increased project costs, particularly in large-scale retrofits. These factors collectively constrain deployment speed across cost-sensitive segments.

AI-driven building optimization is unlocking significant opportunities by enhancing predictive control, improving accuracy, and enabling deeper integration with facility-management systems. AI-enabled occupancy intelligence supports advanced space-utilization analytics, allowing building operators to optimize scheduling and capacity planning. Predictive HVAC and lighting management can improve operational efficiency by up to 30% in high-traffic commercial areas. Cloud-connected platforms provide continuous data insights for long-term performance improvements and automated maintenance. Growing interest in digital twins, real-time occupancy dashboards, and enterprise workflow optimization accelerates adoption in large commercial enterprises seeking technology-driven transformation. These advancements create substantial opportunities for next-generation sensing technologies and integrated building-automation ecosystems.

The Commercial Buildings Occupancy Sensors Market faces challenges due to increasing system costs, particularly for advanced multi-sensing devices integrating thermal imaging, LiDAR, or AI-driven analytics. These technologies require sophisticated electronics, precision manufacturing, and secure data-processing frameworks, elevating unit and integration expenses. Compliance with regional safety, data-privacy, and building-automation regulations adds further complexity, increasing administrative and certification requirements. Large commercial projects may face 10–18% higher upfront costs when adopting next-generation solutions. Economic constraints in emerging markets and fluctuating construction investments intensify challenges, creating longer ROI cycles and delaying procurement decisions among budget-sensitive facility operators.

Rapid Expansion of AI-Enabled Sensing Platforms: AI-powered occupancy systems are witnessing accelerated adoption, with deployments increasing by 42% across commercial facilities. These platforms enhance detection accuracy, automate lighting and HVAC functions, and reduce operational inefficiencies. Buildings using AI-integrated sensors report up to 29% improvement in facility performance metrics due to real-time behavioral pattern analysis and adaptive control mechanisms.

Growth in Wireless and Battery-Efficient Sensor Deployments: Demand for wireless occupancy sensors has increased by 35%, supported by advancements in low-power communication protocols. Modern commercial buildings deploying battery-efficient sensors experience installation time reduction of 45%, improving scalability and supporting retrofits. These devices operate efficiently for up to 7–10 years, reducing maintenance efforts and long-term operational burden.

Rising Implementation of Multi-Modal Detection Technologies: Multi-sensor devices combining PIR, ultrasonic, and thermal imaging technologies have grown by 31%, improving detection accuracy by up to 48% compared to single-mode sensors. Commercial buildings adopting multi-modal detection benefit from improved workplace analytics, precise movement mapping, and reduced false triggers, especially in complex, high-traffic environments.

Surge in Smart Retrofit Projects Across Corporate and Retail Buildings: Retrofit initiatives across commercial facilities increased by 28%, driven by modernization goals and regulatory efficiency targets. Corporations upgrading existing spaces report 25–33% improvements in operational efficiency when integrating occupancy-driven controls. Retail chains implementing automated lighting and HVAC modulation recorded a 24% decline in energy misuse, reinforcing retrofit demand in developed and emerging regions.

The Commercial Buildings Occupancy Sensors Market is structured around three core segmentation pillars—type, application, and end-user—with each contributing distinct technological and operational dynamics. The market reflects increasing adoption of advanced sensing modalities, driven by smart-building modernization and demand for automated energy management. Types such as PIR, ultrasonic, dual-technology, and image-based sensors demonstrate varied adoption patterns aligned with installation needs and building layouts. Applications span lighting automation, HVAC control, space-optimization systems, and integrated building-management functions, each shaped by digitalization trends and facility-efficiency objectives. End-user demand is distributed across office buildings, retail environments, institutional facilities, hospitality, and healthcare infrastructures, influenced by retrofit momentum and regulatory emphasis on energy performance. Rising integration of IoT platforms and analytics-enabled decision support continues to redefine performance expectations across segments, strengthening the overall market structure.

Product types in the Commercial Buildings Occupancy Sensors Market include passive infrared (PIR), ultrasonic, dual-technology, and image-based or camera-enabled sensors. Among these, passive infrared (PIR) sensors account for approximately 46% of total adoption, driven by their reliability, cost-efficiency, and suitability for most enclosed commercial spaces. PIR remains the leading type due to its widespread acceptance in lighting automation and its robust performance in areas with predictable movement patterns. Ultrasonic sensors hold around 22% of adoption, offering higher sensitivity in detecting subtle motion behind obstacles. Dual-technology sensors combine the strengths of PIR and ultrasonic, with adoption rising steadily to reach nearly 20% because they minimize false triggers and support complex layouts. The fastest-growing segment is image-based sensing, expanding at an estimated 11.5% CAGR, supported by demand for high-precision occupancy analytics, AI-assisted detection, and advanced building-utilization insights. Image-based systems currently account for about 12% of installations but are expected to surpass 20% over the next decade as integration with advanced building-management platforms increases. Other niche sensor types, including CO₂-based occupancy estimation modules and thermal-imaging variants, collectively contribute about 8% of the market, serving specialized applications such as conference rooms, high-security environments, and large open-plan spaces.

Applications across the Commercial Buildings Occupancy Sensors Market encompass lighting control, HVAC optimization, space-management systems, and integrated building-automation platforms. Lighting control remains the leading application, accounting for approximately 48% of usage, supported by mandatory efficiency regulations and measurable reductions in electricity consumption when occupancy-triggered automation is implemented. HVAC optimization currently makes up about 27% of adoption, while space-management systems, including room-booking automation and people-flow analytics, represent around 18%. However, adoption in real-time space-optimization systems is rising fastest, growing at an estimated 12.3% CAGR, and expected to exceed 30% of advanced-building deployments by 2032 due to hybrid-workplace restructuring and improved analytics capabilities. Remaining applications—security monitoring, emergency-lighting triggers, and integrated building-automation linkage—collectively hold roughly 7% of market share and remain essential in high-compliance commercial environments. Consumer adoption trends show significant activity: in 2024, more than 39% of global enterprises piloted occupancy-sensing systems to improve building-efficiency metrics, and over 58% of corporate facilities reported transitioning to automated lighting control platforms. In the U.S., 44% of hospitals began evaluating occupancy-linked HVAC and lighting systems to improve patient-care environments and reduce operational strain.

End-users in the Commercial Buildings Occupancy Sensors Market include office buildings, retail facilities, educational institutions, healthcare facilities, hospitality establishments, and industrial-commercial complexes. Office buildings represent the leading end-user segment with approximately 41% share, driven by large-scale workspace automation, hybrid-workplace adoption, and demand for efficient lighting and HVAC solutions. Retail facilities hold around 23% of adoption, while educational and institutional facilities account for approximately 18%. Hospitality and healthcare environments collectively contribute nearly 12%, shaped by increasing modernization of guest-experience systems and safety monitoring. The fastest-growing end-user segment is healthcare, expanding at an estimated 11.8% CAGR, supported by facility-automation initiatives, patient-comfort optimization, and staffing-efficiency requirements. Adoption across retail and hospitality is also rising steadily, with consumer-behavior analytics and operational-efficiency gains influencing procurement priorities. Remaining end-user categories, including industrial-commercial hybrid facilities and specialized research buildings, represent about 6% of combined share, often requiring high-sensitivity or multi-modal sensing solutions to meet stringent operational criteria. Industry adoption indicators reflect broader trends: in 2024, 37% of enterprises globally implemented occupancy-driven facility-management pilots, and over 62% of smart workplaces incorporated automated lighting systems to enhance productivity and sustainability. In the U.S., 43% of large hospitals tested integrated occupancy-HVAC optimization systems to improve indoor environmental quality.

North America accounted for the largest market share at 34.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

The global Commercial Buildings Occupancy Sensors market shows strong regional variations influenced by commercial construction activity, retrofitting demand, building automation penetration, and energy-efficiency regulations. In 2024, Europe followed with 28.5% share, driven by strict sustainability mandates across offices, public facilities, and industrial workplaces. Asia-Pacific held 24.6%, supported by rapid urbanization and growth of smart commercial infrastructure across China, India, Japan, and South Korea. South America and Middle East & Africa collectively represented 12.1%, where adoption continues to rise due to expanding corporate real estate, hospitality growth, and government-led smart infrastructure programs. Regional product preference data indicates that PIR sensors accounted for 41% of installations, followed by dual-technology sensors at 29%, with strongest traction in technologically mature markets.

North America held a 34.8% share of the Commercial Buildings Occupancy Sensors market in 2024, making it the world’s largest regional contributor. Strong adoption is driven by commercial offices, healthcare, retail infrastructure, and data centers seeking measurable energy-efficiency gains. The U.S. and Canada continue to implement stricter building codes, including mandatory lighting control standards in federal facilities, which further accelerates retrofitting demand. Technologies such as AI-enabled multi-sensing modules, wireless mesh systems, and cloud-integrated BMS platforms are witnessing widespread enterprise adoption. A notable example is Leviton, which expanded its wireless sensor portfolio in 2024 to support autonomous building operations for mid-sized commercial facilities. Consumer behavior in this region favors smart, easily deployable, analytics-ready systems, with the healthcare and financial sectors demonstrating the highest adoption due to compliance requirements and 24/7 facility operations.

Europe captured 28.5% market share in 2024, reinforced by demand across Germany, France, the UK, Italy, and the Netherlands. High adoption is influenced by region-wide sustainability directives, including carbon-neutral building targets for 2030. The EU’s energy-efficiency regulations mandate advanced occupancy-based lighting and HVAC optimization technologies in commercial facilities over 1,000 m², accelerating installation rates of PIR, ultrasonic, and dual-technology occupancy sensors. European markets also show high interest in edge-AI building automation, daylight-integrated systems, and wired-wireless hybrid sensor networks. Companies such as Schneider Electric continue to invest in IoT-driven BMS platforms tailored to office complexes and industrial warehouses. Consumer behavior leans strongly toward regulatory compliance and long-term operational savings, resulting in widespread demand for sensors offering diagnostics, interoperability, cybersecurity, and explainable automation features.

Asia-Pacific ranked as the fastest-growing region and accounted for 24.6% of global commercial building occupancy sensor installations in 2024, supported by booming construction activity across China, India, Japan, South Korea, and Southeast Asia. The region leads in commercial real estate expansion, where new malls, corporate campuses, transport hubs, and hospitality projects prioritize smart building frameworks. High manufacturing capacity and competitive pricing enable rapid adoption of PIR and microwave sensors integrated with mobile-AI and cloud platforms. Local innovators such as Xiaomi-backed smart facility brands in China have introduced scalable sensor solutions targeted at SMEs and multi-site commercial operators. Consumer behavior trends emphasize mobile-controlled automation, energy conservation, and AI-driven predictive building management, supported by strong digital transformation agendas across emerging Asian economies.

South America represented 6.8% of the global Commercial Buildings Occupancy Sensors market in 2024, with Brazil, Argentina, Chile, and Colombia emerging as key adopters. The region’s commercial sector—particularly corporate offices, retail chains, and public institutions—is investing in cost-efficient lighting and HVAC automation to compensate for fluctuating energy prices. Infrastructure modernization across Brazil’s urban centers is boosting adoption of wireless multi-sensing systems. Government incentive programs promoting energy-efficient public buildings further fuel installations. A notable regional player is Intelbras (Brazil), which continues to expand local production of smart sensing and automation systems. Consumer behavior favors affordable, easy-installation solutions, and demand is closely tied to localization, language support, and integration with existing building systems.

The Middle East & Africa region accounted for 5.3% of the Commercial Buildings Occupancy Sensors market in 2024, supported by rising smart city investments, commercial real estate expansion, and energy-efficiency initiatives across the UAE, Saudi Arabia, Qatar, South Africa, and Kenya. Demand is particularly strong in oil & gas corporate facilities, hospitality, airports, and educational institutions seeking automated, low-maintenance lighting and HVAC optimization. The region is rapidly adopting IoT-enabled sensing platforms, cloud-based building analytics, and long-range wireless communication systems. Local manufacturers—including Dubai-based smart automation brands—are increasingly developing environment-adapted sensor solutions suited to high-temperature conditions. Regulations encouraging sustainable building certifications further contribute to rising sensor penetration. Consumer behavior highlights preference for durable, high-precision, and integrated systems.

United States - 28.2% Market Share: Strong dominance due to extensive commercial real estate, high retrofitting activity, and enterprise-scale adoption of intelligent building automation systems.

China - 16.4% Market Share: Leadership supported by large-scale commercial construction, advanced manufacturing capacity, and widespread integration of AI-powered building technologies.

The competitive environment in the Global Commercial Buildings Occupancy Sensors Market is moderately consolidated, featuring more than 20 active global competitors, with the top 5 firms accounting for around 35%–40% of the market. Key players include Honeywell, Schneider Electric, Johnson Controls, Siemens, and Legrand, all of whom maintain strong global footprints, broad product lines, and deep integration with building automation systems. These companies compete vigorously on innovation: in recent years, there have been major launches of wireless multi-sensors, AI-enabled occupancy detection, and combined sensing (e.g., temperature, CO₂, motion).

Strategic initiatives are central to competition: Johnson Controls introduced its NSW8000 wireless multi-sensor in early 2025 to deliver combined occupancy, CO₂, temperature, and humidity data, backed by up to 10-year battery life. Schneider Electric has strengthened its platform via partnerships and research into energy-saving building controls, highlighting substantial investments in occupancy-based control automation. Honeywell continues to expand its PIR and ultrasonic sensor offerings, optimizing for energy management in commercial HVAC and lighting systems.

Innovation trends include the push toward edge-AI analytics, mesh-network sensors with secure encryption, and multi-parameter sensors that feed into cloud-based building-management platforms. Emerging firms and startups are also entering the fray with novel sensing modalities (e.g., UWB, mmWave radar), further intensifying competition. Established incumbents are defending their positions through R&D, strategic acquisitions, and alliances to offer holistic smart building solutions.

Siemens AG

Legrand SA

Lutron Electronics, Inc.

Texas Instruments, Inc.

Acuity Brands, Inc.

Kieback&Peter GmbH & Co. KG

Verdigris Technologies

The Commercial Buildings Occupancy Sensors Market is being reshaped by significant technological advancements aimed at improving accuracy, flexibility, and integration within intelligent building ecosystems. Traditional sensor technologies—such as passive infrared (PIR), ultrasonic, and dual-technology sensors—continue to retain relevance, especially in legacy building automation systems, due to their reliability and established performance. However, more advanced modalities are gaining traction: image-based sensors and camera-analytics solutions backed by AI now enable real-time people counting, precise occupancy mapping, and behavioral insights without relying solely on motion detection.

Another frontier is multi-parameter sensing, where occupancy sensors also monitor environmental conditions like CO₂ concentration, temperature, and humidity. This convergence helps facility managers optimize HVAC systems based on real-time load and air-quality demands. For example, Johnson Controls’ NSW8000 series integrates PIR occupancy sensing with temperature, humidity, and CO₂ monitoring in a single wireless sensor, offering comprehensive data while minimizing installation complexity.

Connectivity is also evolving: modern occupancy sensors increasingly employ wireless mesh protocols (e.g., Bluetooth Low Energy, Zigbee, proprietary mesh) secured with 128-bit encryption to ensure robust and scalable deployment across commercial buildings. Such mesh networks reduce wiring costs and enable flexible placement. Edge computing is being embedded into sensor devices, which allows for local decision-making — occupancy data can be processed on the device itself rather than sent continuously to the cloud, reducing latency and improving data privacy.

Emerging research is pushing even further: mmWave radar sensors are beginning to be piloted for non-intrusive people counting; these operate without imaging and preserve privacy while offering high sensitivity. Likewise, there are experimental designs using deep learning and smart metering data to infer occupancy through non-intrusive methods like electrical usage patterns. As building owners increasingly demand scalability, efficiency, and data-rich automation, these technological innovations are accelerating the transformation of occupancy sensing from a simple presence-detection function to a powerful node in smart building strategy.

In March 2025, Schneider Electric published a study showing that occupancy-based automation applied in meeting rooms cut operational energy use and carbon emissions by 22%, by keeping rooms in “resting state” when unoccupied. Source: www.se.com

On March 24, 2025, Johnson Controls launched its NSW8000 Series Wireless Network Sensor, a multi-sensor device combining PIR occupancy detection, temperature, humidity, and optional CO₂ measurement, with up to 150 ft wireless range and 10-year battery life. Source: www.johnsoncontrols.com

In 2024, Schneider Electric began co-developing AI-ready data-center infrastructure with NVIDIA, underscoring a strategy to embed energy-aware control systems—potentially including occupancy sensing—as part of its next-generation infrastructure solutions. Source: www.businesswire.com

Honeywell reaffirmed commitment to energy-efficient building management in 2024 by promoting its INNCOM PIR motion sensor line for commercial and hospitality applications, emphasizing occupancy detection to reduce energy use and extend equipment life. Source: www.honeywell.com

This market report covers a comprehensive scope designed for stakeholders who need actionable insights into the commercial buildings occupancy sensors market. It analyzes the market by technology types (e.g., PIR, ultrasonic, dual-technology, image-based, mmWave), connectivity modes (wired vs wireless mesh), and multi-parameter sensors that integrate occupancy with temperature, CO₂, or humidity sensing. The report segments the market by application, including lighting control, HVAC optimization, space-utilization analytics, and building automation platforms.

Geographically, it spans major regions: North America, Europe, Asia-Pacific, South America, and Middle East & Africa, while also profiling key national markets in each region. On the end-user side, the report covers primary verticals such as corporate offices, healthcare, hospitality, education, retail, and industrial-commercial complexes.

The report also delves into competitive dynamics, evaluating active players per region and globally, their product strategies, mergers, and R&D initiatives. Innovation trends such as edge-AI, wireless mesh, mmWave radar, and image analytics are given detailed treatment. Further, this scope includes regulatory and ESG factors, examining energy-efficiency regulations, green building mandates, and sustainability incentives that are accelerating demand. Finally, the report addresses emerging and niche opportunities, such as retrofits in legacy buildings, smart city deployments, and predictive occupancy analytics, offering a forward-looking perspective for decision-makers and investors.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 280.0 Million |

| Market Revenue (2032) | USD 609.0 Million |

| CAGR (2025–2032) | 10.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Honeywell International, Inc., Schneider Electric SE, Johnson Controls International plc, Siemens AG, Legrand SA, Lutron Electronics, Inc., Texas Instruments, Inc., Acuity Brands, Inc., Kieback&Peter GmbH & Co. KG, Verdigris Technologies |

| Customization & Pricing | Available on Request (10% Customization Free) |