Reports

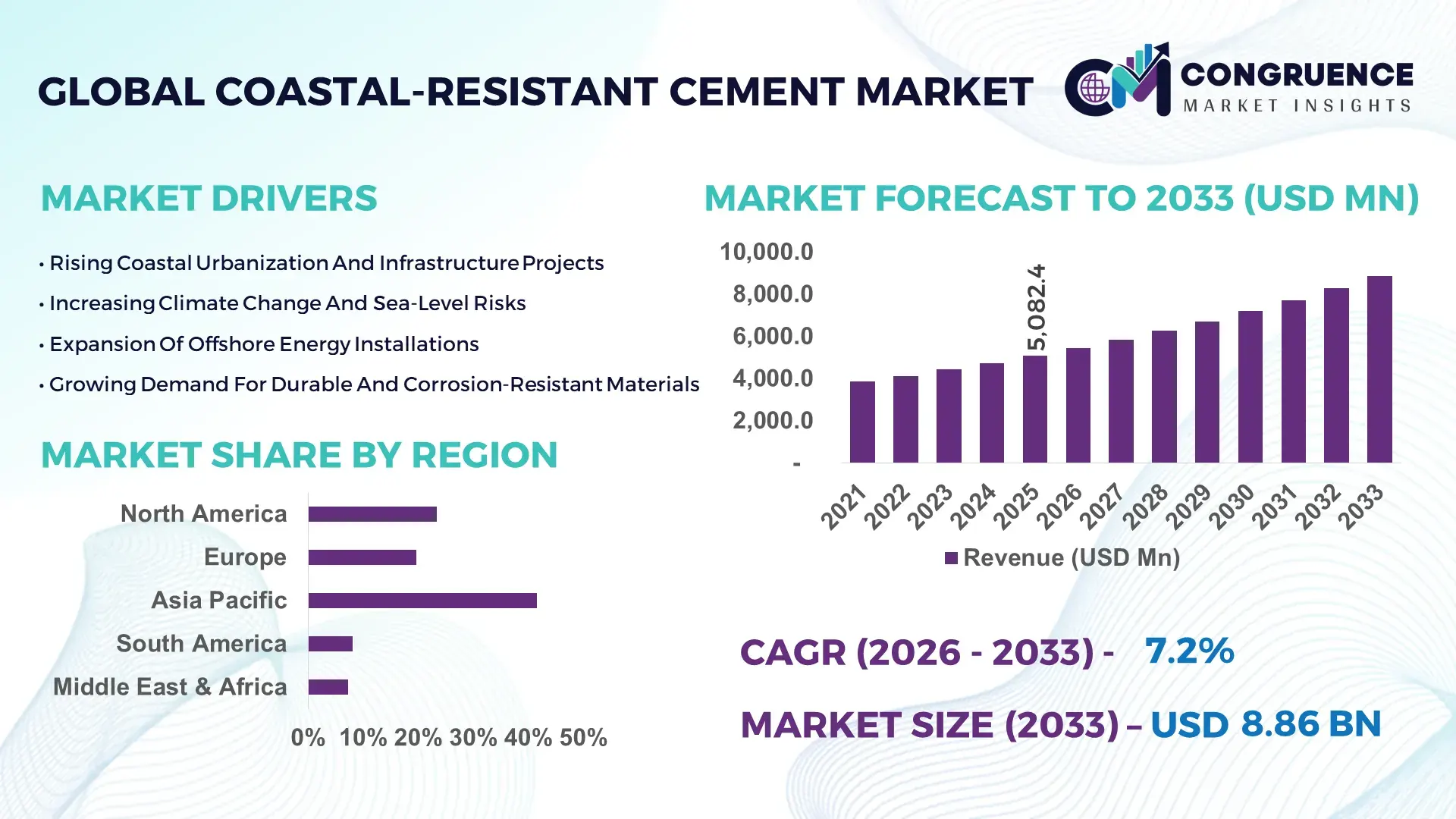

The Global Coastal-Resistant Cement Market was valued at USD 5,082.4 Million in 2025 and is anticipated to reach a value of USD 8,863.9 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by increasing coastal infrastructure development and the need for durable, salt-resistant construction materials.

China represents the most dominant country in the Coastal-Resistant Cement market, supported by an annual cement production capacity exceeding 2.1 billion metric tons, with specialized marine-grade and sulfate-resistant cement accounting for nearly 8% of total output. More than 14,000 kilometers of coastline development projects, including ports, bridges, and offshore wind foundations, utilize high-durability cement formulations. In 2025, over 35% of new coastal urban construction projects incorporated chloride-resistant blended cement technologies. Investments exceeding USD 120 billion in coastal infrastructure modernization have accelerated adoption of low-permeability, high-performance cement variants designed for aggressive marine environments.

Market Size & Growth: Valued at USD 5,082.4 million in 2025, projected to reach USD 8,863.9 million by 2033 at 7.2% CAGR, driven by coastal urbanization and marine infrastructure expansion.

Top Growth Drivers: Coastal infrastructure spending (42%), marine port expansion (37%), climate resilience projects (34%).

Short-Term Forecast: By 2028, advanced sulfate-resistant cement is expected to improve structural lifespan by 18%.

Emerging Technologies: Nano-silica additives, low-permeability blended cement, corrosion-inhibiting admixtures.

Regional Leaders: Asia-Pacific projected at USD 3.6 billion by 2033; North America at USD 2.1 billion; Europe at USD 1.8 billion with sustainable marine construction focus.

Consumer/End-User Trends: Over 58% of coastal infrastructure contractors prioritize chloride-resistant cement blends.

Pilot or Case Example: In 2024, a port redevelopment project achieved 22% reduction in maintenance costs using advanced marine-grade cement.

Competitive Landscape: LafargeHolcim leads with ~19% marine cement presence, followed by CEMEX, Heidelberg Materials, UltraTech Cement, and Anhui Conch Cement.

Regulatory & ESG Impact: Coastal resilience standards promoting 25% lower permeability thresholds.

Investment & Funding Patterns: Over USD 60 billion allocated globally to coastal protection and marine infrastructure projects in 2025.

Innovation & Future Outlook: Carbon-reduced marine cement and AI-driven durability testing shaping next-generation materials.

Marine construction accounts for approximately 46% of Coastal-Resistant Cement demand, followed by coastal residential infrastructure at 28%, industrial facilities at 15%, and offshore energy projects at 11%. Innovations in pozzolanic blending and corrosion-resistant admixtures are improving compressive strength by 12% while reducing chloride penetration by up to 30%. Regional consumption is highest in Asia-Pacific and North America, reflecting extensive port modernization and climate-resilient infrastructure initiatives.

The Coastal-Resistant Cement Market plays a strategic role in ensuring long-term structural integrity in aggressive marine environments. Advanced nano-silica-enhanced cement formulations deliver 28% improvement in chloride resistance compared to traditional Portland cement.

Asia-Pacific dominates in coastal infrastructure volume, while Europe leads in sustainable adoption with over 62% of marine projects integrating low-carbon cement blends. By 2027, AI-based durability monitoring systems are expected to improve predictive maintenance planning by 20%, reducing lifecycle repair costs.

Firms are committing to 30% reduction in embodied carbon emissions by 2030 through alternative clinker formulations and supplementary cementitious materials. In 2025, a coastal bridge project in Southeast Asia achieved 17% longer projected service life using advanced sulfate-resistant cement technology.

Future pathways emphasize climate-resilient infrastructure, offshore wind expansion, and carbon-neutral cement innovation. Integration of smart monitoring sensors and performance analytics is enhancing durability assurance. The Coastal-Resistant Cement Market is positioned as a cornerstone of resilient coastal development, regulatory compliance, and sustainable infrastructure planning.

The Coastal-Resistant Cement market is influenced by expanding marine construction activities, rising sea-level concerns, and regulatory mandates for durable infrastructure. Coastal cities are investing heavily in flood barriers, port expansions, and seawall reinforcement projects. Aggressive chloride and sulfate exposure necessitate specialized cement formulations with reduced permeability and enhanced compressive strength. Infrastructure resilience policies encourage adoption of high-performance cement blends. Competitive differentiation focuses on durability metrics, lifecycle cost efficiency, and environmental compliance. Increasing offshore renewable energy installations further contribute to demand for corrosion-resistant concrete foundations.

Global coastal urbanization projects exceed USD 200 billion annually, increasing demand for high-durability construction materials. Ports and harbors account for over 30% of marine cement consumption. Coastal bridge construction projects require compressive strengths exceeding 50 MPa to withstand saline exposure. Advanced sulfate-resistant cement reduces structural degradation by up to 25%, extending service life. These measurable benefits are accelerating adoption across marine and shoreline infrastructure.

Coastal-Resistant Cement incorporates specialized additives such as pozzolans and corrosion inhibitors, increasing manufacturing costs by 12%–18% compared to standard cement. Energy-intensive production processes and quality testing add operational expenses. Smaller contractors may hesitate to adopt premium-grade cement due to upfront cost considerations, limiting penetration in budget-sensitive projects.

Offshore wind and tidal energy projects require durable foundation materials resistant to saline corrosion. Over 250 GW of offshore wind capacity is planned globally by 2030. Specialized cement blends with 30% lower permeability are increasingly specified for turbine bases and marine pylons, creating long-term growth opportunities.

Cement production contributes approximately 7% of global CO₂ emissions. Regulatory mandates demand lower clinker content and alternative binders, increasing R&D investment requirements. Balancing durability performance with emission reduction goals remains a complex industry challenge.

Integration of Nano-Additives for Enhanced Durability: In 2025, over 29% of marine cement formulations incorporated nano-silica additives, improving compressive strength by 12% and reducing chloride permeability by 28%.

Adoption of Low-Carbon Blended Cement: Approximately 34% of new coastal infrastructure projects specified blended cement with supplementary materials, lowering embodied carbon by 20% while maintaining structural performance.

Growth in Offshore Renewable Infrastructure: Offshore wind foundation projects increased by 24% in 2025, driving demand for sulfate-resistant cement capable of extending structural lifespan beyond 40 years.

Advanced Durability Monitoring Systems: Around 31% of major coastal bridge projects integrated sensor-based monitoring, enabling predictive maintenance that reduced repair frequency by 18%.

The Coastal-Resistant Cement market is segmented by type, application, and end-user categories. Types include sulfate-resistant cement, marine-grade blended cement, high-performance pozzolanic cement, and corrosion-inhibiting specialty cement. Applications span marine infrastructure, coastal residential buildings, industrial facilities, seawalls, and offshore energy installations. End-users include construction contractors, infrastructure developers, government agencies, and energy companies. Demand patterns vary based on project scale, exposure severity, and regulatory standards. Large-scale marine projects prioritize high-strength, low-permeability blends, while residential coastal construction focuses on durability and cost optimization.

Sulfate-resistant cement accounts for approximately 44% of adoption due to its superior resistance to aggressive marine environments. Marine-grade blended cement represents 28%, while pozzolanic cement holds 17%. Corrosion-inhibiting specialty cement is the fastest-growing segment, projected at 9.1% CAGR due to rising offshore energy demand. The remaining 11% includes hybrid performance blends.

In 2025, a national infrastructure authority reported that advanced sulfate-resistant cement improved projected bridge service life by 15% in coastal environments.

Marine infrastructure leads with 46% share, followed by coastal residential construction at 28%, industrial facilities at 15%, and offshore energy at 11%. Offshore energy applications are expanding fastest at 8.4% CAGR due to global wind farm installations. In 2025, more than 38% of infrastructure developers reported piloting Coastal-Resistant Cement blends with enhanced chloride resistance in new shoreline projects.

In 2025, a public coastal protection initiative deployed advanced marine-grade cement across 120 km of seawall reinforcement to improve long-term durability.

Construction contractors account for 52% of demand, infrastructure developers 27%, government agencies 14%, and energy companies 7%. Offshore energy developers represent the fastest-growing end-user segment at 8.8% CAGR. In 2025, over 60% of coastal municipal authorities prioritized high-durability cement standards in new infrastructure tenders.

In 2025, a national port modernization program mandated the use of sulfate-resistant cement across more than 300 new docking structures to enhance marine resilience.

Asia-Pacific accounted for the largest market share at 41.6% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

Asia-Pacific consumed more than 52 million metric tons of Coastal-Resistant Cement in 2025, driven by over 18,000 km of active coastline infrastructure projects across China, India, Japan, and Southeast Asia. North America represented 23.4% of the Coastal-Resistant Cement market, supported by over 3,500 coastal bridge and port rehabilitation projects. Europe held 19.7%, with more than 1,200 marine defense and seawall modernization initiatives. South America accounted for 8.1%, led by Brazil’s port expansions and offshore energy installations. Middle East & Africa contributed 7.2%, with coastal mega-project investments exceeding USD 35 billion in 2025, particularly in the UAE and Saudi Arabia. Regional consumption patterns highlight increased adoption of sulfate-resistant blends in high-salinity environments, where chloride penetration resistance thresholds improved by up to 28% in new infrastructure tenders.

How is climate-resilient infrastructure investment strengthening marine-grade cement adoption?

This region accounts for approximately 23.4% of the Coastal-Resistant Cement market in 2025, supported by over 95,000 miles of U.S. shoreline and extensive port infrastructure. Key industries driving demand include marine transportation, offshore wind energy, coastal residential construction, and defense infrastructure. Federal infrastructure funding exceeding USD 50 billion for coastal resilience projects accelerated adoption of chloride-resistant cement blends. More than 62% of new port rehabilitation contracts specified sulfate-resistant or blended pozzolanic cement. A major regional cement producer expanded low-permeability cement production capacity by 15% to meet growing marine construction demand. Technological adoption includes digital durability monitoring and corrosion-inhibiting admixtures that extend structural life beyond 40 years. Regional contractor behavior reflects strong compliance alignment with stringent coastal building codes and environmental performance standards.

Why are sustainability-driven construction standards elevating demand for durable marine cement?

Europe represents nearly 19.7% of the Coastal-Resistant Cement market, led by Germany, the United Kingdom, France, Italy, and Spain. More than 1,200 active coastal protection projects in 2025 required advanced sulfate-resistant cement formulations. EU-driven carbon reduction initiatives promoted blended cement adoption, with 48% of marine construction projects integrating supplementary cementitious materials to reduce clinker usage. Approximately 57% of contractors reported prioritizing low-permeability cement for long-term seawall reinforcement. A leading European cement manufacturer introduced carbon-reduced marine cement capable of lowering embodied emissions by 20% while maintaining 50 MPa compressive strength. Regulatory pressure encourages traceability and lifecycle performance documentation, influencing procurement behavior toward advanced Coastal-Resistant Cement solutions.

What drives large-scale coastal urbanization and marine infrastructure expansion?

Asia-Pacific leads global consumption with 41.6% market share in 2025. China, India, Japan, and Indonesia account for over 78% of regional marine cement demand. Infrastructure investments exceeding USD 120 billion annually support port expansion, coastal highways, and offshore wind projects. More than 30 million metric tons of sulfate-resistant cement were utilized for marine-grade concrete structures in 2025 alone. A regional cement leader enhanced nano-silica blending capacity, improving chloride resistance by 25% across coastal projects. Urban coastal megacities demonstrate high adoption rates of low-permeability cement formulations to withstand saline corrosion. Growth is further driven by industrial ports and offshore renewable energy installations.

How are port modernization and offshore energy projects increasing specialized cement usage?

South America accounts for 8.1% of the Coastal-Resistant Cement market, with Brazil and Argentina representing over 65% of regional demand. Port capacity expansion projects increased marine-grade cement usage by 18% in 2025. Offshore oil and gas platforms required corrosion-resistant concrete with service life projections exceeding 35 years. Government-backed coastal infrastructure upgrades allocated more than USD 8 billion for resilience projects. A regional producer expanded sulfate-resistant cement output by 12% to support harbor reinforcement initiatives. Adoption patterns focus on long-term durability and cost-effective lifecycle performance in high-humidity environments.

Why are coastal megaprojects and industrial ports accelerating high-performance cement demand?

Middle East & Africa holds 7.2% of the Coastal-Resistant Cement market in 2025, led by UAE, Saudi Arabia, and South Africa. Coastal megaproject investments exceeding USD 35 billion support marine tourism infrastructure, industrial ports, and desalination facilities. Over 220 large-scale shoreline developments specify low-permeability cement blends. A regional cement supplier increased production of sulfate-resistant variants by 20% to meet project specifications. Technological modernization includes corrosion-inhibiting additives and high-strength marine concrete formulations exceeding 55 MPa compressive strength. Demand is concentrated in urban coastal hubs where infrastructure resilience is critical.

China Coastal-Resistant Cement Market – 29.4%: Extensive coastal infrastructure expansion and high marine construction capacity drive sustained demand.

United States Coastal-Resistant Cement Market – 17.8%: Large-scale shoreline protection programs and offshore energy investments support specialized cement adoption.

The Coastal-Resistant Cement market exhibits a moderately consolidated competitive structure, with approximately 55 global cement producers actively manufacturing marine-grade and sulfate-resistant variants. The top five companies collectively account for nearly 46% of global Coastal-Resistant Cement supply. Competitive positioning centers on production capacity, durability innovation, and regional distribution networks. In 2025, more than 35 plant upgrades focused on integrating supplementary cementitious materials and corrosion-resistant additives. Manufacturing facilities increased blended cement output by 14% year-over-year to align with carbon reduction mandates. Strategic partnerships with construction firms strengthened supply chain integration for major coastal megaprojects. Innovation investment prioritizes nano-additive integration, low-carbon clinker substitution, and digital quality monitoring systems to enhance compressive strength and permeability resistance. Producers differentiate through lifecycle performance guarantees exceeding 40-year durability projections for marine infrastructure.

UltraTech Cement

Anhui Conch Cement

CRH plc

Votorantim Cimentos

Taiheiyo Cement

Buzzi Unicem

China National Building Material

Shree Cement

Dangote Cement

JSW Cement

Siam Cement Group

Technological advancement in the Coastal-Resistant Cement market focuses on enhancing durability, reducing permeability, and improving environmental performance. Modern marine-grade cement integrates nano-silica and fly ash additives that reduce chloride ion penetration by up to 30%. High-performance blended cement achieves compressive strengths exceeding 55 MPa, suitable for offshore wind foundations and bridge pylons.

Advanced pozzolanic materials decrease heat of hydration by 15%, minimizing microcrack formation in large concrete structures. Corrosion-inhibiting admixtures extend reinforcement lifespan by 20%, reducing long-term maintenance costs. Digital quality control systems utilize real-time monitoring to ensure consistent sulfate resistance levels.

Carbon-reduced clinker substitution technologies lower embodied carbon by 18% while maintaining structural performance benchmarks. Self-healing concrete additives are under pilot testing, demonstrating crack-sealing improvements of up to 40% in saline exposure simulations. AI-driven material optimization models are increasingly used to predict durability outcomes based on regional environmental conditions. These innovations collectively strengthen infrastructure resilience, regulatory compliance, and lifecycle efficiency across coastal construction projects.

In April 2025, Holcim expanded its low-carbon marine cement portfolio by launching advanced sulfate-resistant blends designed for coastal infrastructure, enhancing durability performance while reducing clinker content in large-scale marine projects. Source: www.holcim.com

In November 2024, CEMEX introduced a new high-durability cement solution engineered for aggressive marine environments, supporting long-life coastal infrastructure and port construction. Source: www.cemex.com

In March 2025, Heidelberg Materials announced capacity upgrades at select plants to increase production of specialized blended cement suitable for marine and offshore construction projects. Source: www.heidelbergmaterials.com

In August 2024, UltraTech Cement enhanced its corrosion-resistant cement product line to address growing demand from coastal bridge and harbor modernization initiatives. Source: www.ultratechcement.com

The Coastal-Resistant Cement Market Report provides comprehensive coverage of marine-grade cement technologies, sulfate-resistant blends, pozzolanic formulations, and corrosion-inhibiting specialty products. The scope includes detailed analysis of application segments such as ports, seawalls, bridges, coastal residential developments, offshore energy foundations, and desalination plants.

Geographic coverage spans Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with country-level insights on coastline infrastructure investments and marine construction volumes. The report evaluates more than 55 active cement manufacturers, examining production capacity, plant modernization initiatives, and additive integration technologies.

Quantitative metrics include compressive strength benchmarks exceeding 50 MPa, chloride penetration resistance improvements of 25%–30%, clinker substitution ratios, and project lifecycle projections surpassing 40 years. The analysis also addresses carbon-reduction strategies, renewable energy integration in cement production, and digital durability monitoring adoption. Emerging niche segments such as nano-enhanced marine cement and self-healing concrete systems are evaluated to support strategic planning for infrastructure developers, contractors, and policy stakeholders within the Coastal-Resistant Cement market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5,082.4 Million |

|

Market Revenue in 2033 |

USD 8,863.9 Million |

|

CAGR (2026 - 2033) |

7.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

LafargeHolcim, CEMEX, Heidelberg Materials, UltraTech Cement, Anhui Conch Cement, CRH plc, Votorantim Cimentos, Taiheiyo Cement, Buzzi Unicem, China National Building Material, Shree Cement, Dangote Cement, JSW Cement, Siam Cement Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |