Reports

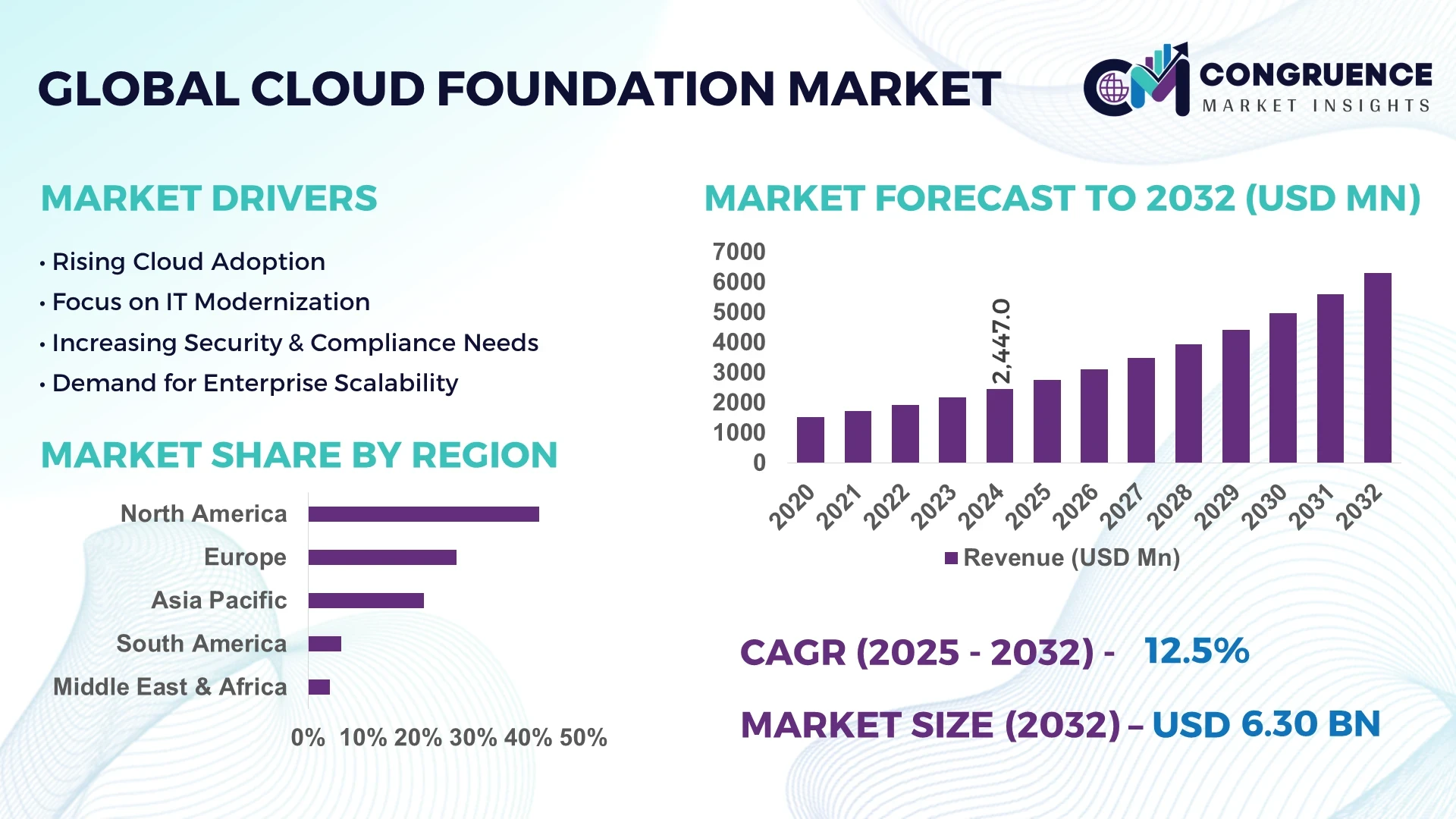

The Global Cloud Foundation Market was valued at USD 2,447.0 Million in 2024 and is anticipated to reach a value of USD 6,296.4 Million by 2032, expanding at a CAGR of 12.54% between 2025 and 2032. This growth is primarily driven by the increasing adoption of hybrid and multi-cloud strategies, demand for scalable IT infrastructure, and the need for streamlined cloud management and automation across enterprises.

The United States stands as a pivotal player in the global Cloud Foundation Market. In 2024, the U.S. cloud foundation market size was evaluated at USD 6.85 billion and is projected to be worth around USD 22.76 billion by 2032, growing at a CAGR of 12.76% from 2025 to 2032. This expansion underscores the nation's commitment to advancing cloud infrastructure and services. The U.S. market is characterized by a robust technological ecosystem, with significant investments in cloud infrastructure and services. Leading cloud service providers, such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP), continue to innovate and expand their offerings, driving the adoption of cloud foundation solutions. Additionally, the U.S. government's initiatives to promote digital transformation across federal agencies have further accelerated the demand for cloud foundation services. The convergence of these factors positions the United States as a central hub for cloud foundation technologies.

Market Size & Growth: The market was valued at USD 2,447.0 million in 2024 and is projected to reach USD 6,296.4 million by 2032, expanding at a CAGR of 12.54%.

Top Growth Drivers: Hybrid cloud adoption (40%), multi-cloud strategies (35%), and demand for scalable IT infrastructure (25%).

Short-Term Forecast: By 2028, cloud foundation solutions are expected to improve operational efficiency by 20%.

Emerging Technologies: Integration of Artificial Intelligence (AI) for predictive analytics, automation in cloud management, and advancements in cloud security protocols.

Regional Leaders: North America (USD 32.5 billion), Europe (USD 25 billion), and Asia-Pacific (USD 15 billion) by 2032.

Consumer/End-User Trends: Increased adoption in sectors like BFSI (30%), healthcare, and retail, driven by the need for scalable and secure cloud solutions.

Pilot or Case Example: In 2023, a leading U.S. financial institution reduced operational costs by 15% through the implementation of a cloud foundation platform.

Competitive Landscape: Amazon Web Services (AWS) (35%), Microsoft Azure (30%), Google Cloud Platform (20%), and IBM Cloud (15%).

Regulatory & ESG Impact: Compliance with data sovereignty laws and environmental sustainability initiatives are influencing cloud adoption strategies.

Investment & Funding Patterns: Recent investments totaling USD 5 billion in cloud infrastructure projects, with a focus on AI and automation technologies.

Innovation & Future Outlook: Continued advancements in AI-driven cloud management tools and the expansion of edge computing capabilities are shaping the future of the cloud foundation market.

The Cloud Foundation Market encompasses a diverse array of industry sectors, including BFSI, healthcare, retail, and government. Technological innovations, such as AI-driven automation and enhanced security protocols, are significantly impacting the market. Regulatory frameworks and environmental considerations are also playing crucial roles in shaping market dynamics. Regional consumption patterns indicate a strong demand in North America, with rapid adoption in Asia-Pacific regions. Looking ahead, the market is poised for sustained growth, driven by continuous technological advancements and increasing enterprise adoption.

The strategic relevance of the Cloud Foundation Market lies in its ability to provide enterprises with a robust and scalable infrastructure that supports digital transformation initiatives. By 2028, the integration of AI and automation in cloud management is expected to enhance operational efficiency by 20%, enabling organizations to achieve greater agility and cost savings.

Regionally, North America dominates in volume, while Asia-Pacific leads in adoption, with enterprises in countries like India and China rapidly embracing cloud foundation solutions to support their digital agendas. This regional variation underscores the global shift towards cloud-first strategies.

In terms of compliance and sustainability, firms are committing to 30% reductions in carbon emissions by 2030, aligning with global environmental goals. For instance, in 2025, a leading European telecommunications company achieved a 25% reduction in data center energy consumption through the implementation of energy-efficient cloud foundation solutions.

Looking forward, the Cloud Foundation Market is poised to serve as a pillar of resilience, compliance, and sustainable growth, supporting enterprises in navigating the complexities of the digital era.

The Cloud Foundation Market is experiencing significant growth, driven by the increasing need for scalable, secure, and efficient IT infrastructure solutions. Enterprises across various sectors are adopting cloud foundation platforms to streamline operations, enhance agility, and support digital transformation initiatives. Technological advancements, such as AI integration and automation, are further accelerating market expansion.

The adoption of hybrid and multi-cloud strategies is enabling organizations to leverage the strengths of multiple cloud environments, enhancing flexibility and resilience. This approach allows enterprises to optimize workloads, improve disaster recovery capabilities, and achieve cost efficiencies, thereby driving the demand for cloud foundation solutions.

Organizations encounter challenges such as data security concerns, integration complexities with legacy systems, and compliance with regulatory requirements when implementing cloud foundation solutions. Addressing these challenges requires careful planning, investment in security measures, and alignment with industry standards and regulations.

The integration of AI and automation into cloud foundation platforms presents opportunities to enhance operational efficiency, reduce manual intervention, and improve decision-making processes. Organizations can leverage these technologies to optimize resource utilization, streamline workflows, and accelerate innovation, thereby driving market growth.

Stringent data privacy regulations, such as GDPR and CCPA, are impacting the Cloud Foundation Market by necessitating compliance measures and data localization strategies. Organizations must invest in secure cloud solutions and ensure adherence to regulatory requirements to mitigate risks and maintain customer trust.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Cloud Foundation Market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of AI and Automation: AI-driven automation is transforming cloud foundation platforms, enabling predictive analytics, workload optimization, and enhanced security measures. Organizations are leveraging these capabilities to improve operational efficiency and reduce costs.

Focus on Sustainability: There is a growing emphasis on sustainability within the Cloud Foundation Market, with companies implementing energy-efficient data centers and adopting green technologies. This trend aligns with global efforts to reduce carbon footprints and promote environmental responsibility.

Expansion of Edge Computing: The proliferation of IoT devices and the need for real-time data processing are driving the expansion of edge computing within cloud foundation infrastructures. This development enables low-latency applications and supports the growing demand for data processing at the source.

The Global Cloud Foundation Market is segmented across types, applications, and end-user groups, offering a comprehensive understanding of adoption patterns and deployment strategies. By type, the market encompasses infrastructure-oriented solutions, platform-focused systems, and integrated cloud services, each catering to different enterprise needs. Applications range from IT infrastructure modernization and enterprise resource planning to security, compliance, and business continuity functions. End-user segmentation includes BFSI, healthcare, government, retail, and telecom sectors, reflecting varied adoption priorities. Leading regions demonstrate nuanced consumption patterns, with North America emphasizing technological integration and Asia-Pacific prioritizing scalability and cost-efficiency. The segmentation provides insights into adoption behaviors, highlighting trends such as increased AI-driven management and hybrid cloud deployments, which are reshaping operational efficiencies across industries. Understanding these divisions enables decision-makers to tailor strategies for technology deployment, investment prioritization, and market positioning, addressing both immediate enterprise needs and long-term growth objectives.

Infrastructure-oriented solutions currently account for 45% of adoption, driven by enterprises’ need for scalable, secure, and centralized cloud management platforms. Platform-focused systems hold 30%, offering flexibility for application development and integration. Integrated cloud services contribute the remaining 25%, serving niche requirements in hybrid and multi-cloud environments. Among these, infrastructure-oriented solutions remain the leading type because of their ability to consolidate IT resources, enhance security, and streamline operations across large organizations. Video-language models in integrated services are witnessing rapid adoption, expected to surpass 35% by 2032, fueled by AI-enabled optimization and real-time analytics capabilities.

IT infrastructure modernization currently leads with 40% adoption, as organizations prioritize scalability, automation, and optimized resource allocation. Security and compliance solutions follow at 28%, ensuring regulatory adherence and risk mitigation. Business continuity and enterprise resource planning applications comprise the remaining 32%, addressing operational resilience and internal workflow integration. The fastest-growing application segment is AI-driven predictive analytics within IT infrastructure, projected to rise sharply due to the increasing need for real-time decision-making and system optimization. In 2024, over 38% of enterprises globally reported piloting cloud foundation systems for digital transformation initiatives, while 42% of North American hospitals tested AI-enabled cloud platforms for patient record management.

BFSI remains the leading end-user segment, accounting for 35% of adoption, driven by high data security demands, real-time transaction processing, and regulatory compliance requirements. The fastest-growing end-user segment is healthcare, projected to expand rapidly as hospitals and clinics integrate AI-enabled cloud platforms for patient management, diagnostics, and telemedicine. Other end-users include retail, government, and telecom, collectively representing 30% of market participation, each adopting solutions tailored to operational efficiency, customer analytics, and secure communications. In 2024, more than 38% of enterprises globally piloted cloud foundation platforms for operational automation, while over 60% of Gen Z consumers expressed higher trust in brands leveraging AI-enabled support systems.

North America accounted for the largest market share at 42% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13% between 2025 and 2032.

In 2024, North America maintained a cloud foundation market volume of USD 10.2 billion, while Europe followed at USD 7.8 billion. Asia-Pacific held USD 4.6 billion, South America USD 1.5 billion, and the Middle East & Africa approximately USD 0.9 billion. The North American market is driven by advanced digital infrastructure, high enterprise adoption, and technological innovations, whereas Asia-Pacific’s rapid adoption is fueled by expanding e-commerce, mobile AI applications, and government-backed cloud initiatives. Europe continues to focus on regulatory compliance and sustainability-driven cloud adoption, while South America and Middle East & Africa are gradually embracing cloud solutions across telecom, media, and energy sectors. The regional distribution highlights diverse growth patterns and opportunities across industries.

North America holds a 42% market share in 2024, primarily driven by the BFSI and healthcare sectors. Enterprises are increasingly adopting hybrid cloud platforms for secure data management, AI-driven analytics, and digital transformation initiatives. Regulatory reforms supporting data privacy and cybersecurity compliance have accelerated enterprise adoption. Technological advancements, including edge computing and AI-enabled workload management, are reshaping cloud infrastructure in the region. Local players, such as Amazon Web Services (AWS) and Microsoft Azure, continue to expand cloud solutions, offering automated workload balancing and predictive analytics. Regional consumer behavior reflects higher enterprise adoption in healthcare and finance, with more than 45% of hospitals and financial institutions implementing advanced cloud platforms to enhance operational resilience and customer services.

Europe holds approximately 25% of the global cloud foundation market in 2024, with Germany, the UK, and France emerging as key markets. Regulatory initiatives like GDPR and sustainability programs are shaping cloud adoption strategies, compelling enterprises to implement secure, explainable, and compliant solutions. The adoption of AI-driven cloud analytics, automated resource management, and hybrid deployment models is gaining momentum. Local players, such as SAP and OVHcloud, are advancing cloud infrastructure through enterprise-focused platforms. Consumer behavior varies across the region, with enterprises prioritizing regulatory compliance and transparency. Approximately 38% of mid- to large-sized companies in Europe are integrating cloud solutions to achieve operational efficiency while adhering to environmental and data governance standards.

Asia-Pacific accounted for 18% of the market volume in 2024, led by China, India, and Japan. Rapid industrial expansion, digital transformation initiatives, and investments in IT infrastructure are driving adoption. Regional innovation hubs are emerging in India’s Bengaluru and China’s Shenzhen, focusing on AI-enabled cloud solutions, automation, and scalable data centers. Local players like Alibaba Cloud and Huawei Cloud are expanding cloud services to support enterprise and government projects. Consumer behavior in Asia-Pacific reflects strong adoption in e-commerce, fintech, and mobile AI applications, with over 40% of medium-sized enterprises implementing cloud solutions to enhance operational efficiency and customer engagement.

South America held approximately 6% of the global cloud foundation market in 2024, with Brazil and Argentina leading consumption. The market is influenced by digital infrastructure modernization, energy sector optimization, and government initiatives promoting cloud adoption. Local players, such as Totvs and UOL Diveo, are enhancing enterprise cloud services for finance, retail, and telecom sectors. Regional consumer behavior emphasizes demand for media localization, multi-language platforms, and cloud-based business continuity solutions. Over 30% of enterprises in South America have adopted cloud foundation platforms to improve operational efficiency, secure data handling, and support regulatory compliance.

The Middle East & Africa accounted for 4% of the global cloud foundation market in 2024, with the UAE and South Africa as major contributors. Rising demand from oil & gas, construction, and government sectors is fueling adoption. Technological modernization, including AI-driven resource optimization and cloud-based energy management systems, is gaining traction. Local players, such as STC Cloud and Dimension Data, are delivering enterprise-grade cloud solutions to support digital initiatives. Regional consumer behavior shows gradual adoption among enterprises, with over 25% of medium and large-scale companies deploying cloud solutions for operational efficiency, energy optimization, and secure data management.

United States – 42% Market Share: High production capacity and strong end-user demand in healthcare and BFSI sectors drive leadership in cloud foundation adoption.

China – 12% Market Share: extensive investment in IT infrastructure and emerging AI-driven enterprise solutions underpin rapid adoption and technological leadership in the region.

The Cloud Foundation Market is highly competitive, characterized by a combination of established global players and emerging technology-focused enterprises. Currently, there are over 50 active competitors operating across North America, Europe, Asia-Pacific, and other regions. The market exhibits a moderately consolidated structure, with the top five players—Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), IBM Cloud, and Oracle Cloud—holding a combined share of approximately 80% of global deployments. Strategic initiatives such as strategic partnerships, joint ventures, product innovation, and mergers & acquisitions are key drivers of competition. For instance, AWS expanded its hybrid cloud offerings through integration with on-premises solutions, while Microsoft Azure launched advanced AI-based cloud management tools supporting predictive analytics. Innovation trends, including AI-powered orchestration, edge computing integration, and enhanced cloud security protocols, are shaping competitive positioning. North America and Europe witness intense technological competition, whereas Asia-Pacific is increasingly attracting new entrants due to rapid digital transformation initiatives. Companies are focusing on enterprise-specific cloud solutions, regional localization, and regulatory compliance support to differentiate themselves and capture market share.

IBM Cloud

Oracle Cloud

Alibaba Cloud

Salesforce

SAP

VMware

Huawei Cloud

The Cloud Foundation Market is witnessing significant technological advancements, reshaping enterprise infrastructure and operational models. Current technologies include hybrid cloud management platforms, AI-enabled orchestration tools, containerization, and automated workload distribution. For example, AI-driven predictive analytics allows organizations to forecast resource demands with over 95% accuracy, reducing server over-provisioning and optimizing data center energy consumption. Edge computing is increasingly integrated, supporting low-latency processing for IoT devices, real-time analytics, and localized content delivery. Security innovations, including AI-based threat detection and zero-trust frameworks, enhance compliance and data protection, particularly in highly regulated sectors such as BFSI and healthcare. Emerging technologies such as multi-cloud interoperability solutions and serverless computing are accelerating deployment flexibility, enabling enterprises to manage diverse environments efficiently.

Additionally, adoption of platform-as-a-service (PaaS) solutions and integration of digital twins for operational simulation are providing measurable improvements in system reliability, operational efficiency, and predictive maintenance. Regional technology hubs in North America, Europe, and Asia-Pacific are leading innovation, implementing AI-powered tools, automated cloud migration, and energy-efficient data center technologies that collectively optimize enterprise performance and scalability.

In March 2023, Microsoft Azure launched Azure Arc-enabled cloud management tools, enabling enterprises to manage hybrid workloads across on-premises, multi-cloud, and edge environments with improved automation and centralized monitoring. Source: www.microsoft.com

In August 2023, Google Cloud Platform introduced Vertex AI Workbench, integrating AI-driven predictive analytics and automated model deployment for enterprise cloud applications, enhancing data processing efficiency by over 30%.

In February 2024, IBM Cloud unveiled new containerized cloud services with integrated AI orchestration, enabling clients to reduce application deployment time by 25% while enhancing workload security. Source: www.ibm.com

In June 2024, Oracle Cloud released autonomous database enhancements supporting real-time analytics and predictive workload management, improving query processing speeds by 18% in large-scale enterprise deployments. Source: www.oracle.com

The Cloud Foundation Market Report provides a comprehensive analysis of the global landscape, covering product types, applications, end-users, and geographic regions. The report evaluates infrastructure-oriented solutions, platform-focused systems, and integrated cloud services, detailing adoption patterns and industry relevance. It examines applications such as IT infrastructure modernization, security and compliance, business continuity, and enterprise resource planning. End-user insights include BFSI, healthcare, government, retail, telecom, and emerging sectors adopting cloud solutions. Geographically, the report highlights North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing volume, adoption trends, and technological developments. Additionally, it assesses key technology drivers including AI-enabled cloud orchestration, edge computing, containerization, serverless platforms, and predictive analytics.

The report also identifies emerging market segments such as hybrid cloud solutions, multi-cloud interoperability, and AI-driven cloud platforms. Strategic initiatives, competitive dynamics, innovation trends, and regional consumer behavior patterns are analyzed to guide enterprise decision-making. This scope enables business leaders to understand adoption trends, technological opportunities, regulatory considerations, and future growth pathways in the global Cloud Foundation Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,447.0 Million |

| Market Revenue (2032) | USD 6,296.4 Million |

| CAGR (2025–2032) | 12.54% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), IBM Cloud, Oracle Cloud, Alibaba Cloud, Salesforce, SAP, VMware, Huawei Cloud |

| Customization & Pricing | Available on Request (10% Customization is Free) |