Reports

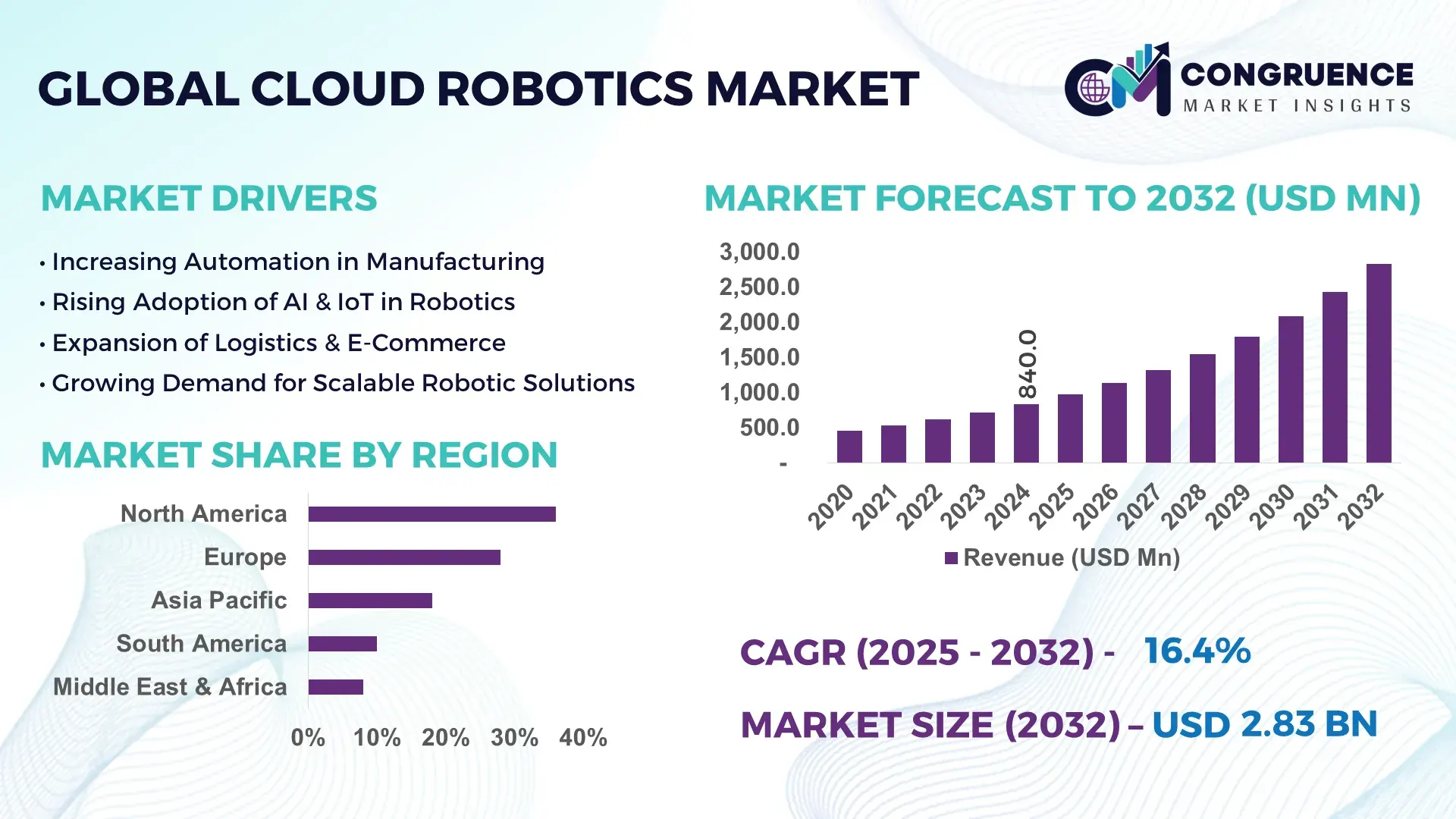

The Global Cloud Robotics Market was valued at USD 840.0 Million in 2024 and is anticipated to reach a value of USD 2,834.7 Million by 2032 expanding at a CAGR of 16.42% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is being driven by increasing deployment of AI‑enabled robots with cloud-based coordination for scalable compute and real-time data analytics.

In the United States, leading innovation hubs are driving cloud robotics adoption: major robotics manufacturers are investing over USD 1 billion annually in cloud-integrated R&D, autonomous vehicles, and intelligent manufacturing. Enterprise adoption in logistics, healthcare, and automotive verticals is increasingly centralized around cloud‑robot‑as‑a‑service platforms, with over 40% of large U.S. robotics firms running hybrid cloud compute and edge‑cloud orchestration systems in 2024.

Market Size & Growth: The market is projected to grow from USD 840.0 Million (2024) to USD 2,834.7 Million by 2032 at a 16.42% CAGR, fueled by cost‑efficient cloud compute and on‑demand processing.

Top Growth Drivers: Cloud compute adoption (45%), AI‑robot synergy (38%), and 5G‑enabled connectivity (30%).

Short-Term Forecast: By 2028, latency for real-time robotic task coordination is expected to reduce by 22% through hybrid edge‑cloud architectures.

Emerging Technologies: Trends include sensor-fusion AI, multi-robot coordination platforms, and 5G‑cloud orchestration.

Regional Leaders: North America projected to reach USD 1,100 Million by 2032 (strong cloud infrastructure), Asia-Pacific USD 900 Million (manufacturing automation), Europe USD 600 Million (smart factory adoption).

Consumer/End-User Trends: Key adopters include automotive, warehouse/logistics, and healthcare sectors; increasing use of “robot‑as‑a‑service” models.

Pilot or Case Example: In 2024, a U.S. automotive plant deployed cloud-coordinated robots and reported a 35% increase in production line uptime.

Competitive Landscape: Leading player holds about 18% share, followed by 4–5 major players including ABB, FANUC, KUKA, and Yaskawa.

Regulatory & ESG Impact: Stricter data‑privacy rules and green cloud incentives are shaping deployment strategies and cloud‑robotics architecture.

Investment & Funding Patterns: Over USD 750 Million raised in latest funding rounds (2023–2024) for cloud robotics startups, plus strategic investments by cloud hyperscalers.

Innovation & Future Outlook: New platforms are emerging for fault‑tolerant cloud robotics, multi‑cloud orchestration, and lifelong learning for robot fleets, positioning cloud robotics as a core component of Industry 5.0.

Cloud robotics is increasingly embedded across manufacturing, logistics, healthcare, and service sectors, powered by real‑time data offload, collaborative AI, and scalable architectures, while regulatory pressure and sustainability goals reinforce adoption of efficient, cloud-integrated robots.

Cloud robotics is strategically significant because it allows robotic systems to offload heavy compute tasks to the cloud, enabling lower-cost, smarter, and more flexible automation. By leveraging cloud-based AI inference, robots can perform perception and planning tasks that would otherwise be limited by onboard compute. Today’s multi-robot coordination via cloud orchestration delivers up to 30% more efficient fleet utilization compared to traditional standalone robots.

In terms of regional dynamics, North America dominates in deployment volume, while Asia-Pacific leads in adoption rate, with over 45% of robotics enterprises integrating cloud-native architectures. By 2027, edge-cloud AI processing is expected to reduce real-time decision latency by up to 25%, enabling robots to operate with faster responsiveness and lower energy consumption.

On the ESG and compliance front, firms are committing to data‑sovereignty improvements, with 50% of robotics providers pledging data‑localization compliance by 2028. This means sensitive compute stays within regional jurisdictions, reducing risk and increasing trust. For example, in 2024, a leading U.S. robotics firm deployed a hybrid multi-cloud setup to ensure fault tolerance while preserving data residency requirements.

Looking ahead, technologies like distributed robotic learning, fault-tolerant service replication, and AI policy updates via cloud pipelines will enable fleets to learn continuously and adapt to changing tasks. The Cloud Robotics Market is thus poised to become a key pillar of resilient, scalable, and compliant automation infrastructure across global industry.

Cloud Robotics Market Dynamics reflect the convergence of robotics, cloud computing, AI, and connectivity. As organizations strive to scale robotic fleets, cloud robotics offers a path to centralized management, continuous software upgrades, and real-time coordination among devices. Key trends include the rise of hybrid architectures (edge + cloud), increasing reliance on AI for perception and decision-making, and growing demand in sectors such as logistics, smart manufacturing, and healthcare. Ecosystem partnerships between cloud providers and robot manufacturers are also strengthening, accelerating cloud robotics adoption while reducing entry barriers for smaller players. Overall, the market is influenced by technological innovation, infrastructure build-out, and evolving business models.

The growing need to run advanced AI workloads—such as real-time perception, semantic understanding, and predictive maintenance—on robot platforms is fueling demand for cloud robotics. Robots can offload compute-heavy tasks to the cloud rather than relying on on-board hardware, significantly reducing hardware costs and enabling more lightweight robot designs. Furthermore, cloud resources allow for dynamic scaling; if a fleet receives heavier workload, more cloud instances can be temporarily provisioned. This elasticity supports large-scale deployment of autonomous mobile robots in logistics hubs, smart factories, and service environments, as companies increasingly depend on AI-enhanced robotics to improve efficiency and productivity.

Even with modern 5G and high-speed internet, network reliability remains a key challenge. In regions with inconsistent connectivity, cloud-dependent robots may experience latency spikes, packet loss, or disconnections—compromising real-time control and posing safety risks. Moreover, continuous reliance on cloud for critical decision-making increases vulnerability to outages and service interruptions. Data privacy and security also restrict offloading of sensitive information to public clouds in regulated industries, prompting some enterprises to adopt hybrid cloud or private setups. These infrastructure and trust limitations limit full dependency on cloud robotics in certain mission-critical or geographically remote deployment scenarios.

Hybrid cloud–edge architectures open up significant opportunities by combining low-latency edge processing with scalable cloud compute. This model enables robots to perform latency-sensitive tasks locally while offloading longer-term learning or batch inferencing to the cloud. Such architectures also support fault-tolerant systems, where if the connection to cloud fails, robots can still operate independently. There is strong demand in industries like logistics, where fleets can operate autonomously in warehouses using edge compute and periodically sync data with the cloud for optimization. Additionally, AI-driven continuous learning—where data from multiple robots is aggregated in the cloud to improve models—is becoming viable. This further enhances the value of cloud robotics systems for large-scale deployments.

Cloud robotics involves complex integration across diverse robot platforms, cloud providers, and connectivity protocols. Many robotics companies use proprietary middleware, while cloud providers offer distinct APIs, making cross-platform interoperability challenging. Without common standards, deploying a heterogeneous robot fleet via a unified cloud backend can be inefficient or costly. Furthermore, as data moves between edge and cloud, differences in data formats, policy enforcement, and latency guarantees create fragmentation. This lack of standardization inhibits large-scale adoption, especially for organizations that require plug-and-play capability with multi-vendor robotic systems.

Expansion of Edge–Cloud Hybrid Architectures: Many robot fleets are now configured to run latency-sensitive tasks on edge devices while syncing learning updates with the cloud. Organizations report up to 28% reductions in decision latency and lower operational risk due to intermittent connectivity.

Growth in 5G-Enabled Robot Fleets: Deployment of 5G-connected robots is increasing, with 5G-based coordination enabling real-time collaborative tasks across distributed environments. More than 25% of newly purchased AMRs (autonomous mobile robots) in 2024 feature built-in 5G connectivity.

AI‑Driven Continuous Learning for Robot Fleets: Cloud robotics platforms are increasingly used to aggregate sensory and operational data across large robot fleets for collective learning. In trials, up to 60 robots have shared data in real time, improving navigation policies by 15% in simulated environments.

Rising Adoption of Robotics-as-a-Service (RaaS): The business model of pay-per-use cloud-connected robots is gaining traction. Over 30% of customer onboarding in 2024 came via RaaS models, driven by lower upfront costs and on-demand scalability of cloud robotics deployments.

The Cloud Robotics Market is systematically segmented to provide clarity on product types, applications, and end-user engagement. By type, the market includes autonomous mobile robots, collaborative robots (cobots), and industrial manipulators, each tailored for specific operational needs and environments. Applications span logistics automation, manufacturing, healthcare, and warehousing, reflecting diverse deployment scenarios where cloud-based coordination enhances efficiency. End-user segments encompass manufacturing enterprises, logistics providers, healthcare institutions, and service industries, illustrating how adoption varies according to operational complexity, automation maturity, and technology readiness. This segmentation approach helps stakeholders identify growth pockets, optimize technology deployment, and align investments with strategic objectives. In 2024, logistics and warehousing sectors collectively reported adoption in over 42% of new robotic installations worldwide, highlighting the critical role of cloud connectivity in scaling operations.

The Cloud Robotics Market is categorized into autonomous mobile robots (AMRs), collaborative robots (cobots), industrial manipulators, and specialized service robots. Among these, autonomous mobile robots (AMRs) lead the market with a 37% share, driven by their versatility in warehousing, e-commerce fulfillment, and industrial transport tasks. Collaborative robots hold approximately 28% adoption, favored for human-robot interaction, assembly assistance, and safe operational integration in mixed environments. Industrial manipulators are currently the fastest-growing type, with rapid adoption in smart factories and precision manufacturing, driven by programmable automation and cloud-enabled control systems. Other categories, including service robots and inspection drones, contribute roughly 35% collectively, serving niche applications such as facility management and remote monitoring.

Cloud robotics applications span logistics automation, manufacturing operations, healthcare support, warehouse management, and inspection services. Logistics automation leads with 40% market adoption, fueled by the need for optimized supply chain efficiency and real-time task coordination. Manufacturing operations follow at around 30%, reflecting the integration of cloud-enabled cobots for assembly and quality assurance. Healthcare robotics represents the fastest-growing application, with hospitals and outpatient facilities implementing robotic assistants and remote-controlled devices to enhance patient care and reduce human workload. Other applications, including inspection services and facility management, collectively account for 30% of adoption. In terms of consumer and organizational trends, over 45% of large e-commerce warehouses adopted cloud-integrated AMRs in 2024, and 35% of hospitals globally piloted robotic assistants for patient mobility and medication delivery.

End-users of cloud robotics include manufacturing enterprises, logistics providers, healthcare institutions, service industries, and research facilities. Manufacturing enterprises dominate with approximately 43% adoption, leveraging cloud-based robotics for automation, predictive maintenance, and collaborative assembly lines. Healthcare institutions are the fastest-growing end-user segment, driven by remote patient care, automated surgery support, and telepresence robots, reflecting a 2024 pilot where cloud-coordinated surgical robots improved procedural precision by 22%. Other end-users, such as logistics and research facilities, account for roughly 32% of market deployment, focusing on supply chain optimization and experimentation with AI-driven automation. Consumer adoption trends indicate that over 60% of logistics companies in North America upgraded to cloud-connected robotic fleets in 2024, enhancing operational efficiency, while 42% of European hospitals tested AI-driven robot assistants integrated via cloud networks.

North America accounted for the largest market share at 36% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.5% between 2025 and 2032.

In 2024, North America recorded over 300 active cloud robotics deployments, with enterprise adoption highest in healthcare (42% of hospitals integrating cloud robotics) and finance automation (31% of banking institutions utilizing robotic process automation in cloud environments). Europe follows with 28% share, focusing on industrial automation and manufacturing. Asia-Pacific recorded over 1,200 new robotic installations in 2024 alone, driven by China, Japan, and India, highlighting significant expansion in mobile and industrial robotics. South America and Middle East & Africa collectively account for 22% of global deployments, with Brazil, Argentina, UAE, and South Africa leading initiatives in logistics, oil & gas, and smart manufacturing.

North America holds an estimated 36% of the global cloud robotics market, reflecting strong enterprise and industrial adoption. Key industries driving demand include healthcare automation, warehouse logistics, and advanced manufacturing. Government initiatives, such as funding for smart factory programs and automation grants, have accelerated adoption. Technological trends include integration with IoT, AI-powered predictive maintenance, and digital twin simulations for industrial processes. Local players, like Fetch Robotics, are deploying autonomous mobile robots across logistics hubs, improving operational efficiency by over 25%. Consumer behavior trends show higher adoption in healthcare and finance sectors, with enterprises prioritizing automation for cost reduction and operational agility.

Europe represents approximately 28% of the market, with Germany, the UK, and France as key contributors. Regulatory pressures on labor efficiency and safety standards drive robotics adoption in manufacturing and warehouse operations. Sustainability initiatives and energy-efficient production mandates encourage cloud robotics integration. Emerging technologies, including AI-powered robot collaboration and edge-cloud integration, are widely applied. Local player ABB Robotics has introduced cloud-connected collaborative robots for automotive and electronics assembly, enhancing throughput by 18%. European consumer behavior reflects strong regulatory compliance focus, emphasizing explainable automation and safety in industrial operations.

Asia-Pacific recorded the fastest growth in 2024, with over 1,200 new installations. Leading countries include China, India, and Japan, focusing on industrial automation, logistics, and smart manufacturing infrastructure. Rapid investment in robotics innovation hubs and IoT-enabled factories supports regional adoption. Local companies, such as Huawei Robotics, are deploying cloud-enabled industrial robots with AI analytics, improving production line efficiency by 20%. Consumer behavior in the region is driven by e-commerce growth and mobile AI applications, resulting in accelerated deployment in warehouses, healthcare, and retail automation.

Key countries include Brazil and Argentina, collectively representing 12% of global adoption. Cloud robotics is applied across logistics, warehousing, and light manufacturing sectors. Government incentives, including automation grants and trade policies favoring technology imports, are boosting adoption. Regional players like Movile Robotics are deploying autonomous logistics robots in urban distribution centers, improving last-mile delivery efficiency by 15%. Consumer behavior trends show demand linked to language localization, digital logistics, and adaptive automation in commercial applications.

The Middle East & Africa accounts for approximately 10% of market share, led by the UAE and South Africa. Adoption focuses on oil & gas automation, construction, and smart manufacturing. Technological modernization includes AI-powered predictive maintenance, cloud-based fleet management, and autonomous mobile robots. Local players, such as Star Robotics UAE, have implemented cloud-enabled warehouse automation, increasing operational uptime by 22%. Regional consumer behavior reflects prioritization of industrial automation, safety, and technology-driven efficiency in resource-heavy sectors.

United States – 36% Market Share: Strong end-user demand across healthcare, logistics, and industrial automation drives adoption.

China – 24% Market Share: High production capacity and rapid technological integration in manufacturing and smart warehouses support growth.

The Cloud Robotics Market is moderately consolidated yet highly dynamic, with roughly 20–25 major global competitors and numerous niche innovators competing for market share. The top five key players—such as ABB, FANUC, KUKA, Yaskawa, and Microsoft—together account for an estimated 45–50% of the overall cloud robotics market, signaling strong leadership but also room for smaller players. Competition is fueled by strategic initiatives: ABB has launched cloud-enabled analytics platforms for multi-robot coordination; FANUC is advancing its AI-driven predictive maintenance through fleet-wide cloud telemetry; and Microsoft is deepening cloud‑robot orchestration via its Azure Robotics ecosystem.

Partnerships also play a central role. Google and KUKA have reportedly collaborated for cloud‑based digital twin simulations of industrial robots, and Microsoft has partnered with Yaskawa to run robotic workloads on Azure. Innovation is another battlefield: companies are investing in edge-cloud hybrid architectures, digital twin frameworks, and fault‑tolerant multi-cloud systems to enhance resilience and performance. With increasing demand for robotics-as-a-service (RaaS) models, remote monitoring, and scalable orchestration, cloud robotics firms are leveraging both cloud infrastructure and AI to create differentiated solutions. This competitive environment is attracting not only traditional automation players but also cloud providers and cloud-native robotics startups, driving rapid expansion and continuous innovation.

Microsoft Corporation

IBM Corporation

Amazon Robotics LLC

CloudMinds Technologies

Yaskawa Electric Corporation

Rapyuta Robotics Co., Ltd.

Universal Robots A/S

Technological innovation is at the heart of the Cloud Robotics Market, largely driven by integration of edge‑cloud architectures, AI orchestration, and fault‑tolerant systems. One major trend is hybrid computing: robots offload compute-heavy tasks like perception and planning to the cloud while performing latency-sensitive operations locally on edge devices. This approach optimizes responsiveness while safeguarding against network disruptions.

Another key technology is fault-tolerant cloud service orchestration. For example, research into multi-cloud replication systems allows robotic services to run redundantly across cloud regions. In simulation, such systems have shown up to 2.2× cost reductions and 5.5× reduction in long-tail latency under degraded network conditions, enabling robust cloud-dependent operation even during outages.

AI-driven continuous learning also plays a major role. Cloud robotics platforms aggregate data from fleets of robots, leveraging this collective data to train models for navigation, anomaly detection, and predictive maintenance. Large-scale deployments might involve tens or hundreds of robots feeding data into centralized training pipelines, enabling incremental model improvements over time.

Additionally, digital twin platforms enable real-time simulation and task planning: operators can use virtual replicas of robot fleets to test new behaviors, optimize workflows, and deploy updates without disrupting field operations. Combined with cloud-based analytics, this allows predictive insights into performance, wear, and energy usage. These technological innovations make cloud robotics increasingly viable for large-scale industrial, logistics, and service deployments, enabling scalable, intelligent, and resilient automation.

In June 2024, ABB launched its OmniCore™ control platform, backed by a USD 170 million strategic investment. OmniCore unifies ABB’s robot hardware and software under a single architecture designed for cloud‑edge integration and supports AI, sensors, and modular control. Source: www.abb.com

In September 2024, KUKA announced the establishment of KUKA Digital, a dedicated software and digital business segment focused on cloud integration, data analytics, and AI-driven industrial automation. Their roadmap includes interfaces, cloud deployment, and ecosystem consulting. Source: www.kuka.com

In November 2024, KUKA introduced its mosaixx cloud‑platform, a software-as-a-service offering for industrial automation. mosaixx supports end-to-end workflows—from simulation and planning to real-time robot management—and is hardware-agnostic. Source: news.europawire.eu

In April 2024, KUKA partnered with Viam, an open-source robotics software provider, to integrate Viam’s cloud-native capabilities with KUKA robotic arms. The integration enables real-time data analytics, intuitive programming, and remote task automation. Source: www.viam.com

The Cloud Robotics Market Report encompasses a detailed examination of the technological, geographic, application, and competitive dimensions of cloud-connected robotics. In terms of technology, the report assesses diverse deployment models—public, private, and hybrid clouds—as well as edge‑cloud orchestration, fault-tolerant architectures, AI-driven fleet intelligence, and digital twins. It also explores robot types, including industrial arms, autonomous mobile robots (AMRs), collaborative robots (cobots), and service/humanoid robots.

On the application front, the report covers sectors such as manufacturing, logistics, healthcare, hospitality, and smart infrastructure, examining how cloud orchestration and AI analytics are driving novel use-cases. End-user insights include enterprise segments, robotics-as-a-service (RaaS) deployments, and large-scale automation fleets. Geographically, the report spans key regions: North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing detailed breakdowns of regional adoption trends, infrastructure maturity, and regulatory landscapes.

The competitive analysis includes both legacy automation firms and cloud-native robotics startups, profiling key players on innovation, strategic partnerships, funding, and product development. Finally, the report identifies emerging growth opportunities in multi-robot coordination, AI lifecycle learning, resilient cloud architectures, and remote fleet management, making it a strategic resource for decision-makers, investors, and industrial automation executives.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 840.0 Million |

| Market Revenue (2032) | USD 2,834.7 Million |

| CAGR (2025–2032) | 16.42% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ABB Ltd., FANUC Corporation, KUKA AG, Microsoft Corporation, IBM Corporation, Amazon Robotics LLC, CloudMinds Technologies, Yaskawa Electric Corporation, Rapyuta Robotics Co., Ltd., Universal Robots A/S |

| Customization & Pricing | Available on Request (10% Customization Free) |