Reports

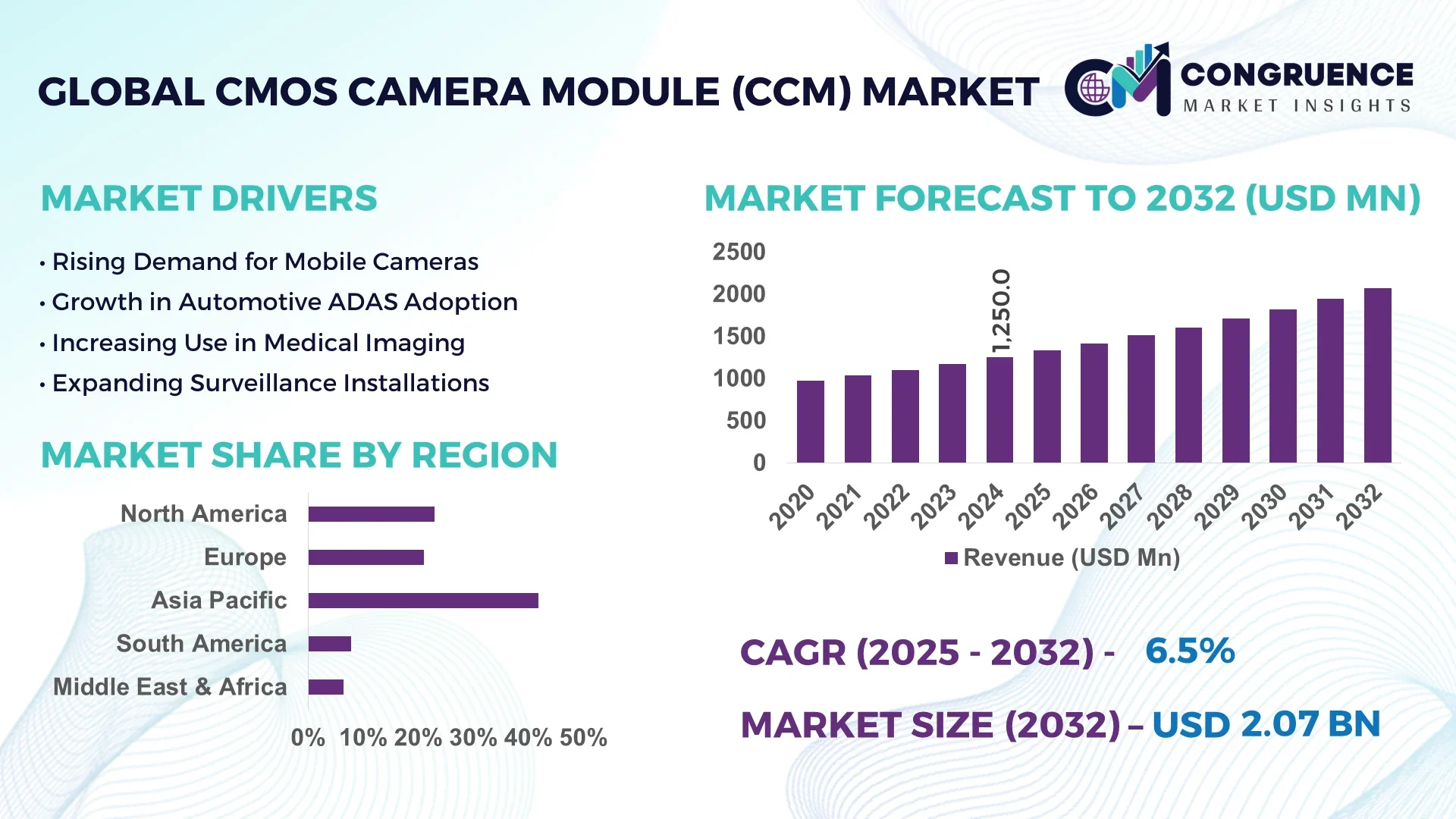

The Global CMOS Camera Module (CCM) Market was valued at USD 1,250.0 Million in 2024 and is anticipated to reach a value of USD 2,068.7 Million by 2032 expanding at a CAGR of 6.5% between 2025 and 2032.

China leads the CMOS Camera Module (CCM) Market with unparalleled production capacity, operating over 200 automated fabrication lines dedicated to high-volume module assembly. The country has attracted over USD 1.2 billion in investment across its top five semiconductor clusters since 2023, enabling continuous innovation in sensor miniaturization. Chinese manufacturers are focusing on advanced automotive-grade modules, expanding testing facilities for ADAS applications, and have introduced 8-megapixel modules optimized for machine vision in industrial automation.

The CMOS Camera Module (CCM) Market spans critical industry sectors including consumer electronics, automotive, security & surveillance, healthcare, and industrial automation. Consumer electronics, primarily smartphones and tablets, contribute approximately 40% to unit shipments, while automotive applications—driven by ADAS and cabin monitoring—account for nearly 25%. Recent innovations include wafer-level optics integration, BSI sensor architecture, and hybrid autofocus combining voice coil and piezo actuators, all enhancing low-light and high-speed imaging. Regulatory drivers include the EU’s upcoming REACH restrictions on certain photoresist chemicals, prompting shifts to greener alternatives. Environmental concerns are influencing module packaging: low-waste substrates and halogen-free flex cables are being adopted. Regional consumption patterns show North America and Europe favoring automotive modules, whereas Asia Pacific remains dominated by mobile-grade CCMs. Emerging trends include embedded edge-AI processing within modules, sensor fusion with LiDAR for ADAS, and multi-spectral imaging for agriculture. Looking ahead, the market is expected to pivot toward vertically integrated optical modules and smart camera wafers, positioning manufacturers to supply turnkey intelligent vision solutions.

AI is rapidly revolutionizing the CMOS Camera Module (CCM) Market by embedding intelligent capabilities directly within imaging hardware, enabling real-time processing and higher operational efficiency. Today’s smart CCMs integrate on-chip neural processing units (NPUs) that can execute AI inference at the sensor level, reducing latency by up to 80% compared to traditional off-chip analytics. This distributed intelligence enables modules to perform scene recognition, anomaly detection, and adaptive exposure control without external compute resources.

Decision-makers in security and automotive markets appreciate that AI-enabled CCMs support edge-based threat detection and ADAS enhancements such as pedestrian recognition and lane-change assistance. OEMs report that modules equipped with embedded AI consume 30–40% less power during continuous monitoring versus legacy CCM systems, extending battery life in drones and IoT devices. Manufacturers also leverage federated learning to update camera performance across large fleets, improving accuracy over time while preserving data privacy. In terms of operational performance, AI-enhanced CCMs can triage image frames in real time, reducing wasted bandwidth by flagging only relevant footage or triggering conditional recording.

Beyond hardware, AI advancements in design automation are transforming production workflows. Computer vision–driven quality control tools inspect each wafer and module, improving defect detection rates by 15%, slashing scrap rates and elevating overall yield. In supply chain logistics, AI forecasting systems anticipate demand spikes for specific CCM variants, enabling just-in-time production and reducing inventory costs by over 20%. The CMOS Camera Module (CCM) Market is thus becoming increasingly intelligence-driven—boosting efficiency, reducing power consumption, elevating performance, and optimizing production through AI’s pervasive influence.

“In 2024, a semiconductor firm introduced a CMOS Camera Module with a 2 TOPS onboard neural processor, enabling real-time people counting at 60 fps and reducing latency from 25 ms to under 5 ms in smart city deployments.”

The CMOS Camera Module (CCM) Market dynamics reflect a highly competitive landscape, fueled by rapid technological innovation and evolving end‑user demand. Leading trends include integration of multifunctional modules combining imaging, LiDAR, and IR sensing. Suppliers are investing heavily in miniaturized, wafer-level lens stacks to serve compact mobile and wearable markets. Cross-sector applications—spanning telehealth, robotics, drones, and automotive—drive diversified demand. Manufacturers are negotiating strategic partnerships to co-develop modules tailored for specific platforms, such as vision-guided robots and driver monitoring systems. Additionally, the market is influenced by standardization efforts in interface protocols like MIPI CSI‑3 and GMSL 2+, enabling high-speed data transfer. Supply chain consolidation continues: larger players secure silicon and glass substrates to protect margins. Regulatory changes such as halogen restrictions in electronics packaging are prompting supply-chain shifts. Overall, the CMOS Camera Module (CCM) Market is maturing, with convergence toward smart, multifunctional imaging solutions enabling embedded AI and connectivity.

Automotive-grade CMOS Camera Module (CCM) Market growth is being significantly driven by rising adoption of advanced driver assistance systems (ADAS) and autonomous vehicle technologies. In 2024, the number of cameras per vehicle increased from an average of 3 to 5 units, reflecting higher demand for wide-angle, high-resolution modules. OEMs are deploying stereo and front-facing CCMs for lane-keeping, automatic parking, and traffic sign recognition systems. Investments by global car manufacturers have funded new automotive testing lines, enhancing production throughput. As a result, the CCM industry is focusing on automotive-grade sensor validation, functional safety certifications, and in‑sensor HDR imaging to meet stringent operational requirements for road safety applications.

The CMOS Camera Module (CCM) Market is challenged by supply-side constraints, particularly shortages in specialized glass lenses and filter coatings. In early 2025, lead times for autofocus lens assemblies extended to 26 weeks, up from 12 weeks in 2022. Long procurement cycles impede manufacturers’ ability to scale or switch production models rapidly. In addition, price inflation in rare-earth materials used in motorized actuators has increased module costs by approximately 8% year-over-year. These disruptions slow time-to-market and limit responsiveness to fluctuating consumer electronics cycles, negatively impacting tier‑2 and tier‑3 CCM suppliers.

The industrial automation segment presents a strong opportunity for the CMOS Camera Module (CCM) Market, especially through the integration of 3D stereo and structured-light modules. In 2024, global demand for 3D vision systems in logistics, warehousing, and robotics increased by 22%, driven by automated picking and palletizing systems. CCM manufacturers are beginning to bundle 3D depth sensors with conventional imaging modules, enabling simultaneous color and depth sensing. Factories retrofitting robotic arms for complex assembly tasks are ordering 3D CCM kits at volumes ~2x higher than standard 2D modules. This shift creates room for modular 3D camera solutions tailored to discrete automation use cases.

Manufacturers in the CMOS Camera Module (CCM) Market face escalating costs related to certification and compliance. In 2024, expenses for AEC‑Q104 automotive-grade module certification and sensor shock/vibration testing increased by 30%, totaling over USD 150,000 per module variant. Additionally, compliance with EMI/EMC standards in industrial and consumer applications demands new test lab investments. Smaller CCM firms struggle to absorb these overheads, which often force consolidation or OEM partnership alternatives. These regulatory and certification pressures slow product development cycles and raise barriers for new market entrants.

Expansion of Embedded Edge-AI Imaging: Manufacturers are embedding neural acceleration within CCMs, enabling camera modules to execute real-time analytics such as facial recognition and object detection at the sensor edge. In 2024, deployment of AI-enabled CCMs increased by 45% in smart surveillance installations, significantly reducing backend processing loads and network bandwidth usage.

Shift to Wafer-Level Optics (WLO) Solutions: Companies are adopting wafer-level optics to reduce module size and improve alignment precision. In 2024, WLO-based CCMs constituted over 30% of smartphone camera modules, lowering assembly complexity and cutting per-unit lens stacking time by 25%.

Multi-Spectral CCM Adoption in Agriculture and Healthcare: There is growing use of multi-spectral CMOS Camera Module (CCM) Market variants incorporating NIR, red-edge, and thermal bands. Key agricultural drone OEMs report multi-spectral CCMs account for 18% of their camera volume, enabling plant health sensing and disease detection in real time.

Standardization of High-Speed Interfaces: Adoption of MIPI CSI‑3 and Serializer/Deserializer standards is accelerating, particularly in automotive and industrial sectors. In 2024, module shipments featuring 12 Gbps CSI‑3 interfaces grew by over 60%, supporting higher-resolution imaging and faster frame rates required for autonomous systems.

The CMOS Camera Module (CCM) Market exhibits a highly structured segmentation, primarily divided by type, application, and end-user domains. The segmentation reflects technological advancements, varied industry needs, and evolving end-user expectations across verticals. By type, the market is classified into modules with differing sensor resolutions, autofocus mechanisms, and mounting formats—each catering to specific device form factors and performance requirements. Application-based segmentation spans mobile devices, automotive systems, security & surveillance, healthcare, and industrial automation. Among end-users, demand varies widely from consumer electronics manufacturers to automotive OEMs and smart infrastructure integrators. Each segment presents unique adoption drivers—ranging from miniaturization demands in smartphones to image accuracy in robotics. With the rapid pace of innovation and integration of AI capabilities, segmentation continues to evolve, influencing product design, packaging, and use-case specific feature development. This segmentation analysis helps stakeholders identify high-potential niches and tailor strategic priorities based on emerging consumption patterns and operational requirements.

The CMOS Camera Module (CCM) Market includes various product types such as fixed-focus modules, autofocus modules, zoom modules, and 3D sensing modules. Among these, autofocus camera modules hold the dominant position due to their widespread adoption in smartphones, tablets, and automotive systems where clarity and adaptability are essential. These modules are favored for their ability to dynamically adjust focal length, providing superior image sharpness in varying conditions, especially in motion-heavy scenarios like driving or video calling.

The fastest-growing type is the 3D sensing module, driven by increased demand in facial recognition, gesture-based control systems, and depth-mapping applications, especially in AR/VR headsets and autonomous robotics. These modules leverage technologies such as structured light and time-of-flight sensors, enhancing spatial recognition accuracy.

Fixed-focus modules continue to serve low-cost and compact devices such as entry-level mobile phones, smart home sensors, and wearables, offering simplicity and cost efficiency. Zoom modules, though more niche, are increasingly adopted in high-end surveillance and inspection equipment where long-range visibility and detail resolution are critical. This diverse type segmentation reflects tailored product strategies based on performance, application precision, and form factor constraints.

The CMOS Camera Module (CCM) Market spans multiple application domains, each with distinct performance and integration needs. Mobile and consumer electronics remain the largest application area, driven by the ubiquity of smartphones, tablets, and laptops that demand high-resolution imaging, low-light optimization, and compact form factors. Smartphone manufacturers, in particular, deploy multi-lens camera arrays featuring wide-angle, telephoto, and macro modules to elevate user experience.

The automotive sector is currently the fastest-growing application, propelled by the integration of advanced driver assistance systems (ADAS), rear-view and surround-view systems, and in-cabin monitoring. Automotive-grade CCMs are engineered for thermal stability, high dynamic range, and real-time processing—key features for road safety and automation.

Other applications include security and surveillance, where night-vision optimized modules and AI-enhanced face/object detection are transforming urban safety systems. In healthcare, CCMs are used in endoscopy, diagnostics, and patient monitoring equipment. Industrial automation utilizes these modules for machine vision and defect detection tasks. Each application segment drives specific innovation cycles, ensuring continuous evolution and diversification in module design.

End-user segmentation in the CMOS Camera Module (CCM) Market highlights varied adoption levels across industry verticals. The consumer electronics industry remains the leading end-user, with continuous demand from mobile phone and laptop manufacturers for compact, high-performance camera modules. The shift toward multi-camera configurations, AI-based image processing, and ultra-slim form factors keeps this segment at the forefront of volume consumption.

The automotive sector is emerging as the fastest-growing end-user, spurred by rising integration of vision-based safety systems, interior monitoring, and autonomous driving features. OEMs and Tier-1 suppliers are deploying a growing number of camera modules per vehicle, leading to significant order volumes and customization needs.

Healthcare and medical device manufacturers are also notable contributors, integrating high-resolution and miniaturized modules into diagnostic and surgical imaging systems. Industrial end-users increasingly leverage CCMs for inspection, robotics, and automation processes. Smart infrastructure developers, especially in smart cities and transport, are adopting intelligent camera modules for surveillance and traffic management. This multifaceted demand profile underscores the market's adaptability to diverse end-user innovations and operational challenges.

Asia-Pacific accounted for the largest market share at 41.8% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

The Asia-Pacific region leads the CMOS Camera Module (CCM) Market due to its dominant electronics manufacturing infrastructure, high smartphone penetration, and significant automotive component exports. Countries like China, South Korea, and Japan host extensive fabrication and assembly facilities for camera modules, benefiting from integrated supply chains and R&D clusters. In contrast, North America is poised for rapid growth due to increasing adoption of ADAS technologies, AI-based surveillance systems, and robust medical imaging demands. Government-backed investments in smart infrastructure and industrial automation are further accelerating the adoption of intelligent CCMs across sectors. Additionally, regional preferences for edge-AI solutions and advanced camera architectures are fostering innovation and localization of production in North American markets. The contrasting growth dynamics of these regions underline the global diversification and tailored strategies shaping the CMOS Camera Module (CCM) Market landscape.

North America held 22.6% of the global CMOS Camera Module (CCM) Market in 2024, driven by strong adoption across the automotive, security, and industrial automation sectors. The U.S. and Canada are key contributors, with major automotive OEMs integrating multiple camera modules into vehicles for driver assistance and monitoring. Advanced surveillance systems, especially in government and commercial infrastructure, are boosting regional demand for intelligent imaging modules. Regulatory reforms such as the expansion of vehicle safety mandates and data privacy regulations are influencing product specifications. Technological progress includes AI-optimized modules and onboard neural processors that facilitate edge analytics. Additionally, federal support for semiconductor manufacturing through initiatives like CHIPS Act funding is catalyzing domestic production of core imaging components, fostering self-reliance and innovation in the regional market.

Europe accounted for 18.3% of the CMOS Camera Module (CCM) Market in 2024, with Germany, the UK, and France representing the primary hubs. The continent’s leadership in automotive innovation, particularly in ADAS and autonomous driving systems, fuels demand for high-resolution and thermally resilient CCMs. Regulatory frameworks from the European Commission, including enhanced automotive safety protocols and sustainability benchmarks, are pushing manufacturers toward energy-efficient, low-emission modules. Europe's industrial sector is increasingly adopting machine-vision CCMs for factory automation and quality inspection. The integration of AI, IoT, and robotics into manufacturing workflows has led to a rise in demand for camera modules with real-time image processing capabilities. Digital transformation across logistics and healthcare further complements the expanding application base of CCMs in Europe.

Asia-Pacific dominated the CMOS Camera Module (CCM) Market with 41.8% share in 2024, supported by top-consuming countries such as China, India, Japan, and South Korea. China continues to lead in camera module manufacturing and exports, with high-volume smartphone production driving substantial demand. Japan contributes heavily through automotive-grade module innovations, while South Korea’s electronics giants push high-performance sensor R&D. India is rapidly emerging as a secondary manufacturing hub due to its favorable policies under Make-in-India and electronics production-linked incentive (PLI) schemes. Regional trends include smart city deployments, AI surveillance systems, and mobile camera advancements. Innovation hubs in Shenzhen, Tokyo, and Seoul are continuously advancing wafer-level packaging, 3D imaging, and neural-integrated CCM designs. The dense tech ecosystem and vertically integrated manufacturing chains position Asia-Pacific as the global innovation and supply core for the CCM industry.

South America contributed approximately 6.1% to the CMOS Camera Module (CCM) Market in 2024, with Brazil and Argentina emerging as the primary markets. The region is experiencing a growing shift toward smart surveillance, traffic management systems, and industrial automation that leverage intelligent imaging. Brazil's expanding automotive industry is incorporating CCMs into mid-range and premium vehicles for driver assistance and reverse parking features. Infrastructure upgrades in urban centers are driving the deployment of CCTV and AI-vision systems, supported by municipal and national safety initiatives. Trade policies promoting electronic component assembly and reduced import tariffs have also supported regional distribution and integration. Government efforts to digitize public spaces and utility infrastructure further enhance CCM adoption across various sectors.

The Middle East & Africa region accounted for 4.7% of the CMOS Camera Module (CCM) Market in 2024. Demand is largely driven by growth in sectors like construction, energy, and public safety. The UAE and South Africa are key contributors, leveraging camera modules in surveillance systems across commercial complexes, oil refineries, and urban infrastructure. Adoption of thermal and night-vision CCMs is increasing in the security sector to handle extreme environmental conditions. Governments are investing in smart city development projects that integrate AI-powered camera systems for traffic control and population management. Additionally, construction firms are implementing machine-vision modules for monitoring remote job sites. Trade partnerships and relaxed import regulations are enabling greater accessibility of advanced imaging components in the region. Continued modernization and the shift to intelligent infrastructure are setting a foundation for long-term CCM demand in this market.

China – 28.4% Market Share

High production capacity and extensive consumer electronics manufacturing ecosystem make China the leading country in the CMOS Camera Module (CCM) Market.

United States – 19.5% Market Share

Strong end-user demand across automotive, surveillance, and healthcare sectors supports the U.S. leadership position in the global CMOS Camera Module (CCM) Market.

The CMOS Camera Module (CCM) Market is highly competitive, featuring over 60 active global and regional players offering differentiated products to meet evolving end-use requirements. Market leaders maintain their dominance through consistent investment in R&D, with a focus on miniaturization, AI-enabled imaging, and multi-lens integration. Key players are strategically positioned through strong alliances with smartphone manufacturers, automotive OEMs, and surveillance solution providers. In recent years, strategic initiatives such as vertical integration, cross-sector partnerships, and product launches featuring enhanced resolution and low-light performance have intensified market competition.

Mergers and acquisitions remain a common approach to gaining technological advantages and expanding geographic presence. For instance, companies are acquiring sensor or lens specialists to streamline in-house capabilities. Additionally, Asian manufacturers are expanding capacity and moving up the value chain with proprietary module designs. Innovation is driving segmentation within the market—companies are introducing thermal, 3D, and time-of-flight (ToF) sensors tailored to industrial, medical, and automotive use. Competitive intensity is further fueled by the entry of startups focused on edge AI and imaging analytics. The global nature of supply chains, IP competitiveness, and regulatory compliance also continue to shape the strategic landscape.

LG Innotek Co., Ltd.

OFILM Group Co., Ltd.

Sunny Optical Technology (Group) Co., Ltd.

Samsung Electro-Mechanics Co., Ltd.

Hon Hai Precision Industry Co., Ltd. (Foxconn)

Luxvisions Innovation Limited

Chicony Electronics Co., Ltd.

Q Technology Group Company Limited

Cowell E Holdings Inc.

Truly Opto-electronics Ltd.

STMicroelectronics N.V.

ON Semiconductor Corporation

Himax Technologies, Inc.

Omnivision Technologies, Inc.

Technological advancements are reshaping the CMOS Camera Module (CCM) Market, with a strong emphasis on compactness, low power consumption, and intelligent imaging capabilities. Manufacturers are integrating AI-powered image processing directly within modules to enable edge computing for real-time analysis, benefiting applications in automotive safety, surveillance, and medical diagnostics.

Multi-camera arrays and periscope-style lens systems are being adopted extensively in smartphones to enhance optical zoom and wide-angle functionality without increasing device thickness. Innovations such as Backside Illuminated (BSI) sensors and Stacked CMOS architectures are enabling better light sensitivity and faster frame rates, making them suitable for low-light environments and high-speed video capture.

In the automotive segment, global shutter sensors and time-of-flight (ToF) technology are gaining momentum, facilitating accurate object detection and 3D depth mapping for ADAS and autonomous driving systems. Meanwhile, wafer-level packaging (WLP) and chip-on-board (COB) assembly techniques are streamlining module integration and reducing costs across mass-market products.

The medical industry is also adopting ultra-miniature modules with 4K resolution and sterilizable optics for endoscopy and diagnostic imaging. Additionally, thermal imaging and multi-spectral modules are emerging in industrial and defense sectors, addressing unique imaging needs. As demand for real-time visual intelligence grows, the CCM market continues to be shaped by a wave of application-specific and performance-driven innovations.

• In January 2024, LG Innotek unveiled a folded zoom camera module for smartphones featuring 4x to 9x optical zoom with no image degradation. The innovation leverages a telescopic design to maintain device slimness while enhancing zoom performance.

• In March 2024, Sunny Optical Technology expanded its Vietnam-based production facility, aiming to increase monthly output of CCMs by 20% to meet rising demand from Southeast Asian smartphone manufacturers.

• In August 2023, Omnivision launched the OX08D10, an 8MP CMOS sensor designed for automotive applications, integrating AI-optimized HDR imaging and cybersecurity features compliant with new ISO standards.

• In December 2023, Samsung Electro-Mechanics introduced a high-resolution 200MP camera module for premium mobile devices, incorporating AI image signal processing and adaptive HDR support for improved image clarity.

The CMOS Camera Module (CCM) Market Report provides a comprehensive analysis of key industry dynamics, covering the full spectrum of technologies, applications, and regions influencing market behavior. The report evaluates the market across major segments, including Type (such as autofocus, fixed-focus, and zoom modules), Application (smartphones, automotive, surveillance, industrial, medical), and End-User (consumer electronics, healthcare, automotive, manufacturing, and aerospace).

Geographically, the report assesses market trends and competitive dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering deep insights into regional drivers and growth patterns. It also highlights emerging economies where infrastructure development, mobile adoption, and industrial digitization are fueling new demand.

The technology section emphasizes the impact of AI-enabled imaging, 3D vision, miniaturized optics, and advanced packaging techniques, as well as the growing relevance of ToF, thermal, and multispectral modules in niche applications. Additionally, the report considers supply chain trends, geopolitical impacts, and regulatory frameworks affecting manufacturing and deployment.

With a focus on innovation, strategic developments, and market maturity across use cases, the report serves as a vital resource for decision-makers, investors, and industry stakeholders aiming to understand current opportunities and future directions in the global CMOS Camera Module (CCM) Market.CMOS Camera Module (CCM) Market Report Summary

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 1,250 Million |

| Market Revenue (2032) | USD 2,068.7 Million |

| CAGR (2025–2032) | 6.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | LG Innotek Co., Ltd., OFILM Group Co., Ltd., Sunny Optical Technology (Group) Co., Ltd., Samsung Electro-Mechanics Co., Ltd., Hon Hai Precision Industry Co., Ltd. (Foxconn), Luxvisions Innovation Limited, Chicony Electronics Co., Ltd., Q Technology Group Company Limited, Cowell E Holdings Inc., Truly Opto-electronics Ltd., STMicroelectronics N.V., ON Semiconductor Corporation, Himax Technologies, Inc., Omnivision Technologies, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |