Universal Robots A/S, FANUC Corporation, ABB Ltd., TECHMAN ROBOT INC., KUKA AG, Doosan Robotics Inc., Denso Corporation, Yaskawa Electric Corporation, Rethink Robotics GmbH, AUBO Robotics

Reports

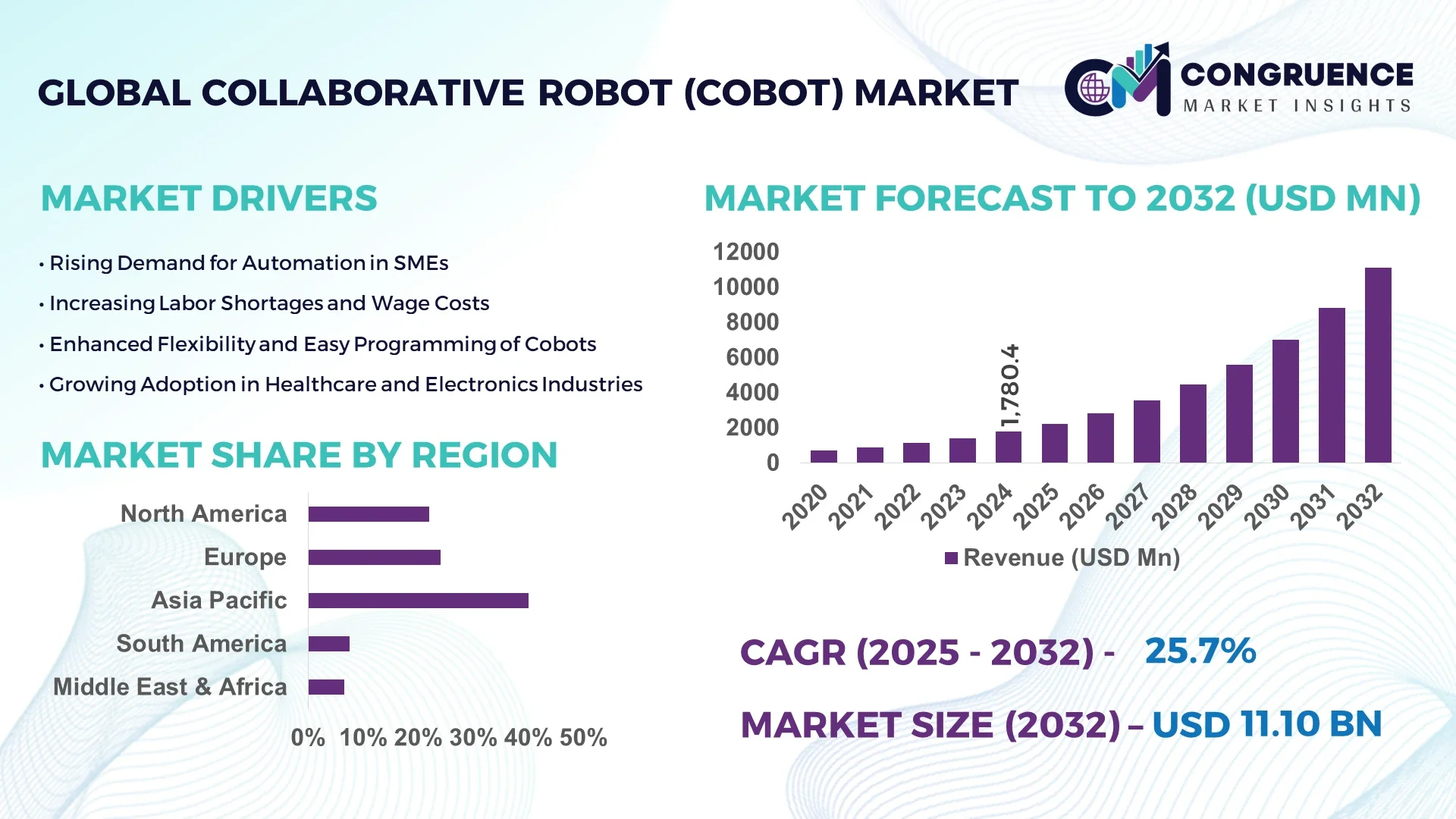

The Global Collaborative Robot (Cobot) Market was valued at USD 1,780.4 Million in 2024 and is anticipated to reach a value of USD 11,096.9 Million by 2032 expanding at a CAGR of 25.7% between 2025 and 2032.

The Collaborative Robot (Cobot) Market is redefining automation across manufacturing and industrial sectors by enabling humans and machines to work safely side-by-side. Unlike traditional robots, cobots are lightweight, flexible, and easy to program, making them ideal for small and medium enterprises looking to automate tasks without major infrastructure changes. The adoption of cobots is growing significantly due to their ability to perform repetitive, high-precision tasks efficiently. Industries such as electronics, automotive, and food processing are integrating cobots for assembly, testing, and packaging. The global emphasis on human safety, cost savings, and productivity enhancement is accelerating the growth of collaborative robots, especially in regions with rising labor costs and aging workforces.

Artificial Intelligence is playing a crucial role in enhancing the intelligence, flexibility, and efficiency of collaborative robots (cobots). With AI integration, cobots are now able to understand context, learn from interactions, and adapt to new tasks without reprogramming. AI-enabled cobots are increasingly deployed in dynamic environments such as warehouse logistics, surgical assistance, and quality control in electronics manufacturing. Cobots powered by machine learning algorithms can optimize their movements in real-time, reducing energy consumption and improving accuracy. AI also allows for natural language processing and computer vision, giving cobots the ability to recognize objects, assess defects, and collaborate with human workers using gestures and voice commands. The increased autonomy and smart adaptability of AI-powered cobots have opened up new application frontiers in the service sector and consumer electronics assembly. As businesses look for agility and cost efficiency, AI is emerging as a game-changer in collaborative robot systems.

In February 2024, Universal Robots introduced AI-enhanced cobots equipped with advanced vision systems capable of real-time 3D object recognition, allowing them to pick irregular items in logistics and packaging operations with over 95% accuracy.

The Collaborative Robot (Cobot) Market is experiencing a technological evolution driven by automation, safety, and cost-effectiveness. Cobots are becoming essential in human-machine hybrid workplaces. The shift towards Industry 4.0 and smart manufacturing is further fueling their demand. Emerging economies in Asia Pacific are investing in factory automation to stay competitive globally. Meanwhile, Europe is witnessing a surge in cobot deployment in high-precision tasks like electronics assembly and medical device manufacturing. The market dynamics are also influenced by evolving labor laws, demand for improved workplace ergonomics, and the increasing need to maintain production efficiency amidst labor shortages.

The rising demand for precision and consistency in the electronics and automotive sectors is pushing companies to deploy cobots for tasks such as screwdriving, soldering, and component insertion. In 2024, over 38% of cobot deployments globally were in electronics and automotive assembly lines. Cobots help reduce production errors, enhance yield, and maintain flexible manufacturing lines. Their quick redeployment capability adds to their value, especially for manufacturers dealing with frequent design changes and small batch production runs.

Despite their flexible design, many small and mid-sized manufacturers find the initial investment in collaborative robots to be high. The cost of sensors, end-effectors, AI integration, and safety certifications adds to the capital expenditure. In 2024, more than 45% of SMEs in developing regions cited high integration costs as a barrier to cobot adoption. Additionally, the complexity involved in training personnel to operate and maintain AI-powered cobots also poses a hurdle for first-time adopters.

The healthcare industry is rapidly emerging as a significant adopter of collaborative robots, especially for drug dispensing, physical therapy, and surgical assistance. In 2024, healthcare-related cobot deployments grew by nearly 32%, with cobots being used for repetitive and delicate operations. Their precision and low error rates are crucial in reducing human fatigue in long surgical procedures and diagnostic tests. As patient load rises and healthcare staffing faces constraints, the opportunity for cobots in this sector continues to expand.

One of the major challenges facing the Collaborative Robot (Cobot) Market is the lack of skilled operators and the resistance from workers fearing job displacement. While cobots are designed to assist rather than replace workers, over 40% of surveyed employees in 2024 expressed concern about job security due to increasing cobot usage. Additionally, the lack of training programs and insufficient knowledge of programming or AI-enhanced systems creates hurdles in smooth cobot integration, especially in non-technical sectors.

The Collaborative Robot (Cobot) Market is undergoing dynamic transformation with rapid adoption across sectors. One key trend is the miniaturization of cobots, making them more accessible to space-constrained production units. In 2024, compact cobots under 10kg payload capacity accounted for nearly 55% of total shipments globally. There's also a growing trend of integrating cobots with cloud platforms for remote monitoring and predictive maintenance, enhancing uptime and efficiency. Another significant development is the rising customization of cobots for niche applications such as laboratory research and jewelry manufacturing. Dual-arm cobots with AI-powered coordination systems are being introduced to manage complex multi-step tasks without human intervention. The market is also witnessing a surge in plug-and-play cobots that require minimal setup time and can be operational within hours. Furthermore, rental and leasing models for cobots are gaining traction among SMEs, allowing them to experiment with automation without heavy capital investment. This trend is expected to continue, especially in emerging economies seeking productivity enhancements.

The Collaborative Robot (Cobot) Market is segmented into various categories based on type, application, and end-user industries. This segmentation allows manufacturers and investors to pinpoint key growth areas and deploy resources effectively. By analyzing the specific performance and adoption trends of different types of cobots, their applications in industrial settings, and the demand from various end-user sectors, a clearer picture emerges of how this market is evolving globally. Each segment reveals distinct dynamics influenced by automation needs, labor costs, precision requirements, and industry-specific challenges. Understanding the segmentation is critical for strategic decision-making and for identifying areas with the highest potential for cobot integration and ROI.

Upright Cobots: Upright collaborative robots dominate the market due to their vertical movement capacity, versatility, and widespread adoption in industrial setups. These cobots are primarily used in material handling, machine tending, and palletizing operations. In 2024, upright cobots accounted for over 34% of global shipments. Their ability to operate in both narrow and high-clearance workspaces makes them ideal for logistics and warehouse automation. Upright cobots offer enhanced reach and payload handling, contributing significantly to automation efficiency. With programmable interfaces and robust safety features, upright cobots are increasingly replacing traditional robotic arms in SMEs looking for compact yet powerful automation tools.

SCARA Cobots: SCARA (Selective Compliance Articulated Robot Arm) cobots are gaining traction in high-speed and high-precision operations. In 2024, SCARA cobots witnessed a 29% adoption rate in sectors such as electronics and semiconductor assembly. These cobots are highly efficient in pick-and-place, insertion, and small component assembly tasks. Their compact footprint and horizontal movement design make them suitable for cleanroom environments and compact assembly lines. SCARA cobots are preferred where speed and repeatability are critical, particularly in repetitive production lines requiring consistent performance. Their growing integration into circuit board manufacturing and sensor calibration highlights their relevance in precision-driven markets.

Articulated Cobots: Articulated cobots, known for their human-like arm movement and high degree of flexibility, are widely used in complex manufacturing environments. These cobots can perform multi-axis operations and adapt to varied tasks such as welding, gluing, and polishing. In 2024, articulated cobots captured over 26% of the global market share. Automotive and aerospace sectors are prime adopters, leveraging their precision and adaptability for high-torque tasks. The ability to mimic human arm movements makes articulated cobots ideal for labor-intensive applications. Their enhanced motor control and sensor fusion technology also contribute to safety and operational efficiency in human-robot collaboration zones.

Others: The "Others" category includes delta, cylindrical, and dual-arm cobots, which serve niche yet growing needs in the market. Delta cobots are commonly used for lightweight pick-and-place applications in food and pharmaceutical industries. Dual-arm cobots, introduced recently, are capable of handling complex bimanual tasks such as circuit board testing and medical kit assembly. In 2024, these non-mainstream cobots showed a combined growth of 18% year-over-year due to their customized applications and unique operational design. As industries increasingly demand specialized solutions, these cobot types are gaining relevance across precision-critical and hygiene-sensitive segments.

Assembly: Assembly remains one of the top applications for collaborative robots, particularly in electronics and consumer goods manufacturing. Cobots are extensively used for screwdriving, fastening, and small-part assembly due to their accuracy and fatigue-free operation. In 2024, over 30% of cobot deployments were for assembly tasks. Their ease of programming and consistent force application enhance product quality and reduce defect rates. Cobots also allow for modular assembly line setups, making it easier for manufacturers to adapt to product changes. Their collaborative nature minimizes workplace injuries and improves ergonomic working conditions, especially in repetitive or awkward tasks.

Pick & Place: Pick & place operations have become a cornerstone of cobot utilization, especially in packaging, sorting, and logistics. In 2024, this application accounted for more than 25% of cobot usage. Cobots used for pick & place tasks are designed with advanced grippers and AI-enabled vision systems to identify and handle items of various shapes and sizes. They are highly effective in fast-paced production lines and e-commerce fulfillment centers. The reduction in human handling not only boosts throughput but also improves hygiene, making pick & place cobots ideal for food and pharmaceutical sectors where contamination must be minimized.

Packaging: Cobots are revolutionizing packaging operations by performing tasks such as box folding, labeling, sealing, and palletizing with high accuracy. In 2024, packaging applications grew significantly, contributing to over 20% of the total cobot installations globally. Their ability to work safely alongside human operators ensures smooth workflows, especially during seasonal demand spikes. Cobots can adapt to different packaging formats and automate end-of-line processes without major line modifications. Their scalability makes them a top choice for both startups and large manufacturing units aiming to optimize packaging throughput while maintaining quality control.

Quality Testing: Quality testing cobots are becoming indispensable in electronics, automotive, and medical device industries. These cobots are integrated with advanced sensors, cameras, and data analytics tools to identify defects in real-time. In 2024, cobots for quality testing saw a 24% increase in demand. They can perform non-destructive tests, visual inspections, and functional verifications with minimal human supervision. Cobots reduce the margin for error and ensure product consistency, which is vital for highly regulated industries. The ability to record and analyze test data in real-time also supports compliance and traceability standards.

Others: Other applications include machine tending, polishing, soldering, welding, and drug dispensing in healthcare. In 2024, these applications made up roughly 18% of the cobot market. Machine tending cobots enhance CNC and injection molding productivity, while cobots used in welding and gluing ensure uniform output with less waste. Their integration into non-traditional sectors like agriculture and hospitality is also expanding, with cobots being tested for precision farming and automated barista services. These emerging use cases signal a future where cobots become part of everyday operational settings beyond industrial floors.

Automotive: The automotive sector continues to lead in cobot adoption, contributing to nearly 35% of global usage in 2024. Cobots in this sector are utilized for spot welding, painting, assembly, and quality inspection. Their flexibility allows them to switch between models and designs, supporting mass customization in vehicle manufacturing. Automotive OEMs and component manufacturers deploy cobots to boost production throughput, minimize errors, and improve workplace safety. As electric vehicle (EV) production increases, cobots are being introduced for battery assembly, connector placement, and high-voltage system installation, driving further demand in this segment.

Electronics: Electronics manufacturers rely heavily on cobots for tasks demanding precision and static-free environments. In 2024, the electronics sector accounted for 28% of the total market share. Cobots are widely used for circuit board handling, micro-welding, and display assembly. Their ability to operate with minimal vibration and static discharge makes them ideal for delicate semiconductor tasks. The increasing complexity of consumer electronics and the miniaturization of components are further pushing the demand for cobots that can perform intricate tasks quickly and consistently without compromising quality.

Healthcare: Healthcare is emerging as one of the fastest-growing end-users of collaborative robots. In 2024, healthcare applications witnessed a 30% surge in adoption. Cobots are deployed for tasks such as drug dispensing, lab automation, and surgical assistance. Their role in pandemic preparedness and reducing hospital-acquired infections has also boosted demand. Cobots contribute to improving operational efficiency in laboratories and hospitals by automating repetitive, time-sensitive procedures. They also aid in patient care and rehabilitation, enabling healthcare professionals to focus on more critical tasks.

Food & Beverage: The food and beverage industry is increasingly integrating cobots to meet hygiene standards and improve production speed. In 2024, this sector represented 22% of cobot deployments. Cobots are used for packaging, filling, sorting, and palletizing tasks under strict cleanliness protocols. They reduce cross-contamination risks and ensure uniform portioning, making them suitable for meat processing, dairy packaging, and ready-to-eat food assembly. Cobots are also gaining ground in specialty food preparation like chocolate molding and cake decoration, supporting customized and artisanal production.

Others: Other end-user segments include logistics, retail, education, and pharmaceuticals. In 2024, these segments collectively contributed to over 15% of cobot utilization. In logistics, cobots handle sorting and bin-picking in warehouses. In education, they are used as training tools in robotics and automation labs. Pharmaceutical companies deploy cobots for pill sorting, vial filling, and sterile handling. These diversified use cases highlight the market’s expansion beyond traditional industries and underscore the potential for cobots in both commercial and academic domains.

Asia Pacific accounted for the largest market share at 41.3% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 27.6% between 2025 and 2032.

The robust adoption of automation across Asia Pacific’s manufacturing sector, especially in China, Japan, and South Korea, continues to drive massive demand for collaborative robots. Rising labor costs and the need for operational efficiency are accelerating cobot deployment in production lines. In contrast, North America is witnessing a surge in demand due to Industry 4.0 initiatives, labor shortages, and advancements in AI-driven robotics. Companies across sectors like automotive, electronics, and healthcare are accelerating cobot investments to meet productivity goals.

High Demand for Human-Robot Collaboration in Smart Manufacturing

The North America collaborative robot market is witnessing strong momentum due to increasing adoption in smart factories and agile manufacturing lines. In 2024, the region accounted for 24.8% of the global cobot market. The U.S. leads in integration, with cobots being deployed for welding, packaging, and inspection across automotive and aerospace sectors. Healthcare applications, including surgical assistance and diagnostics, have also grown rapidly. Canada is focusing on cobot training in educational institutions and research labs, creating future-ready automation ecosystems. With a strong base of robotics companies and tech-driven startups, the region is scaling cobot use across SMEs and large manufacturers alike.

Strong Growth in Automotive and Electronics Sectors

Europe represented 21.6% of the global cobot market in 2024, driven by widespread automation in Germany, France, and the UK. Germany, being a major automotive hub, heavily utilizes cobots in component assembly, precision welding, and logistics. In the UK, collaborative robots are gaining momentum in electronics assembly and healthcare logistics. The European Union’s emphasis on sustainable manufacturing and workplace safety further supports cobot adoption. Cobots are increasingly seen in cleanroom environments, food processing units, and pharmaceutical labs. Manufacturers are also deploying cobots to address an aging workforce and maintain operational efficiency with minimal human error.

Industrial Automation Surge Across China, Japan, and South Korea

Asia Pacific led the market with a 41.3% share in 2024, with China dominating regional sales. Major economies like Japan and South Korea are investing in next-gen robotic automation for automotive, electronics, and food sectors. China’s “Made in China 2025” initiative fuels the rapid adoption of cobots in small and medium-sized factories. Japan continues to innovate in humanoid and lightweight cobots for precise assembly and cleanroom tasks. South Korea is focusing on AI-integrated cobots for semiconductor production and logistics. The region’s manufacturing density, tech advancements, and labor shortage issues collectively make it the most lucrative cobot market worldwide.

Emerging Automation Needs in Oil, Gas, and Healthcare

The Middle East & Africa collaborative robot market is in a nascent stage but showing promising growth. In 2024, it held a 4.2% market share. The UAE and Saudi Arabia are leading regional adoption, especially in oil & gas infrastructure, where cobots are used for inspection, pipeline welding, and hazard monitoring. Healthcare providers in the UAE are investing in robotic solutions for lab testing and surgical procedures. South Africa is seeing early-stage adoption in automotive and logistics, particularly in port operations and warehousing. Government-backed digital transformation initiatives are creating a foundation for cobot expansion across industrial, utility, and medical sectors.

The global Collaborative Robot (Cobot) market is characterized by intense competition, with both established players and emerging startups striving to enhance their market presence. In 2024, established companies accounted for approximately 68% of the market share, while startups captured the remaining 32%. This dynamic landscape is fueled by continuous technological advancements and the growing demand for automation across various industries.

Key players are focusing on expanding their product portfolios and improving the capabilities of their cobots to cater to a broader range of applications. For instance, in November 2023, Universal Robots introduced the UR30, a 30 kg payload cobot designed for tasks requiring higher payloads and precision. Similarly, in December 2023, Fanuc launched the CRX-10iA, a lightweight cobot weighing only 39 kg, suitable for applications in driverless transport systems and AGVs.

Strategic collaborations are also prevalent in the market. In June 2023, Universal Robots and SICK AG partnered to develop an innovative safety solution, enhancing the safety measures in human-robot collaborative applications. Such collaborations aim to integrate advanced technologies and improve the overall efficiency and safety of cobot operations.

The competitive landscape is further intensified by the entry of new players and the continuous evolution of existing technologies. Companies are investing heavily in research and development to innovate and stay ahead in the market. As the demand for collaborative robots continues to rise, the market is expected to witness increased competition and the introduction of more advanced and versatile cobots.

Universal Robots A/S (Denmark)

FANUC Corporation (Japan)

ABB Ltd. (Switzerland)

TECHMAN ROBOT INC. (Taiwan)

KUKA AG (Germany)

Doosan Robotics Inc. (South Korea)

Denso Corporation (Japan)

Yaskawa Electric Corporation (Japan)

Rethink Robotics GmbH (Germany)

AUBO Robotics (China)

The technological landscape of the Collaborative Robot (Cobot) market is rapidly evolving, driven by advancements in artificial intelligence (AI), machine learning, and sensor technologies. These innovations are enhancing the capabilities of cobots, making them more adaptable, intelligent, and efficient in various industrial applications.

AI integration is enabling cobots to learn from their environment and improve their performance over time. For example, the use of machine learning algorithms allows cobots to optimize their movements and tasks based on real-time data, reducing errors and increasing productivity. Additionally, advancements in computer vision are enabling cobots to better recognize objects and navigate complex environments, enhancing their utility in sectors like manufacturing and logistics.

Sensor technologies are also playing a crucial role in the development of cobots. High-precision force sensors and torque sensors are allowing cobots to perform delicate tasks with greater accuracy and safety. These sensors enable cobots to detect and respond to human presence, ensuring safe collaboration in shared workspaces.

Moreover, the integration of Internet of Things (IoT) technologies is facilitating real-time monitoring and control of cobots, allowing for predictive maintenance and reducing downtime. This connectivity is also enabling seamless integration of cobots into existing industrial automation systems, enhancing overall operational efficiency.

The development of user-friendly programming interfaces is making it easier for non-experts to program and operate cobots. Graphical user interfaces and drag-and-drop programming tools are reducing the learning curve and expanding the adoption of cobots across various industries.

As technology continues to advance, cobots are expected to become more versatile and capable, opening up new applications and driving further growth in the market. Continuous innovation and investment in research and development will be key to unlocking the full potential of collaborative robots in the coming years.

In November 2023, TECHMAN ROBOT INC. unveiled the TM AI Cobot TM25S at iREX 2023, featuring a 25kg payload capacity and integration with NVIDIA's Isaac Sim platform, reducing programming times by 70% and cycle times by 20%.

In June 2023, Universal Robots A/S and SICK AG collaborated on a safety solution for human-robot collaborative applications, introducing a protective volume around the robot tool and handled objects, facilitating easier deployment.

In December 2023, Fanuc Corp. launched the CRX-10iA, a lightweight cobot weighing 39kg, suitable for applications in driverless transport systems and AGVs, with reach options of 1,200mm and 1,400mm and a maximum payload of 10kg.

In May 2023, MG Tech Group introduced a high-duty cobot palletizer featuring an HC30 Yaskawa cobot and a Rockwell Automation system, capable of up to 6 cycles per minute and saving up to 15% more space compared to standard robotic palletizers.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series, featuring a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

The Collaborative Robot (Cobot) Market Report provides a comprehensive analysis of the global market, focusing on key trends, growth drivers, challenges, and opportunities. It covers various aspects of the market, including product types, applications, end-user industries, and regional insights.

The report delves into the different types of cobots available in the market, such as articulated, SCARA, and cartesian, highlighting their specific features and applications. It also examines the diverse applications of cobots across industries like automotive, electronics, healthcare, and logistics, providing insights into how these robots are transforming operations and improving efficiency.

End-user insights are a crucial component of the report, offering an in-depth understanding of how various industries are adopting cobots to address labor shortages, enhance productivity, and ensure workplace safety. The report also explores the regional dynamics of the market, identifying key

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1,780.4 Million |

|

Market Revenue in 2032 |

USD 11,096.9 Million |

|

CAGR (2025 - 2032) |

25.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |