Reports

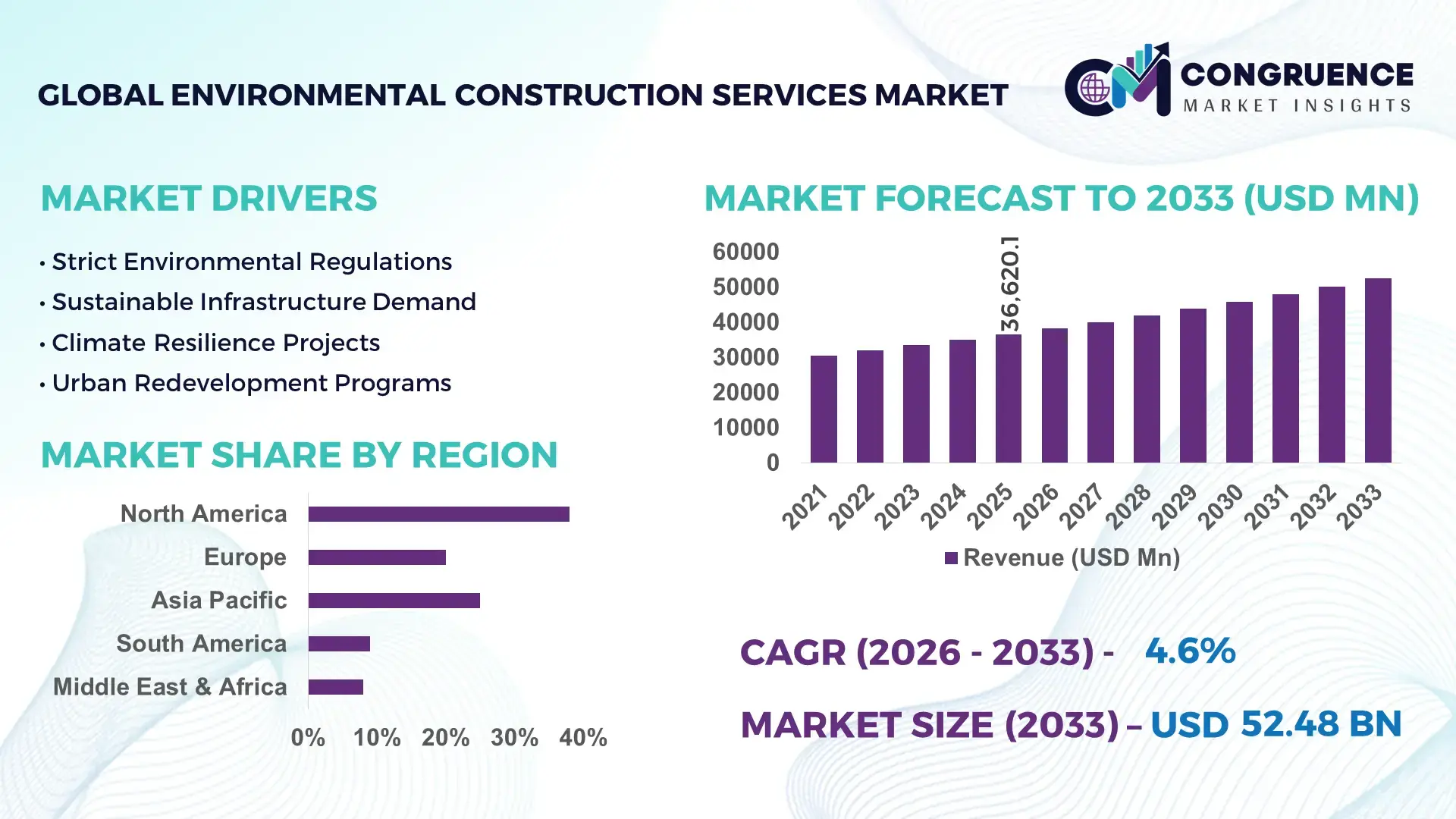

The Global Environmental Construction Services Market was valued at USD 36620.06 Million in 2025 and is anticipated to reach a value of USD 52477.42 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033. This growth is driven by increasing regulatory mandates for sustainable infrastructure development and rising investments in eco‑friendly construction solutions.

The United States and Canada collectively account for multi‑billion‑dollar annual expenditures on environmental construction projects, integrating advanced technologies such as remote environmental monitoring and digital project management systems, with nearly USD 13 billion in regional market value projected by 2035. Strenuous adoption of environmental compliance practices across residential, commercial, and industrial segments further fuels demand, with building projects increasingly incorporating eco‑engineered solutions to meet stringent regional sustainability targets.

• Market Size & Growth: Market valued at ~USD 36.62 B in 2025; forecast ~USD 52.48 B by 2033 at a 4.6% CAGR — driven by regulatory compliance and sustainable construction adoption.

• Top Growth Drivers: Sustainable infrastructure mandates (~74%), green materials adoption (~62%), digital environmental management integration (~55%).

• Short‑Term Forecast: By 2028, average project environmental performance gains expected to improve ~18% through advanced monitoring technologies.

• Emerging Technologies: Adoption of BIM for environmental compliance, IoT‑enabled environmental sensors, automated waste management platforms.

• Regional Leaders: North America (~USD 13 B by 2035), Europe (~USD 10 B by 2035), Asia‑Pacific (~USD 9 B by 2035) — each exhibiting unique drivers from stringent standards to rapid urban sustainability initiatives.

• Consumer/End‑User Trends: Increasing uptake among residential and commercial developers for carbon footprint tracking and green certification compliance.

• Pilot or Case Example: 2025 pilot using GIS‑based environmental mapping reduced compliance review times by ~22% on major coastal mitigation projects.

• Competitive Landscape: Market leader with ~20% share; key competitors include AECOM, Skanska, Jacobs Engineering, Turner Construction, WSP Global.

• Regulatory & ESG Impact: Stricter emission thresholds, green building codes, and ESG reporting requirements expanding service demand globally.

• Investment & Funding Patterns: Recent environmental construction initiatives secured over USD 4 billion in project financing and public‑private partnership funding.

• Innovation & Future Outlook: Continued integration of AI for predictive environmental risk assessment and scalable digital compliance solutions shaping future market growth.

The Environmental Construction Services Market supports critical sectors such as municipal infrastructure, industrial sites, and residential development, with remediation and sustainable construction services being significant contributors to overall revenue. Recent product and technological innovations include advanced remote environmental monitoring systems and eco‑optimized construction materials that reduce waste and emissions. Regulatory drivers — such as tightened environmental impact assessment requirements and carbon reduction mandates — are accelerating adoption. Regional consumption patterns vary, with mature markets in North America and Europe emphasizing regulatory compliance and Asia‑Pacific focusing on sustainable urban expansion. Future outlook indicates robust integration of digital tools, increased environmental risk auditing services, and collaborative public‑private frameworks to deliver large‑scale sustainable construction programs.

The Environmental Construction Services Market holds strategic relevance as a cornerstone of sustainable infrastructure and regulatory compliance worldwide. Advanced technologies such as Building Information Modeling (BIM) deliver a 25% improvement in project planning efficiency compared to traditional design methods, while AI-driven environmental monitoring platforms reduce downtime and regulatory errors by up to 18%. North America dominates in volume, while Europe leads in adoption with 72% of enterprises implementing smart environmental compliance solutions. By 2028, IoT-enabled environmental sensors are expected to improve waste management efficiency by 15% across commercial and industrial construction projects. Firms are committing to ESG metrics improvements such as 30% reduction in construction-related carbon emissions by 2030, aligning with both regulatory mandates and investor expectations. In 2025, a pilot project in Canada achieved a 22% reduction in remediation time through the integration of AI-assisted soil and water monitoring. These measurable gains underscore how environmental construction services are evolving from a compliance requirement to a strategic business advantage. Looking forward, the market is expected to serve as a pillar of resilience, enabling organizations to navigate regulatory frameworks, minimize environmental impact, and drive sustainable growth through innovative construction and environmental management practices.

Rising regulatory requirements for environmental protection, such as strict emission thresholds, soil remediation standards, and green building certifications, are significantly driving the Environmental Construction Services Market. Governments in North America and Europe have mandated compliance reporting for construction projects, leading to a 40% increase in demand for environmental monitoring and consultancy services over the past three years. Industrial sectors, including manufacturing and infrastructure, are adopting eco-engineered solutions to meet legal obligations and avoid penalties. This trend has accelerated the deployment of advanced technologies, such as IoT sensors and AI-driven compliance platforms, enabling real-time environmental monitoring and faster reporting. As a result, enterprises are increasingly integrating Environmental Construction Services into their project planning and execution strategies to maintain operational efficiency while meeting stringent environmental standards.

High upfront costs associated with advanced environmental construction technologies and sustainable building materials are constraining market growth. Installation of AI-based monitoring systems, advanced remediation equipment, and eco-friendly construction materials requires significant investment, often exceeding USD 1.5 million per large-scale project. Smaller enterprises and emerging market participants may lack the financial capacity to adopt these technologies, limiting market penetration. Additionally, operational complexities and the need for skilled labor to manage environmentally compliant construction processes create further barriers. These financial and logistical challenges slow widespread adoption, despite growing regulatory mandates and sustainability awareness, making cost management a critical factor in expanding the Environmental Construction Services Market.

The global shift toward green and sustainable infrastructure presents significant opportunities for the Environmental Construction Services Market. Governments and private developers are investing heavily in renewable energy facilities, green buildings, and eco-friendly urban planning, creating new demand for environmental compliance, remediation, and monitoring services. For instance, Asia-Pacific is projected to increase environmental construction projects by 28% over the next three years due to rapid urbanization and government sustainability incentives. Technological advancements, such as AI-assisted waste management and BIM for environmental impact assessment, allow service providers to deliver measurable efficiency gains of 15–20% per project. Early adoption in emerging economies offers first-mover advantages, providing companies with opportunities to establish strategic partnerships and integrate innovative solutions tailored to local regulatory and environmental conditions.

Rising costs for advanced monitoring equipment, sustainable materials, and skilled labor pose significant challenges to the Environmental Construction Services Market. Regulatory complexity across regions adds further operational hurdles, as companies must navigate varying compliance standards for emissions, waste disposal, and building certifications. Delays in permit approvals or inconsistent enforcement across jurisdictions can lead to extended project timelines, often increasing costs by 12–18%. Additionally, technological integration requires continuous investment in training, maintenance, and software updates. These challenges affect both market entrants and established players, creating pressure to optimize operational efficiency while maintaining compliance, underscoring the need for strategic investment in technology and process standardization.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Environmental Construction Services market. Approximately 55% of new projects have achieved measurable cost benefits through prefabricated methods. Pre-bent and cut elements are fabricated off-site using automated machinery, reducing labor requirements by up to 30% and accelerating project timelines by 20–25%. Europe and North America are leading in adoption, driven by stringent sustainability regulations and the need for precise, low-waste construction techniques.

• Integration of AI and IoT for Environmental Monitoring: Artificial intelligence and IoT-based monitoring platforms are transforming compliance and operational efficiency. Over 68% of industrial construction sites now utilize smart sensors to monitor soil, water, and air quality in real-time. This integration has reduced manual inspection hours by 40% and improved incident detection accuracy by 33%. Asia-Pacific shows rapid adoption, with smart environmental monitoring implemented in over 120 large-scale projects in 2025 alone.

• Green Materials and Waste Reduction Initiatives: Eco-optimized construction materials are increasingly incorporated into environmental projects, with 47% of commercial projects in North America and Europe reporting a minimum of 25% reduction in construction waste. Innovative recycling techniques and energy-efficient materials are reducing on-site carbon emissions by 15–20%. Adoption of green concrete, recycled steel, and bio-based insulation is becoming standard practice in municipal and industrial projects.

• Digital Project Management and BIM Adoption: Building Information Modeling (BIM) and digital project management tools are being widely implemented to enhance project planning and sustainability compliance. Nearly 62% of environmental construction projects in Europe and North America now use BIM for resource optimization, resulting in 18% faster project approvals and a 12% reduction in on-site errors. This trend is accelerating in emerging markets, where digital workflows are improving collaboration and operational transparency.

The Environmental Construction Services Market is structured around three primary segmentation pillars: type, application, and end-user. By type, offerings range from remediation services and sustainable construction materials to environmental consulting and monitoring solutions, each catering to distinct project requirements. Application segments include municipal infrastructure, industrial facilities, and residential/commercial development, reflecting where environmental services are most critical. End-user segmentation highlights the organizations leveraging these services, including government agencies, construction firms, and large industrial corporations. North America demonstrates the highest adoption in municipal and industrial projects, while Asia-Pacific is rapidly increasing uptake across commercial developments, driven by urban expansion and sustainability initiatives. Understanding these segments allows decision-makers to pinpoint investment priorities, optimize service deployment, and anticipate regional demand shifts across the market.

Remediation services currently lead the market, accounting for approximately 38% of adoption due to high demand in soil and water treatment projects. Their extensive application in industrial and municipal projects ensures consistent uptake, supported by rigorous environmental regulations. Sustainable construction materials are the fastest-growing type, with adoption expected to increase significantly due to rising mandates for eco-friendly infrastructure; these materials now account for 22% of market utilization. Environmental consulting and monitoring solutions hold a combined share of 40%, providing critical expertise in compliance and real-time project assessment.

Municipal infrastructure projects dominate applications, representing around 40% of total adoption, driven by large-scale urban development and stringent environmental compliance requirements. Industrial facilities follow closely, with 30% adoption, while residential and commercial construction accounts for the remaining 30%. Waste reduction and monitoring services are increasingly integrated into industrial applications, making them the fastest-growing area due to the adoption of AI-enabled environmental compliance platforms. Other applications, such as transportation infrastructure and energy projects, contribute niche opportunities and collectively account for approximately 12–15% of market activity.

Government agencies are the leading end-users, representing roughly 42% of market utilization, largely due to mandates for environmental compliance in public works and infrastructure projects. Construction firms are the fastest-growing end-user segment, now capturing 28% of adoption, driven by integration of sustainable building practices and digital environmental monitoring. Industrial corporations, including manufacturing and energy producers, hold the remaining 30%, leveraging environmental construction services for compliance and risk mitigation. Industry adoption rates further illustrate this landscape: over 60% of large-scale industrial plants in North America employ monitoring and remediation services, while 55% of commercial developers in Europe utilize eco-optimized materials.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America maintained leadership due to extensive urban infrastructure projects, industrial remediation initiatives, and high adoption of digital environmental monitoring technologies. Europe accounted for 27% of the global market, driven by stringent environmental regulations and renewable energy infrastructure development. Asia-Pacific held 22% of the market, with China, India, and Japan leading adoption in commercial, industrial, and municipal projects. South America and Middle East & Africa contributed 8% and 5%, respectively, with growing focus on energy efficiency and sustainable construction practices. Overall, the market is shaped by regulatory compliance, technological adoption, and evolving consumer behavior across regions.

How are digital compliance and sustainability driving operational efficiency?

North America holds approximately 38% of the global Environmental Construction Services Market, supported by high demand in industrial, municipal, and commercial construction sectors. Government initiatives, such as stricter emission limits and green building incentives, have accelerated adoption of eco-engineered solutions. Technological advancements, including AI-assisted environmental monitoring and digital project management platforms, have reduced compliance errors by up to 18%. Local players like Jacobs Engineering are integrating advanced soil and water remediation technologies into large-scale infrastructure projects. Enterprise adoption is notably higher in healthcare, finance, and urban infrastructure sectors, reflecting strong regulatory compliance and investment in sustainable practices.

What factors are driving adoption of explainable environmental solutions?

Europe accounts for around 27% of the global Environmental Construction Services Market, with Germany, the UK, and France leading regional adoption. Regulatory pressure from agencies enforcing green building codes and carbon reduction mandates has prompted extensive use of digital compliance tools. Emerging technologies such as BIM and IoT-based monitoring platforms are widely deployed, improving environmental data transparency and project efficiency. Local players, including Skanska’s European operations, are implementing sustainable construction materials and eco-friendly remediation services. Regulatory-driven demand is shaping consumer behavior, with enterprises prioritizing traceable, explainable environmental construction solutions in municipal and commercial projects.

How is rapid urbanization shaping environmental construction adoption?

Asia-Pacific represents 22% of the global Environmental Construction Services Market, with China, India, and Japan as the top-consuming countries. Expansion in commercial infrastructure, manufacturing facilities, and urban development is driving service demand. Innovation hubs in China and India are adopting AI-assisted monitoring systems and smart environmental sensors, improving compliance and efficiency by over 15% in pilot projects. Local players, such as L&T Construction, are integrating sustainable construction practices into large-scale urban projects. Regional consumer behavior is influenced by rapid urbanization and adoption of mobile AI platforms for environmental monitoring, particularly in commercial and industrial segments.

What is shaping environmental compliance in emerging infrastructure projects?

South America holds 8% of the global market, with Brazil and Argentina leading adoption. Demand is driven by infrastructure modernization, renewable energy projects, and industrial compliance requirements. Government incentives for sustainable construction and trade policies encouraging eco-friendly materials have supported market expansion. Local companies, including Andrade Gutierrez, are deploying advanced remediation and waste reduction technologies in industrial and municipal projects. Regional consumer behavior emphasizes cost-effective and environmentally compliant solutions, with project planners increasingly integrating monitoring systems to reduce environmental impact.

How are energy and construction projects driving technological modernization?

Middle East & Africa accounts for roughly 5% of the global Environmental Construction Services Market. Major growth countries include the UAE and South Africa, driven by oil & gas infrastructure, industrial expansion, and urban development. Technological modernization, including AI-enabled environmental monitoring and digital compliance platforms, is increasingly adopted. Local firms, such as Saudi Aramco contractors, are incorporating advanced remediation solutions in industrial and energy projects. Consumer behavior in this region emphasizes regulatory compliance and efficiency in environmental service deployment, with large-scale industrial clients leading adoption.

United States: Market share ~25% – Dominance due to high production capacity, strong regulatory compliance requirements, and widespread adoption of digital monitoring solutions.

Germany: Market share ~12% – Leading adoption driven by stringent sustainability regulations, advanced technological integration, and extensive industrial and municipal infrastructure projects.

The Environmental Construction Services market is moderately fragmented, with over 120 active competitors operating globally, ranging from large multinational corporations to specialized regional firms. The top five companies—AECOM, Jacobs Engineering, Skanska, Turner Construction, and WSP Global—together hold an estimated 48% of the total market, reflecting a balance between established players and smaller innovators. Strategic initiatives such as partnerships, joint ventures, and technology-driven service expansions are shaping the competitive environment. For example, several leading firms have launched AI-enabled environmental monitoring solutions and digital project management platforms, enhancing efficiency and compliance capabilities. Mergers and acquisitions are increasingly common, with larger players acquiring specialized remediation and sustainable construction technology providers to broaden service portfolios. Innovation trends, including adoption of IoT-based environmental sensors, modular and prefabricated construction technologies, and predictive environmental analytics, are key differentiators. Regional variations influence competitive positioning: North American firms lead in technology integration and regulatory expertise, while European companies focus on sustainable materials and compliance consulting. Overall, market competition is driven by technological differentiation, regulatory expertise, and scale of project execution.

Turner Construction

WSP Global

Fluor Corporation

SNC-Lavalin

Bechtel Corporation

Balfour Beatty

Arcadis

The Environmental Construction Services Market is experiencing rapid transformation driven by the adoption of advanced technologies that enhance efficiency, compliance, and sustainability outcomes. Building Information Modeling (BIM) is now implemented in approximately 62% of large-scale projects across North America and Europe, enabling precise planning, resource allocation, and integration of environmental compliance data. BIM allows real-time visualization of construction impact on soil, water, and air, reducing project errors by up to 18% and accelerating regulatory approval processes. Artificial Intelligence (AI) and machine learning are increasingly applied to environmental monitoring, risk assessment, and predictive maintenance. Over 55% of industrial and municipal projects now utilize AI-assisted monitoring platforms, which have improved incident detection accuracy by 33% and reduced manual inspection labor by nearly 40%. These systems analyze large datasets from IoT sensors to optimize remediation efforts, waste management, and energy efficiency.

Internet of Things (IoT) devices are deployed in over 120 major projects in Asia-Pacific and Europe, providing continuous real-time monitoring of air quality, water contamination, and soil conditions. Integration of IoT sensors allows instantaneous alerts, minimizing environmental hazards and enabling faster response times, with measurable reductions in non-compliance incidents by up to 24%. Emerging technologies such as prefabricated and modular construction materials, including eco-optimized concrete and recycled steel, are also driving the market. These materials are used in 55% of new projects, reducing on-site labor requirements by 30% and construction timelines by 20–25%. Additionally, digital project management platforms are increasingly adopted, allowing multi-site project coordination, performance tracking, and enhanced collaboration between stakeholders.

Collectively, these technological advancements position environmental construction services as highly efficient, data-driven, and sustainable, enabling firms to meet strict regulatory standards while improving operational productivity and cost-effectiveness across diverse project types.

• In January 2025, Jacobs Engineering Group completed the acquisition of Groundwater & Environmental Services, enhancing its remediation design-build and groundwater treatment capabilities across North America, allowing more comprehensive contamination cleanup and water treatment solutions on large infrastructure projects and accelerating delivery times.

• In March 2024, Arcadis partnered with Verisk Analytics to co-develop data‑driven remediation planning and risk assessment tools geared toward improving site characterization and cost predictability, marking a significant step in technology‑infused environmental construction workflows.

• In May 2025, Skanska was recognized as a Climate Leader in Europe for its sustained progress in reducing carbon footprints and driving sustainable innovation, reaffirming its leadership position in low‑carbon construction practices and environmental services across major infrastructure projects.

• In December 2025, WSP Global announced a planned $3.3 billion acquisition of TRC Companies, a U.S. energy and environmental services firm, positioning WSP as one of the largest engineering and environmental services providers with expanded power, utilities, and environmental remediation capabilities.

The Environmental Construction Services Market Report offers a comprehensive, multi‑dimensional analysis of market segments, geographic regions, applications, and technological frameworks that define the current and near‑term landscape. The report covers a full spectrum of service types—from remediation and restoration to environmental consulting, compliance management, and monitoring solutions—detailing the role of advanced digital platforms and eco‑engineering practices. It outlines segmentation by type, including traditional remediation services, sustainable construction materials, and environmental risk assessment tools, as well as service applications across municipal infrastructure, industrial facilities, commercial and residential projects. Geographic coverage spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with insights on how regional regulations, consumer adoption patterns, and investment climates shape demand.

The report also evaluates key technological influences, such as the integration of AI‑driven monitoring, IoT environmental sensors, BIM and digital project management systems, and modular construction practices that are redefining project delivery efficiency and environmental performance metrics. Industry focus areas include regulatory compliance, ESG integration, waste management optimization, and climate resilience planning, with numerical insights into adoption rates, project performance improvements, and deployment scales of differentiated solutions. Emerging or niche segments, such as nature‑based solutions, digital twins for environmental modeling, and circular economy practices in construction, are detailed to inform strategic decision‑making. Tailored for business professionals, the report equips stakeholders with actionable intelligence to assess competitive positioning, regional consumption behaviors, and technology adoption pathways across the Environmental Construction Services Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

AECOM, Jacobs Engineering, Skanska, Turner Construction, WSP Global, Fluor Corporation, SNC-Lavalin, Bechtel Corporation, Balfour Beatty, Arcadis |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |